Credo Partners with TensorWave to Enhance AI Cluster Performance

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 25 2026

0mins

Source: Newsfilter

- Collaboration Background: Credo Technology Group has partnered with AMD-exclusive AI cloud provider TensorWave to deploy Credo's ZeroFlap (ZF) family of Active Electrical Cables (AECs) and optics across TensorWave's next-generation AI cluster infrastructure, aiming to accelerate the time from physical deployment to first token.

- Technical Advantages: Credo's ZeroFlap AECs and optics provide reliability up to 1,000 times better than legacy interconnect solutions and integrate with Credo's PILOT telemetry management system, ensuring high network availability and increased tokens delivered per hour.

- Market Demand: As AI cluster sizes continue to grow, network reliability becomes a critical factor affecting time-to-revenue and sustained uptime, with Credo's solutions helping TensorWave reduce deployment friction and accelerate time to first token while meeting customer demands.

- Strategic Significance: Backed by over $166 million in funding, TensorWave is focused on building high-performance AI infrastructure, and Credo's technology will further enhance its competitiveness in the global market, ensuring customers can confidently train and deploy models at scale.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CRDO?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CRDO

Wall Street analysts forecast CRDO stock price to fall

13 Analyst Rating

12 Buy

1 Hold

0 Sell

Strong Buy

Current: 229.000

Low

170.00

Averages

221.82

High

260.00

Current: 229.000

Low

170.00

Averages

221.82

High

260.00

About CRDO

Credo Technology Group Holding Ltd is a Cayman Islands-based holding company. The Company delivers high-speed solutions to break bandwidth barriers on every wired connection in the data infrastructure market. It provides high-speed connectivity solutions that deliver improved power efficiency as data rates and corresponding bandwidth requirements increase exponentially throughout the data infrastructure market. Its connectivity solutions are optimized for optical and electrical Ethernet applications, including the emerging 100 gigabits per second (G), 200G, 400G, 800G and the emerging 1.6 terabits per second (T) port markets. Its products are based on its Serializer/Deserializer (SerDes) and Digital Signal Processor (DSP) technologies. Its product families include integrated circuits (ICs) for the optical and line card markets, active electrical cables (AECs) and SerDes Chiplets. The Company’s intellectual property (IP) solutions consist primarily of SerDes IP licensing.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Strong Start for June Stocks, Focus on Three Tech Giants

- Profitability Highlight: Micron Technology (MU) boasts a 41.5% net profit margin over the past 12 months, with an expected earnings growth rate of 619.8% this year, showcasing its strong competitive position in the memory and storage market, thus attracting investor interest for future growth potential.

- High-Speed Connectivity Solutions: Credo Technology (CRDO) offers high-speed connectivity solutions for Ethernet and PCIe applications, achieving a 31.8% net profit margin over the past year, with an anticipated earnings growth rate of 371.4% this year, indicating significant profitability in the rapidly evolving tech market.

- Automated Testing Systems: Teradyne (TER) excels in developing automated test systems and robotics solutions, achieving a 22.6% net profit margin over the past year, with an expected earnings growth rate of 79% this year, reflecting strong growth potential in the automation sector.

- Investment Strategy Effectiveness: Zacks' stock-picking strategies have outperformed the S&P's average gain of 7.7% per year since 2000, with average gains of 48.4%, 50.2%, and 56.7%, demonstrating their effectiveness and attractiveness in the market.

See More

Dow Jones Rises Amid Ongoing U.S.-Iran Talks; Celestica Sees Major Movement

- Dow Jones Rises: The Dow Jones index climbed on Tuesday amid ongoing U.S.-Iran talks, reflecting market optimism regarding diplomatic progress, which could enhance investor confidence and drive further stock market gains.

- Celestica's Major Movement: Celestica's stock experienced significant fluctuations, potentially linked to its latest earnings report or market dynamics, which may attract short-term traders and impact its shareholder structure.

- Nvidia's Decline: Nvidia's stock fell, likely due to market concerns about its future performance, especially in the context of increasing competition, which could affect its market share and investor confidence.

