Key Takeaways

Stocks under $5 offer accessible entry points with exponential growth potential, as demonstrated by Oncology Institute's 884% year-to-date gain.

• Biotech stocks lead upside potential: Pyxis Oncology (309% upside) and Zentalis Pharmaceuticals (57% upside) offer substantial returns tied to clinical trial results in 2026.

• Technology companies provide balanced risk-reward: Valens Semiconductor maintains $94M cash with no debt while targeting $220-300M revenue by 2029.

• Financial health varies dramatically: While some companies like Zentalis hold $280M cash, others like Polar Power face going-concern warnings with just $4,000 cash.

• Analyst consensus favors biotech and tech: Five of seven stocks carry "Buy" or "Strong Buy" ratings, with price targets suggesting 54-309% upside potential.

• Due diligence is critical: These sub-$5 stocks span from promising growth stories to speculative turnaround plays requiring careful risk assessment before investment.

The key to success with penny stocks lies in identifying fundamentally strong companies experiencing temporary setbacks rather than businesses with permanent structural problems. While the potential for 100%+ returns exists when a $3 stock doubles, investors must balance this opportunity against the inherent volatility and binary risks these investments present.

Want to boost your portfolio with the best stocks under $5? You're not alone. A single cheap stock—Oncology Institute Inc. (TOI)—has already delivered an amazing year-to-date gain of nearly 884%.

Penny stocks, which trade under $5, give investors with limited capital an available entry point. A $300 investment could buy 100 shares at $3, and the value would double if the stock price rises just $3. The secret lies in spotting fundamentally strong companies going through temporary setbacks rather than those facing permanent problems.

You'll find many compelling options in the market today. Bitfarms Ltd. (BITF), valued at $1.6 billion, has already gained 87.3% year-to-date. Perspective Therapeutics shows promise with a potential 304.9% upside based on consensus price targets. GoPro Inc. (GPRO) looks attractive too, with a high Sharpe Ratio of 1.79.

Ready to find those hidden gems that could revolutionize your investment portfolio? Let's look at seven expert-recommended stocks under $5 worth watching in 2026.

Valens Semiconductor (VLN)

Valens Semiconductor (VLN) stands out from other semiconductor stocks at $2.48. This Israel-based company has a market cap of about $253.87 million. Wall Street analysts have set a price target of $3.83, which points to a possible 54% upside.

Valens Semiconductor key features

Valens makes high-performance connectivity solutions through two main segments: Audio-Video and Automotive. The company's HDBaseT technology is its flagship product. It can send ultra-high-definition digital video, audio, Ethernet, USB, control signals, and power through one long-reach cable. This innovative approach makes the company valuable across several markets.

The company leads in semiconductor products across multiple sectors:

Enterprise solutions: Delivering connectivity for video conferencing, education, and digital signage

Automotive applications: Providing chipsets that support advanced driver-assistance systems (ADAS)

Industrial Machine Vision: Offering solutions for manufacturing efficiency and inspection accuracy

Medical technology: Supplying components for endoscopy and other medical devices

The company's financial position looks solid with about $94 million in cash and no debt as of September 2025. This healthy balance sheet gives them room to operate and a runway of about 6.5 years at current cash burn rates.

Valens Semiconductor growth potential

The company has big plans for growth through expansion and strategic buyouts. At its 2024 Investor Day, the team shared some ambitious targets. They aim to hit total revenue between $220-$300 million by 2029. That's a big jump from their 2024 revenue of $57.86 million.

Valens can tap into several growing markets with a combined total addressable market (TAM) of about $5.5 billion. Here's how it breaks down:

Video-Conferencing: TAM expected to reach $350 million by 2029

Automotive: TAM projected to grow to $4.5 billion by 2029

Industrial Machine Vision: TAM predicted to reach $460 million by 2029

Medical (single-use endoscopes): Potential TAM of $625 million pending regulatory approval

Wall Street seems excited about these prospects and rates VLN stock as "Strong Buy". The company landed three new design wins with European automotive OEMs for its ADAS connectivity chipsets in vehicles starting in 2026. This shows that the market believes in their technology.

Valens Semiconductor risk factors

The company faces some challenges that investors should know about. Right now, it's not making money, with a net income of -$30.13 million and an EBITDA of -$29.11 million. While this raises concerns, analysts believe the company will reach cash flow breakeven before running out of cash.

The cash burn rate has shot up by 274% over the last year. Revenue only grew by 7.5% during this time. This gap raises questions about how sustainable their growth strategy really is.

The semiconductor industry goes through ups and downs. Revenue dropped by 31.25% in 2024 compared to the previous year. This shows just how volatile the sector can be. The company also faces tough competition in both audio-video and automotive semiconductor markets.

In spite of that, several analysts predict a breakout, and their target price sits well above current trading levels. Valens Semiconductor might reward investors who can handle these risks. With plenty of cash, solid technology, and expansion into growing markets, this sub-$5 stock looks interesting for investors who want growth opportunities in semiconductors.

