Lululemon Cuts Earnings Forecast, Joins DocuSign, Samsara And Other Big Stocks Moving Lower In Friday's Pre-Market Session

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jun 06 2025

0mins

Source: Benzinga

Stock Market Overview: U.S. stock futures are up, with Dow futures increasing by about 100 points; however, several companies, including Lululemon and Vera Therapeutics, saw significant declines in pre-market trading due to lowered earnings forecasts or disappointing results.

Company Performance Highlights: Lululemon's shares dropped 20.9% after cutting its FY25 EPS guidance, while DocuSign's shares fell despite better-than-expected results, indicating mixed reactions to earnings reports among various stocks.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DOCU?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DOCU

Wall Street analysts forecast DOCU stock price to rise

16 Analyst Rating

3 Buy

13 Hold

0 Sell

Hold

Current: 42.580

Low

70.00

Averages

80.23

High

105.00

Current: 42.580

Low

70.00

Averages

80.23

High

105.00

About DOCU

DocuSign, Inc. provides intelligent agreement management (IAM) platform an eSignature solution, and contract lifecycle management (CLM) solution - allow organizations to increase productivity, accelerate contract review cycles, and transform agreement data into insights and actions. The Company’s IAM platform automates agreement workflows, uncovers actionable insights, and leverages artificial intelligence (AI) capabilities, enabling organizations to create, commit, and manage agreements virtually. Its products include eSignature, CLM, IAM Apps, and Add-on Products. Its Add-on Products include Payments to collect payments along with signed agreements; Identity and standards-based signature for enhanced signer-identification and signatures with digital certification; Notary for remote online notarization; Monitor for advanced analytics; Gen for Salesforce for automated agreement generation within Salesforce, among others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

DocuSign Launches Slack App for Agreement Management Integration

- App Launch: DocuSign has launched a Slack app that integrates its agreement management tools, allowing users to access contract data and automate workflows directly within workplace messaging, thereby enhancing operational efficiency.

- Intelligent Agreement Management: The app connects DocuSign's Intelligent Agreement Management platform to Slack using Model Context Protocol, enabling users to query contract information through natural language prompts, significantly reducing fragmentation in contract-related work.

- Process Automation: Users can automate processes such as approvals, contract reviews, and signatures directly within Slack conversations, improving team collaboration and minimizing manual tasks.

- Data Synchronization and Alerts: The system can synchronize agreement data with Salesforce and provide alerts on deadlines, renewals, and compliance obligations, further optimizing contract management workflows.

See More

Docusign Launches Slackbot Integration App for Agreement Management

- Intelligent Agreement Management: Docusign's new Slackbot app integrates its Intelligent Agreement Management platform directly into Slack via Model Context Protocol (MCP), enabling teams to quickly access agreement intelligence in their daily workflows, thereby enhancing operational efficiency.

- Workflow Automation: Powered by the Docusign Iris AI engine, the app allows users to ask natural language questions about agreements and receive instant answers based on chat history and CRM data, streamlining workflows for sales, legal, and HR departments.

- Enhanced Collaboration: Docusign CEO Allan Thygesen noted that this integration will enable teams to take action directly within Slack, reducing time spent switching between multiple tools and improving cross-departmental collaboration efficiency.

- Global Availability: The Slackbot app is now available globally in the Slack Marketplace for English users, marking a significant step in Docusign's push for digital transformation in agreement management, expected to attract attention from nearly 1.9 million customers.

See More

Docusign Launches Slackbot Integration App for Agreement Management

- Intelligent Agreement Management: Docusign's newly launched Slackbot app integrates the Intelligent Agreement Management platform directly into Slack via Model Context Protocol (MCP), enabling teams to access agreement intelligence and automate workflows within their work conversations, thereby enhancing operational efficiency.

- Instant Response Capability: The app allows users to ask questions about agreements using natural language and receive quick answers regarding obligations, renewal dates, and key terms, significantly improving the speed and accuracy of teams when handling agreements.

- Accelerated Sales Cycles: By generating agreements from real-time Salesforce CRM data and monitoring renewal opportunities, this integration helps accelerate sales cycles, ensuring teams can seize business expansion opportunities in a timely manner, thus enhancing overall performance.

