Zscaler Reports Strong Q2 Earnings but Lowers FY26 Sales Guidance

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 27 2026

0mins

Should l Buy ZS?

Source: Benzinga

- Earnings Beat: Zscaler reported Q2 earnings of $1.01 per share, surpassing the analyst consensus of $0.90, indicating strong performance in the cybersecurity sector despite a challenging market environment.

- Revenue Growth: The quarterly revenue reached $815.75 million, exceeding the analyst estimate of $798.82 million, reflecting sustained demand for cybersecurity solutions in the AI era and enhancing its competitive position.

- Guidance Downgrade: Zscaler lowered its FY26 revenue outlook to a range of $3.31 billion to $3.32 billion, down from the previous estimate of $3.3 billion, indicating a cautious outlook that may impact investor confidence.

- Stock Volatility: Following the earnings announcement, Zscaler's shares fell 13.4% to $144.97 in pre-market trading, reflecting negative market sentiment towards the lowered guidance, with analysts adjusting their price targets potentially exacerbating market fluctuations.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ZS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ZS

Wall Street analysts forecast ZS stock price to rise

30 Analyst Rating

24 Buy

6 Hold

0 Sell

Strong Buy

Current: 146.170

Low

260.00

Averages

325.62

High

390.00

Current: 146.170

Low

260.00

Averages

325.62

High

390.00

About ZS

Zscaler, Inc. is a cloud security company. The Company has developed a platform incorporating core security functionalities needed to enable fast and secure access to cloud resources based on identity, context and an organization’s policies. Its Zscaler Zero Trust Exchange platform protects thousands of customers from cyberattacks and data loss by securely connecting users, devices, and applications in any location. Its solution is a purpose-built, multi-tenant, distributed cloud platform that incorporates the security functionality needed to enable users, applications, and devices to safely and efficiently utilize authorized applications and services based on an organization’s business policies. It delivers its solutions using a software-as-a-service (SaaS) business model and sells subscriptions to customers to access its cloud platform, together with related support services. It offers a security platform that combines its platform with automated security operations.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

