REFILE-BUZZ-ROYAL UNIBREW EXPERIENCES LOWEST PERFORMANCE IN 17 YEARS FOLLOWING END OF NORTHERN EUROPE CONTRACT WITH PEPSI

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 21 2026

0mins

Source: moomoo

Refile Buzz: The article discusses the recent performance of Royal Unibrew, highlighting it as the worst day in 17 years for the company.

Northern Europe Contract: It mentions the impact of the Northern Europe contract with PepsiCo, which has contributed to the company's current challenges.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PEP?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PEP

Wall Street analysts forecast PEP stock price to rise

12 Analyst Rating

6 Buy

6 Hold

0 Sell

Moderate Buy

Current: 149.290

Low

144.00

Averages

161.90

High

172.00

Current: 149.290

Low

144.00

Averages

161.90

High

172.00

About PEP

PepsiCo, Inc. is a global beverage and convenient food company. The Company’s segments include PepsiCo Foods North America (PFNA), PepsiCo Beverages North America (PBNA), International Beverages Franchise (IB Franchise), Europe, Middle East and Africa (EMEA), Latin America Foods (LatAm Foods), and Asia Pacific Foods. PFNA segment includes all of its convenient food businesses in the United States and Canada. PBNA segment includes all of its beverage businesses in the United States and Canada. IB Franchise segment includes its international franchise beverage businesses, as well as its SodaStream business. EMEA segment includes its convenient food businesses and beverage businesses with Company-owned bottlers in Europe, the Middle East and Africa. LatAm Foods segment includes all of its convenient food businesses in Latin America. Asia Pacific Foods segment consists of its convenient food businesses in Asia Pacific, including China, Australia and New Zealand, as well as India.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

PepsiCo Plans Price Hike on Chips Amid Rising Costs

- Reason for Price Increase: PepsiCo is preparing to raise prices on some smaller bags of chips by 10 to 20 cents due to rising production, distribution, and retail costs in the U.S., indicating a strategic adjustment to manage cost pressures.

- Product Scope: The price hike will affect certain single-serve bags currently retailing at $2.69, along with smaller bags often sold at two for $1, demonstrating the company's commitment to maintaining profitability amidst rising costs.

- Timeline for Implementation: The price increases are expected to take effect in the coming weeks, with some single-serve products seeing price adjustments starting in late June, reflecting the company's sensitivity to market dynamics and its ability to respond quickly.

- Market Performance: Despite the impending price hikes, PepsiCo exceeded Wall Street estimates in April, partly due to previous price cuts on salty snacks in the U.S., showcasing the company's flexibility in price management.

See More

PepsiCo Plans Price Increase on Small Chip Bags

- Price Increase Plan: PepsiCo is set to raise prices on certain small bags of chips by $0.10 to $0.20, expected to take effect in late June, as a response to rising production, distribution, and retail costs in the U.S.

- Historical Price Stability: Some single-serve chip prices have remained unchanged for nearly 15 years, and this price hike reflects the company's reaction to cost pressures, which may influence consumer purchasing decisions.

- First Quarter Performance: PepsiCo's convenient food segment showed strong results in Q1, with revenue increasing by 8.5% year-over-year to $19.4 billion, surpassing market expectations, indicating the company's adaptability post-price adjustments.

- Regional Sales Disparity: While total food volume rose by 4%, the North America food segment only grew by 1%, contrasting with a 7% increase in the Europe, Middle East, and Africa segment, highlighting the need for strategic adjustments across different markets.

