Raises FY26 Adjusted EBITDA Outlook to Over $235M

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Should l Buy GDRX?

Consensus $764.78M. Raises FY26 adjusted EBITDA view to over $235M from over $230M.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GDRX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GDRX

Wall Street analysts forecast GDRX stock price to rise

10 Analyst Rating

4 Buy

4 Hold

2 Sell

Hold

Current: 2.840

Low

2.60

Averages

4.46

High

7.00

Current: 2.840

Low

2.60

Averages

4.46

High

7.00

About GDRX

GoodRx Holdings, Inc. is a platform for medication savings in the United States, used by consumers and healthcare professionals. The Company connects consumers, healthcare professionals, payers, pharmacy benefit managers (PBMs), pharma manufacturers, and retail pharmacies to make saving on medications easier. The Company's offerings include prescription marketplace and pharma manufacturer solutions. Its prescription marketplace consists of its prescription transactions offering and its supplemental subscription and telehealth offerings. Through its GoodRx Care platform, the Company offers consumers access to telehealth visits on a cash-pay basis outside of insurance. The Company partners with pharma manufacturers to advertise and integrate their affordable solutions into its platform. These solutions, provided by pharma manufacturers, include co-pay cards, patient assistance programs, care portals, and other savings options to ensure consumers can access their medications.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

