Magnolia Oil & Gas Leads $4B Bid for WildFire Energy Acquisition

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Source: seekingalpha

- Acquisition Potential: Magnolia Oil & Gas is poised to acquire WildFire Energy for over $4 billion, marking its largest acquisition to date, which underscores the company's ambition to expand its footprint in the Texas shale sector.

- Operational Scale: WildFire Energy operates more than 2,000 wells with a production exceeding 50,000 barrels of oil equivalent per day, and with its robust production capacity and experienced management team, WildFire presents significant opportunities for Magnolia to enhance output and market share.

- Market Competition: While Magnolia is currently the frontrunner in the bidding process, the report indicates that other bidders could still emerge, introducing uncertainty into the acquisition timeline and final outcome, which could impact Magnolia's strategic plans.

- Historical Context: The management team at WildFire previously sold WildHorse Resource Development Corp. to Chesapeake Energy for $1.9 billion in 2019, providing Magnolia with strategic value and industry expertise that could enhance the success of the acquisition.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MGY?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MGY

Wall Street analysts forecast MGY stock price to fall

11 Analyst Rating

7 Buy

3 Hold

1 Sell

Moderate Buy

Current: 27.200

Low

21.00

Averages

26.44

High

31.00

Current: 27.200

Low

21.00

Averages

26.44

High

31.00

About MGY

Magnolia Oil & Gas Corporation is an oil and gas exploration and production company with operations primarily in South Texas in the core of the Eagle Ford Shale and Austin Chalk formations. The Company's oil and natural gas properties are located primarily in the Karnes and Giddings areas in South Texas. Its assets consist of a total leasehold position of 818,230 gross (613,360 net) acres, including 79,350 gross (55,370 net) acres in the Karnes area and 738,880 gross (557,990 net) acres in the Giddings area. The Giddings area comprises oil and natural gas assets primarily located in Brazos, Burleson, Fayette, Grimes, Lee, Milam, Robertson, and Washington Counties, Texas. The Karnes area comprises oil and natural gas assets primarily located in Karnes, Dimmit, Gonzales, and Zavala Counties, Texas, in the core of the Eagle Ford Shale. The acreage comprising the Karnes area also includes the Austin Chalk formation overlying the Eagle Ford Shale.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Magnolia Oil & Gas Leads $4B Bid for WildFire Energy Acquisition

- Acquisition Potential: Magnolia Oil & Gas is poised to acquire WildFire Energy for over $4 billion, marking its largest acquisition to date, which underscores the company's ambition to expand its footprint in the Texas shale sector.

- Operational Scale: WildFire Energy operates more than 2,000 wells with a production exceeding 50,000 barrels of oil equivalent per day, and with its robust production capacity and experienced management team, WildFire presents significant opportunities for Magnolia to enhance output and market share.

- Market Competition: While Magnolia is currently the frontrunner in the bidding process, the report indicates that other bidders could still emerge, introducing uncertainty into the acquisition timeline and final outcome, which could impact Magnolia's strategic plans.

- Historical Context: The management team at WildFire previously sold WildHorse Resource Development Corp. to Chesapeake Energy for $1.9 billion in 2019, providing Magnolia with strategic value and industry expertise that could enhance the success of the acquisition.

See More

Key Wall Street Rating Updates on Monday

- Tesla Rating Maintained: Jefferies raised Tesla's price target from $350 to $375, indicating that the stock did not sell off ahead of the SPCX IPO, which suggests a consensus on a potential merger that could turn TSLA into a tracker to minimize shareholder dilution risk.

- Kimco Realty Upgrade: Wolfe upgraded Kimco Realty from Peer Perform to Outperform with a price target of $28, anticipating approximately a 16% total return, reflecting strong fundamentals and signaling a recovery potential in the real estate market.

- Cleveland-Cliffs Downgrade: Morgan Stanley downgraded Cleveland-Cliffs from Overweight to Equal Weight with a new price target of $12.5, indicating a more balanced risk-reward profile in line with peers, reflecting a cautious market sentiment towards the stock.

- Micron Technology Reiteration: Bernstein raised Micron's price target from $510 to $1,300 while maintaining an Outperform rating, driven by optimistic forecasts for conventional memory and high bandwidth memory pricing, highlighting a robust recovery in the semiconductor sector.

