PNC, Coinbase Partnership Aims To Revolutionize Crypto Banking Infrastructure

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jul 22 2025

0mins

Source: Benzinga

Strategic Alliance: PNC Bank and Coinbase have formed a partnership to enhance secure cryptocurrency offerings and banking services for both retail and institutional clients, integrating Coinbase's Crypto-as-a-Service platform into PNC's operations.

Financial Growth: The collaboration aims to leverage PNC's banking expertise and Coinbase's digital asset capabilities to create a resilient financial ecosystem, with both companies experiencing significant stock gains over the past year.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy COIN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on COIN

Wall Street analysts forecast COIN stock price to rise

25 Analyst Rating

17 Buy

7 Hold

1 Sell

Moderate Buy

Current: 165.480

Low

230.00

Averages

361.63

High

440.00

Current: 165.480

Low

230.00

Averages

361.63

High

440.00

About COIN

Coinbase Global, Inc. is a holding company of Coinbase, Inc. and other subsidiaries. The Company provides a platform that serves as a compliant on-ramp to the onchain economy and enables users to engage in a variety of activities with their crypto assets in both proprietary and third-party product experiences enabled by access to decentralized applications. It offers consumers their primary financial account for the onchain economy; institutions a full-service prime brokerage platform with access to deep pools of liquidity across the crypto marketplace, and developers a suite of products granting access to build onchain. The Company offers products and services to various customer groups: consumers, businesses, institutions, and developers. Its transaction products consist of consumer trading, prime trading, markets, base protocol and Coinbase wallet. The Company also provides market infrastructure in the form of exchanges for customers to trade spots and derivatives.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Coinbase Stock Rises with Optimistic Earnings Outlook

- Stock Performance: Coinbase Global, Inc. (COIN) closed at $168.87, reflecting a 2.05% increase from the previous trading session, outperforming the S&P 500's gain of 0.72%, indicating positive market sentiment towards its stock.

- Earnings Expectations: The company is expected to report an EPS of $0.31, representing a substantial year-over-year increase of 158.33%, although the revenue forecast of $1.36 billion shows a 9.27% decline compared to the prior year, highlighting market concerns about its profitability.

- Annual Outlook: The Zacks Consensus Estimates predict earnings of $1.74 per share and revenue of $5.95 billion for the fiscal year, indicating declines of 56.82% and 17.13% respectively from the previous year, which may affect investor confidence.

- Valuation Metrics: Coinbase's forward P/E ratio stands at 95.18, significantly higher than the industry average of 11.13, suggesting its stock is trading at a premium, while a PEG ratio of 5.84 indicates insufficient expected earnings growth potential, which could impact future investment decisions.

See More

Coinbase Secures UK Investment Services Authorization

- Market Expansion: Coinbase announced it has secured UK investment services authorization, allowing UK users to trade derivatives and equities on a single platform for the first time, enhancing user convenience and the platform's competitive edge.

- Product Diversification: The new authorization will enable institutional and advanced traders to access a variety of derivatives, including crypto, equities, and commodity perpetual futures, further enriching Coinbase's product offerings to meet diverse user needs.

- New Opportunities for Retail Users: Retail users will be able to trade equities on Coinbase for the first time, a move that not only broadens their investment options but also has the potential to attract more users, thereby increasing the platform's market share.

- Enhanced Compliance: This authorization, combined with Coinbase's e-money license and crypto registration in the UK, demonstrates the company's ongoing commitment to compliance, laying a solid foundation for future business expansion.