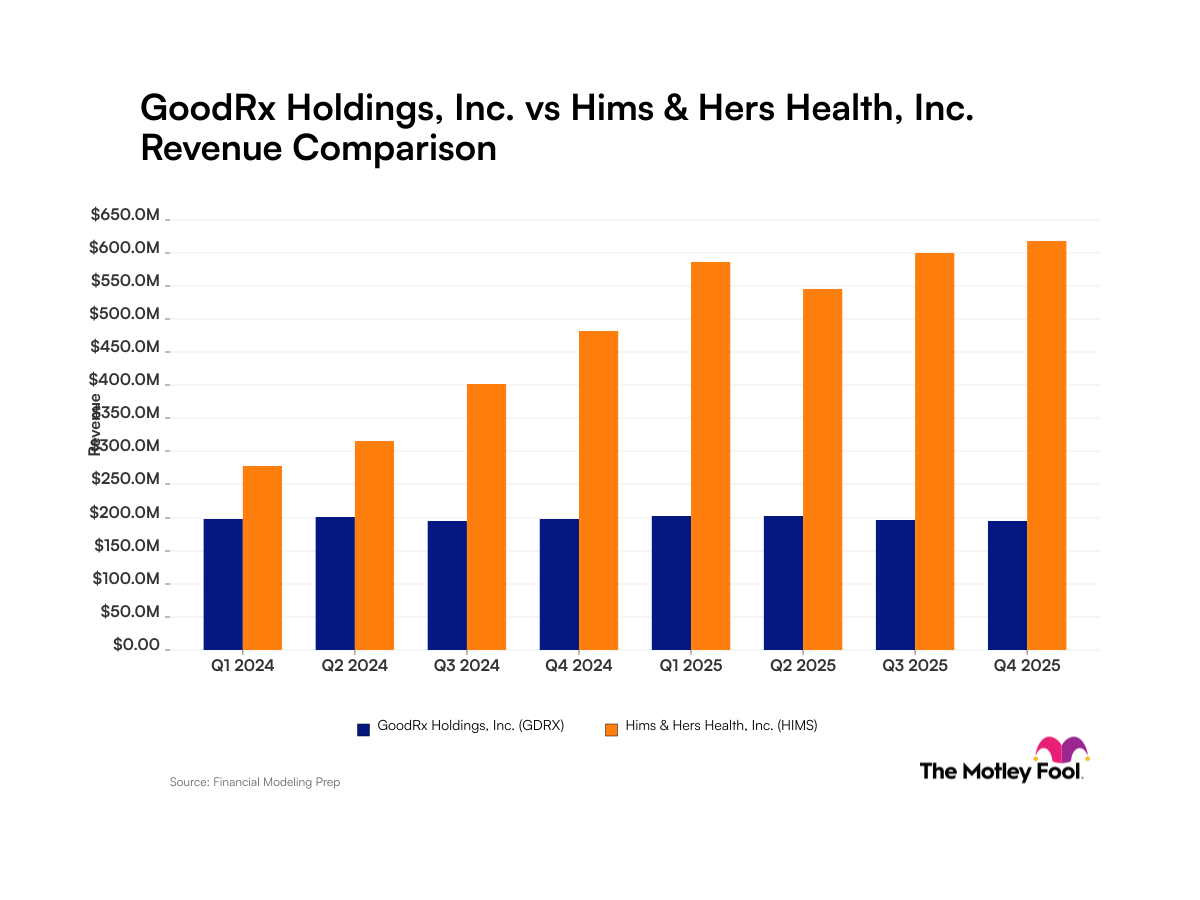

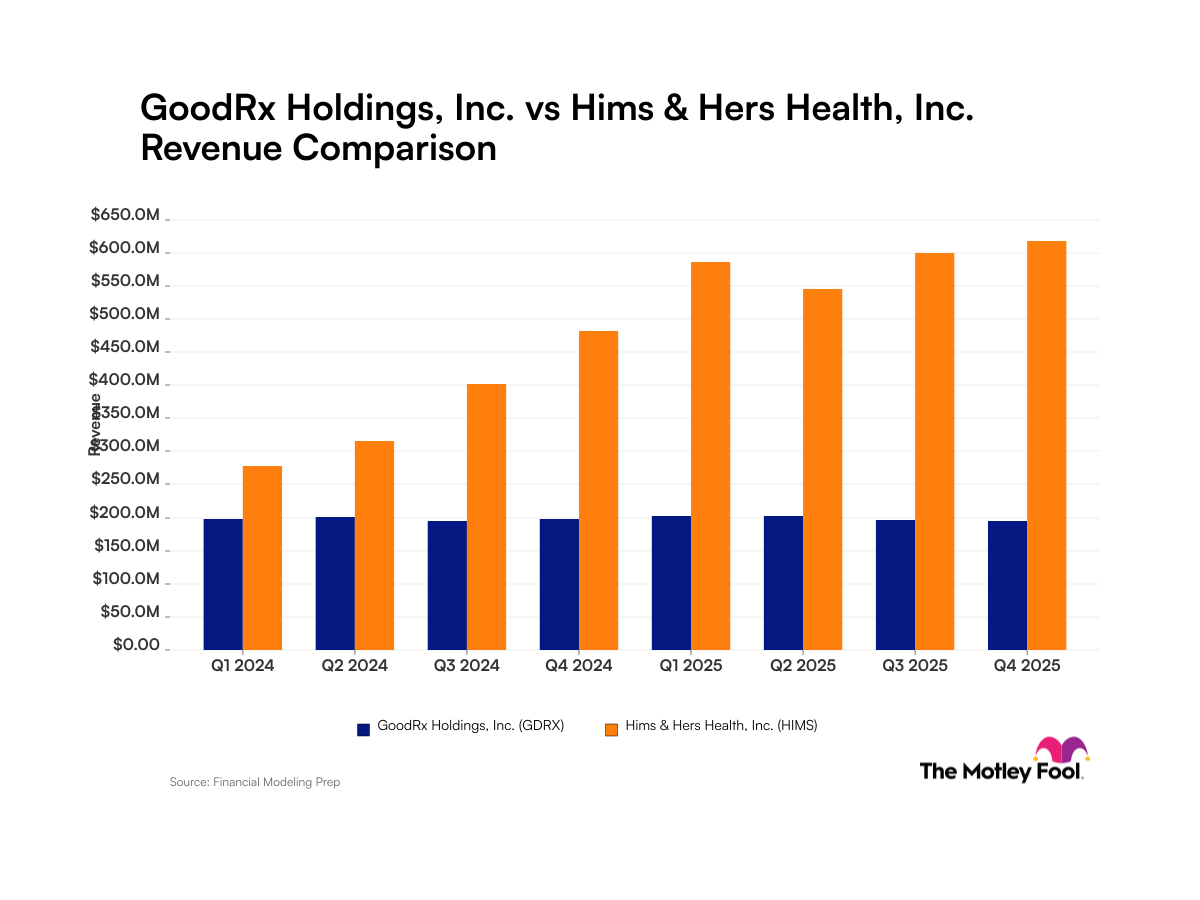

Hims & Hers Health Continues to Outperform GoodRx in Revenue Growth

- Revenue Growth Comparison: Hims & Hers Health has demonstrated consistent revenue growth, with a 59% year-over-year increase in Q4 2025, while GoodRx reported a 4.4% decline in the same period, indicating a stronger competitive position for Hims & Hers in the market.

- Margin Discrepancy: Hims & Hers Health achieved approximately 72% gross margin in Q4 2025, compared to GoodRx's 21% EBIT margin, reflecting significant operational efficiency and profitability advantages that may attract more investor interest.

- Market Dynamics Shift: With the average annual cost of family health plans reaching $27,000 in 2026, fewer Americans have access to primary care, providing a strong market tailwind for Hims & Hers Health's alternative platform, further expanding its market share.

- Investor Focus: GoodRx's Pharma Direct business saw an 82% year-over-year growth in Q1, and while overall revenue stagnated, this segment's performance may capture investor attention, indicating growth potential in specific areas.

See More

GoodRx and Hims & Hers Financial Report Analysis

- GoodRx Revenue Trends: GoodRx reported a 4.4% year-over-year decline in Q1 2026 sales to $194 million, yet its Pharma Direct business surged 82% to $52 million, accounting for 27% of total revenue, indicating potential growth amidst a competitive landscape.

- Hims & Hers Growth Performance: Hims & Hers achieved a remarkable 59% year-over-year revenue increase in Q4 2025, reaching $617.8 million, alongside a 13% growth in subscribers, showcasing strong demand in the telehealth sector.

- Market Environment Impact: With the average annual cost of family health plans hitting $27,000 in 2026, fewer Americans have access to primary care, providing robust market support for Hims & Hers' alternative platform, further driving revenue growth.

