Middle-Income Households Delay Major Purchases Amid Rising Costs

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 09 2026

0mins

Source: Newsfilter

- Widespread Spending Delays: The latest Financial Security Monitor survey reveals that 65% of middle-income households have postponed major purchases in the past year, indicating a shift from short-term budgeting to long-term deferral of critical needs, which could lead to decreased financial stability in the future.

- Cost of Living Pressures: The survey shows that 80% of middle-income Americans expect gas prices to rise in the next six months, with 75% anticipating increases in grocery prices and 78% expecting higher utility costs, suggesting that these widespread cost expectations will further exacerbate financial pressures on households.

- Inadequate Savings Ability: Over 69% of middle-income families rate their ability to save for the future negatively, and 61% do not believe they are saving enough for retirement, indicating that this widespread difficulty in saving could impact long-term financial health and quality of life for families.

- Heavy Debt Burden: More than 56% of middle-income Americans are currently paying down credit card debt, with most typically carrying a balance rather than paying it off in full, which not only affects daily spending but may also limit financial flexibility and future investment opportunities for households.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PRI?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PRI

Wall Street analysts forecast PRI stock price to rise

5 Analyst Rating

1 Buy

4 Hold

0 Sell

Hold

Current: 299.180

Low

267.00

Averages

303.50

High

340.00

Current: 299.180

Low

267.00

Averages

303.50

High

340.00

About PRI

Primerica, Inc. is a provider of financial products and services to middle-income households in North America. The Company's segments include Term Life Insurance, Investment and Savings Products, and Corporate and Other Distributed Products. The Company, through its three life insurance subsidiaries, Primerica Life Insurance Company, National Benefit Life Insurance Company and Primerica Life Insurance Company of Canada (Primerica Life Canada), offers term life insurance to clients in the United States, its territories, and Canada. The Company, through Primerica Financial Services, LLC; PFS Investments Inc.; Primerica Life Canada; PFSL Investments Canada Ltd., and licensed independent sales representatives, distributes and sells to its clients a range of investment products such as mutual funds; managed investments; variable, index-linked, fixed and fixed indexed annuities, and segregated funds. It distributes other products, including prepaid legal services and mortgage loan referrals.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Primerica Household Budget Index Declines to 98.3%

- Index Decline: The Primerica Household Budget Index (HBI™) fell to 98.3% in May, down 1.1% from April and 1.7% year-over-year, indicating ongoing pressure on middle-income families' purchasing power and reflecting the fragility of economic recovery.

- Gas Price Impact: Gas prices rose by 8.6% in May, although the growth rate slowed from 11% in April, remaining the primary driver of financial pressure for middle-income families, highlighting the significant impact of rising living costs on household budgets.

- Slow Income Growth: Earned income for middle-income families increased by 0.2% month-over-month and 2.5% year-over-year in May, but this growth has not effectively offset the rising costs of everyday necessities, revealing a disconnect between income growth and living expenses.

- CPI and HBI Relationship: The Consumer Price Index (CPI) rose by 4.2% year-over-year in May, while the cost of necessities tracked by the HBI increased by 6.2%, indicating greater economic challenges for middle-income families in coping with inflation and underscoring the index's importance in assessing economic trends.

See More

Primerica Household Budget Index Declines to 98.3%

- Household Budget Index Decline: The Primerica Household Budget Index (HBI™) is estimated at 98.3% in May, down 1.1% from April and 1.7% year-over-year, indicating ongoing pressure on the purchasing power of middle-income families.

- Significant Gas Price Impact: Gas prices rose by 8.6% in May, although this growth slowed from 11% in April, remaining the primary driver of financial pressure for middle-income families, reflecting the persistent rise in everyday living costs.

- Slow Income Growth: Earned income for middle-income families increased by 0.2% month-over-month and 2.5% year-over-year in May, but this growth has not effectively offset the rising costs of necessities, highlighting the fragility of household finances.

- CPI and HBI Relationship: The Consumer Price Index (CPI) rose by 4.2% year-over-year in May, while the cost of necessities tracked by the HBI increased by 6.2%, indicating greater economic pressure on middle-income families in coping with inflation.

See More

Canadians Skeptical of Financial Influencers Amid Economic Uncertainty

- Trust in Professional Guidance: According to Primerica Canada's latest Financial Security Monitor survey, 85% of Canadians do not trust financial influencers, and 71% would not consider seeking their advice, indicating a strong preference for professional financial advisors amidst rising economic uncertainty.

- Skepticism Towards AI: The survey reveals that 76% of Canadians are not interested in using AI tools like ChatGPT for budgeting and investing, with 79% preferring human financial advice over AI or influencers, highlighting a continued emphasis on the human aspect of financial guidance.