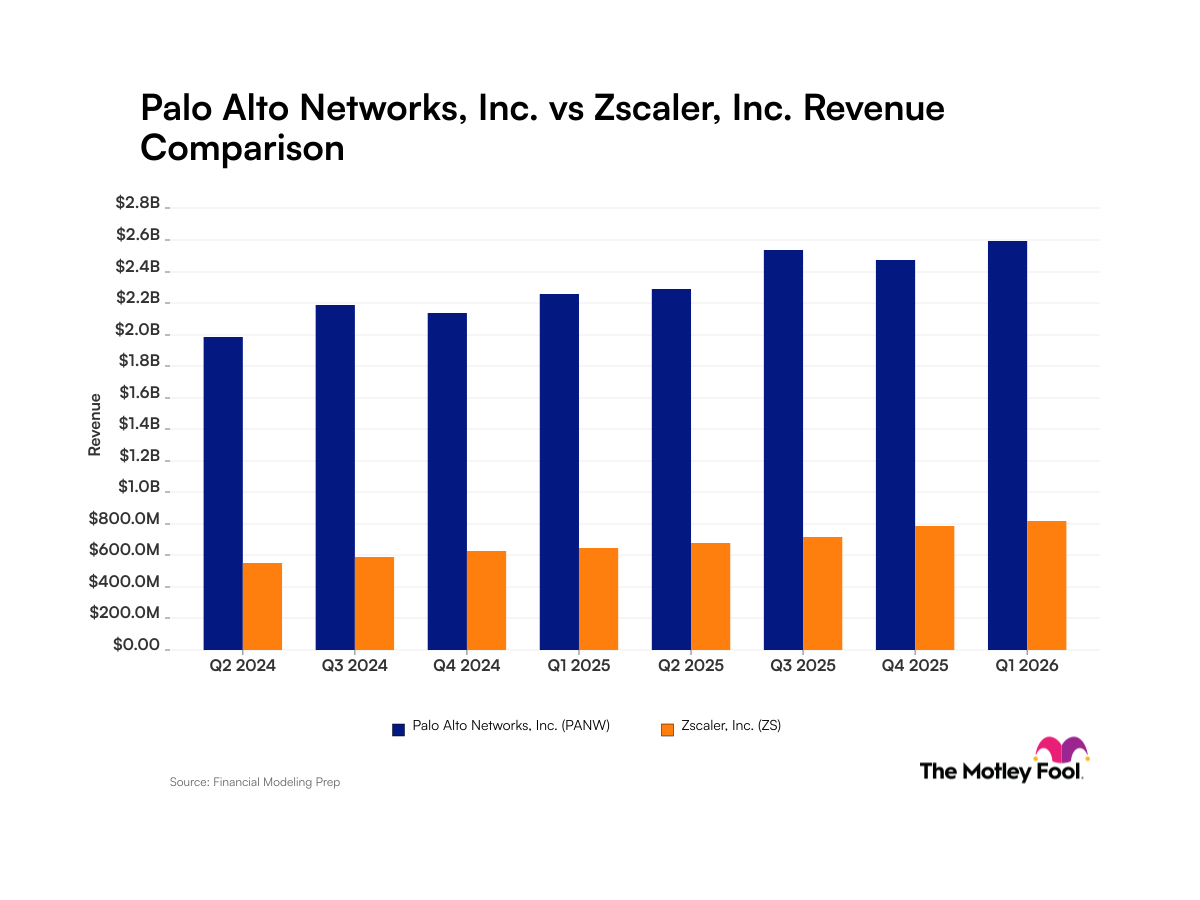

Palo Alto Networks Shows Steady Revenue Growth

- Significant Revenue Growth: Palo Alto Networks reported $2.6 billion in revenue for Q1 2026, reflecting a year-over-year growth of approximately 17%, underscoring its strong demand and leadership in the cybersecurity sector.

- Acquisition Impact: The completion of a $25 billion acquisition of CyberArk Software not only enhances its product portfolio but also potentially increases future market share and competitive strength.

- Zscaler Revenue Dynamics: Zscaler achieved $815.8 million in revenue for Q1 2026, despite a net loss of $34 million, indicating its rapid sales growth outpaces that of Palo Alto Networks, showcasing its expansion potential.

- Market Reaction and AI Influence: Concerns over AI potentially affecting customer retention led to a sell-off in the cybersecurity sector, yet both companies successfully integrated AI into their solutions, demonstrating continued strong market demand for their products.

See More

U.S. Stocks Rise, Nasdaq Hits Record High

- Nasdaq Hits Record High: The Nasdaq 100 index surged 1.32% to reach a new record high, primarily driven by chipmakers and AI infrastructure stocks, indicating strong market confidence in technology stocks that may attract further investor interest in the tech sector.

- Strong Employment Data: U.S. nonfarm payrolls rose by 115,000 in April, exceeding expectations of 65,000, while March figures were revised up to 185,000, demonstrating resilience in the labor market that could lead the Fed to maintain interest rates in upcoming policy meetings.

- Corporate Earnings Support Market: So far, 84% of the 425 S&P 500 companies have beaten earnings estimates, with Q1 earnings projected to climb 12% year-over-year, providing robust support for the stock market and reflecting the potential for economic recovery.

- Geopolitical Impact on Oil Prices: Iran's seizure of an oil tanker in the Strait of Hormuz has led to a slight increase in WTI crude oil prices, heightening concerns over future oil price volatility and potentially affecting the stability of global energy supply chains.

See More

US Stocks Close Lower Amid Cautious Market Sentiment

- Market Weakness: On Thursday, the S&P 500 Index fell by 0.38%, the Dow Jones Industrial Average dropped by 0.63%, and the Nasdaq 100 Index decreased by 0.12%, reflecting investor skepticism regarding a potential US-Iran peace deal, which led to a reversal of early gains and impacted market confidence.

- Economic Data Support: Despite the market decline, initial jobless claims rose by 10,000 to 200,000, below the expected 205,000, indicating resilience in the labor market, while Q1 nonfarm productivity increased by 0.8%, surpassing the 0.6% forecast, providing some support to the market.

- Earnings Report Impact: As of Thursday, 84% of the 425 S&P 500 companies that reported earnings exceeded expectations, with Q1 earnings projected to rise by 12% year-over-year, although growth outside the tech sector is only expected to be around 3%, indicating a divergence that may influence investor allocation strategies.

- Oil Price Recovery: WTI crude oil prices rebounded after a 4% decline on Thursday, as the market focused on the potential resumption of US military operations to ensure safe passage through the Strait of Hormuz, which is expected to have ongoing implications for global oil prices and related stocks.

See More

U.S. Stock Market Retreats as Oil Prices Surge

- Market Retreat: The S&P 500 Index fell by 0.40%, the Dow Jones Industrial Average by 0.51%, and the Nasdaq 100 by 0.28%, indicating a retreat in market sentiment as rising oil prices weigh on investor confidence and raise concerns about future economic prospects.

