U.S. Stocks Hit All-Time Highs Amid Rising Geopolitical Risks

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 6 hours ago

0mins

Source: stocktwits

- Market Performance: The Dow, S&P 500, and Nasdaq reached all-time highs on Tuesday, indicating a robust market rebound despite geopolitical risks and trade tensions, with investor sentiment remaining optimistic.

- New Tariff Proposal: The U.S. Trade Representative's new tariff proposal could impose 10% to 12.5% tariffs on imports from approximately 60 economies, particularly targeting China and India, aimed at combating imports produced with forced labor, which may impact supply chains and cost structures for affected companies.

- Bitcoin Decline: Bitcoin fell below $66,000, marking its lowest level since February, reflecting a rotation of investor capital between equities and cryptocurrencies, which could lead to further volatility in the crypto market.

- Corporate Developments: Palo Alto Networks saw a 4% drop despite beating revenue expectations, indicating strong demand for its AI security offerings but ongoing market pressures, while Shopify announced an additional $3 billion share repurchase program, demonstrating confidence in future growth.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PANW?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PANW

Wall Street analysts forecast PANW stock price to fall

34 Analyst Rating

28 Buy

5 Hold

1 Sell

Strong Buy

Current: 297.180

Low

157.00

Averages

232.49

High

265.00

Current: 297.180

Low

157.00

Averages

232.49

High

265.00

About PANW

Palo Alto Networks, Inc. is a global artificial intelligence (AI) cybersecurity company, with a comprehensive portfolio of cybersecurity solutions and platforms across network, cloud, security operations, AI and Identity. Its network security platform includes Secure Access Service Edge (SASE), Next-Generation Firewalls, Cloud Delivered Security Services (CDSS), Prisma AIRS, and Strata Cloud Manager (SCM). It delivers security operations capabilities that unifies standalone Security Information and Event Management (SIEM) tools, endpoint security, security automation, cloud detection and response (CDR), as well as attack surface management (ASM) capabilities on its Cortex platform. It delivers comprehensive security across the cloud application development lifecycle through Cortex Cloud. Its Unit 42 brings together expertise across threat research, incident response, and security consulting to deliver intelligence-driven, response-ready outcomes that help customers reduce cyber risk.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Palo Alto Networks Q3 Results Beat Estimates Despite Stock Decline

- Strong Earnings Report: Palo Alto Networks reported an adjusted Q3 profit of $0.85 per share and a 31% revenue growth to $3 billion, both exceeding market expectations, indicating robust performance in the cybersecurity sector.

- Stock Price Decline: Despite the strong results, shares fell about 7%, as analysts expressed concerns over persistent overvaluation and dilution, which negatively impacted investor sentiment and confidence in the stock.

- Increased ETF Focus: The decline in stock price has shifted investor attention to ETFs with significant exposure to Palo Alto, such as the Direxion Daily PANW Bull 2X ETF, which has a 13.91% allocation, reflecting varying market perspectives on the company's future performance.

- Divergent Analyst Ratings: While analysts remain generally positive about Palo Alto Networks' outlook, some, like Kenio Fontes, maintain a 'sell' rating, highlighting the ongoing divergence and uncertainty regarding the company's long-term valuation in the market.

See More

Palo Alto Networks Stock Drops 6.8% Despite Strong Earnings Report

- Earnings Beat Expectations: Palo Alto Networks reported an adjusted profit of $0.85 per share and $3 billion in sales for Q3 of fiscal 2026, surpassing Wall Street forecasts, indicating strong market performance.

- Significant Sales Growth: The company experienced a 31% year-over-year sales increase, with remaining performance obligations reaching $18.4 billion, up 36%, highlighting robust future revenue potential and market demand.

- Negative Market Reaction: Despite strong earnings, the stock fell 6.8%, reflecting investor concerns about future growth amid rising oil prices and bond yields, which are exerting bearish pressure on the broader market.

