Synaptics Reports Strong Q2 2026 Earnings with 13% Revenue Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 06 2026

0mins

Should l Buy SYNA?

Source: seekingalpha

- Significant Revenue Growth: Synaptics reported Q2 revenue of $302.5 million, reflecting a 13% year-over-year increase, marking the company's fifth consecutive quarter of double-digit growth, underscoring the robust performance of its Core IoT products.

- Core Product Drivers: The Core IoT segment achieved a remarkable 53% year-over-year growth, contributing to the overall performance, while non-GAAP EPS rose to $1.21, indicating the company's increasing competitiveness in the market.

- Strategic Integration: CEO Rahul Patel announced the merger of the processors and connectivity teams to better align resources and accelerate the product roadmap, thereby enhancing the efficiency of delivering integrated processor and wireless system solutions.

- Optimistic Future Outlook: The company anticipates Q3 revenues to be around $290 million, slightly below Q2 actuals, yet management remains confident in the multi-year growth outlook, particularly driven by Astra products and edge AI solutions.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SYNA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SYNA

Wall Street analysts forecast SYNA stock price to rise

11 Analyst Rating

8 Buy

3 Hold

0 Sell

Moderate Buy

Current: 83.060

Low

65.00

Averages

89.22

High

106.00

Current: 83.060

Low

65.00

Averages

89.22

High

106.00

About SYNA

Synaptics Incorporated is a developer and fabless supplier of mixed signal semiconductor solutions that enable people to engage with connected devices and data, engineering experiences throughout the home, at work, in the car and on the go. The Company's product categories include core Internet of things (IoT), enterprise and automotive, and mobile product applications. Its core IoT solutions consist of wireless connectivity (Wi-Fi, Bluetooth, Bluetooth Low Energy, Zigbee, Thread, global positioning system, and Ultra Low Energy) products, System-on-Chip (SoC), products, and its Astra family of artificial intelligence (AI)-native edge processors. Its enterprise product applications include solutions for personal computers (PCs), a range of audio and video products and solutions for enterprise workspaces. The Company's mobile product applications include smartphones, tablets, large touchscreen applications, as well as a variety of mobile, handheld, and entertainment devices.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Synaptics to Report Q3 FY2026 Financial Results on May 7, 2026

- Earnings Announcement: Synaptics will report its Q3 FY2026 financial results on May 7, 2026, after market close, reflecting the company's commitment to transparency and investor communication.

- Analyst Conference Call: A conference call will be held on the same day at 2:00 PM PT (5:00 PM ET), requiring analysts and investors to pre-register for dial-in information, indicating the company's desire to enhance direct engagement with stakeholders.

- Live and Archived Webcast: The call will be accessible via a live and archived webcast on the company's Investor Relations section, ensuring all stakeholders can access critical information, thereby improving information accessibility.

- Innovation-Driven Context: Synaptics focuses on AI at the Edge, transforming intelligent connected devices, showcasing the company's ongoing investment and potential for growth at the forefront of technology.