- System Synchronization and Risk Management: The app automatically writes agreement status and data back to Salesforce, eliminating the need for manual updates, while providing proactive notifications about upcoming deadlines, helping teams better manage compliance requirements and contractual commitments, thereby reducing business risks.

See More

High Options Volume for DocuSign and Reddit

- DocuSign Options Volume: Today, DocuSign's options volume reached 42,841 contracts, representing approximately 4.3 million shares, which is 104.3% of its average daily trading volume over the past month, indicating strong market interest in its future performance.

- High Strike Call Activity: Within DocuSign, the $48.50 strike call option is particularly active, with 31,283 contracts traded today, equating to about 3.1 million shares, suggesting investor expectations for upward movement in the stock.

- Reddit Options Dynamics: Concurrently, Reddit's options volume is also robust at 51,833 contracts, representing approximately 5.2 million shares, which is 97.7% of its average daily trading volume over the past month, reflecting investor recognition of its potential value.

- Active Call Options for Reddit: For Reddit, the $200 strike call option has seen 2,773 contracts traded today, amounting to approximately 277,300 shares, indicating optimistic sentiment regarding its future performance.

See More

Docusign Launches AI Platform to Drive Transformation

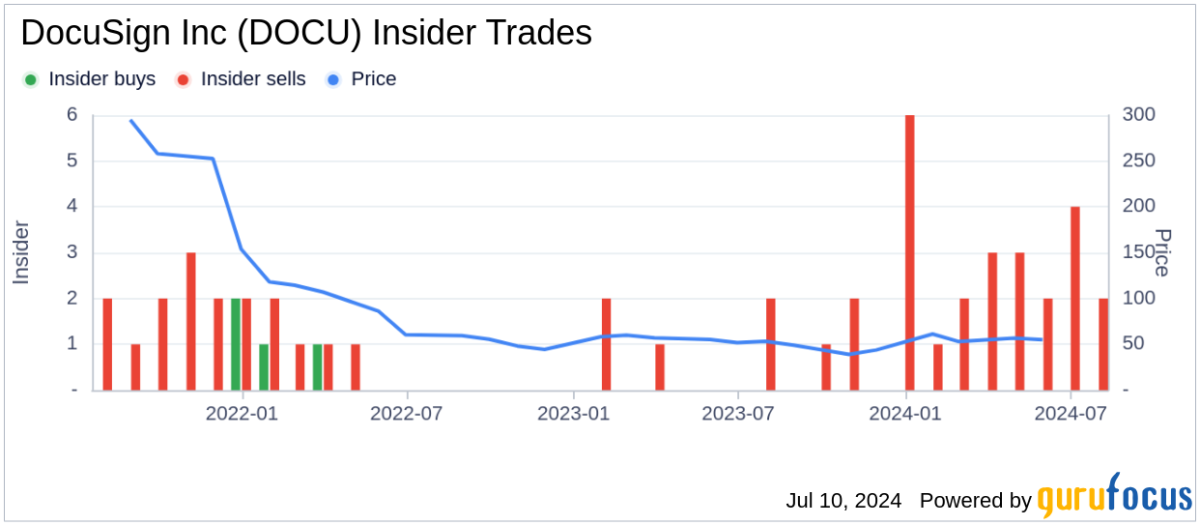

- Pandemic Business Support: Docusign's digital agreement management tools enabled thousands of businesses to operate during the pandemic, driving its stock price to an all-time high of $310 in late 2021, a tenfold increase from its IPO price of $29 in 2018.

- Declining Demand Challenge: As social conditions normalized, demand for Docusign's products significantly declined in 2022, resulting in a slowdown in revenue growth and a current stock price of $48, which is 84% below its 2021 peak.

- Launch of AI Platform: In 2024, Docusign launched a new platform called Intelligent Agreement Management (IAM), designed to transform contract management processes through AI technology, which is already showing strong market demand and could serve as a bullish catalyst for the company's long-term turnaround.

- Financial Performance and Growth Potential: In the first quarter of fiscal 2027, Docusign generated $830.2 million in revenue, exceeding management's forecast, although the growth rate was only 9%; IAM's revenue contribution increased from 10.8% to 12.6%, indicating potential for future growth.

See More

Docusign Launches AI-Driven New Platform

- Market Demand Shift: Docusign's stock peaked at $310 in 2021 but now trades at $48, an 84% decline from its peak, reflecting a sharp decrease in demand post-pandemic, prompting the company to reassess its growth strategy.