- Investor Reaction: GoodRx's stock rose over 10% following its Q1 earnings report, reflecting investor optimism regarding its Pharma Direct business, despite overall revenue stagnation, indicating sustained confidence in future growth prospects.

See More

GoodRx vs Hims & Hers: Revenue Stagnation vs Growth

- GoodRx Revenue Trends: GoodRx reported a 4.4% year-over-year decline in Q1 2026 sales to $194 million, yet its Pharma Direct business saw an impressive 82% growth, contributing approximately 27% to total revenue, indicating potential amidst stagnation.

- Hims & Hers Growth Performance: Hims & Hers achieved a remarkable 59% year-over-year revenue increase in Q4 2025, reaching $617.8 million, alongside a 13% growth in subscribers, showcasing its strong market position and consumer appeal.

- Market Environment Impact: With the average annual cost of family health plans hitting $27,000 in 2026, fewer Americans have access to primary care, creating a robust tailwind for Hims & Hers' alternative platform, further driving its business growth.

- Investor Considerations: Despite GoodRx's revenue stagnation, the Motley Fool analyst team did not include it in their current top investment stocks list, reflecting a cautious market sentiment regarding its future performance, prompting investors to carefully assess its investment value.

See More

GoodRx Q1 2026 Earnings Call Highlights

- Significant Revenue Growth: GoodRx reported $194 million in revenue for Q1 2026, with adjusted EBITDA of $58.3 million, achieving a 30% adjusted EBITDA margin, indicating robust execution on profitability.

- Strong Pharma Direct Growth: GoodRx Pharma Direct experienced an 82% year-over-year growth, with over 125 self-pay programs live, establishing itself as a key growth engine expected to drive future revenue increases.

- Upward Guidance Revision: CFO McGinnis raised the full-year 2026 revenue guidance to a range of $765 million to $785 million, with adjusted EBITDA expected to be at least $235 million, reflecting optimism about Pharma Direct's performance.