See More

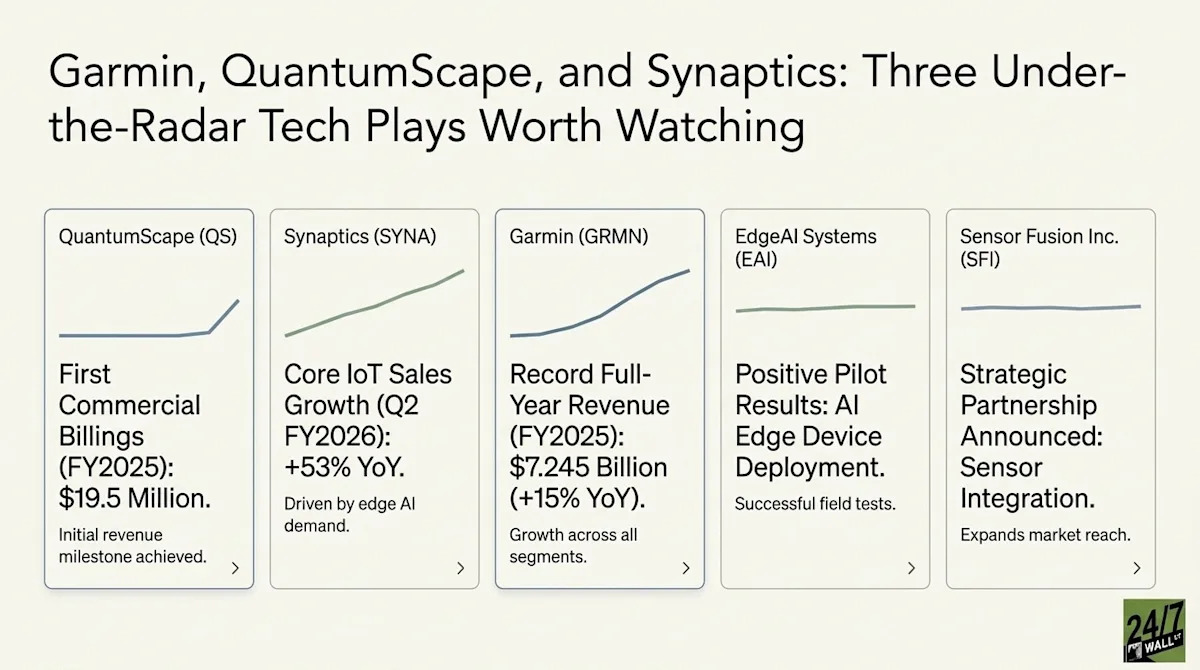

Garmin, Synaptics, and QuantumScape Report Key Financial Highlights

- Garmin Financial Performance: Garmin achieved record revenue of $7.245 billion in FY2025, a 15% year-over-year increase, with all five business segments posting record results, showcasing the company's strong market competitiveness and sustained growth potential.

- Synaptics Growth Momentum: Synaptics reported Q2 FY2026 revenue of $302.5 million, up 13% year over year, with core IoT product sales surging 53%, indicating the company's significant position in the rapidly growing edge AI market.

- QuantumScape Commercial Milestone: QuantumScape generated its first-ever customer billings of $19.5 million in FY2025, marking a successful transition from pre-revenue to commercial production, although it still faces significant losses, the technological advancements and customer base expansion indicate future growth potential.

- Capital Return Plan: Garmin announced a 17% increase in its annual dividend to $4.20 per share and authorized a new $500 million share repurchase program, reflecting the company's confidence in future performance and commitment to shareholders.

See More

Synaptics Unveils Astra Series AI Microcontrollers for Enhanced IoT Experiences

- Audio Application Innovation: The Astra™ SR80 series microcontrollers launched by Synaptics are designed for high-performance audio applications, supporting multimodal sensor fusion and intelligent processing, significantly enhancing sound quality experiences across consumer and enterprise IoT platforms, thereby strengthening market competitiveness.

- Enhanced AI Computing Power: The Astra™ SRW1500 series is among the industry's first single-chip AI microcontroller platforms with integrated Wi-Fi®7, featuring an efficient Arm®Cortex®-M52 and Arm®U55 NPU, capable of efficiently handling sensor fusion and signal processing tasks, driving the intelligent evolution of IoT networks.

- Market Standardization: The new series of microcontrollers enables customers to standardize on a single architecture in production by offering advanced features such as multimodal sensing and secure connectivity, thereby reducing development costs and accelerating time-to-market, further solidifying Synaptics' leadership in AI edge computing.

- Product Release Timeline: The Astra™ SR80 and SRW1500 series are expected to begin sampling in the second quarter of 2026, with production targeted for the last quarter of 2026, which will provide customers with faster product iterations and market responsiveness.

See More

Synaptics Launches Limited Edition Coral Dev Board for Edge AI

- Product Launch: Synaptics has unveiled a limited edition Coral Dev Board that integrates the industry's first Google Research Coral NPU, aimed at accelerating AI applications across wearables and smart home devices, thereby enhancing the company's leadership in the Edge AI market.

- Technological Innovation: The dev board features a 1 TOPS Synaptics Torq NPU, enabling fast and efficient on-device inference for all-day AI experiences in battery-constrained environments, which enhances user experience and expands market potential.

- Developer-Friendly: The Coral Dev Board provides an open environment for AI and ML engineers, supporting popular machine learning frameworks and simplifying the development process from model optimization to deployment, facilitating rapid prototyping and time-to-market.

