Lumen Technologies Shifts Focus to AI Infrastructure Amid Financial Challenges

- Strategic Transformation: Lumen Technologies is pivoting from traditional telecom services to become an AI infrastructure provider, planning a multi-billion-dollar network upgrade to meet enterprise AI bandwidth needs, with expectations that cloud spending will double to $1 trillion by 2030, thus seizing market opportunities.

- Financial Challenges: Despite generating $12.4 billion in revenue in 2025, down from $13.1 billion in 2024, Lumen faced a net loss of $1.7 billion due to rising expenses, highlighting the financial pressures during its transition.

- Increased Capital Expenditures: Lumen's capital expenditures reached $4.4 billion in 2025, up from $3.2 billion in 2024, aimed at building a future-proof fiber network, but this has exacerbated its debt burden, with over $17 billion in debt by the end of 2025.

- Future Outlook: Although Lumen forecasts free cash flow of at least $1.2 billion and adjusted EBITDA between $3.1 billion and $3.3 billion for 2026, its high-risk investment profile suggests that only investors with strong risk tolerance should consider this stock.

Trade with 70% Backtested Accuracy

Analyst Views on LUMN

About LUMN

About the author

Lumen Technologies Q1 2026 Earnings Call Insights

- Acquisition Announcement: Lumen plans to acquire software company Alkira for $475 million, with the deal expected to close in Q3, financed through cash on hand, aiming to enhance competitiveness in a rapidly growing market.

- Customer Growth: In Q1, customer adoption grew by 25% quarter-over-quarter, with active ports and services increasing by 35% and 32% respectively, indicating strong demand in the NaaS sector, and over 20% of new customers were first-time users of Lumen.

- Financial Performance: Despite a 3.2% year-over-year decline in total business revenue to $2.44 billion, North American enterprise revenue fell only 0.8%, demonstrating resilience in specific markets, while Q1 free cash flow reached $756 million, indicating a healthy cash flow position.

- Future Outlook: Management raised the 2026 free cash flow guidance to $1.9 billion to $2.1 billion, primarily due to proceeds from the fiber sale to AT&T, with expectations that the acquisition will have a positive long-term impact on financials, though neutral in the short term.

Lumen Technologies Unveils $1 Billion Offering of Senior Notes Maturing in 2037

Company Announcement: Lumen Technologies has announced a $1 billion senior notes offering.

Use of Proceeds: The proceeds from this offering are intended for general corporate purposes.

Maturity Date: The senior notes are due in 2037, indicating a long-term financing strategy.

Market Impact: This move may influence Lumen's financial positioning and investor confidence in the company.

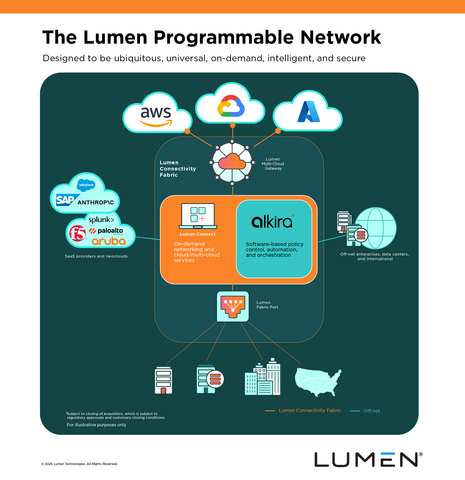

Lumen Acquires Alkira to Enhance Digital Platform Strategy

- Acquisition Overview: Lumen has entered into an agreement to acquire Alkira for $475 million, which will integrate Alkira's cloud-native control plane with Lumen's fiber network, advancing Lumen's digital platform strategy aimed at delivering cloud-like consumption for global enterprise networking.

- Market Expansion Potential: By leveraging Alkira's technology, Lumen estimates its total addressable market will reach approximately $70 billion, particularly in the rapidly growing cloud-to-cloud and data center interconnect segments, significantly enhancing its competitive position.