Offerpad Solutions (OPAD)

Offerpad Solutions (OPAD) trades at $2.19 and looks like an interesting player in the real estate technology space. This Arizona company's modest market cap of $80.72 million shows promise through its smart strategic shifts that could spark future growth despite tough market conditions.

Offerpad Solutions key features

Offerpad runs a technology-enabled real estate platform that makes buying and selling homes easier. The company's business model revolves around several key services:

Cash Offer: Homeowners can get quick cash offers for their properties through a simple digital process

HomePro: A new platform available in all markets where specialized agents help sellers explore their options through scheduled appointments

Renovate: B2B renovation service that works with institutional and investor partners

Direct+: A program that helps investors connect with sellers

The company uses its own technology to speed up transactions. They blend human expertise with smart automation to deliver quality service that works for many customers. This tech-focused approach helps Offerpad stay disciplined even when market conditions get tough.

The numbers show Offerpad brought in Q3 2025 revenue of $132.70 million and sold 367 homes during that time. They have over $75 million in total liquidity, giving them room to adapt their business model.

Offerpad Solutions growth potential

The company's growth plan focuses on expanding services that need less capital and offer better margins. This smart shift aims to boost transaction numbers and create steady revenue streams over time.

Their Renovate service shows real promise. It hit record quarterly revenue of $8.50 million in Q3 2025 – the best performance since launch. This growth tells management they're on the right track.

The company has made great strides:

They cut operating expenses by 38% compared to last year

The balance sheet looks stronger after raising capital

New AI tools like picture recognition and smart scoping make operations run smoother

The company wants to sell 1,000 homes each quarter once markets settle down. Their Agent Partnership Program helps them find customers more cheaply and strengthens their growth strategy.

Offerpad Solutions risk factors

Good moves aside, Offerpad faces big challenges. Money pressures top the list – they're losing money with a net income of -$54.89 million and a worrying profit margin of -8.74%.

The debt load looks heavy for a company this size:

They owe $171.26 million but only have $30.96 million in cash

The debt/equity ratio sits at 429.75%, showing they're highly leveraged

A current ratio of 1.13 points to tight cash flow

Real estate market conditions add extra risk. Higher interest rates make homes less affordable and slow down sales. The iBuying business model goes up and down with market cycles and needs lots of capital.

Revenue projections for Q4 2025 range between $100 million and $125 million with expected sales of 300 to 350 homes. These numbers fall well short of last year's $208.10 million.

Offerpad stands out as a risky bet among stocks under $5. Their shift toward lighter-asset services could lead to stability, but investors should weigh the money troubles against growth plans before jumping into this speculative investment.