- Strategic Partnerships: Synaptics' collaboration with Grinn Global and RS ensures production readiness and rapid prototyping capabilities for the dev board, further solidifying its strategic position within the Edge AI ecosystem.

See More

Synaptics Unveils Next-Gen AI Microcontrollers for Edge Applications

- Product Innovation: Synaptics has launched the Astra™ SR80 and SRW1500 series microcontrollers, designed for high-performance audio applications, supporting multimodal sensing and intelligent processing, which is expected to enhance user experience and market competitiveness in IoT devices.

- Technical Advantages: The SR80 series features a highly integrated architecture combining an Arm® Cortex®-M33 core and audio CODEC, enabling efficient voice interaction and personalized experiences, which is anticipated to accelerate time-to-market and meet the demand for audio quality in the market.

- Wireless Connectivity: The SRW1500 series is among the industry's first single-chip AI microcontroller platforms with integrated Wi-Fi®7, supporting efficient edge computing and sensor fusion, expected to drive the intelligence and security of IoT networks, enhancing user connectivity experiences.

- Market Outlook: The new microcontroller series is expected to begin sampling in Q2 2026, with production targeted for the last quarter of 2026, marking Synaptics' continued investment and market expansion in the AI and IoT sectors.

See More

Synaptics Launches Limited Edition Coral Dev Board for Edge AI Development

- Product Innovation: Synaptics' limited edition Coral Dev Board integrates the industry's first Google Coral NPU with 1 TOPS Synaptics Torq NPU, aimed at accelerating AI applications across wearables and smart home devices, enhancing user experience and driving market demand.

- Developer Friendly: The dev board supports various hardware interfaces, including camera, display, and Wi-Fi/Bluetooth connectivity, designed for AI and ML engineers, providing an open experimental environment that facilitates rapid prototyping and helps companies shorten time-to-market.

- Partnership Strategy: The board, launched in collaboration with Grinn Global and RS, comes pre-configured with the Gemma 3 270M model, enabling immediate support for generative and perception-based AI workloads, showcasing the company's strategic positioning and market orientation in the Edge AI space.

- Market Showcase: Synaptics will showcase the dev board at the Embedded World 2026 exhibition, further enhancing brand visibility and attracting global developer interest, promoting the adoption and application of Edge AI technologies.

See More

Synaptics to Report Q3 FY2026 Financial Results on May 7, 2026

- Earnings Announcement: Synaptics will report its Q3 FY2026 financial results on May 7, 2026, after market close, reflecting the company's commitment to transparency and investor communication.

- Analyst Conference Call: A conference call will be held on the same day at 2:00 PM PT (5:00 PM ET), requiring analysts and investors to pre-register for dial-in information, indicating the company's desire to enhance direct engagement with stakeholders.

- Live and Archived Webcast: The call will be accessible via a live and archived webcast on the company's Investor Relations section, ensuring all stakeholders can access critical information, thereby improving information accessibility.

- Innovation-Driven Context: Synaptics focuses on AI at the Edge, transforming intelligent connected devices, showcasing the company's ongoing investment and potential for growth at the forefront of technology.

See More

Garmin, Synaptics, and QuantumScape Report Key Financial Highlights

- Garmin Financial Performance: Garmin achieved record revenue of $7.245 billion in FY2025, a 15% year-over-year increase, with all five business segments posting record results, showcasing the company's strong market competitiveness and sustained growth potential.

- Synaptics Growth Momentum: Synaptics reported Q2 FY2026 revenue of $302.5 million, up 13% year over year, with core IoT product sales surging 53%, indicating the company's significant position in the rapidly growing edge AI market.

- QuantumScape Commercial Milestone: QuantumScape generated its first-ever customer billings of $19.5 million in FY2025, marking a successful transition from pre-revenue to commercial production, although it still faces significant losses, the technological advancements and customer base expansion indicate future growth potential.

- Capital Return Plan: Garmin announced a 17% increase in its annual dividend to $4.20 per share and authorized a new $500 million share repurchase program, reflecting the company's confidence in future performance and commitment to shareholders.

