Baidu's Q1 Earnings Expected to Decline

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy BIDU?

Source: seekingalpha

- Earnings Decline Expected: Baidu is projected to report Q1 EPS of $1.68, reflecting a 34.1% year-over-year decline, despite a 4% revenue increase to $4.65 billion, indicating significant challenges to profitability amid a prolonged slump in its core advertising business.

- Cloud Services Growth: The company reported a 143% year-over-year surge in subscription revenue from its AI infrastructure in Q4, highlighting Baidu's reliance on cloud and AI services to offset declining advertising revenue and achieve more predictable income streams.

- AI Marketing Revenue Scrutiny: AI-linked marketing revenue reached 2.7 billion yuan in Q4, more than doubling from the previous year, with analysts noting this growth as a key driver for Baidu amid headwinds in its core search business.

- Kunlunxin IPO Plans: Baidu is pursuing a dual listing for its AI chip subsidiary Kunlunxin on the Hong Kong Stock Exchange and Shanghai's STAR Market, targeting a valuation of around 100 billion yuan (approximately $14.7 billion), which could shift capital expenditure burdens to public investors while accelerating growth.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BIDU?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BIDU

Wall Street analysts forecast BIDU stock price to rise

13 Analyst Rating

11 Buy

2 Hold

0 Sell

Strong Buy

Current: 137.710

Low

140.00

Averages

170.39

High

215.00

Current: 137.710

Low

140.00

Averages

170.39

High

215.00

About BIDU

Baidu Inc is a Chinese language Internet search provider. The Company operates its businesses through two segments, Baidu Core segment and iQIYI segment. Baidu Core segment mainly provides search-based, feed-based, and other online marketing services, as well as products and services from the Company’s new artificial intelligence (AI) initiatives, such as display advertisement and based on performance criteria other than cost-per-click, cloud services, smart devices and services, non-marketing consumer-facing services such as membership, and intelligent driving. iQIYI segment produces, aggregates and distributes a wide variety of professionally produced content, as well as a broad spectrum of other video content, in a variety of formats, including a variety of products and services encompassing online video, online games, online literature, comics and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Baidu Q1 2026 Earnings Call Insights Highlight AI Growth

- Revenue Growth Resumes: Baidu reported total revenue of RMB 26 billion in Q1, reflecting a 2% year-over-year increase, marking a return to growth and indicating a gradual recovery in market demand and business stability.

- Core Business Strength: Revenue from AI-powered core business reached RMB 13.6 billion, up 49% year-over-year, accounting for 52% of Baidu's overall revenue for the first time, demonstrating significant progress in the company's strategic focus on AI.

- Exceptional Cloud Performance: AI Cloud Infrastructure revenue grew 79% year-over-year, with GPU Cloud revenue accelerating to 184%, highlighting strong enterprise demand for AI infrastructure and Baidu's competitive edge in this sector.

- Expansion in Autonomous Driving: Baidu delivered 3.2 million fully driverless rides in Q1, sustaining triple-digit year-over-year growth, while preparations for open road testing in Europe are underway, showcasing the company's potential for international market expansion.

See More

Market Volatility and AI Stock Performance

- AI Stock Volatility: At the start of the week, the S&P 500 index fell, with AI-related stocks under pressure, indicating ongoing rotations in AI trades and reflecting investor uncertainty about future growth prospects.

- Oil Price Fluctuations: On Monday morning, oil prices initially dropped before rebounding due to uncertainty surrounding a deal between the U.S. and Iran regarding the Strait of Hormuz, which could impact the profitability of energy-related companies.

- CrowdStrike and Palo Alto New Highs: Despite overall market weakness, CrowdStrike and Palo Alto Networks reached all-time highs, with approximately 30% gains, demonstrating the potential for AI to accelerate their businesses, prompting us to raise price targets to $650 and $255, respectively.

- Home Depot Earnings Expectations: Home Depot's quarterly results are anticipated to be negatively impacted by high mortgage rates delaying the home improvement recovery, which may adversely affect its stock price, warranting investor attention.

See More

Baidu's AI Surge Amidst Transformation Challenges

- Revenue Trends: Baidu's total revenue fell 1% year-over-year in Q1, yet its general business revenue rose 2%, indicating that despite overall weakness, some segments are performing well, reflecting the challenges and opportunities in the company's transformation journey.

- AI Business Growth: Baidu's AI segment grew 49% over the past year, with its AI cloud infrastructure skyrocketing by 79%, demonstrating the company's successful pivot towards emerging technologies to drive future growth.