See More

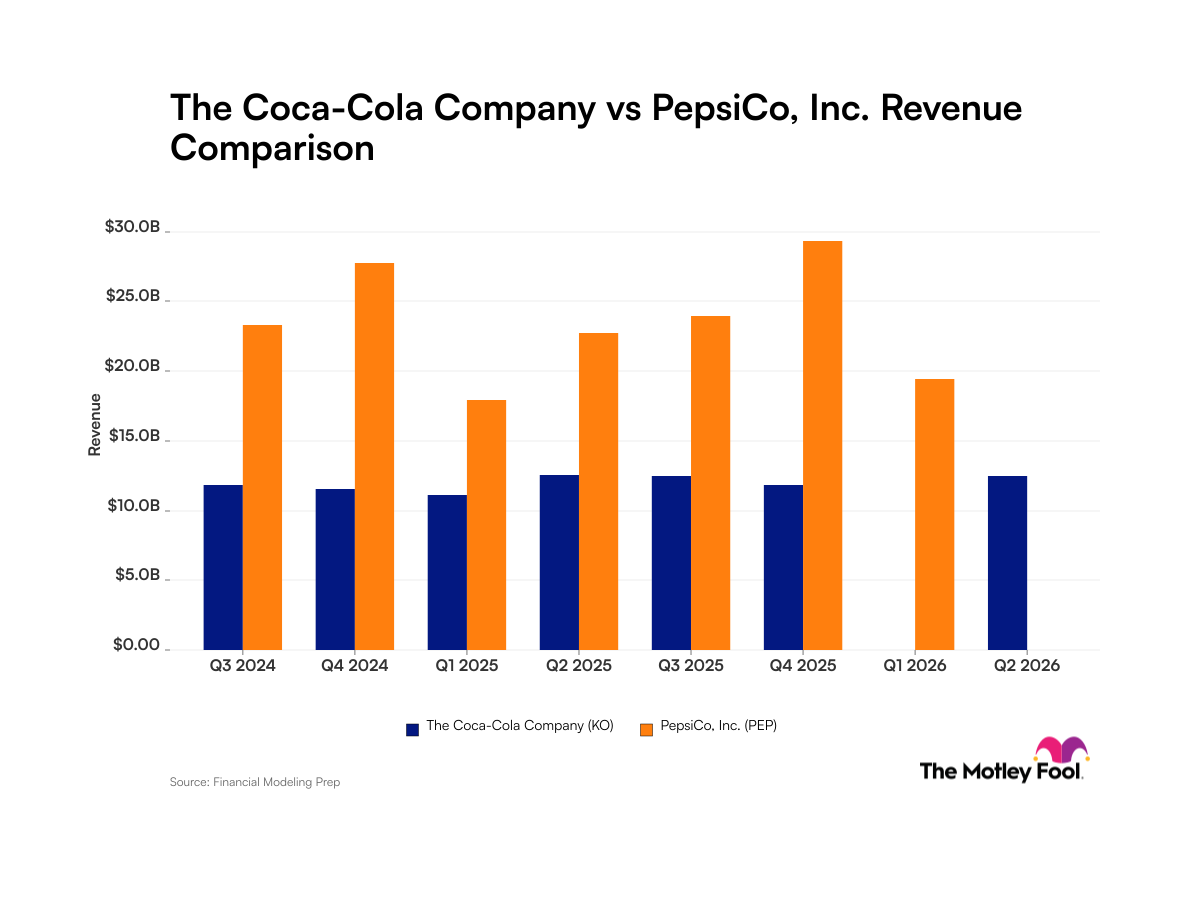

Coca-Cola vs. PepsiCo Revenue Comparison

- Revenue Stability: Coca-Cola generated $49 billion in revenue over the past 12 months with a net income margin of approximately 32%, showcasing its strong competitive position and stable profitability in the beverage market, reflecting its high-margin business model.

- PepsiCo's Volatility: PepsiCo's revenue reached $95 billion during the same period, but with a net income margin of only 12%, its diversified business leads to greater revenue fluctuations, indicating uncertainty in its market performance.

- Investment Return Performance: Over the past two years, Coca-Cola's stock has risen by 36%, while PepsiCo's has declined by 12%, demonstrating Coca-Cola's superior performance in terms of investor returns, thereby attracting more investor interest.

- Future Growth Potential: Although PepsiCo generates nearly double the annual revenue of Coca-Cola, its investments in product development and cost efficiency will be crucial in determining whether it can enhance earnings growth and drive stock price increases in the future.

See More

Financial Comparison of Coca-Cola and PepsiCo

- Revenue Performance Difference: Coca-Cola generated $49 billion in revenue over the past 12 months, while PepsiCo reached $95 billion; despite PepsiCo's higher revenue, Coca-Cola's stability makes it more attractive to investors.