- Ongoing Prescription Transaction Pressure: Despite a 24% year-over-year decline in prescription transaction revenue to $113.7 million, management views this trend as aligned with internal expectations, emphasizing that growth in Pharma Direct and subscription services will offset this impact.

See More

GoodRx Q1 Earnings Beat Expectations Amid Revenue Decline

- Earnings Highlights: GoodRx reported a Q1 non-GAAP EPS of $0.07, meeting expectations, while revenue of $194 million, down 4.4% year-over-year, beat forecasts by $8.59 million, indicating resilience in profitability despite challenges.

- Annual Outlook: Management anticipates FY 2026 revenue between $765 million and $785 million, representing a decline of 1% to 4% from FY 2025's $796.9 million, reflecting intensified market competition and shifts in consumer demand.

- Adjusted EBITDA Forecast: The company expects adjusted EBITDA to exceed $235 million for FY 2026, showcasing strong cost control capabilities despite revenue pressures, potentially laying the groundwork for future profit growth.

- Market Reaction: Despite the earnings beat, market sentiment towards GoodRx is waning, indicating a diminishing relevance of its services among consumers, which could impact future user growth and market share.

See More

GoodRx Launches Oral Ozempic® Treatment for Diabetes

- Transparent Pricing: GoodRx offers Novo Nordisk's Ozempic® oral medication to eligible self-pay patients at a monthly cost starting at $149, significantly reducing financial barriers and enhancing medication accessibility for diabetes patients.

- Market Expansion Strategy: By introducing the oral Ozempic through its nationwide pharmacy network, GoodRx not only diversifies its medication portfolio but also strengthens its partnership with Novo Nordisk, solidifying its position in the diabetes treatment market.

- Increased Patient Convenience: The launch of the oral formulation provides patients with a more convenient alternative to traditional injections, which is expected to attract more users and drive growth in GoodRx's user base and market share.

- Enhanced Industry Influence: This initiative signifies GoodRx's evolution from a pricing solution to a broader consumer access platform, enabling pharmaceutical companies to connect directly with patients and deliver transparent pricing, thereby improving overall healthcare service efficiency.

See More

Hims & Hers Health Continues to Outperform GoodRx in Revenue Growth

- Revenue Growth Comparison: Hims & Hers Health has demonstrated consistent revenue growth, with a 59% year-over-year increase in Q4 2025, while GoodRx reported a 4.4% decline in the same period, indicating a stronger competitive position for Hims & Hers in the market.

- Margin Discrepancy: Hims & Hers Health achieved approximately 72% gross margin in Q4 2025, compared to GoodRx's 21% EBIT margin, reflecting significant operational efficiency and profitability advantages that may attract more investor interest.

- Market Dynamics Shift: With the average annual cost of family health plans reaching $27,000 in 2026, fewer Americans have access to primary care, providing a strong market tailwind for Hims & Hers Health's alternative platform, further expanding its market share.

- Investor Focus: GoodRx's Pharma Direct business saw an 82% year-over-year growth in Q1, and while overall revenue stagnated, this segment's performance may capture investor attention, indicating growth potential in specific areas.

See More

GoodRx and Hims & Hers Financial Report Analysis

- GoodRx Revenue Trends: GoodRx reported a 4.4% year-over-year decline in Q1 2026 sales to $194 million, yet its Pharma Direct business surged 82% to $52 million, accounting for 27% of total revenue, indicating potential growth amidst a competitive landscape.

- Hims & Hers Growth Performance: Hims & Hers achieved a remarkable 59% year-over-year revenue increase in Q4 2025, reaching $617.8 million, alongside a 13% growth in subscribers, showcasing strong demand in the telehealth sector.

- Market Environment Impact: With the average annual cost of family health plans hitting $27,000 in 2026, fewer Americans have access to primary care, providing robust market support for Hims & Hers' alternative platform, further driving revenue growth.