- Autonomous Driving Leadership: Baidu's Apollo Go remains a leader in autonomous driving, having completed 22 million rides, showcasing its strong performance in the robotaxi market, with expansions into South Korea and the UAE enhancing its competitive edge.

- Market Valuation: Despite challenges in its traditional advertising business, Baidu's AI-native marketing revenue increased by 36% year-over-year, and its forward P/E ratio is in the high teens, indicating market recognition of its growth potential, making it an attractive investment if profitability can be maintained.

See More

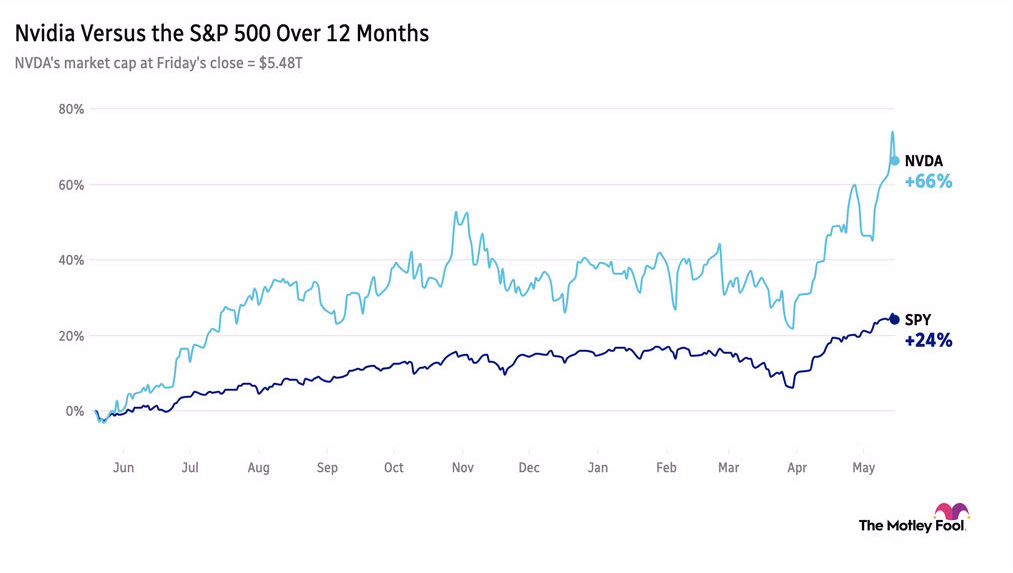

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Baidu Q1 Earnings Beat Expectations with Significant AI Growth

- Revenue and Earnings Beat: Baidu reported total revenue of RMB 32.1 billion for Q1, with adjusted earnings per ADS at RMB 12.06, both exceeding market expectations and demonstrating the company's robust financial performance during its transition.

- Strong AI Business Growth: Revenue from Baidu's core AI business reached RMB 13.6 billion, soaring 79% year-over-year, indicating that AI has become the primary revenue driver and is expected to further propel future growth.

- Expansion of Autonomous Services: Baidu's Apollo Go autonomous ride-hailing service provided over 3.2 million rides in Q1, marking a 120% increase year-over-year, showcasing rapid market expansion and growing user acceptance.

- Investor Sentiment Turns Bullish: Following the release of strong Q1 results, investor sentiment on social media shifted to 'extremely bullish', reflecting confidence in the company's future growth potential.

See More

Baidu Q1 Earnings Preview: Kunlunxin IPO Distorts Valuation Metrics

- Earnings Expectations: Baidu's anticipated non-GAAP EPS of $1.75 exceeds market expectations by $0.07, indicating stable profitability, while revenue of $4.65 billion aligns with forecasts, reflecting cautious market sentiment regarding its growth potential.

- Structural Slowdown: Baidu's Q4 results reaffirm a trend of structural slowdown, yet the company is pivoting towards AI infrastructure and robotaxi services, aiming to leverage emerging technologies for future growth despite potential short-term challenges.

- Kunlunxin IPO Impact: The upcoming IPO of Kunlunxin is expected to distort Baidu's valuation metrics, with market focus on this event likely causing stock price fluctuations, reflecting divergent investor perspectives on the company's strategic direction.

- AI Cloud Growth Potential: The growth potential of Baidu's AI cloud services is a key focus for Q1 earnings, and despite an uncertain market environment, investments in this area could provide new revenue streams and enhance its competitive position.

See More

Baidu Q1 2026 Earnings Call Insights Highlight AI Growth

- Revenue Growth Resumes: Baidu reported total revenue of RMB 26 billion in Q1, reflecting a 2% year-over-year increase, marking a return to growth and indicating a gradual recovery in market demand and business stability.