- Increasing Economic Concerns: Nearly 59% of Canadians cite inflation as a top concern, while 51% worry about health issues and 49% fear another economic recession, collectively intensifying financial stress and driving demand for professional financial advice.

- Pessimistic Outlook on Future: The survey shows that 60% of respondents believe their financial situation has worsened over the past year, with 76% expecting it to remain the same or worsen, reflecting a widespread negative sentiment towards both national and local economies, thereby underscoring the need for trusted financial assistance.

See More

Primerica Household Budget Index Declines

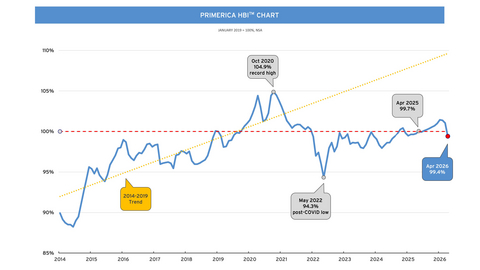

- Index Decline: The Primerica Household Budget Index (HBI™) is estimated at 99.4% in April 2026, down 1.7% from March and 0.3% year-over-year, indicating increased economic pressure on middle-income families.

- Rising Gas Prices: Gas prices surged by 11% in the past month and 28% year-over-year, primarily driving the decline in the HBI™, which exacerbates the cost burden on households.

- Inflation Intensification: The Consumer Price Index (CPI) rose by 3.8% year-over-year in April 2026, while inflation specifically for middle-income families increased to 4.4%, highlighting the ongoing rise in essential living costs.

- Essential Costs Increase: The cost of necessities used in the HBI™ metric, including food, utilities, gas, auto insurance, and healthcare, has risen by 5.5% from a year ago, posing challenges to the purchasing power of middle-income families.

See More

Primerica Household Budget Index Declines

- Index Decline: The Primerica Household Budget Index (HBI™) is estimated at 99.4% for April 2026, down 1.7% from March and 0.3% year-over-year, indicating increased economic pressure on middle-income families.

- Rising Gas Prices: Gas prices surged by 11% in the past month and 28% year-over-year, primarily driving the decline in the HBI™, highlighting the growing burden on households' everyday expenses.

- Inflationary Pressures: The Consumer Price Index (CPI) increased by 3.8% compared to last year, while inflation for middle-income families rose to 4.4%, indicating a persistent rise in the cost of living that affects purchasing power.

- Essential Costs Increase: The cost of necessities included in the HBI™ metric has risen by 5.5% year-over-year, exacerbating economic strain on middle-income families and potentially leading to reduced consumer spending.

See More

PFSL Fund Management Updates Risk Ratings for Concert™ Funds

- Risk Rating Correction: PFSL Fund Management identified inaccuracies in the risk ratings of certain Concert™ Funds during an internal review, with the Primerica Income Fund's rating adjusted from Low to Low to Medium, and the Primerica Canadian Balanced Growth Fund's rating revised from Medium to Low to Medium, ensuring investors receive accurate risk assessments.

- Regulatory Compliance: The updated risk ratings adhere to the standard investment risk classification methodology outlined in National Instrument 81-102, reflecting PFSL's commitment to compliance and aiming to enhance investor trust while maintaining market transparency.

- Trading Restrictions: PFSL confirmed that the Concert™ Funds remain open for limited trading by existing investors, although trading by new investors may be accepted at PFSL's discretion, a strategy that could impact new capital inflows and the funds' liquidity.

- Information Disclosure Channels: Relevant regulatory disclosure documents, including updated prospectuses and fund facts, will be available on www.sedarplus.ca and the designated website of the Concert™ Funds, ensuring investors can access timely information and enhancing transparency.

See More

Primerica Household Budget Index Declines to 98.3%

- Index Decline: The Primerica Household Budget Index (HBI™) fell to 98.3% in May, down 1.1% from April and 1.7% year-over-year, indicating ongoing pressure on middle-income families' purchasing power and reflecting the fragility of economic recovery.

- Gas Price Impact: Gas prices rose by 8.6% in May, although the growth rate slowed from 11% in April, remaining the primary driver of financial pressure for middle-income families, highlighting the significant impact of rising living costs on household budgets.

- Slow Income Growth: Earned income for middle-income families increased by 0.2% month-over-month and 2.5% year-over-year in May, but this growth has not effectively offset the rising costs of everyday necessities, revealing a disconnect between income growth and living expenses.

- CPI and HBI Relationship: The Consumer Price Index (CPI) rose by 4.2% year-over-year in May, while the cost of necessities tracked by the HBI increased by 6.2%, indicating greater economic challenges for middle-income families in coping with inflation and underscoring the index's importance in assessing economic trends.