- Market Sentiment Shifts: Overall market sentiment fluctuated due to international political dynamics, prompting investors to monitor the progress of negotiations in the coming days to assess potential impacts on the stock market.

See More

Solstice and Core Scientific See Active Options Trading

- Solstice Options Volume: Solstice Advanced Materials Inc (Ticker: SOLS) saw options trading volume of 18,645 contracts today, representing approximately 1.9 million shares, which is about 79.3% of its average daily trading volume of 2.4 million shares over the past month, indicating heightened market interest in its future performance.

- High Volume Contracts: The $65 strike put option for SOLS was particularly active, with 15,892 contracts traded today, equating to approximately 1.6 million shares, reflecting investor expectations regarding potential downside risks for the stock.

- Core Scientific Options Activity: Concurrently, Core Scientific Inc (Ticker: CORZ) recorded options trading volume of 113,081 contracts, representing about 11.3 million shares, which accounts for 68.8% of its average daily trading volume of 16.4 million shares over the past month, showcasing strong market interest in its stock.

- Key Contract Insights: Among CORZ options, the $40 strike call option saw a trading volume of 25,119 contracts, approximately 2.5 million shares, indicating investor confidence in the stock's potential upside, which may influence its short-term price movements.

See More

Analysis of Stock Price Movements for Multiple Companies

- Generac Contract Signing: Generac's stock rose nearly 6% after announcing a backup power supply agreement with a leading hyperscale data center operator, with CEO Aaron Jagdfeld stating that this positions the company at the core of supporting essential services and the digital economy.

- USA Rare Earth Investment Plan: USA Rare Earth shares gained close to 5% following the announcement of a $1.2 billion investment to build a magnet manufacturing and refined metals facility in South Carolina, which is expected to enhance the company's competitiveness and market share in the rare earth sector.

- Intuit Stock Decline: Intuit's stock dropped nearly 9% after Goldman Sachs downgraded its rating from hold to sell, with analyst Gabriela Borges projecting a 22% decline from Monday's close, highlighting the heightened competition in the tax sector as a primary concern.

- Shake Shack Earnings Outlook Cut: Shake Shack's stock fell 10% after it lowered its full-year earnings outlook and second-quarter revenue guidance, citing the impact of current macroeconomic uncertainty and competitive landscape on its performance.

See More

Credo Technology Reports Over 150% Revenue Growth in Q4 FY2026

- Significant Revenue Growth: Credo Technology's Q4 FY2026 revenue surged over 150% year-over-year, with expectations of an 80% increase for the entirety of FY2027, indicating strong market demand and business expansion potential.

- Optical Product Contribution: Management noted that approximately half of the revenue growth in FY2027 will come from the optical portfolio, with the other half from the existing copper portfolio, particularly AECs, highlighting the effectiveness of the company's strategic focus on optical technologies.

- Analyst Optimism: Needham raised its FY2027 revenue estimate from $2.35 billion to $2.45 billion and reiterated its Buy rating, increasing the price target from $220 to $275, reflecting strong market confidence in Credo's future growth trajectory.

- Operating Expense Growth: Although operating expenses are expected to grow approximately 50% year-over-year, this increase is below the revenue growth rate, with management projecting a net margin of around 50%, demonstrating the company's effectiveness in cost control.