- Integration Advantages: This acquisition will enable Lumen to unify its network services, allowing customers to design and operate networks through a single control plane, simplifying operations and improving performance to meet the demands of the AI era.

- Financial Impact Analysis: The transaction is expected to be neutral to margins in the near term but will positively impact Lumen's long-term free cash flow as the digital platform scales, reducing platform development execution risk and capital intensity.

Lumen Subsidiary Issues $1 Billion Senior Notes

- Issuance Size: Lumen Technologies' wholly-owned subsidiary Level 3 Financing has agreed to issue $1 billion of 7.500% Senior Notes priced at 100% of their principal amount, maturing in 2037, indicating the company's strong capital market financing capabilities.

- Use of Proceeds: A portion of the net proceeds from this offering will be used to purchase Lumen and its subsidiaries' existing unsecured notes through a cash tender offer, aiming to optimize capital structure and enhance liquidity by reducing financial costs.

- Regulatory Compliance: The Notes will not be registered under U.S. securities laws and are being offered only to qualified institutional buyers, demonstrating the company's commitment to regulatory adherence while actively seeking support from capital markets.

- Market Outlook: Lumen aims to connect people, data, and applications to drive business growth, reflecting its strategic positioning in digital transformation and AI, which is intended to enhance market competitiveness and customer value.

Lumen Technologies Reports Wider-Than-Expected Q1 Loss Amid Acquisition Plans

- Q1 Earnings Miss: Lumen Technologies reported an adjusted loss of $0.47 per share for Q1 2026, significantly worse than the expected $0.12 loss, indicating increased financial pressure on the company.

- Revenue Decline: The company experienced a 9% year-over-year revenue drop to $2.89 billion, although this still exceeded Wall Street estimates by approximately $60 million, reflecting heightened market competition and customer attrition risks.

- Free Cash Flow Improvement: Excluding special items, free cash flow improved to $756 million, up from $354 million a year ago, demonstrating enhanced cash management capabilities within the company.

- Acquisition Announcement: Lumen announced a $475 million acquisition of cloud networking platform Alkira, expected to close in Q3 2026, aimed at bolstering its digital networking platform capabilities, with neutral short-term margin impact but potential long-term free cash flow enhancement.

Lumen Technologies Earnings Snapshot: Growth Under Pressure

- Financial Condition Analysis: Lumen Technologies' balance sheet indicates that despite its partnership with AWS for network connectivity, overall financial performance is under pressure due to revenue growth being constrained by delays in backlog orders.

- Turnaround Story Conclusion: The turnaround narrative for Lumen is nearing its end, with market confidence in future growth waning, leading to a rating downgrade that reflects investor concerns about the company's outlook.

- Revenue Forecast Downgrade: Lumen's revenue forecasts are impacted due to growth being closely tied to delays in backlog orders, which may affect its position in a highly competitive market.

- Long-Term Outlook Adjustment: Analysts have adjusted their long-term outlook for Lumen, suggesting that the company needs to implement more effective strategies to address current market challenges and ensure sustainable growth moving forward.

Lumen Technologies Q1 2026 Earnings Call Insights

- Acquisition Announcement: Lumen plans to acquire software company Alkira for $475 million, with the deal expected to close in Q3, financed through cash on hand, aiming to enhance competitiveness in a rapidly growing market.

- Customer Growth: In Q1, customer adoption grew by 25% quarter-over-quarter, with active ports and services increasing by 35% and 32% respectively, indicating strong demand in the NaaS sector, and over 20% of new customers were first-time users of Lumen.

- Financial Performance: Despite a 3.2% year-over-year decline in total business revenue to $2.44 billion, North American enterprise revenue fell only 0.8%, demonstrating resilience in specific markets, while Q1 free cash flow reached $756 million, indicating a healthy cash flow position.

- Future Outlook: Management raised the 2026 free cash flow guidance to $1.9 billion to $2.1 billion, primarily due to proceeds from the fiber sale to AT&T, with expectations that the acquisition will have a positive long-term impact on financials, though neutral in the short term.