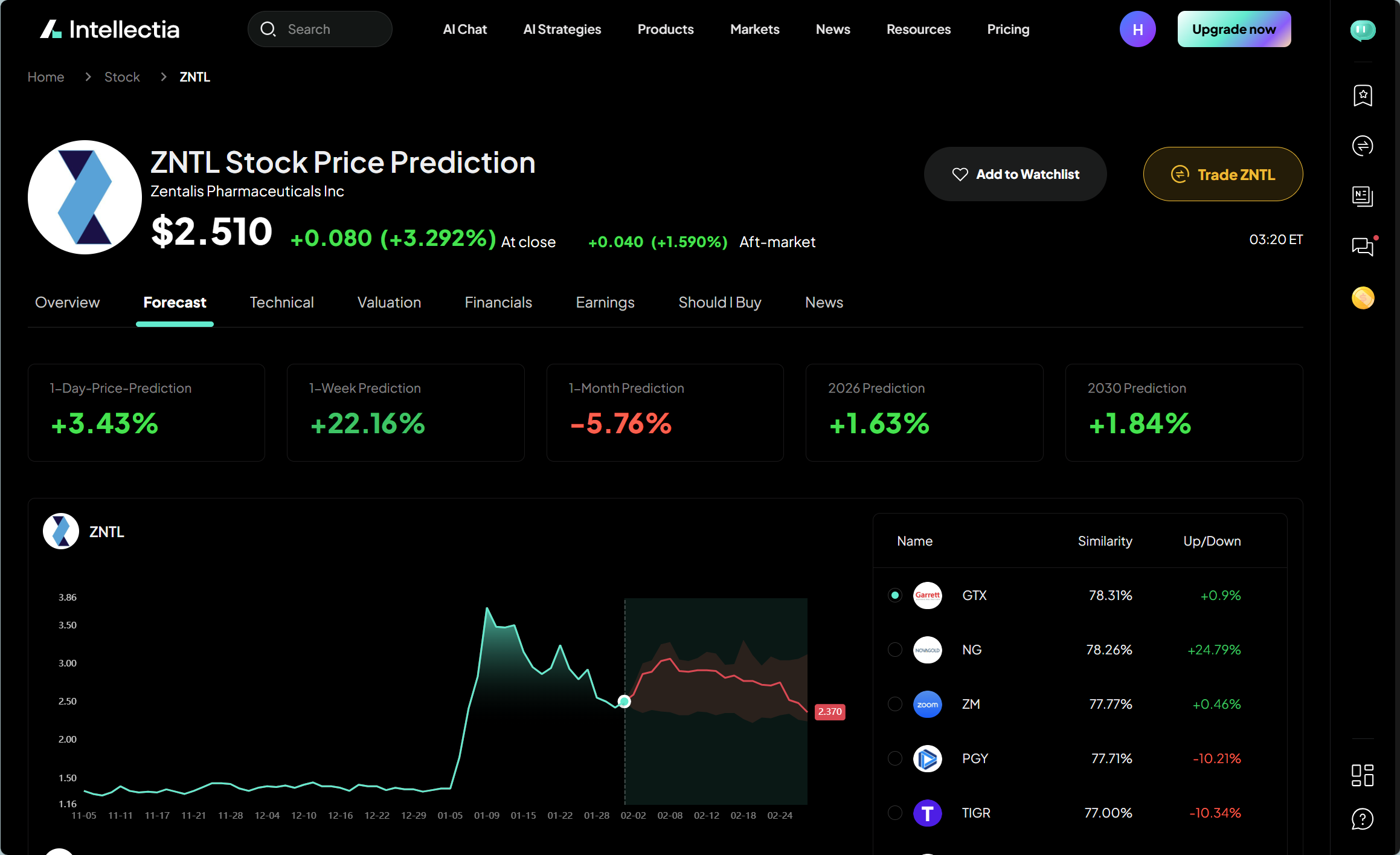

Zentalis Pharmaceuticals (ZNTL)

Zentalis Pharmaceuticals (ZNTL) stands out as a promising clinical-stage biopharmaceutical company. The stock trades at $3.74 per share as of January 9, 2026. Investors looking for stocks under $5 took notice when the share price jumped 31.69% in a single day.

Zentalis Pharmaceuticals key features

The company develops small molecule therapeutics to treat cancer. Their star product is azenosertib, which could become the first WEE1 inhibitor in its class. The drug is now in late-stage clinical development. It works by blocking WEE1, a protein kinase that controls cell cycle checkpoints.

The company builds its strategy around:

Biomarker-driven development that targets Cyclin E1-positive platinum-resistant ovarian cancer (PROC)

Several therapeutic uses including standalone treatment and various combinations

Their own technology that offers better selectivity and pharmacokinetic properties

The market has no FDA-approved WEE1 inhibitors yet, which gives Zentalis a head start. The company's finances look solid with $280.70 million in cash, cash equivalents, and marketable securities as of September 30, 2025. The management team believes this money will last until late 2027.

Zentalis Pharmaceuticals growth potential

The DENALI clinical trial program could be a game-changer for Zentalis. They've finished enrolling patients in Part 2a of this Phase 2 registration-intent trial. The company plans to release topline data from DENALI Part 2 by the end of 2026. This could lead to faster approval if the FDA agrees.

Early results look promising. Part 1b of DENALI showed an objective response rate of 34.9%. Patients with Cyclin E1+ PROC had a median response duration of 6.3 months. The FDA has also approved the design of ASPENOVA, a Phase 3 trial that will compare azenosertib with standard chemotherapy.

The market potential is huge. About half of all PROC patients show high levels of Cyclin E1 protein, based on the company's testing methods. These patients currently lack targeted treatment options.

Wall Street seems bullish on Zentalis:

Analysts rate it as a "Buy"

The average price target sits at $5.87, hinting at a possible 56.95% gain

Several analysts kept their "Buy" ratings in 2025, with price targets ranging from $6.00 to $10.00

Zentalis Pharmaceuticals risk factors

Zentalis faces some tough challenges. The company loses money, with a $149.32 million deficit and loses $2.08 per share. The stock price swings wildly, showing a beta of 1.75. This means it's more volatile than the market.

The numbers raise red flags:

A negative P/E ratio

An Altman Z-Score of -4.29 suggests bankruptcy risks

A low Piotroski F-Score of 2 points to weak finances

Revenue sits at just $26.87 million against big losses

Future projections tell a mixed story. Revenue might grow 26.43% over five years, but earnings per share could drop by 56.74%. The stock has lost 40% of its value in the last twelve months. This shows investors remain cautious.

The biggest risk lies in the DENALI trial results expected late in 2026. These results could make or break the company's future. Until then, investors must weigh the possible rewards against the risks.

