AI Drives Transformation in Storage Industry

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Should l Buy NVDA?

Source: Yahoo Finance

- Surging Storage Demand: The rapid advancement of AI and generative AI has led to a significant increase in data storage needs, with HDD shipments expected to exceed 450 exabytes by 2026, driving long-term growth and investor interest in the storage industry.

- Strategic Differentiation: Western Digital benefits from execution and pricing discipline for stable growth, while Seagate leverages HAMR technology to enhance storage density, reflecting distinct market positioning as both companies capitalize on AI-driven storage demand.

- Revenue Recovery Trend: HDD revenues are projected to recover above $6 billion per quarter by 2024, with Western Digital's disciplined execution and Seagate's technological advancements providing stronger cash flow and margins for both companies in the market.

- Market Revaluation of Storage Economics: Investors are increasingly recognizing the long-term value of storage economics, as evidenced by the significant outperformance of Seagate and Western Digital stocks against long-term trends, indicating a growing acknowledgment of AI infrastructure demand.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 235.740

Low

200.00

Averages

264.97

High

352.00

Current: 235.740

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Morgan Stanley Optimistic on Nvidia's Earnings Outlook

- Earnings Outlook: Morgan Stanley anticipates Nvidia will achieve earnings of $1.72 per share and revenue of $79.264 billion for the fiscal first quarter, up from previous estimates of $78.25 billion in revenue and $1.69 earnings per share, indicating robust market demand and positive financial performance.

- Price Target Increase: The investment bank raised Nvidia's price target from $260 to $285, implying a 26% upside from Friday's close, reflecting strong confidence in the company's future growth potential.

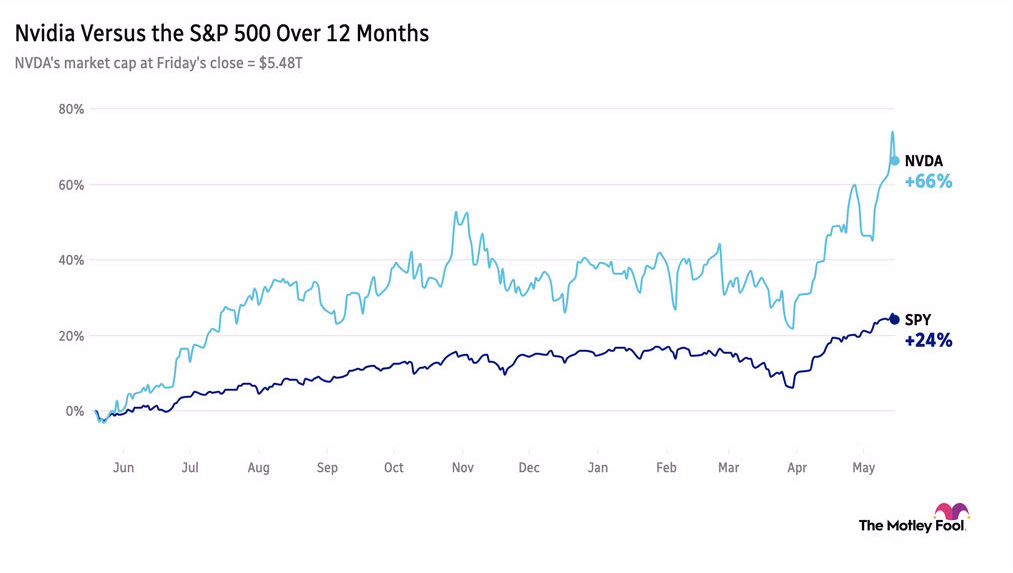

- Strong Market Performance: Nvidia's shares have surged 66% over the past 12 months, significantly outperforming the overall market, underscoring the sustained appeal of artificial intelligence as an investment theme and reinforcing its leadership position in the semiconductor industry.

- Supply Chain Advantage: Analysts noted Nvidia's proactive supply chain management places it in an advantageous position compared to peers, with $95 billion in purchase commitments that can cover much of its shipping plans over the next 18 months, enhancing its competitive edge.

See More

Nvidia's Dominance in the Booming Space Economy

- Market Growth Potential: The global space economy is projected to reach $1.8 trillion by 2035, up from $630 billion in 2023, reflecting a robust annual growth rate of about 9%, indicating strong investment appeal.

- AI Application Outlook: The global AI in space exploration market is expected to grow from $6.2 billion to $110.2 billion by 2035, with a staggering CAGR of 33.4%, presenting significant market opportunities for Nvidia.