- Profit Margin Comparison: Coca-Cola's net income margin stands at approximately 32%, significantly higher than PepsiCo's 12%, reflecting Coca-Cola's advantage in high-margin syrup sales and the effectiveness of its business model.

- Market Performance: Over the past two years, Coca-Cola's stock has risen by 36%, while PepsiCo has seen a 12% decline, indicating that Coca-Cola has delivered better returns to investors, drawing more attention.

- Future Investment Directions: PepsiCo is investing in product development and AI capabilities to boost earnings growth; although the revenue gap is substantial, improving profit margins could positively impact its stock price.

See More

PepsiCo's One-Year Review of Poppi Acquisition

- Brand Integration Success: Since acquiring Poppi, PepsiCo (PEP) has rapidly elevated the brand from a fast-growing niche to a mainstream player, leveraging its distribution and marketing capabilities to enhance its presence in the functional beverage market.

- Revenue Growth Driver: Although PepsiCo does not disclose Poppi's results separately, commentary from its North America beverages business indicates that Poppi has contributed to high single-digit revenue growth, highlighting its market success.

- Accelerated International Expansion: Poppi has begun its international expansion, notably launching in the UK, which further strengthens PepsiCo's competitive position in the global health beverage market and aligns with its strategy for positive-choice offerings.

- Future Investment Strategy: PepsiCo is expected to continue investing in Poppi as a strategic platform rather than merely an add-on product, demonstrating a long-term commitment to the health beverage market.

See More

Barfresh Food Group Reports 92% Revenue Growth, Positioned for 2H26 Inflection

- Significant Revenue Growth: Barfresh Food Group reported a 92% year-over-year revenue increase to $5.6 million in Q1 2026, exceeding management's guidance of $5.0-$5.2 million, primarily driven by strong contributions from Arps Dairy, indicating the company's potential in market recovery.

- Margin Pressure: Despite revenue growth, gross margin declined from 31% to 18%, mainly due to a lower-margin milk mix and startup costs associated with the new facility, reflecting profitability challenges during the transition phase.

- Education Market Recovery: The recovery of customers in the education sector and momentum from large districts suggest a stronger performance in the second half of 2026, particularly as school orders ramp up, indicating a rebound in demand for core products.

- Strategic Investment and Expansion: Barfresh aims to commission its 44,000-square-foot Defiance facility by the end of 2026, which will significantly enhance production capacity and flexibility to support future growth objectives, while also securing a $2.4 million government grant and $7.5 million in convertible note financing to aid facility development.

See More

PepsiCo Plans Price Hike on Chips Amid Rising Costs

- Reason for Price Increase: PepsiCo is preparing to raise prices on some smaller bags of chips by 10 to 20 cents due to rising production, distribution, and retail costs in the U.S., indicating a strategic adjustment to manage cost pressures.

- Product Scope: The price hike will affect certain single-serve bags currently retailing at $2.69, along with smaller bags often sold at two for $1, demonstrating the company's commitment to maintaining profitability amidst rising costs.

- Timeline for Implementation: The price increases are expected to take effect in the coming weeks, with some single-serve products seeing price adjustments starting in late June, reflecting the company's sensitivity to market dynamics and its ability to respond quickly.

- Market Performance: Despite the impending price hikes, PepsiCo exceeded Wall Street estimates in April, partly due to previous price cuts on salty snacks in the U.S., showcasing the company's flexibility in price management.

See More

PepsiCo Plans Price Increase on Small Chip Bags

- Price Increase Plan: PepsiCo is set to raise prices on certain small bags of chips by $0.10 to $0.20, expected to take effect in late June, as a response to rising production, distribution, and retail costs in the U.S.

- Historical Price Stability: Some single-serve chip prices have remained unchanged for nearly 15 years, and this price hike reflects the company's reaction to cost pressures, which may influence consumer purchasing decisions.