See More

Primerica Household Budget Index Declines to 98.3%

- Household Budget Index Decline: The Primerica Household Budget Index (HBI™) is estimated at 98.3% in May, down 1.1% from April and 1.7% year-over-year, indicating ongoing pressure on the purchasing power of middle-income families.

- Significant Gas Price Impact: Gas prices rose by 8.6% in May, although this growth slowed from 11% in April, remaining the primary driver of financial pressure for middle-income families, reflecting the persistent rise in everyday living costs.

- Slow Income Growth: Earned income for middle-income families increased by 0.2% month-over-month and 2.5% year-over-year in May, but this growth has not effectively offset the rising costs of necessities, highlighting the fragility of household finances.

- CPI and HBI Relationship: The Consumer Price Index (CPI) rose by 4.2% year-over-year in May, while the cost of necessities tracked by the HBI increased by 6.2%, indicating greater economic pressure on middle-income families in coping with inflation.

See More

Canadians Skeptical of Financial Influencers Amid Economic Uncertainty

- Trust in Professional Guidance: According to Primerica Canada's latest Financial Security Monitor survey, 85% of Canadians do not trust financial influencers, and 71% would not consider seeking their advice, indicating a strong preference for professional financial advisors amidst rising economic uncertainty.

- Skepticism Towards AI: The survey reveals that 76% of Canadians are not interested in using AI tools like ChatGPT for budgeting and investing, with 79% preferring human financial advice over AI or influencers, highlighting a continued emphasis on the human aspect of financial guidance.

- Increasing Economic Concerns: Nearly 59% of Canadians cite inflation as a top concern, while 51% worry about health issues and 49% fear another economic recession, collectively intensifying financial stress and driving demand for professional financial advice.

- Pessimistic Outlook on Future: The survey shows that 60% of respondents believe their financial situation has worsened over the past year, with 76% expecting it to remain the same or worsen, reflecting a widespread negative sentiment towards both national and local economies, thereby underscoring the need for trusted financial assistance.

See More

Primerica Household Budget Index Declines

- Index Decline: The Primerica Household Budget Index (HBI™) is estimated at 99.4% in April 2026, down 1.7% from March and 0.3% year-over-year, indicating increased economic pressure on middle-income families.

- Rising Gas Prices: Gas prices surged by 11% in the past month and 28% year-over-year, primarily driving the decline in the HBI™, which exacerbates the cost burden on households.

- Inflation Intensification: The Consumer Price Index (CPI) rose by 3.8% year-over-year in April 2026, while inflation specifically for middle-income families increased to 4.4%, highlighting the ongoing rise in essential living costs.

- Essential Costs Increase: The cost of necessities used in the HBI™ metric, including food, utilities, gas, auto insurance, and healthcare, has risen by 5.5% from a year ago, posing challenges to the purchasing power of middle-income families.

See More

Primerica Household Budget Index Declines

- Index Decline: The Primerica Household Budget Index (HBI™) is estimated at 99.4% for April 2026, down 1.7% from March and 0.3% year-over-year, indicating increased economic pressure on middle-income families.

- Rising Gas Prices: Gas prices surged by 11% in the past month and 28% year-over-year, primarily driving the decline in the HBI™, highlighting the growing burden on households' everyday expenses.

- Inflationary Pressures: The Consumer Price Index (CPI) increased by 3.8% compared to last year, while inflation for middle-income families rose to 4.4%, indicating a persistent rise in the cost of living that affects purchasing power.

- Essential Costs Increase: The cost of necessities included in the HBI™ metric has risen by 5.5% year-over-year, exacerbating economic strain on middle-income families and potentially leading to reduced consumer spending.

See More

PFSL Fund Management Updates Risk Ratings for Concert™ Funds

- Risk Rating Correction: PFSL Fund Management identified inaccuracies in the risk ratings of certain Concert™ Funds during an internal review, with the Primerica Income Fund's rating adjusted from Low to Low to Medium, and the Primerica Canadian Balanced Growth Fund's rating revised from Medium to Low to Medium, ensuring investors receive accurate risk assessments.

- Regulatory Compliance: The updated risk ratings adhere to the standard investment risk classification methodology outlined in National Instrument 81-102, reflecting PFSL's commitment to compliance and aiming to enhance investor trust while maintaining market transparency.

- Trading Restrictions: PFSL confirmed that the Concert™ Funds remain open for limited trading by existing investors, although trading by new investors may be accepted at PFSL's discretion, a strategy that could impact new capital inflows and the funds' liquidity.

- Information Disclosure Channels: Relevant regulatory disclosure documents, including updated prospectuses and fund facts, will be available on www.sedarplus.ca and the designated website of the Concert™ Funds, ensuring investors can access timely information and enhancing transparency.

See More