This stock might suit investors who can handle the ups and downs of clinical-stage biotech companies and don't mind waiting for crucial trial results. It's a classic high-risk, high-reward play among stocks under $5.

loanDepot (LDI)

LoanDepot (LDI) shares now trade at $2.91, and investors are paying attention to this mortgage lender after its strong 75.30% return in the last year. This California-based nonbank retail mortgage lender started in 2010 and has grown into a major player in the $11 trillion total addressable market.

loanDepot key features

The company runs a technology-driven residential mortgage platform that offers a complete range of services. Here's how their business works:

Origination of conventional and government mortgage loans

Financing, selling, and servicing residential mortgage loans

Title, escrow, and settlement services for mortgage transactions

The company's proprietary mello® software platform sits at the heart of their operation. This platform has reshaped the traditional mortgage process through new technology. Their tech-first approach lets them offer several loan products:

Conventional agency-conforming and prime jumbo loans

Federal assistance residential mortgage options

Home equity lines of credit and closed-end second liens

The company has a market value of about $969.72 million with 4,553 employees. They use multiple channels to reach customers through direct-to-consumer platforms, local retail offices, and partnerships with homebuilders.

loanDepot growth potential

Founder and Executive Chairman Anthony Hsieh will step in as interim CEO, and the company plans to make the most of its assets to improve operations. Recent quarters show the company is moving in the right direction.

The third quarter of 2025 brought several improvements:

Revenue grew 14% to $323 million from the previous quarter

Pull-through weighted gain on sale margin increased 9 basis points to 339 basis points

Adjusted EBITDA jumped 90% to $49 million

Cash reserves grew to $459 million from $409 million in the prior quarter

Pull-through weighted lock volume hit $7 billion in Q3 2025, up 10% from Q2. These results show loanDepot's strategy of diverse origination and large servicing portfolio is working well.

Their Consumer Direct Lending channel stands out as one of the few tech-powered, large-scale models with excellent lead generation and customer retention. Their preliminary organic refinance consumer direct recapture rate reached 65% in Q3 2025.

loanDepot risk factors

Recent positive trends aside, loanDepot faces real challenges. The company lost $8.7 million in Q3 2025. The trailing twelve-month EPS is -$0.36, with a concerning net margin of -9.63%.

The debt situation raises red flags:

Total debt reaches $4.44 billion

A very high debt-to-equity ratio of 1,724.79%

Beta of 3.16 shows high stock price swings compared to the market

Analysts remain cautious, with 2 analysts giving a consensus "Sell" rating. The valuation presents mixed signals. While the company trades at just 0.6x sales, below the peer average of 3.8x, the forward P/E ratio of 27.45 suggests high growth expectations that might be hard to meet.

Looking ahead, loanDepot expects origination volume between $6.5 billion and $8.5 billion in upcoming quarters. However, market conditions and interest rate changes create uncertainty for mortgage lenders everywhere.