See More

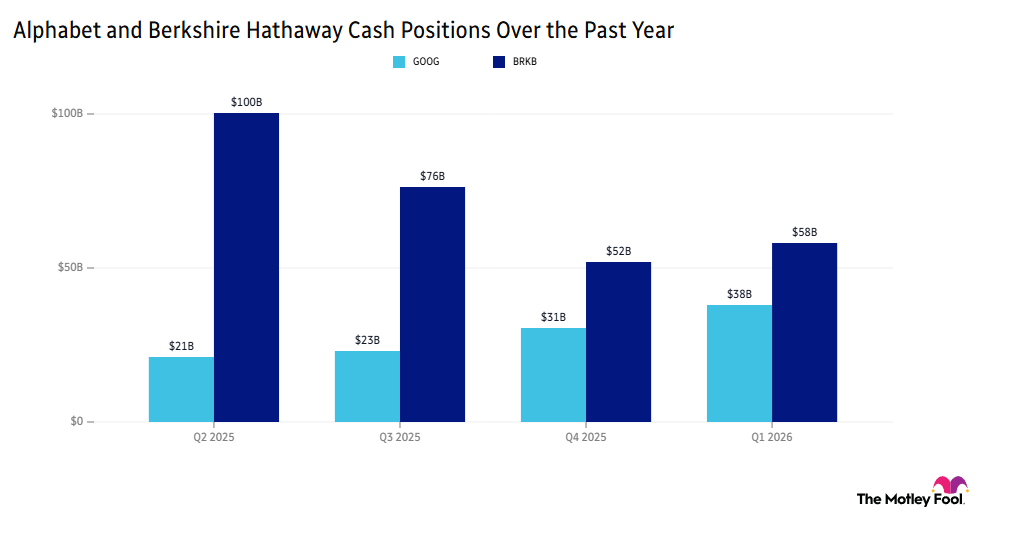

Alphabet's $80 Billion AI Investment Plan

- Historic Stock Sale: Alphabet confirmed it will sell $80 billion in stock, including a $10 billion stake to Berkshire Hathaway, to raise capital for AI compute infrastructure to meet unprecedented customer demand, although its stock fell about 2.5% ahead of the opening bell.

- Berkshire's Increased Stake: Berkshire's current holding in Alphabet is valued at around $20 billion, and this additional $10 billion investment is likely to make it the third-largest portfolio holding, behind Apple and American Express, reflecting confidence in Alphabet's growth potential.

- Strong HPE Performance: Hewlett Packard Enterprise's quarterly results exceeded expectations, with cloud and AI revenue driving its stock up over 25% in pre-market trading, and management now expects revenue growth of 29%-33% for the full year, indicating robust market demand.

- Space Stock Volatility: Ahead of the SpaceX IPO, space-related stocks like Rocket Lab and Redwire fell 14.7% and 15.83% respectively, as investors opted to reduce exposure due to concerns over short-term volatility, despite Rocket Lab outperforming the S&P 500 by 204% since July 2025.

See More

Strong Start for June Stocks, Focus on Three Tech Giants

- Profitability Highlight: Micron Technology (MU) boasts a 41.5% net profit margin over the past 12 months, with an expected earnings growth rate of 619.8% this year, showcasing its strong competitive position in the memory and storage market, thus attracting investor interest for future growth potential.

- High-Speed Connectivity Solutions: Credo Technology (CRDO) offers high-speed connectivity solutions for Ethernet and PCIe applications, achieving a 31.8% net profit margin over the past year, with an anticipated earnings growth rate of 371.4% this year, indicating significant profitability in the rapidly evolving tech market.

- Automated Testing Systems: Teradyne (TER) excels in developing automated test systems and robotics solutions, achieving a 22.6% net profit margin over the past year, with an expected earnings growth rate of 79% this year, reflecting strong growth potential in the automation sector.

- Investment Strategy Effectiveness: Zacks' stock-picking strategies have outperformed the S&P's average gain of 7.7% per year since 2000, with average gains of 48.4%, 50.2%, and 56.7%, demonstrating their effectiveness and attractiveness in the market.

See More

Dow Jones Rises Amid Ongoing U.S.-Iran Talks; Celestica Sees Major Movement

- Dow Jones Rises: The Dow Jones index climbed on Tuesday amid ongoing U.S.-Iran talks, reflecting market optimism regarding diplomatic progress, which could enhance investor confidence and drive further stock market gains.

- Celestica's Major Movement: Celestica's stock experienced significant fluctuations, potentially linked to its latest earnings report or market dynamics, which may attract short-term traders and impact its shareholder structure.

- Nvidia's Decline: Nvidia's stock fell, likely due to market concerns about its future performance, especially in the context of increasing competition, which could affect its market share and investor confidence.

- Market Sentiment Shifts: Overall market sentiment fluctuated due to international political dynamics, prompting investors to monitor the progress of negotiations in the coming days to assess potential impacts on the stock market.