- Technological Leadership: Nvidia's launch of space AI computing platforms has positioned it for first-mover advantage, with the latest Rubin GPU module delivering up to 25 times more AI compute power, facilitating next-gen orbital data centers and autonomous space operations.

- Partner Network Expansion: Nvidia's technology is being utilized by several space companies, including Axiom Space and Planet Labs, the latter of which provides detailed Earth imagery daily, showcasing its attractive business model and future profitability potential.

See More

GF Securities Raises Nvidia Price Target to $308 Ahead of Earnings

- Price Target Increase: GF Securities raised Nvidia's price target from $292 to $308, reflecting an optimistic outlook on the company's financial performance ahead of its upcoming earnings report.

- Share Buyback Anticipation: Analyst Jeff Pu noted that with a strong cash position and free cash flow, Nvidia is expected to announce a new share repurchase program during the earnings call, which would further bolster investor confidence.

- Data Center Market Share: Beyond GPUs, Nvidia is anticipated to capture a larger value share of the data center silicon market, supported by Vera CPU and LPX, which will drive long-term growth for the company.

- Earnings Forecast Adjustment: By factoring in higher Blackwell units and average selling prices, Nvidia's EPS estimates for FY27E and FY28E have been revised up by 0% and 13%, respectively, indicating an improvement in the company's profitability for the upcoming fiscal years.

See More

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Nvidia and AMD Stocks Near All-Time Highs

- Stock Performance: As of May 14, 2026, Nvidia and AMD stocks rose by 4.39% and 5.67% respectively, indicating strong market performance and reflecting investor confidence in both companies.

- Valuation Analysis: Despite trading near all-time highs, analysts suggest that these stocks may not be as 'expensive' as perceived, presenting potential buying opportunities for investors.

- Market Outlook: With the increasing demand for artificial intelligence and high-performance computing, the product demand for Nvidia and AMD continues to rise, potentially driving further stock price increases and enhancing investment appeal.

- Investment Recommendation: In the current market environment, although stock prices are high, analysts believe both stocks remain worthy of attention, urging investors to consider their long-term growth potential.

See More

Iren Reports Earnings and Major Tech Deal

- Power Infrastructure Progress: Iren successfully energized its 1.4-gigawatt Sweetwater 1 site ahead of the April 2026 target, demonstrating reliability and speed in large-scale infrastructure construction, which boosts market confidence.

- Acquisition of Mirantis: Iren's $625 million acquisition of Mirantis aims to enhance its software capabilities and attract more customers needing AI infrastructure, leveraging Mirantis's network of over 1,500 enterprise clients to create new business opportunities.

- Strategic Partnership with Nvidia: Iren signed a five-year, $3.4 billion deal with Nvidia to provide infrastructure cloud services using 60 megawatts of capacity at its Childress, Texas facility, expected to drive annual recurring revenue to $3.1 billion, although revenue recognition will take time.

- Increasing Debt Pressure: Following its earnings report, Iren issued $2.6 billion in convertible notes, highlighting ongoing losses and high debt levels in a capital-intensive industry, raising investor concerns about its long-term profitability despite significant potential in AI infrastructure.

See More

Morgan Stanley Optimistic on Nvidia's Earnings Outlook

- Earnings Outlook: Morgan Stanley anticipates Nvidia will achieve earnings of $1.72 per share and revenue of $79.264 billion for the fiscal first quarter, up from previous estimates of $78.25 billion in revenue and $1.69 earnings per share, indicating robust market demand and positive financial performance.

- Price Target Increase: The investment bank raised Nvidia's price target from $260 to $285, implying a 26% upside from Friday's close, reflecting strong confidence in the company's future growth potential.

- Strong Market Performance: Nvidia's shares have surged 66% over the past 12 months, significantly outperforming the overall market, underscoring the sustained appeal of artificial intelligence as an investment theme and reinforcing its leadership position in the semiconductor industry.

- Supply Chain Advantage: Analysts noted Nvidia's proactive supply chain management places it in an advantageous position compared to peers, with $95 billion in purchase commitments that can cover much of its shipping plans over the next 18 months, enhancing its competitive edge.

See More

Nvidia's Dominance in the Booming Space Economy

- Market Growth Potential: The global space economy is projected to reach $1.8 trillion by 2035, up from $630 billion in 2023, reflecting a robust annual growth rate of about 9%, indicating strong investment appeal.