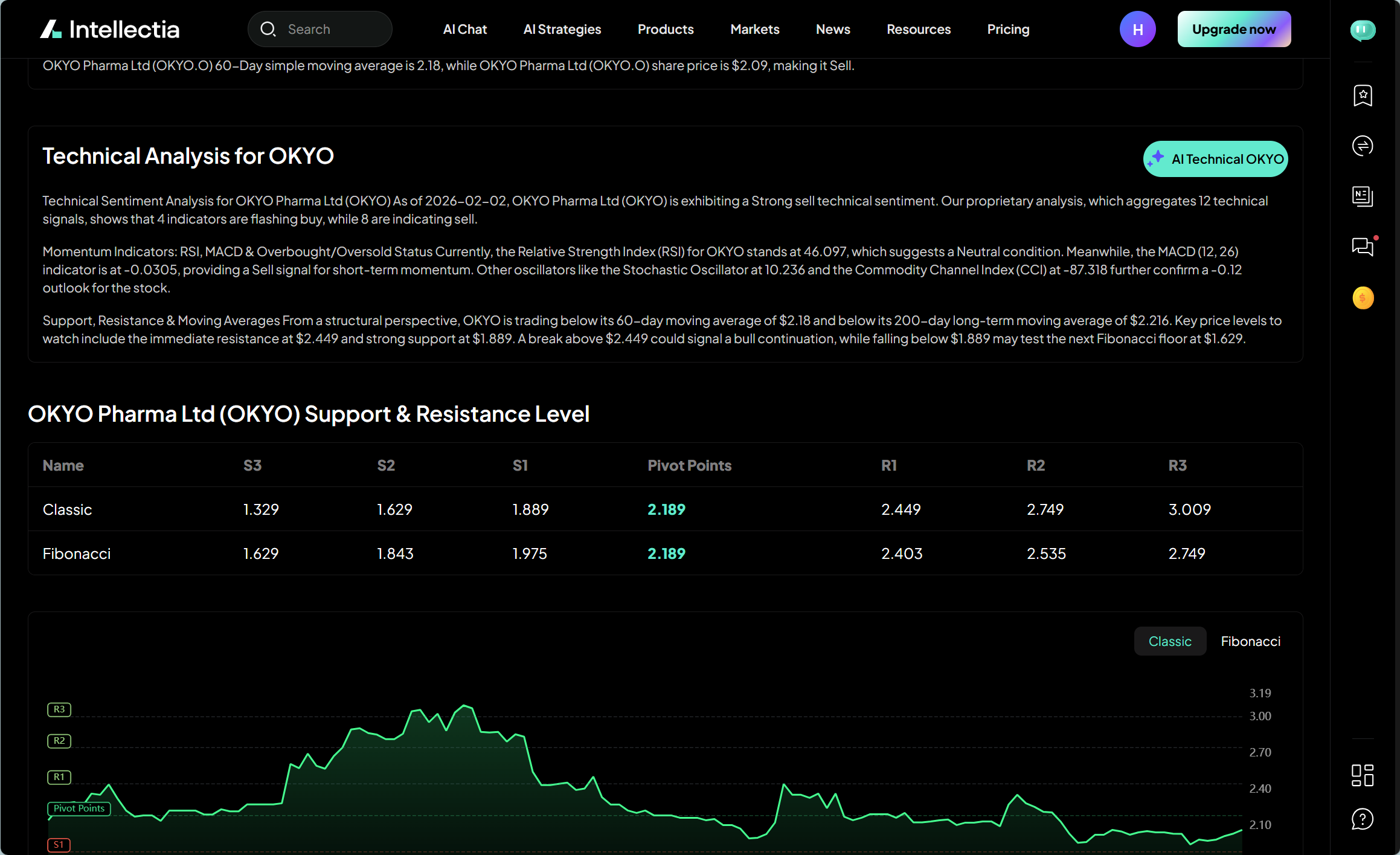

OKYO Pharma (OKYO)

OKYO Pharma (OKYO) trades at $2.76 and develops innovative therapies for inflammatory eye diseases and ocular pain. Analysts have given this clinical-stage biopharmaceutical company a "Strong Buy" rating with a $6.00 price target that points to a possible 117.4% upside.

OKYO Pharma key features

The company's lead drug candidate, urcosimod (formerly OK-101), sits at the heart of OKYO's work. This lipid-conjugated chemerin peptide serves as a first-in-class treatment that can reduce both inflammation and ocular pain. The drug stands out because it:

Uses lipid-conjugated peptide chemistry to reduce drug washout and boost potency

Comes in a preservative-free, EDTA-free form

Targets the ChemR23 G-protein coupled receptor found on immune cells, neurons, and glial cells

OKYO has secured exclusive licensing for urcosimod from OTTx Therapeutics (Boston, MA). The company's pipeline targets several eye conditions, including neuropathic corneal pain (NCP), dry eye disease (DED), allergic conjunctivitis, and uveitis.

The company has a second program, OK-201, in its discovery phase. The FDA has granted urcosimod Fast-Track status, which could speed up its path to approval.

OKYO Pharma growth potential

Urcosimod's promising clinical results drive the company's growth path. The Phase 2 proof-of-concept trial for neuropathic corneal pain showed remarkable results - 75% of per-protocol patients who received 0.05% urcosimod saw their pain drop by more than 80% after 12 weeks. These results have led OKYO to start a larger multiple-ascending-dose clinical trial that will:

Include about 100 NCP patients at several U.S. clinical sites

Find the best doses for future Phase 3 trials

Study urcosimod's micellar drug characteristics more deeply

The company expects topline data from this expanded trial in 2026. OKYO plans to meet with the FDA to discuss what they need for NCP treatment approval and key endpoints.

The drug shows promise beyond NCP. It has proven effective for dry eye disease, hitting statistical targets in multiple areas during a 240-patient Phase 2 trial. This success in two conditions makes the drug even more valuable in the market.

Analysts love what they see. HC Wainwright keeps saying "Strong Buy" with a $7.00 target throughout 2024-2025. B. Riley Securities jumped in with their own "Strong Buy" and $5.00 target in December 2025.

OKYO Pharma risk factors

The company faces real challenges despite its strong clinical data. Money tops the list of concerns - OKYO won't turn a profit in the next three years. The company's total liabilities are higher than its assets, which could spell trouble.

Looking at discounted cash flows paints a mixed picture. The analysis suggests OKYO might be worth 40-47% more than its current share price, but this depends heavily on guesses about future cash flows and growth. The model uses a 7.4% cost of equity as its discount rate.

Big institutions own just 2.97% of the company, though insiders hold a big chunk at 40.46%. Short interest has jumped by 248.24%, which shows some investors are getting nervous.

OKYO faces tough competition as it develops eye treatments, especially as it tries to create the first FDA-approved therapy for neuropathic corneal pain. The company's future rides heavily on FDA approval, making every interaction with regulators crucial yet unpredictable.