See More

Magnolia Oil & Gas Q1 2026 Earnings Call Insights

- Production Growth: In Q1 2026, Magnolia Oil & Gas reported a 6% year-over-year increase in total production volumes to 102,600 barrels of oil equivalent per day, with oil production rising by 4% to an average of 40,700 barrels per day, indicating the company's stable growth potential in the oil and gas market.

- Financial Performance: The company achieved a net income of approximately $101 million, translating to $0.54 per diluted share, with adjusted EBITDAX at $253 million, reflecting strong profitability and cash flow that are expected to drive future investments and shareholder returns.

- Acquisition Activity: During the first quarter, Magnolia completed several small bolt-on oil and gas property acquisitions totaling $155 million, adding roughly 6,200 net acres and approximately 500 BOE per day of low-decline production, further solidifying its market position in the Karnes and Giddings areas.

- Future Outlook: Total production for Q2 is estimated to be around 105,000 barrels per day, with the full-year capital expenditure budget reiterated at $440 million to $480 million, demonstrating the company's confidence in sustained growth while maintaining a disciplined approach to capital spending.

See More

Magnolia Oil & Gas Q1 Earnings Miss Expectations

- Earnings Performance: Magnolia Oil & Gas reported a Q1 GAAP EPS of $0.54, missing expectations by $0.23, indicating pressure on profitability that may affect investor confidence.

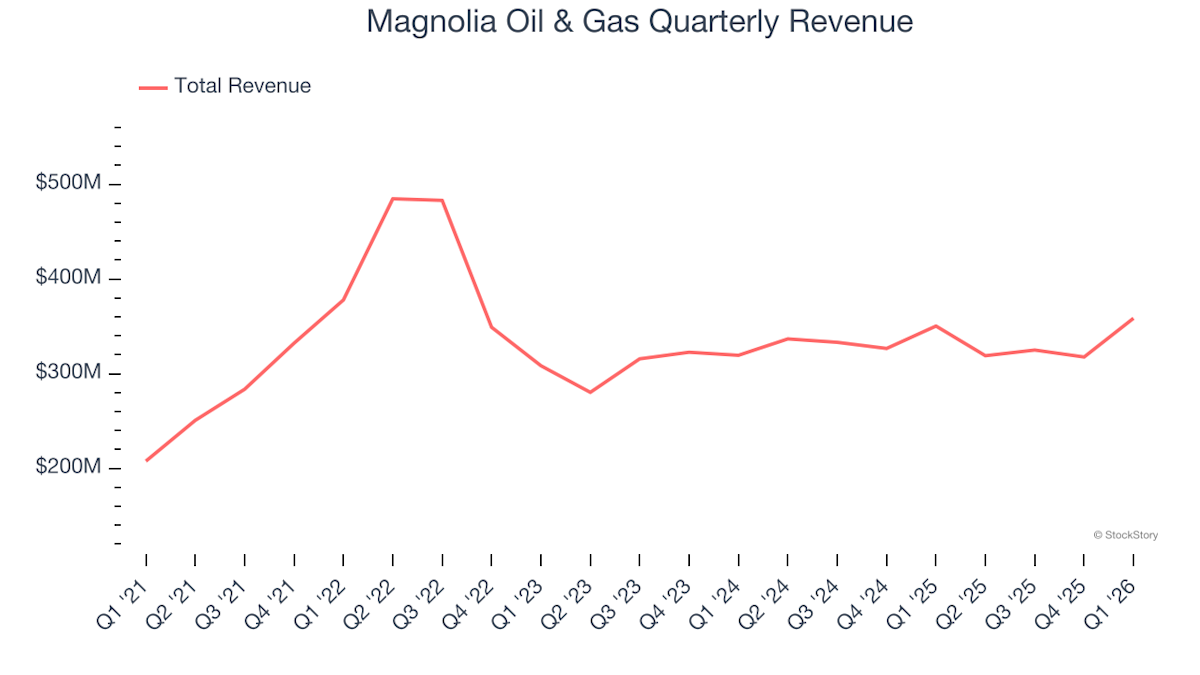

- Revenue Shortfall: The revenue for Q1 was $358.51 million, a 2.3% year-over-year increase, yet it fell short of expectations by $71.97 million, reflecting weak market demand that could lead to future performance declines.