- Optimistic Guidance: Palo Alto anticipates annual recurring revenue for its next-gen security segment to be between $8.90 billion and $8.95 billion, suggesting a 59.5% growth potential, while total sales projections exceed analyst estimates, demonstrating confidence in future growth.

See More

Market Dynamics and Company Performance Analysis

- Market Volatility Analysis: Following the S&P 500's record high, the market is slightly fluctuating due to uncertainties surrounding Iran and tariffs, indicating investor sensitivity to geopolitical risks that may affect short-term investment decisions.

- Cybersecurity Outlook: Palo Alto Networks experienced stock volatility post-earnings, as the CEO highlighted cybersecurity risks posed by artificial intelligence, yet market confidence in its future performance remains shaky, reflecting investor caution towards tech stocks.

- Beauty Industry Growth: Ulta Beauty reported a 5.3% same-store sales growth in Q1, exceeding expectations and indicating consumer demand for value, although the stock has declined from its highs, suggesting market concerns about future growth.

- Telecom Industry Challenges: Oppenheimer downgraded AT&T to hold due to potential threats to long-term broadband subscriber growth from satellite internet competition, reflecting market worries about traditional telecom businesses and hinting at the impact of emerging technologies on the sector.

See More

Palo Alto Networks Reports Strong Q3 Earnings, Analysts Remain Positive

- Earnings Beat: Palo Alto Networks (PANW) reported fiscal Q3 results that exceeded expectations, with shares falling about 2% in premarket trading; however, analysts remain optimistic about the company's prospects, anticipating benefits from growing AI and cybersecurity demand.

- Analyst Upgrades: Jefferies raised its price target for PANW from $300 to $335, while Wedbush increased its target from $300 to $340, reflecting confidence in the company's strong competitive position and market share in the AI security space.

- Growth Expectations: Analysts noted that PANW's Net New Annual Recurring Revenue (NNARR) accelerated due to AI/SIEM/SASE tailwinds, with expectations for continued growth in FY2026, particularly driven by cross-sell synergies and an emerging AI data center narrative.

- Free Cash Flow Guidance: The company reiterated its 40% long-term free cash flow margin guidance, indicating a justified return on investment from recent M&A activities, which further bolsters market confidence in its future financial performance.

See More

Cybersecurity Industry Accelerates Transition Amid AI Advances

- Strong Earnings Report: Palo Alto Networks reported a 31% revenue increase year-over-year, despite a net loss of $177 million due to acquisitions of CyberArk and Chronosphere, indicating robust growth potential in a rapidly evolving market.

- Price Target Increases: TD Cowen raised its price target for Palo Alto from $225 to $330, reflecting optimistic expectations regarding security demand and AI momentum, suggesting sustained market confidence in the company's future performance.

- Platformization Strategy: CEO Nikesh Arora emphasized the company's implementation of a 'platformization' strategy to tackle increasingly sophisticated AI-driven threats, underscoring Palo Alto's leadership and adaptability in the industry.

- Retail Sentiment Surge: On Stocktwits, retail sentiment around Palo Alto remains 'extremely bullish', with message volume surging 696% in the past 24 hours, indicating strong investor confidence in the company's future prospects.