- First Quarter Performance: PepsiCo's convenient food segment showed strong results in Q1, with revenue increasing by 8.5% year-over-year to $19.4 billion, surpassing market expectations, indicating the company's adaptability post-price adjustments.

- Regional Sales Disparity: While total food volume rose by 4%, the North America food segment only grew by 1%, contrasting with a 7% increase in the Europe, Middle East, and Africa segment, highlighting the need for strategic adjustments across different markets.

See More

Coca-Cola vs. PepsiCo Revenue Comparison

- Revenue Stability: Coca-Cola generated $49 billion in revenue over the past 12 months with a net income margin of approximately 32%, showcasing its strong competitive position and stable profitability in the beverage market, reflecting its high-margin business model.

- PepsiCo's Volatility: PepsiCo's revenue reached $95 billion during the same period, but with a net income margin of only 12%, its diversified business leads to greater revenue fluctuations, indicating uncertainty in its market performance.

- Investment Return Performance: Over the past two years, Coca-Cola's stock has risen by 36%, while PepsiCo's has declined by 12%, demonstrating Coca-Cola's superior performance in terms of investor returns, thereby attracting more investor interest.

- Future Growth Potential: Although PepsiCo generates nearly double the annual revenue of Coca-Cola, its investments in product development and cost efficiency will be crucial in determining whether it can enhance earnings growth and drive stock price increases in the future.

See More

Financial Comparison of Coca-Cola and PepsiCo

- Revenue Performance Difference: Coca-Cola generated $49 billion in revenue over the past 12 months, while PepsiCo reached $95 billion; despite PepsiCo's higher revenue, Coca-Cola's stability makes it more attractive to investors.

- Profit Margin Comparison: Coca-Cola's net income margin stands at approximately 32%, significantly higher than PepsiCo's 12%, reflecting Coca-Cola's advantage in high-margin syrup sales and the effectiveness of its business model.

- Market Performance: Over the past two years, Coca-Cola's stock has risen by 36%, while PepsiCo has seen a 12% decline, indicating that Coca-Cola has delivered better returns to investors, drawing more attention.

- Future Investment Directions: PepsiCo is investing in product development and AI capabilities to boost earnings growth; although the revenue gap is substantial, improving profit margins could positively impact its stock price.

See More

PepsiCo's One-Year Review of Poppi Acquisition

- Brand Integration Success: Since acquiring Poppi, PepsiCo (PEP) has rapidly elevated the brand from a fast-growing niche to a mainstream player, leveraging its distribution and marketing capabilities to enhance its presence in the functional beverage market.

- Revenue Growth Driver: Although PepsiCo does not disclose Poppi's results separately, commentary from its North America beverages business indicates that Poppi has contributed to high single-digit revenue growth, highlighting its market success.

- Accelerated International Expansion: Poppi has begun its international expansion, notably launching in the UK, which further strengthens PepsiCo's competitive position in the global health beverage market and aligns with its strategy for positive-choice offerings.

- Future Investment Strategy: PepsiCo is expected to continue investing in Poppi as a strategic platform rather than merely an add-on product, demonstrating a long-term commitment to the health beverage market.

See More

Barfresh Food Group Reports 92% Revenue Growth, Positioned for 2H26 Inflection

- Significant Revenue Growth: Barfresh Food Group reported a 92% year-over-year revenue increase to $5.6 million in Q1 2026, exceeding management's guidance of $5.0-$5.2 million, primarily driven by strong contributions from Arps Dairy, indicating the company's potential in market recovery.

- Margin Pressure: Despite revenue growth, gross margin declined from 31% to 18%, mainly due to a lower-margin milk mix and startup costs associated with the new facility, reflecting profitability challenges during the transition phase.

- Education Market Recovery: The recovery of customers in the education sector and momentum from large districts suggest a stronger performance in the second half of 2026, particularly as school orders ramp up, indicating a rebound in demand for core products.

- Strategic Investment and Expansion: Barfresh aims to commission its 44,000-square-foot Defiance facility by the end of 2026, which will significantly enhance production capacity and flexibility to support future growth objectives, while also securing a $2.4 million government grant and $7.5 million in convertible note financing to aid facility development.

See More