- Strong Employment Data: Initial jobless claims in the U.S. rose by 10,000 to 200,000, indicating a stronger labor market than the expected 205,000, while continuing claims unexpectedly fell by 10,000 to a 2.25-year low of 1.766 million, showcasing economic resilience.

- Productivity and Costs: U.S. Q1 nonfarm productivity increased by 0.8%, surpassing expectations of 0.6%, while unit labor costs rose by 2.3%, below the anticipated 2.5%, which may influence future inflation expectations and Fed policy decisions.

- Fed Policy Outlook: Boston Fed President indicated that interest rates should remain at “mildly restrictive” levels, suggesting that if inflation trends worsen significantly, a reassessment of policy would be necessary, with markets pricing in only a 6% chance of a rate cut at the next FOMC meeting.

See More

US Stocks Show Mixed Movement, Tech Stocks Surge

- Tech Stock Surge: Datadog reported Q1 revenue of $1.01 billion, exceeding the consensus of $957.8 million, leading to a stock price increase of over 30%, which boosts overall market sentiment and reflects strong recovery in the tech sector amid high investor expectations for artificial intelligence.

- Stable Labor Market: Initial jobless claims rose by 10,000 to 200,000, lower than the expected 205,000, indicating resilience in the labor market, while continuing claims unexpectedly fell by 10,000 to a 2.25-year low of 1.766 million, further enhancing market confidence.

- Crude Oil Price Decline: WTI crude oil prices fell by more than 4% as markets await updates on a potential US-Iran peace deal that could reopen the Strait of Hormuz, negatively impacting energy producers and leading to widespread declines in related stocks.

- Fed Policy Outlook: Boston Fed President indicated that interest rates should remain at

See More

Mixed US Stock Indices with Nasdaq 100 Reaching All-Time High

- Nasdaq Milestone: The Nasdaq 100 index rose by 0.20%, achieving a new all-time high, driven by strong performance in tech stocks, particularly Datadog, which surged over 30% following its blowout earnings report.

- Oil Price Decline: WTI crude oil prices fell by more than 4% today as the market awaits updates on a potential US-Iran peace deal that could reopen the Strait of Hormuz, impacting global oil prices and supply chains.

- Stable Labor Market: Initial US unemployment claims rose by 10,000 to 200,000, below expectations of 205,000, indicating labor market resilience, while continuing claims unexpectedly fell to a 2.25-year low of 1.766 million.

- Strong Corporate Earnings: So far, 84% of the 411 S&P 500 companies that reported earnings have beaten estimates, with Q1 earnings projected to climb 12% year-over-year, reflecting ongoing improvements in corporate profitability, although growth outside the tech sector is only 3%.

See More

Palo Alto Networks Shows Steady Revenue Growth

- Significant Revenue Growth: Palo Alto Networks reported $2.6 billion in revenue for Q1 2026, reflecting a year-over-year growth of approximately 17%, underscoring its strong demand and leadership in the cybersecurity sector.

- Acquisition Impact: The completion of a $25 billion acquisition of CyberArk Software not only enhances its product portfolio but also potentially increases future market share and competitive strength.

- Zscaler Revenue Dynamics: Zscaler achieved $815.8 million in revenue for Q1 2026, despite a net loss of $34 million, indicating its rapid sales growth outpaces that of Palo Alto Networks, showcasing its expansion potential.

- Market Reaction and AI Influence: Concerns over AI potentially affecting customer retention led to a sell-off in the cybersecurity sector, yet both companies successfully integrated AI into their solutions, demonstrating continued strong market demand for their products.

See More

U.S. Stocks Rise, Nasdaq Hits Record High

- Nasdaq Hits Record High: The Nasdaq 100 index surged 1.32% to reach a new record high, primarily driven by chipmakers and AI infrastructure stocks, indicating strong market confidence in technology stocks that may attract further investor interest in the tech sector.

- Strong Employment Data: U.S. nonfarm payrolls rose by 115,000 in April, exceeding expectations of 65,000, while March figures were revised up to 185,000, demonstrating resilience in the labor market that could lead the Fed to maintain interest rates in upcoming policy meetings.

- Corporate Earnings Support Market: So far, 84% of the 425 S&P 500 companies have beaten earnings estimates, with Q1 earnings projected to climb 12% year-over-year, providing robust support for the stock market and reflecting the potential for economic recovery.