Lumen Technologies Unveils $1 Billion Offering of Senior Notes Maturing in 2037

Company Announcement: Lumen Technologies has announced a $1 billion senior notes offering.

Use of Proceeds: The proceeds from this offering are intended for general corporate purposes.

Maturity Date: The senior notes are due in 2037, indicating a long-term financing strategy.

Market Impact: This move may influence Lumen's financial positioning and investor confidence in the company.

Lumen Acquires Alkira to Enhance Digital Platform Strategy

- Acquisition Overview: Lumen has entered into an agreement to acquire Alkira for $475 million, which will integrate Alkira's cloud-native control plane with Lumen's fiber network, advancing Lumen's digital platform strategy aimed at delivering cloud-like consumption for global enterprise networking.

- Market Expansion Potential: By leveraging Alkira's technology, Lumen estimates its total addressable market will reach approximately $70 billion, particularly in the rapidly growing cloud-to-cloud and data center interconnect segments, significantly enhancing its competitive position.

- Integration Advantages: This acquisition will enable Lumen to unify its network services, allowing customers to design and operate networks through a single control plane, simplifying operations and improving performance to meet the demands of the AI era.

- Financial Impact Analysis: The transaction is expected to be neutral to margins in the near term but will positively impact Lumen's long-term free cash flow as the digital platform scales, reducing platform development execution risk and capital intensity.

Lumen Subsidiary Issues $1 Billion Senior Notes

- Issuance Size: Lumen Technologies' wholly-owned subsidiary Level 3 Financing has agreed to issue $1 billion of 7.500% Senior Notes priced at 100% of their principal amount, maturing in 2037, indicating the company's strong capital market financing capabilities.

- Use of Proceeds: A portion of the net proceeds from this offering will be used to purchase Lumen and its subsidiaries' existing unsecured notes through a cash tender offer, aiming to optimize capital structure and enhance liquidity by reducing financial costs.

- Regulatory Compliance: The Notes will not be registered under U.S. securities laws and are being offered only to qualified institutional buyers, demonstrating the company's commitment to regulatory adherence while actively seeking support from capital markets.

- Market Outlook: Lumen aims to connect people, data, and applications to drive business growth, reflecting its strategic positioning in digital transformation and AI, which is intended to enhance market competitiveness and customer value.

Lumen Technologies Reports Wider-Than-Expected Q1 Loss Amid Acquisition Plans

- Q1 Earnings Miss: Lumen Technologies reported an adjusted loss of $0.47 per share for Q1 2026, significantly worse than the expected $0.12 loss, indicating increased financial pressure on the company.

- Revenue Decline: The company experienced a 9% year-over-year revenue drop to $2.89 billion, although this still exceeded Wall Street estimates by approximately $60 million, reflecting heightened market competition and customer attrition risks.

- Free Cash Flow Improvement: Excluding special items, free cash flow improved to $756 million, up from $354 million a year ago, demonstrating enhanced cash management capabilities within the company.

- Acquisition Announcement: Lumen announced a $475 million acquisition of cloud networking platform Alkira, expected to close in Q3 2026, aimed at bolstering its digital networking platform capabilities, with neutral short-term margin impact but potential long-term free cash flow enhancement.

Lumen Technologies Earnings Snapshot: Growth Under Pressure

- Financial Condition Analysis: Lumen Technologies' balance sheet indicates that despite its partnership with AWS for network connectivity, overall financial performance is under pressure due to revenue growth being constrained by delays in backlog orders.

- Turnaround Story Conclusion: The turnaround narrative for Lumen is nearing its end, with market confidence in future growth waning, leading to a rating downgrade that reflects investor concerns about the company's outlook.

- Revenue Forecast Downgrade: Lumen's revenue forecasts are impacted due to growth being closely tied to delays in backlog orders, which may affect its position in a highly competitive market.

- Long-Term Outlook Adjustment: Analysts have adjusted their long-term outlook for Lumen, suggesting that the company needs to implement more effective strategies to address current market challenges and ensure sustainable growth moving forward.