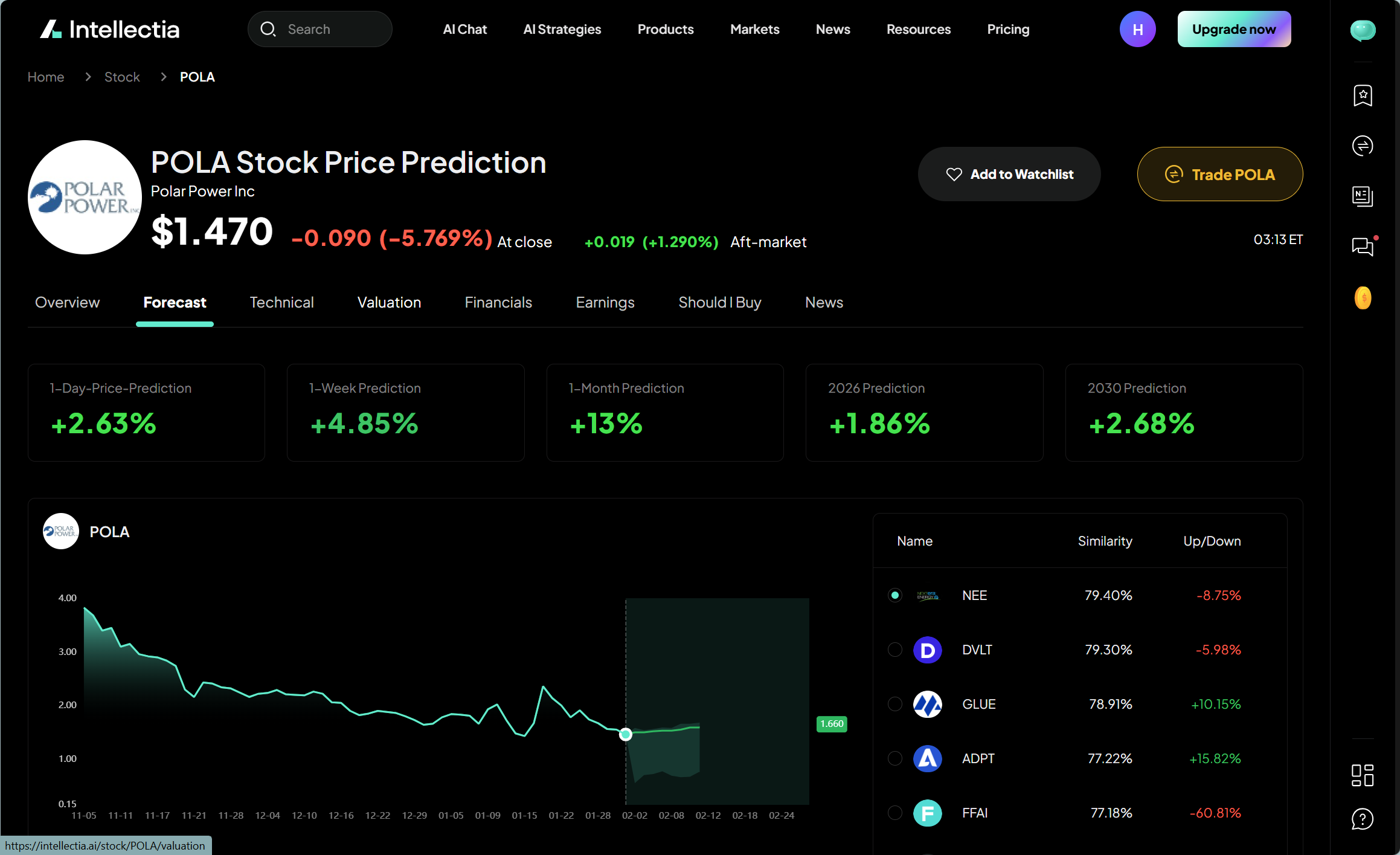

Polar Power (POLA)

Polar Power (POLA) trades at just $1.94 per share and presents a classic high-risk, high-reward opportunity in the DC power generation market. This California-based manufacturer creates direct current (DC) power systems that serve telecommunications, military, commercial, industrial, and marine markets.

Polar Power key features

The company stands out as a global provider of prime, backup, and solar hybrid DC power solutions. Their specialized technology sets them apart by using fewer raw materials than conventional alternatives. Their DC generators need six times less steel and copper to produce the same power output. This creates a cost advantage when making material-heavy products.

The company's product portfolio includes:

DC base power systems

DC hybrid power systems

DC solar hybrid power systems (available in diesel, natural gas, LPG/propane, and renewable fuel formats)

Mobile power systems

The company offers global network management, aftermarket support, and warranty services. Their reach spans Europe, Asia, Africa, South-East Asia, and Australia. Commission-based sales teams operate in key markets like South Africa, Nigeria, Kenya, Papua New Guinea, Turkey, Israel, and the Philippines.

Polar Power growth potential

Product diversification and expansion into niche markets drive the company's growth strategy. They avoid markets dominated by low-cost, single-application products. This strategy has paid off with their backlog growing to $5.30 million as of September 2025, up from $1.20 million in June 2025.

Recent contracts highlight this diversification. The company secured a $0.67 million military order for auxiliary power units and a $1.70 million order for EV chargers that work with Tesla models. Their performance should improve with increased shipments to their largest Tier-1 customer in early 2026.

Polar Power risk factors

Despite these opportunities, Polar Power faces serious challenges. Q3 2025 brought a net loss of $4.09 million, or $(1.63) per share, compared to a net profit of $0.01 per share in Q3 2024. Sales dropped when orders decreased from their largest U.S. telecommunications customer and international clients.