See More

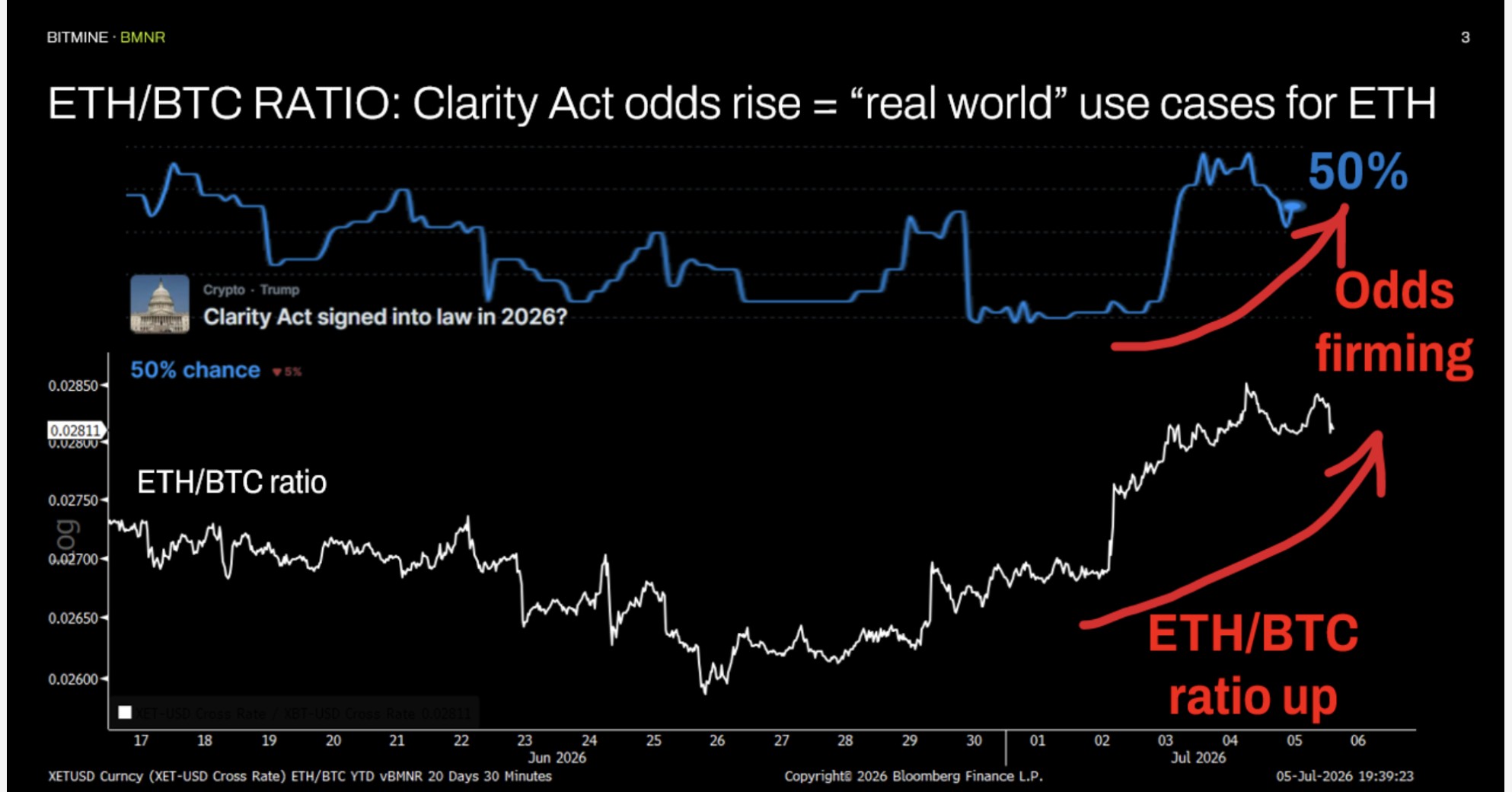

Bitmine Accelerates ETH Holdings to 4.8% of Total Supply

- Significant ETH Holdings: Bitmine currently holds 4.8% of the total ETH supply, approximately 120.7 million ETH, indicating its substantial position in the Ethereum market, which is likely to attract more investor interest.

- Rapid Growth: Over the past 12 months, Bitmine has achieved 95% of its 'Alchemy of 5%' goal, demonstrating its swift expansion in the Ethereum staking sector, which may further enhance its market share and influence.

- Listing Performance: Bitmine was included in the Russell 1000 Large-cap Index on June 26, 2026, increasing its visibility in capital markets and is expected to draw more institutional investor attention.

- Diversified Asset Portfolio: Bitmine's total asset value reaches $11.1 billion, including 5.74 million ETH tokens and $527 million in liquid assets, showcasing its diversified investment strategy across crypto assets and traditional securities.

See More

Bitmine Holds 4.8% of Total ETH Supply

- Significant ETH Holdings: Bitmine currently holds 4,879,157 ETH, valued at approximately $8.8 billion at current prices, highlighting its crucial position in the Ethereum market and laying the groundwork for future investment growth.

- Massive Asset Value: Bitmine's total assets, including cryptocurrencies, liquid funds, and tradable securities, amount to $11.1 billion, comprising 5.74 million ETH and $527 million in liquid assets, reflecting its strong financial strength and market competitiveness.

- Institutional Investor Support: Bitmine has garnered backing from top institutional investors, including Cathie Wood of ARK and Pantera, aiming to achieve its long-term goal of holding 5% of total ETH, which not only enhances its market credibility but may also attract more investor attention.

- Inclusion in Russell 1000 Index: Bitmine was added to the Russell 1000 large-cap index on June 26, 2026, a move that boosts its market visibility and liquidity, potentially driving stock price increases and attracting more institutional investors.

See More

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

See More

Progress on the Digital Asset Market Clarity Act

- Bill Stalled: The House passed the Digital Asset Market Clarity Act, but it remains stalled in the Senate due to stablecoin yield issues, as traditional banks seek to ban stablecoin yields to protect deposits, creating a significant roadblock for the legislation.