- Geopolitical Impact on Oil Prices: Iran's seizure of an oil tanker in the Strait of Hormuz has led to a slight increase in WTI crude oil prices, heightening concerns over future oil price volatility and potentially affecting the stability of global energy supply chains.

See More

US Stocks Close Lower Amid Cautious Market Sentiment

- Market Weakness: On Thursday, the S&P 500 Index fell by 0.38%, the Dow Jones Industrial Average dropped by 0.63%, and the Nasdaq 100 Index decreased by 0.12%, reflecting investor skepticism regarding a potential US-Iran peace deal, which led to a reversal of early gains and impacted market confidence.

- Economic Data Support: Despite the market decline, initial jobless claims rose by 10,000 to 200,000, below the expected 205,000, indicating resilience in the labor market, while Q1 nonfarm productivity increased by 0.8%, surpassing the 0.6% forecast, providing some support to the market.

- Earnings Report Impact: As of Thursday, 84% of the 425 S&P 500 companies that reported earnings exceeded expectations, with Q1 earnings projected to rise by 12% year-over-year, although growth outside the tech sector is only expected to be around 3%, indicating a divergence that may influence investor allocation strategies.

- Oil Price Recovery: WTI crude oil prices rebounded after a 4% decline on Thursday, as the market focused on the potential resumption of US military operations to ensure safe passage through the Strait of Hormuz, which is expected to have ongoing implications for global oil prices and related stocks.

See More

U.S. Stock Market Retreats as Oil Prices Surge

- Market Retreat: The S&P 500 Index fell by 0.40%, the Dow Jones Industrial Average by 0.51%, and the Nasdaq 100 by 0.28%, indicating a retreat in market sentiment as rising oil prices weigh on investor confidence and raise concerns about future economic prospects.

- Strong Employment Data: Initial jobless claims in the U.S. rose by 10,000 to 200,000, indicating a stronger labor market than the expected 205,000, while continuing claims unexpectedly fell by 10,000 to a 2.25-year low of 1.766 million, showcasing economic resilience.

- Productivity and Costs: U.S. Q1 nonfarm productivity increased by 0.8%, surpassing expectations of 0.6%, while unit labor costs rose by 2.3%, below the anticipated 2.5%, which may influence future inflation expectations and Fed policy decisions.

- Fed Policy Outlook: Boston Fed President indicated that interest rates should remain at “mildly restrictive” levels, suggesting that if inflation trends worsen significantly, a reassessment of policy would be necessary, with markets pricing in only a 6% chance of a rate cut at the next FOMC meeting.

See More

US Stocks Show Mixed Movement, Tech Stocks Surge

- Tech Stock Surge: Datadog reported Q1 revenue of $1.01 billion, exceeding the consensus of $957.8 million, leading to a stock price increase of over 30%, which boosts overall market sentiment and reflects strong recovery in the tech sector amid high investor expectations for artificial intelligence.

- Stable Labor Market: Initial jobless claims rose by 10,000 to 200,000, lower than the expected 205,000, indicating resilience in the labor market, while continuing claims unexpectedly fell by 10,000 to a 2.25-year low of 1.766 million, further enhancing market confidence.

- Crude Oil Price Decline: WTI crude oil prices fell by more than 4% as markets await updates on a potential US-Iran peace deal that could reopen the Strait of Hormuz, negatively impacting energy producers and leading to widespread declines in related stocks.

- Fed Policy Outlook: Boston Fed President indicated that interest rates should remain at

See More

Mixed US Stock Indices with Nasdaq 100 Reaching All-Time High

- Nasdaq Milestone: The Nasdaq 100 index rose by 0.20%, achieving a new all-time high, driven by strong performance in tech stocks, particularly Datadog, which surged over 30% following its blowout earnings report.

- Oil Price Decline: WTI crude oil prices fell by more than 4% today as the market awaits updates on a potential US-Iran peace deal that could reopen the Strait of Hormuz, impacting global oil prices and supply chains.

- Stable Labor Market: Initial US unemployment claims rose by 10,000 to 200,000, below expectations of 205,000, indicating labor market resilience, while continuing claims unexpectedly fell to a 2.25-year low of 1.766 million.

- Strong Corporate Earnings: So far, 84% of the 411 S&P 500 companies that reported earnings have beaten estimates, with Q1 earnings projected to climb 12% year-over-year, reflecting ongoing improvements in corporate profitability, although growth outside the tech sector is only 3%.

See More