Financial metrics reveal concerning signs:

Market capitalization sits at $5.20 million

Profit margin shows -104.1%

Quarterly sales fell 73.5% year-over-year

No dividends are being paid

The company's cash dwindled to $4,000 by September 2025. This led management and auditors to question Polar Power's ability to continue operating.

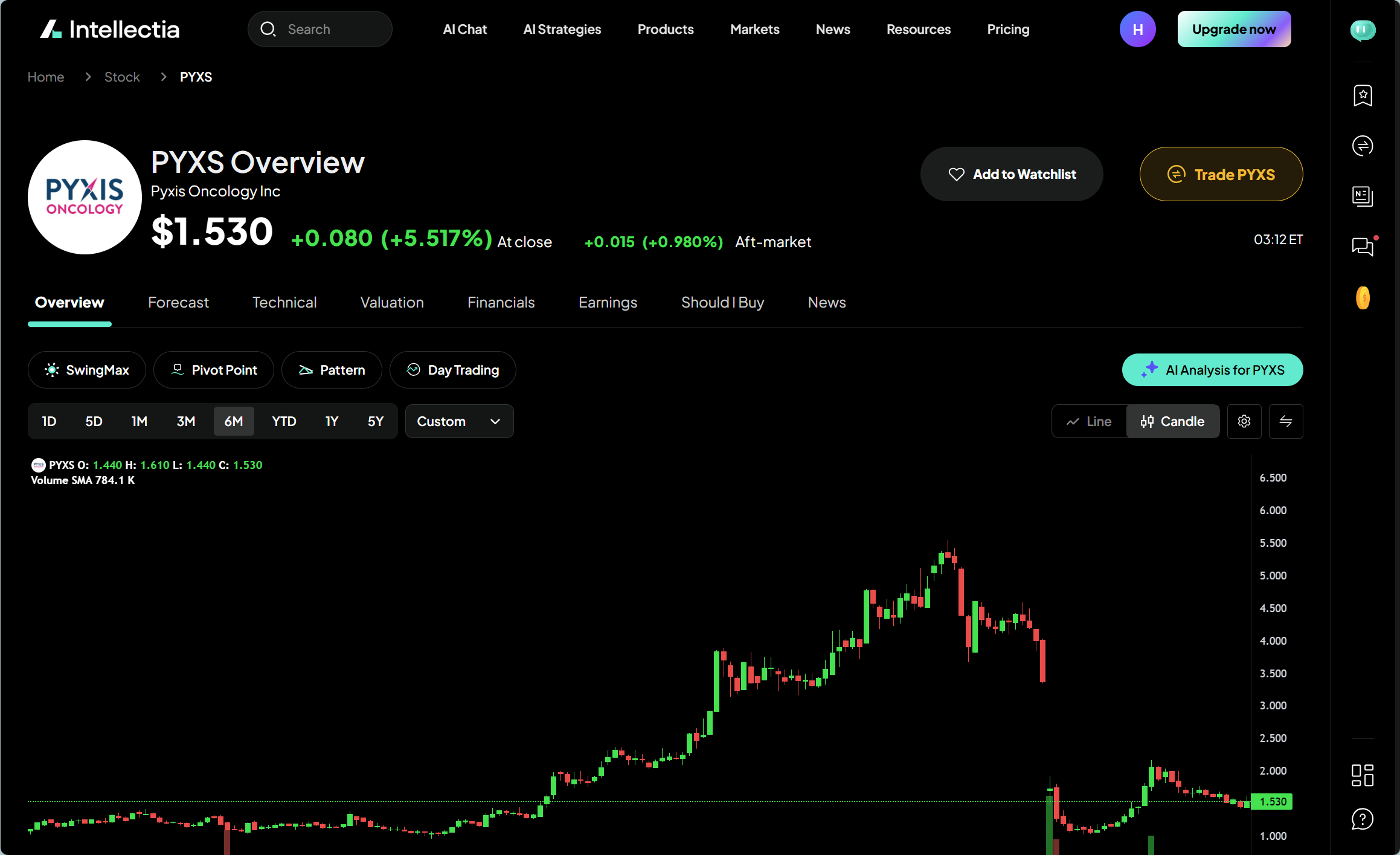

Pyxis Oncology (PYXS)

Pyxis Oncology (PYXS) has emerged as a promising clinical-stage biotech company. The stock trades at $1.76, and analysts see a potential 309.1% upside with a median target of $7.20. Wall Street has given the company a "Strong Buy" consensus rating, thanks to its innovative approach to fighting stubborn cancers.

Pyxis Oncology key features

The company's main focus lies in developing next-generation cancer therapeutics through its flagship drug candidate, micvotabart pelidotin (MICVO). This drug stands out from typical antibody-drug conjugates (ADCs). Instead of targeting cancer cells directly, MICVO targets the extradomain-B splice variant of fibronectin (EDB+FN) in the tumor microenvironment. This unique extracellular targeting approach lets MICVO potentially deliver its payload in a variety of tumor types.