See More

Synaptics Unveils Astra Series AI Microcontrollers for Enhanced IoT Experiences

- Audio Application Innovation: The Astra™ SR80 series microcontrollers launched by Synaptics are designed for high-performance audio applications, supporting multimodal sensor fusion and intelligent processing, significantly enhancing sound quality experiences across consumer and enterprise IoT platforms, thereby strengthening market competitiveness.

- Enhanced AI Computing Power: The Astra™ SRW1500 series is among the industry's first single-chip AI microcontroller platforms with integrated Wi-Fi®7, featuring an efficient Arm®Cortex®-M52 and Arm®U55 NPU, capable of efficiently handling sensor fusion and signal processing tasks, driving the intelligent evolution of IoT networks.

- Market Standardization: The new series of microcontrollers enables customers to standardize on a single architecture in production by offering advanced features such as multimodal sensing and secure connectivity, thereby reducing development costs and accelerating time-to-market, further solidifying Synaptics' leadership in AI edge computing.

- Product Release Timeline: The Astra™ SR80 and SRW1500 series are expected to begin sampling in the second quarter of 2026, with production targeted for the last quarter of 2026, which will provide customers with faster product iterations and market responsiveness.

See More

Synaptics Launches Limited Edition Coral Dev Board for Edge AI

- Product Launch: Synaptics has unveiled a limited edition Coral Dev Board that integrates the industry's first Google Research Coral NPU, aimed at accelerating AI applications across wearables and smart home devices, thereby enhancing the company's leadership in the Edge AI market.

- Technological Innovation: The dev board features a 1 TOPS Synaptics Torq NPU, enabling fast and efficient on-device inference for all-day AI experiences in battery-constrained environments, which enhances user experience and expands market potential.

- Developer-Friendly: The Coral Dev Board provides an open environment for AI and ML engineers, supporting popular machine learning frameworks and simplifying the development process from model optimization to deployment, facilitating rapid prototyping and time-to-market.

- Strategic Partnerships: Synaptics' collaboration with Grinn Global and RS ensures production readiness and rapid prototyping capabilities for the dev board, further solidifying its strategic position within the Edge AI ecosystem.

See More

Synaptics Unveils Next-Gen AI Microcontrollers for Edge Applications

- Product Innovation: Synaptics has launched the Astra™ SR80 and SRW1500 series microcontrollers, designed for high-performance audio applications, supporting multimodal sensing and intelligent processing, which is expected to enhance user experience and market competitiveness in IoT devices.

- Technical Advantages: The SR80 series features a highly integrated architecture combining an Arm® Cortex®-M33 core and audio CODEC, enabling efficient voice interaction and personalized experiences, which is anticipated to accelerate time-to-market and meet the demand for audio quality in the market.

- Wireless Connectivity: The SRW1500 series is among the industry's first single-chip AI microcontroller platforms with integrated Wi-Fi®7, supporting efficient edge computing and sensor fusion, expected to drive the intelligence and security of IoT networks, enhancing user connectivity experiences.

- Market Outlook: The new microcontroller series is expected to begin sampling in Q2 2026, with production targeted for the last quarter of 2026, marking Synaptics' continued investment and market expansion in the AI and IoT sectors.

See More

Synaptics Launches Limited Edition Coral Dev Board for Edge AI Development

- Product Innovation: Synaptics' limited edition Coral Dev Board integrates the industry's first Google Coral NPU with 1 TOPS Synaptics Torq NPU, aimed at accelerating AI applications across wearables and smart home devices, enhancing user experience and driving market demand.

- Developer Friendly: The dev board supports various hardware interfaces, including camera, display, and Wi-Fi/Bluetooth connectivity, designed for AI and ML engineers, providing an open experimental environment that facilitates rapid prototyping and helps companies shorten time-to-market.

- Partnership Strategy: The board, launched in collaboration with Grinn Global and RS, comes pre-configured with the Gemma 3 270M model, enabling immediate support for generative and perception-based AI workloads, showcasing the company's strategic positioning and market orientation in the Edge AI space.

- Market Showcase: Synaptics will showcase the dev board at the Embedded World 2026 exhibition, further enhancing brand visibility and attracting global developer interest, promoting the adoption and application of Edge AI technologies.

See More