See More

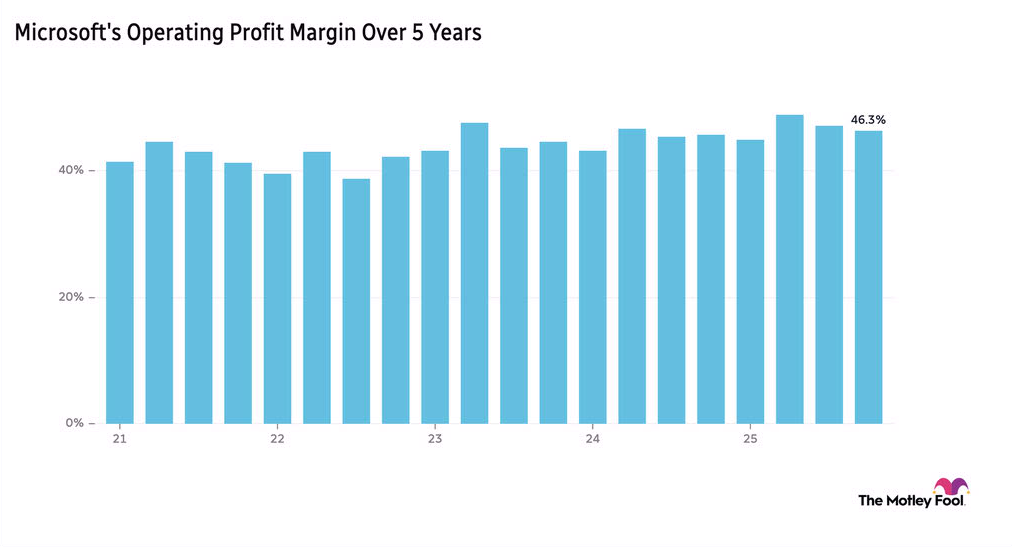

Microsoft Unveils AI Coding Tool, Pushing Tech Frontier

- AI Coding Tool Launch: Microsoft unveiled its MAI-Code-1-Flash tool at the Build conference in San Francisco, enabling non-technical users to generate software source code through text interaction, marking a significant advancement in AI, although the stock fell 4.2% on the day.

- Quantum Processor Development: The new Majorana 2 quantum processor introduced by Microsoft can stabilize qubits for 20 seconds, approximately 1,000 times longer than its predecessor, with commercial availability targeted for 2029, enhancing its competitive edge in quantum computing.

- Palo Alto's Strong Earnings: Palo Alto reported a 60% year-over-year increase in annual recurring revenue, reaching $8.13 billion, despite rising component costs, and management raised Q4 revenue guidance, indicating robust performance in the security sector.

- Ulta Beauty's Revenue Growth: Ulta Beauty reported an 11.1% year-over-year increase in Q1 revenue, with the CEO attributing growth to strong core U.S. business performance, leading to a roughly 1% rise in stock price during pre-market trading.

See More

Palo Alto Networks Q3 Results Beat Estimates Despite Stock Decline

- Strong Earnings Report: Palo Alto Networks reported an adjusted Q3 profit of $0.85 per share and a 31% revenue growth to $3 billion, both exceeding market expectations, indicating robust performance in the cybersecurity sector.

- Stock Price Decline: Despite the strong results, shares fell about 7%, as analysts expressed concerns over persistent overvaluation and dilution, which negatively impacted investor sentiment and confidence in the stock.

- Increased ETF Focus: The decline in stock price has shifted investor attention to ETFs with significant exposure to Palo Alto, such as the Direxion Daily PANW Bull 2X ETF, which has a 13.91% allocation, reflecting varying market perspectives on the company's future performance.

- Divergent Analyst Ratings: While analysts remain generally positive about Palo Alto Networks' outlook, some, like Kenio Fontes, maintain a 'sell' rating, highlighting the ongoing divergence and uncertainty regarding the company's long-term valuation in the market.

See More

Palo Alto Networks Stock Drops 6.8% Despite Strong Earnings Report

- Earnings Beat Expectations: Palo Alto Networks reported an adjusted profit of $0.85 per share and $3 billion in sales for Q3 of fiscal 2026, surpassing Wall Street forecasts, indicating strong market performance.

- Significant Sales Growth: The company experienced a 31% year-over-year sales increase, with remaining performance obligations reaching $18.4 billion, up 36%, highlighting robust future revenue potential and market demand.

- Negative Market Reaction: Despite strong earnings, the stock fell 6.8%, reflecting investor concerns about future growth amid rising oil prices and bond yields, which are exerting bearish pressure on the broader market.

- Optimistic Guidance: Palo Alto anticipates annual recurring revenue for its next-gen security segment to be between $8.90 billion and $8.95 billion, suggesting a 59.5% growth potential, while total sales projections exceed analyst estimates, demonstrating confidence in future growth.