- Capital Expenditure Overview: The D&C capital spending for Q1 was $128.7 million, representing approximately 51% of adjusted EBITDAX, indicating a cautious approach to expansion that may impact long-term growth potential.

- Production Growth Slowdown: Total production volumes grew by 6% year-over-year to 102.6 Mboe/d in Q1, but the growth rate is slowing, with an estimated production of 105 Mboe/d for Q2, suggesting insufficient growth momentum.

See More

Magnolia Oil & Gas Q1 Results Exceed Expectations

- Revenue Growth: Magnolia Oil & Gas reported Q1 revenue of $358.5 million, reflecting a 2.3% year-on-year increase that surpassed analyst expectations of $351.7 million, indicating the company's resilience and appeal in a competitive energy market.

- Earnings Per Share Beat: The GAAP EPS of $0.54 exceeded analysts' expectations of $0.51 by 5.3%, showcasing effective management in cost control and profitability.

- Free Cash Flow Performance: The company generated $197.6 million in free cash flow with a margin of 55.1%, up 28.5 percentage points from the same quarter last year, highlighting its strong capacity for capital return and reinvestment.

- Profitability Stability: Although the EBITDA margin decreased by 7.9 percentage points to 70.7% year-on-year, it remains above industry averages, demonstrating Magnolia's ability to maintain profitability amid market fluctuations.

See More

Magnolia Oil & Gas Set to Announce Q1 Earnings on May 7

- Earnings Announcement: Magnolia Oil & Gas is set to release its Q1 2023 earnings report on May 7 before market open, with consensus estimates predicting an EPS of $0.52 and revenue of $354.39 million, reflecting a 1.3% year-over-year growth, which will provide critical insights into the company's financial health.

- Performance Beat Record: Over the past year, MGY has exceeded EPS estimates 50% of the time and revenue estimates 75% of the time, demonstrating the company's resilience and profitability amid market fluctuations, thereby boosting investor confidence.

- Revision Trends: In the last three months, EPS estimates have seen 13 upward revisions and 1 downward revision, while revenue estimates have experienced 9 upward revisions with no downward adjustments, indicating analysts' optimistic outlook on the company's future performance, which could drive stock price increases.

- Future Growth Targets: Magnolia aims for a 5% production growth in 2026 while maintaining disciplined capital spending, a strategy that will help the company sustain its growth in a competitive market environment.

See More

Magnolia Oil & Gas Leads $4B Bid for WildFire Energy Acquisition

- Acquisition Potential: Magnolia Oil & Gas is poised to acquire WildFire Energy for over $4 billion, marking its largest acquisition to date, which underscores the company's ambition to expand its footprint in the Texas shale sector.

- Operational Scale: WildFire Energy operates more than 2,000 wells with a production exceeding 50,000 barrels of oil equivalent per day, and with its robust production capacity and experienced management team, WildFire presents significant opportunities for Magnolia to enhance output and market share.

- Market Competition: While Magnolia is currently the frontrunner in the bidding process, the report indicates that other bidders could still emerge, introducing uncertainty into the acquisition timeline and final outcome, which could impact Magnolia's strategic plans.

- Historical Context: The management team at WildFire previously sold WildHorse Resource Development Corp. to Chesapeake Energy for $1.9 billion in 2019, providing Magnolia with strategic value and industry expertise that could enhance the success of the acquisition.

See More

Key Wall Street Rating Updates on Monday

- Tesla Rating Maintained: Jefferies raised Tesla's price target from $350 to $375, indicating that the stock did not sell off ahead of the SPCX IPO, which suggests a consensus on a potential merger that could turn TSLA into a tracker to minimize shareholder dilution risk.

- Kimco Realty Upgrade: Wolfe upgraded Kimco Realty from Peer Perform to Outperform with a price target of $28, anticipating approximately a 16% total return, reflecting strong fundamentals and signaling a recovery potential in the real estate market.

- Cleveland-Cliffs Downgrade: Morgan Stanley downgraded Cleveland-Cliffs from Overweight to Equal Weight with a new price target of $12.5, indicating a more balanced risk-reward profile in line with peers, reflecting a cautious market sentiment towards the stock.