- Compromise Reached: Senators Thom Tillis and Angela Alsobrooks brokered a compromise to ban passive stablecoin rewards while allowing activity-based rewards, enabling the Senate to draft a new version of the bill that could potentially clear a final vote.

- Banking Warnings: JPMorgan CEO Jamie Dimon warned that yield-bearing stablecoins could create a

See More

Coinbase Stock Rises with Optimistic Earnings Outlook

- Stock Performance: Coinbase Global, Inc. (COIN) closed at $168.87, reflecting a 2.05% increase from the previous trading session, outperforming the S&P 500's gain of 0.72%, indicating positive market sentiment towards its stock.

- Earnings Expectations: The company is expected to report an EPS of $0.31, representing a substantial year-over-year increase of 158.33%, although the revenue forecast of $1.36 billion shows a 9.27% decline compared to the prior year, highlighting market concerns about its profitability.

- Annual Outlook: The Zacks Consensus Estimates predict earnings of $1.74 per share and revenue of $5.95 billion for the fiscal year, indicating declines of 56.82% and 17.13% respectively from the previous year, which may affect investor confidence.

- Valuation Metrics: Coinbase's forward P/E ratio stands at 95.18, significantly higher than the industry average of 11.13, suggesting its stock is trading at a premium, while a PEG ratio of 5.84 indicates insufficient expected earnings growth potential, which could impact future investment decisions.

See More

Coinbase Secures UK Investment Services Authorization

- Market Expansion: Coinbase announced it has secured UK investment services authorization, allowing UK users to trade derivatives and equities on a single platform for the first time, enhancing user convenience and the platform's competitive edge.

- Product Diversification: The new authorization will enable institutional and advanced traders to access a variety of derivatives, including crypto, equities, and commodity perpetual futures, further enriching Coinbase's product offerings to meet diverse user needs.

- New Opportunities for Retail Users: Retail users will be able to trade equities on Coinbase for the first time, a move that not only broadens their investment options but also has the potential to attract more users, thereby increasing the platform's market share.

- Enhanced Compliance: This authorization, combined with Coinbase's e-money license and crypto registration in the UK, demonstrates the company's ongoing commitment to compliance, laying a solid foundation for future business expansion.

See More

Bitmine Accelerates ETH Holdings to 4.8% of Total Supply

- Significant ETH Holdings: Bitmine currently holds 4.8% of the total ETH supply, approximately 120.7 million ETH, indicating its substantial position in the Ethereum market, which is likely to attract more investor interest.

- Rapid Growth: Over the past 12 months, Bitmine has achieved 95% of its 'Alchemy of 5%' goal, demonstrating its swift expansion in the Ethereum staking sector, which may further enhance its market share and influence.

- Listing Performance: Bitmine was included in the Russell 1000 Large-cap Index on June 26, 2026, increasing its visibility in capital markets and is expected to draw more institutional investor attention.

- Diversified Asset Portfolio: Bitmine's total asset value reaches $11.1 billion, including 5.74 million ETH tokens and $527 million in liquid assets, showcasing its diversified investment strategy across crypto assets and traditional securities.

See More

Bitmine Holds 4.8% of Total ETH Supply

- Significant ETH Holdings: Bitmine currently holds 4,879,157 ETH, valued at approximately $8.8 billion at current prices, highlighting its crucial position in the Ethereum market and laying the groundwork for future investment growth.

- Massive Asset Value: Bitmine's total assets, including cryptocurrencies, liquid funds, and tradable securities, amount to $11.1 billion, comprising 5.74 million ETH and $527 million in liquid assets, reflecting its strong financial strength and market competitiveness.

- Institutional Investor Support: Bitmine has garnered backing from top institutional investors, including Cathie Wood of ARK and Pantera, aiming to achieve its long-term goal of holding 5% of total ETH, which not only enhances its market credibility but may also attract more investor attention.

- Inclusion in Russell 1000 Index: Bitmine was added to the Russell 1000 large-cap index on June 26, 2026, a move that boosts its market visibility and liquidity, potentially driving stock price increases and attracting more institutional investors.

See More

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

See More

Progress on the Digital Asset Market Clarity Act

- Bill Stalled: The House passed the Digital Asset Market Clarity Act, but it remains stalled in the Senate due to stablecoin yield issues, as traditional banks seek to ban stablecoin yields to protect deposits, creating a significant roadblock for the legislation.

- Compromise Reached: Senators Thom Tillis and Angela Alsobrooks brokered a compromise to ban passive stablecoin rewards while allowing activity-based rewards, enabling the Senate to draft a new version of the bill that could potentially clear a final vote.

- Banking Warnings: JPMorgan CEO Jamie Dimon warned that yield-bearing stablecoins could create a

See More