MICVO fights cancer through three collaborative mechanisms:

Direct tumor cell killing

Bystander killing of adjacent tumor cells

Immunogenic cell death that activates immune response

The U.S. Food and Drug Administration has granted Fast Track Designation to MICVO. This designation applies to adult patients with recurrent/metastatic head and neck squamous cell carcinoma (R/M HNSCC) whose disease has progressed after platinum-based chemotherapy and anti-PD(L)-1 therapy.

Pyxis Oncology growth potential

The company plans to share preliminary data from ongoing Phase 1 clinical studies of MICVO in R/M HNSCC patients in Q4 2025. This update will include findings from both the monotherapy dose expansion study and the combination trial with Merck's KEYTRUDA®.

Analysts expect earnings to grow by 11.9% with revenue jumping 65.5% per year. New data from the Phase 1 monotherapy study will come in mid-2026, followed by combination study results in the second half of 2026.

Several Wall Street firms have issued "Buy" ratings with price targets between $5.00 and $9.00. The FDA has already approved the clinical trial design for a planned pivotal monotherapy study.

Pyxis Oncology risk factors

Despite its promising pipeline, Pyxis faces significant financial hurdles. Q3 2025 brought a net loss of $22.00 million (-$0.35 per share). The company will likely stay unprofitable for the next three years.

Cash and cash equivalents stood at $77.70 million in September 2025. Management believes this will support operations into the second half of 2026. The quarterly R&D expenses of $17.80 million suggest the company might need additional funding.

Like all clinical-stage biotechs, Pyxis faces a make-or-break moment with its upcoming trial results. The stock shows significant volatility with a beta of 1.45.

Comparison Table

| Stock (Symbol) | Current Price | Market Cap | Analyst Rating | Price Target/Upside | Key Business Focus | Notable Financial Metrics |

| Valens (VLN) | $2.48 | $253.87M | Strong Buy | $3.83 (54% upside) | Continuous connection solutions for Audio-Video and Automotive | Cash: $94M, No debt, Net Income: -$30.13M |

| Offerpad (OPAD) | $2.19 | $80.72M | Not mentioned | Not mentioned | Real estate platform with tech focus | Total debt: $171.26M, Cash: $30.96M, Net Income: -$54.89M |

| Zentalis (ZNTL) | $3.74 | Not mentioned | Buy | $5.87 (56.95% upside) | Cancer therapeutics development | Cash: $280.70M, Net Loss: $149.32M |

| loanDepot (LDI) | $2.91 | $969.72M | Sell | Not mentioned | Tech-driven mortgage lending | Total debt: $4.44B, EPS: -$0.36 |

| OKYO Pharma (OKYO) | $2.76 | Not mentioned | Strong Buy | $6.00 (117.4% upside) | Eye inflammation treatment solutions | Not profitable, Low institutional ownership: 2.97% |

| Polar Power (POLA) | $1.94 | $5.20M | Not mentioned | Not mentioned | DC power generation systems | Net Loss: $4.09M, Cash: $4,000 |

| Pyxis Oncology (PYXS) | $1.76 | Not mentioned | Strong Buy | $7.20 (309.1% upside) | Cancer therapeutics development | Cash: $77.70M, Net Loss: $22.00M |

Conclusion

Seven stocks under $5 show different risk-reward profiles in a variety of sectors. Biotech players like Pyxis Oncology and Zentalis Pharmaceuticals could deliver big returns, but their success depends on upcoming clinical milestones. Tech companies like Valens Semiconductor have strong cash positions and promising market chances, though they're not profitable yet.

Sign up Intellectia.AI today to get daily AI stock picks, trading signals and in-depth market analysis to guide your journey from beginner to pro. A great starting point is the Intellectia.ai AI Screener. You can use it to instantly filter the entire market for companies that best to buy under $5. Furthermore, for those looking for concise daily recommendations, the AI Stock Picker provides data-driven, actionable insights.

Your risk tolerance should line up with how you invest in these stocks. OKYO Pharma and Polar Power sit at opposite ends of the spectrum. Analysts love OKYO Pharma with its projected 117% upside. Polar Power, despite its innovative tech, struggles with serious cash flow issues. On top of that, companies like loanDepot show how even 20-year-old businesses with big market caps can become bargains during tough times.

You need to do your homework before putting money into any sub-$5 stock. Stock Technical Analysis and Quant AI tools help you see how past earnings affect current prices. Intellectia's Stock Chart Patterns let you spot support levels where big institutions likely place their buy orders, giving you better timing than regular investors.

These investments attract attention because they're easy to buy and could grow exponentially. While they're definitely speculative, carefully picked stocks under $5 give you a chance to get in early on game-changing companies. Just look at Oncology Institute's amazing 884% gain this year - it proves hidden gems exist if you know where to find them.