- Micron Technology Reiteration: Bernstein raised Micron's price target from $510 to $1,300 while maintaining an Outperform rating, driven by optimistic forecasts for conventional memory and high bandwidth memory pricing, highlighting a robust recovery in the semiconductor sector.

See More

Magnolia Oil & Gas Q1 2026 Earnings Call Insights

- Production Growth: In Q1 2026, Magnolia Oil & Gas reported a 6% year-over-year increase in total production volumes to 102,600 barrels of oil equivalent per day, with oil production rising by 4% to an average of 40,700 barrels per day, indicating the company's stable growth potential in the oil and gas market.

- Financial Performance: The company achieved a net income of approximately $101 million, translating to $0.54 per diluted share, with adjusted EBITDAX at $253 million, reflecting strong profitability and cash flow that are expected to drive future investments and shareholder returns.

- Acquisition Activity: During the first quarter, Magnolia completed several small bolt-on oil and gas property acquisitions totaling $155 million, adding roughly 6,200 net acres and approximately 500 BOE per day of low-decline production, further solidifying its market position in the Karnes and Giddings areas.

- Future Outlook: Total production for Q2 is estimated to be around 105,000 barrels per day, with the full-year capital expenditure budget reiterated at $440 million to $480 million, demonstrating the company's confidence in sustained growth while maintaining a disciplined approach to capital spending.

See More

Magnolia Oil & Gas Q1 Earnings Miss Expectations

- Earnings Performance: Magnolia Oil & Gas reported a Q1 GAAP EPS of $0.54, missing expectations by $0.23, indicating pressure on profitability that may affect investor confidence.

- Revenue Shortfall: The revenue for Q1 was $358.51 million, a 2.3% year-over-year increase, yet it fell short of expectations by $71.97 million, reflecting weak market demand that could lead to future performance declines.

- Capital Expenditure Overview: The D&C capital spending for Q1 was $128.7 million, representing approximately 51% of adjusted EBITDAX, indicating a cautious approach to expansion that may impact long-term growth potential.

- Production Growth Slowdown: Total production volumes grew by 6% year-over-year to 102.6 Mboe/d in Q1, but the growth rate is slowing, with an estimated production of 105 Mboe/d for Q2, suggesting insufficient growth momentum.

See More

Magnolia Oil & Gas Q1 Results Exceed Expectations

- Revenue Growth: Magnolia Oil & Gas reported Q1 revenue of $358.5 million, reflecting a 2.3% year-on-year increase that surpassed analyst expectations of $351.7 million, indicating the company's resilience and appeal in a competitive energy market.

- Earnings Per Share Beat: The GAAP EPS of $0.54 exceeded analysts' expectations of $0.51 by 5.3%, showcasing effective management in cost control and profitability.

- Free Cash Flow Performance: The company generated $197.6 million in free cash flow with a margin of 55.1%, up 28.5 percentage points from the same quarter last year, highlighting its strong capacity for capital return and reinvestment.

- Profitability Stability: Although the EBITDA margin decreased by 7.9 percentage points to 70.7% year-on-year, it remains above industry averages, demonstrating Magnolia's ability to maintain profitability amid market fluctuations.

See More

Magnolia Oil & Gas Set to Announce Q1 Earnings on May 7

- Earnings Announcement: Magnolia Oil & Gas is set to release its Q1 2023 earnings report on May 7 before market open, with consensus estimates predicting an EPS of $0.52 and revenue of $354.39 million, reflecting a 1.3% year-over-year growth, which will provide critical insights into the company's financial health.

- Performance Beat Record: Over the past year, MGY has exceeded EPS estimates 50% of the time and revenue estimates 75% of the time, demonstrating the company's resilience and profitability amid market fluctuations, thereby boosting investor confidence.

- Revision Trends: In the last three months, EPS estimates have seen 13 upward revisions and 1 downward revision, while revenue estimates have experienced 9 upward revisions with no downward adjustments, indicating analysts' optimistic outlook on the company's future performance, which could drive stock price increases.

- Future Growth Targets: Magnolia aims for a 5% production growth in 2026 while maintaining disciplined capital spending, a strategy that will help the company sustain its growth in a competitive market environment.

See More