See More

Market Dynamics and Company Performance Analysis

- Market Volatility Analysis: Following the S&P 500's record high, the market is slightly fluctuating due to uncertainties surrounding Iran and tariffs, indicating investor sensitivity to geopolitical risks that may affect short-term investment decisions.

- Cybersecurity Outlook: Palo Alto Networks experienced stock volatility post-earnings, as the CEO highlighted cybersecurity risks posed by artificial intelligence, yet market confidence in its future performance remains shaky, reflecting investor caution towards tech stocks.

- Beauty Industry Growth: Ulta Beauty reported a 5.3% same-store sales growth in Q1, exceeding expectations and indicating consumer demand for value, although the stock has declined from its highs, suggesting market concerns about future growth.

- Telecom Industry Challenges: Oppenheimer downgraded AT&T to hold due to potential threats to long-term broadband subscriber growth from satellite internet competition, reflecting market worries about traditional telecom businesses and hinting at the impact of emerging technologies on the sector.

See More

Palo Alto Networks Reports Strong Q3 Earnings, Analysts Remain Positive

- Earnings Beat: Palo Alto Networks (PANW) reported fiscal Q3 results that exceeded expectations, with shares falling about 2% in premarket trading; however, analysts remain optimistic about the company's prospects, anticipating benefits from growing AI and cybersecurity demand.

- Analyst Upgrades: Jefferies raised its price target for PANW from $300 to $335, while Wedbush increased its target from $300 to $340, reflecting confidence in the company's strong competitive position and market share in the AI security space.

- Growth Expectations: Analysts noted that PANW's Net New Annual Recurring Revenue (NNARR) accelerated due to AI/SIEM/SASE tailwinds, with expectations for continued growth in FY2026, particularly driven by cross-sell synergies and an emerging AI data center narrative.

- Free Cash Flow Guidance: The company reiterated its 40% long-term free cash flow margin guidance, indicating a justified return on investment from recent M&A activities, which further bolsters market confidence in its future financial performance.

See More

Cybersecurity Industry Accelerates Transition Amid AI Advances

- Strong Earnings Report: Palo Alto Networks reported a 31% revenue increase year-over-year, despite a net loss of $177 million due to acquisitions of CyberArk and Chronosphere, indicating robust growth potential in a rapidly evolving market.

- Price Target Increases: TD Cowen raised its price target for Palo Alto from $225 to $330, reflecting optimistic expectations regarding security demand and AI momentum, suggesting sustained market confidence in the company's future performance.

- Platformization Strategy: CEO Nikesh Arora emphasized the company's implementation of a 'platformization' strategy to tackle increasingly sophisticated AI-driven threats, underscoring Palo Alto's leadership and adaptability in the industry.

- Retail Sentiment Surge: On Stocktwits, retail sentiment around Palo Alto remains 'extremely bullish', with message volume surging 696% in the past 24 hours, indicating strong investor confidence in the company's future prospects.

See More

Microsoft Unveils AI Coding Tool, Pushing Tech Frontier

- AI Coding Tool Launch: Microsoft unveiled its MAI-Code-1-Flash tool at the Build conference in San Francisco, enabling non-technical users to generate software source code through text interaction, marking a significant advancement in AI, although the stock fell 4.2% on the day.

- Quantum Processor Development: The new Majorana 2 quantum processor introduced by Microsoft can stabilize qubits for 20 seconds, approximately 1,000 times longer than its predecessor, with commercial availability targeted for 2029, enhancing its competitive edge in quantum computing.

- Palo Alto's Strong Earnings: Palo Alto reported a 60% year-over-year increase in annual recurring revenue, reaching $8.13 billion, despite rising component costs, and management raised Q4 revenue guidance, indicating robust performance in the security sector.

- Ulta Beauty's Revenue Growth: Ulta Beauty reported an 11.1% year-over-year increase in Q1 revenue, with the CEO attributing growth to strong core U.S. business performance, leading to a roughly 1% rise in stock price during pre-market trading.

See More