- AI Application Outlook: The global AI in space exploration market is expected to grow from $6.2 billion to $110.2 billion by 2035, with a staggering CAGR of 33.4%, presenting significant market opportunities for Nvidia.

- Technological Leadership: Nvidia's launch of space AI computing platforms has positioned it for first-mover advantage, with the latest Rubin GPU module delivering up to 25 times more AI compute power, facilitating next-gen orbital data centers and autonomous space operations.

- Partner Network Expansion: Nvidia's technology is being utilized by several space companies, including Axiom Space and Planet Labs, the latter of which provides detailed Earth imagery daily, showcasing its attractive business model and future profitability potential.

See More

GF Securities Raises Nvidia Price Target to $308 Ahead of Earnings

- Price Target Increase: GF Securities raised Nvidia's price target from $292 to $308, reflecting an optimistic outlook on the company's financial performance ahead of its upcoming earnings report.

- Share Buyback Anticipation: Analyst Jeff Pu noted that with a strong cash position and free cash flow, Nvidia is expected to announce a new share repurchase program during the earnings call, which would further bolster investor confidence.

- Data Center Market Share: Beyond GPUs, Nvidia is anticipated to capture a larger value share of the data center silicon market, supported by Vera CPU and LPX, which will drive long-term growth for the company.

- Earnings Forecast Adjustment: By factoring in higher Blackwell units and average selling prices, Nvidia's EPS estimates for FY27E and FY28E have been revised up by 0% and 13%, respectively, indicating an improvement in the company's profitability for the upcoming fiscal years.

See More

Nvidia Earnings in Focus as Market Reacts Mutedly

- Nvidia Earnings Expectations: Nvidia is expected to report an 80% year-over-year revenue growth for Q1, with its market cap briefly exceeding $5.7 trillion last week, underscoring its leadership in the AI sector, despite a 4.4% drop in stock price last Friday.

- Market Impact Analysis: Analysts note that Nvidia accounts for 9% of the S&P 500 index and contributed 20% to the index's total returns for 2026, highlighting its significant influence on overall market performance, particularly driven by AI stocks.

- Retail Earnings Outlook: TJX anticipates a 6% year-over-year revenue increase for Q1, while Walmart is expected to maintain strong performance following a 12% EPS growth, indicating continued consumer spending resilience.

- Berkshire Portfolio Adjustments: Berkshire Hathaway, under new CEO Abel, acquired a $2.6 billion stake in Delta Air Lines and reduced investments in banking and healthcare sectors, reflecting a strategy focused on concentrated investments.

See More

Nvidia and AMD Stocks Near All-Time Highs

- Stock Performance: As of May 14, 2026, Nvidia and AMD stocks rose by 4.39% and 5.67% respectively, indicating strong market performance and reflecting investor confidence in both companies.

- Valuation Analysis: Despite trading near all-time highs, analysts suggest that these stocks may not be as 'expensive' as perceived, presenting potential buying opportunities for investors.

- Market Outlook: With the increasing demand for artificial intelligence and high-performance computing, the product demand for Nvidia and AMD continues to rise, potentially driving further stock price increases and enhancing investment appeal.

- Investment Recommendation: In the current market environment, although stock prices are high, analysts believe both stocks remain worthy of attention, urging investors to consider their long-term growth potential.

See More

Iren Reports Earnings and Major Tech Deal

- Power Infrastructure Progress: Iren successfully energized its 1.4-gigawatt Sweetwater 1 site ahead of the April 2026 target, demonstrating reliability and speed in large-scale infrastructure construction, which boosts market confidence.

- Acquisition of Mirantis: Iren's $625 million acquisition of Mirantis aims to enhance its software capabilities and attract more customers needing AI infrastructure, leveraging Mirantis's network of over 1,500 enterprise clients to create new business opportunities.

- Strategic Partnership with Nvidia: Iren signed a five-year, $3.4 billion deal with Nvidia to provide infrastructure cloud services using 60 megawatts of capacity at its Childress, Texas facility, expected to drive annual recurring revenue to $3.1 billion, although revenue recognition will take time.

- Increasing Debt Pressure: Following its earnings report, Iren issued $2.6 billion in convertible notes, highlighting ongoing losses and high debt levels in a capital-intensive industry, raising investor concerns about its long-term profitability despite significant potential in AI infrastructure.

See More