See More

Solstice and Core Scientific See Active Options Trading

- Solstice Options Volume: Solstice Advanced Materials Inc (Ticker: SOLS) saw options trading volume of 18,645 contracts today, representing approximately 1.9 million shares, which is about 79.3% of its average daily trading volume of 2.4 million shares over the past month, indicating heightened market interest in its future performance.

- High Volume Contracts: The $65 strike put option for SOLS was particularly active, with 15,892 contracts traded today, equating to approximately 1.6 million shares, reflecting investor expectations regarding potential downside risks for the stock.

- Core Scientific Options Activity: Concurrently, Core Scientific Inc (Ticker: CORZ) recorded options trading volume of 113,081 contracts, representing about 11.3 million shares, which accounts for 68.8% of its average daily trading volume of 16.4 million shares over the past month, showcasing strong market interest in its stock.

- Key Contract Insights: Among CORZ options, the $40 strike call option saw a trading volume of 25,119 contracts, approximately 2.5 million shares, indicating investor confidence in the stock's potential upside, which may influence its short-term price movements.

See More

Analysis of Stock Price Movements for Multiple Companies

- Generac Contract Signing: Generac's stock rose nearly 6% after announcing a backup power supply agreement with a leading hyperscale data center operator, with CEO Aaron Jagdfeld stating that this positions the company at the core of supporting essential services and the digital economy.

- USA Rare Earth Investment Plan: USA Rare Earth shares gained close to 5% following the announcement of a $1.2 billion investment to build a magnet manufacturing and refined metals facility in South Carolina, which is expected to enhance the company's competitiveness and market share in the rare earth sector.

- Intuit Stock Decline: Intuit's stock dropped nearly 9% after Goldman Sachs downgraded its rating from hold to sell, with analyst Gabriela Borges projecting a 22% decline from Monday's close, highlighting the heightened competition in the tax sector as a primary concern.

- Shake Shack Earnings Outlook Cut: Shake Shack's stock fell 10% after it lowered its full-year earnings outlook and second-quarter revenue guidance, citing the impact of current macroeconomic uncertainty and competitive landscape on its performance.

See More

Credo Technology Reports Over 150% Revenue Growth in Q4 FY2026

- Significant Revenue Growth: Credo Technology's Q4 FY2026 revenue surged over 150% year-over-year, with expectations of an 80% increase for the entirety of FY2027, indicating strong market demand and business expansion potential.

- Optical Product Contribution: Management noted that approximately half of the revenue growth in FY2027 will come from the optical portfolio, with the other half from the existing copper portfolio, particularly AECs, highlighting the effectiveness of the company's strategic focus on optical technologies.

- Analyst Optimism: Needham raised its FY2027 revenue estimate from $2.35 billion to $2.45 billion and reiterated its Buy rating, increasing the price target from $220 to $275, reflecting strong market confidence in Credo's future growth trajectory.

- Operating Expense Growth: Although operating expenses are expected to grow approximately 50% year-over-year, this increase is below the revenue growth rate, with management projecting a net margin of around 50%, demonstrating the company's effectiveness in cost control.

See More

Alphabet's $80 Billion AI Investment Plan

- Historic Stock Sale: Alphabet confirmed it will sell $80 billion in stock, including a $10 billion stake to Berkshire Hathaway, to raise capital for AI compute infrastructure to meet unprecedented customer demand, although its stock fell about 2.5% ahead of the opening bell.

- Berkshire's Increased Stake: Berkshire's current holding in Alphabet is valued at around $20 billion, and this additional $10 billion investment is likely to make it the third-largest portfolio holding, behind Apple and American Express, reflecting confidence in Alphabet's growth potential.

- Strong HPE Performance: Hewlett Packard Enterprise's quarterly results exceeded expectations, with cloud and AI revenue driving its stock up over 25% in pre-market trading, and management now expects revenue growth of 29%-33% for the full year, indicating robust market demand.

- Space Stock Volatility: Ahead of the SpaceX IPO, space-related stocks like Rocket Lab and Redwire fell 14.7% and 15.83% respectively, as investors opted to reduce exposure due to concerns over short-term volatility, despite Rocket Lab outperforming the S&P 500 by 204% since July 2025.

See More