- Core Business Strength: Revenue from AI-powered core business reached RMB 13.6 billion, up 49% year-over-year, accounting for 52% of Baidu's overall revenue for the first time, demonstrating significant progress in the company's strategic focus on AI.

- Exceptional Cloud Performance: AI Cloud Infrastructure revenue grew 79% year-over-year, with GPU Cloud revenue accelerating to 184%, highlighting strong enterprise demand for AI infrastructure and Baidu's competitive edge in this sector.

- Expansion in Autonomous Driving: Baidu delivered 3.2 million fully driverless rides in Q1, sustaining triple-digit year-over-year growth, while preparations for open road testing in Europe are underway, showcasing the company's potential for international market expansion.

See More

Market Volatility and AI Stock Performance

- AI Stock Volatility: At the start of the week, the S&P 500 index fell, with AI-related stocks under pressure, indicating ongoing rotations in AI trades and reflecting investor uncertainty about future growth prospects.

- Oil Price Fluctuations: On Monday morning, oil prices initially dropped before rebounding due to uncertainty surrounding a deal between the U.S. and Iran regarding the Strait of Hormuz, which could impact the profitability of energy-related companies.

- CrowdStrike and Palo Alto New Highs: Despite overall market weakness, CrowdStrike and Palo Alto Networks reached all-time highs, with approximately 30% gains, demonstrating the potential for AI to accelerate their businesses, prompting us to raise price targets to $650 and $255, respectively.

- Home Depot Earnings Expectations: Home Depot's quarterly results are anticipated to be negatively impacted by high mortgage rates delaying the home improvement recovery, which may adversely affect its stock price, warranting investor attention.

See More

Baidu's AI Surge Amidst Transformation Challenges

- Revenue Trends: Baidu's total revenue fell 1% year-over-year in Q1, yet its general business revenue rose 2%, indicating that despite overall weakness, some segments are performing well, reflecting the challenges and opportunities in the company's transformation journey.

- AI Business Growth: Baidu's AI segment grew 49% over the past year, with its AI cloud infrastructure skyrocketing by 79%, demonstrating the company's successful pivot towards emerging technologies to drive future growth.

- Autonomous Driving Leadership: Baidu's Apollo Go remains a leader in autonomous driving, having completed 22 million rides, showcasing its strong performance in the robotaxi market, with expansions into South Korea and the UAE enhancing its competitive edge.

- Market Valuation: Despite challenges in its traditional advertising business, Baidu's AI-native marketing revenue increased by 36% year-over-year, and its forward P/E ratio is in the high teens, indicating market recognition of its growth potential, making it an attractive investment if profitability can be maintained.

See More

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Baidu Q1 Earnings Beat Expectations with Significant AI Growth

- Revenue and Earnings Beat: Baidu reported total revenue of RMB 32.1 billion for Q1, with adjusted earnings per ADS at RMB 12.06, both exceeding market expectations and demonstrating the company's robust financial performance during its transition.

- Strong AI Business Growth: Revenue from Baidu's core AI business reached RMB 13.6 billion, soaring 79% year-over-year, indicating that AI has become the primary revenue driver and is expected to further propel future growth.

- Expansion of Autonomous Services: Baidu's Apollo Go autonomous ride-hailing service provided over 3.2 million rides in Q1, marking a 120% increase year-over-year, showcasing rapid market expansion and growing user acceptance.

- Investor Sentiment Turns Bullish: Following the release of strong Q1 results, investor sentiment on social media shifted to 'extremely bullish', reflecting confidence in the company's future growth potential.

See More

Baidu Q1 Earnings Preview: Kunlunxin IPO Distorts Valuation Metrics

- Earnings Expectations: Baidu's anticipated non-GAAP EPS of $1.75 exceeds market expectations by $0.07, indicating stable profitability, while revenue of $4.65 billion aligns with forecasts, reflecting cautious market sentiment regarding its growth potential.

- Structural Slowdown: Baidu's Q4 results reaffirm a trend of structural slowdown, yet the company is pivoting towards AI infrastructure and robotaxi services, aiming to leverage emerging technologies for future growth despite potential short-term challenges.

- Kunlunxin IPO Impact: The upcoming IPO of Kunlunxin is expected to distort Baidu's valuation metrics, with market focus on this event likely causing stock price fluctuations, reflecting divergent investor perspectives on the company's strategic direction.

- AI Cloud Growth Potential: The growth potential of Baidu's AI cloud services is a key focus for Q1 earnings, and despite an uncertain market environment, investments in this area could provide new revenue streams and enhance its competitive position.

See More