- Investor Reaction: GoodRx's stock rose over 10% following its Q1 earnings report, reflecting investor optimism regarding its Pharma Direct business, despite overall revenue stagnation, indicating sustained confidence in future growth prospects.

See More

GoodRx vs Hims & Hers: Revenue Stagnation vs Growth

- GoodRx Revenue Trends: GoodRx reported a 4.4% year-over-year decline in Q1 2026 sales to $194 million, yet its Pharma Direct business saw an impressive 82% growth, contributing approximately 27% to total revenue, indicating potential amidst stagnation.

- Hims & Hers Growth Performance: Hims & Hers achieved a remarkable 59% year-over-year revenue increase in Q4 2025, reaching $617.8 million, alongside a 13% growth in subscribers, showcasing its strong market position and consumer appeal.

- Market Environment Impact: With the average annual cost of family health plans hitting $27,000 in 2026, fewer Americans have access to primary care, creating a robust tailwind for Hims & Hers' alternative platform, further driving its business growth.

- Investor Considerations: Despite GoodRx's revenue stagnation, the Motley Fool analyst team did not include it in their current top investment stocks list, reflecting a cautious market sentiment regarding its future performance, prompting investors to carefully assess its investment value.

See More

GoodRx Q1 2026 Earnings Call Highlights

- Significant Revenue Growth: GoodRx reported $194 million in revenue for Q1 2026, with adjusted EBITDA of $58.3 million, achieving a 30% adjusted EBITDA margin, indicating robust execution on profitability.

- Strong Pharma Direct Growth: GoodRx Pharma Direct experienced an 82% year-over-year growth, with over 125 self-pay programs live, establishing itself as a key growth engine expected to drive future revenue increases.

- Upward Guidance Revision: CFO McGinnis raised the full-year 2026 revenue guidance to a range of $765 million to $785 million, with adjusted EBITDA expected to be at least $235 million, reflecting optimism about Pharma Direct's performance.

- Ongoing Prescription Transaction Pressure: Despite a 24% year-over-year decline in prescription transaction revenue to $113.7 million, management views this trend as aligned with internal expectations, emphasizing that growth in Pharma Direct and subscription services will offset this impact.

See More

GoodRx Q1 Earnings Beat Expectations Amid Revenue Decline

- Earnings Highlights: GoodRx reported a Q1 non-GAAP EPS of $0.07, meeting expectations, while revenue of $194 million, down 4.4% year-over-year, beat forecasts by $8.59 million, indicating resilience in profitability despite challenges.

- Annual Outlook: Management anticipates FY 2026 revenue between $765 million and $785 million, representing a decline of 1% to 4% from FY 2025's $796.9 million, reflecting intensified market competition and shifts in consumer demand.

- Adjusted EBITDA Forecast: The company expects adjusted EBITDA to exceed $235 million for FY 2026, showcasing strong cost control capabilities despite revenue pressures, potentially laying the groundwork for future profit growth.

- Market Reaction: Despite the earnings beat, market sentiment towards GoodRx is waning, indicating a diminishing relevance of its services among consumers, which could impact future user growth and market share.

See More

GoodRx Launches Oral Ozempic® Treatment for Diabetes

- Transparent Pricing: GoodRx offers Novo Nordisk's Ozempic® oral medication to eligible self-pay patients at a monthly cost starting at $149, significantly reducing financial barriers and enhancing medication accessibility for diabetes patients.

- Market Expansion Strategy: By introducing the oral Ozempic through its nationwide pharmacy network, GoodRx not only diversifies its medication portfolio but also strengthens its partnership with Novo Nordisk, solidifying its position in the diabetes treatment market.

- Increased Patient Convenience: The launch of the oral formulation provides patients with a more convenient alternative to traditional injections, which is expected to attract more users and drive growth in GoodRx's user base and market share.

- Enhanced Industry Influence: This initiative signifies GoodRx's evolution from a pricing solution to a broader consumer access platform, enabling pharmaceutical companies to connect directly with patients and deliver transparent pricing, thereby improving overall healthcare service efficiency.

See More