- New Platform Launch: In 2024, Docusign launched the Intelligent Agreement Management (IAM) platform aimed at addressing the 55 billion hours wasted annually due to inefficient agreement management, which is expected to serve as a bullish catalyst for the company's long-term turnaround.

- Steady Financial Performance: In Q1 of fiscal 2027, Docusign generated $830.2 million in revenue, exceeding management's forecast of $822 million to $826 million, although the growth rate was only 9%, indicating a shift towards prioritizing profitability over top-line growth.

- Attractive Investment Opportunity: Docusign's current price-to-sales ratio of 3.1 is significantly lower than its long-term average of 12.1 since its IPO, and with the growth potential of IAM, the current stock price presents an attractive entry point for long-term investors.

See More

DocuSign Launches Slack App for Agreement Management Integration

- App Launch: DocuSign has launched a Slack app that integrates its agreement management tools, allowing users to access contract data and automate workflows directly within workplace messaging, thereby enhancing operational efficiency.

- Intelligent Agreement Management: The app connects DocuSign's Intelligent Agreement Management platform to Slack using Model Context Protocol, enabling users to query contract information through natural language prompts, significantly reducing fragmentation in contract-related work.

- Process Automation: Users can automate processes such as approvals, contract reviews, and signatures directly within Slack conversations, improving team collaboration and minimizing manual tasks.

- Data Synchronization and Alerts: The system can synchronize agreement data with Salesforce and provide alerts on deadlines, renewals, and compliance obligations, further optimizing contract management workflows.

See More

Docusign Launches Slackbot Integration App for Agreement Management

- Intelligent Agreement Management: Docusign's new Slackbot app integrates its Intelligent Agreement Management platform directly into Slack via Model Context Protocol (MCP), enabling teams to quickly access agreement intelligence in their daily workflows, thereby enhancing operational efficiency.

- Workflow Automation: Powered by the Docusign Iris AI engine, the app allows users to ask natural language questions about agreements and receive instant answers based on chat history and CRM data, streamlining workflows for sales, legal, and HR departments.

- Enhanced Collaboration: Docusign CEO Allan Thygesen noted that this integration will enable teams to take action directly within Slack, reducing time spent switching between multiple tools and improving cross-departmental collaboration efficiency.

- Global Availability: The Slackbot app is now available globally in the Slack Marketplace for English users, marking a significant step in Docusign's push for digital transformation in agreement management, expected to attract attention from nearly 1.9 million customers.

See More

Docusign Launches Slackbot Integration App for Agreement Management

- Intelligent Agreement Management: Docusign's newly launched Slackbot app integrates the Intelligent Agreement Management platform directly into Slack via Model Context Protocol (MCP), enabling teams to access agreement intelligence and automate workflows within their work conversations, thereby enhancing operational efficiency.

- Instant Response Capability: The app allows users to ask questions about agreements using natural language and receive quick answers regarding obligations, renewal dates, and key terms, significantly improving the speed and accuracy of teams when handling agreements.

- Accelerated Sales Cycles: By generating agreements from real-time Salesforce CRM data and monitoring renewal opportunities, this integration helps accelerate sales cycles, ensuring teams can seize business expansion opportunities in a timely manner, thus enhancing overall performance.

- System Synchronization and Risk Management: The app automatically writes agreement status and data back to Salesforce, eliminating the need for manual updates, while providing proactive notifications about upcoming deadlines, helping teams better manage compliance requirements and contractual commitments, thereby reducing business risks.

See More

High Options Volume for DocuSign and Reddit

- DocuSign Options Volume: Today, DocuSign's options volume reached 42,841 contracts, representing approximately 4.3 million shares, which is 104.3% of its average daily trading volume over the past month, indicating strong market interest in its future performance.

- High Strike Call Activity: Within DocuSign, the $48.50 strike call option is particularly active, with 31,283 contracts traded today, equating to about 3.1 million shares, suggesting investor expectations for upward movement in the stock.

- Reddit Options Dynamics: Concurrently, Reddit's options volume is also robust at 51,833 contracts, representing approximately 5.2 million shares, which is 97.7% of its average daily trading volume over the past month, reflecting investor recognition of its potential value.

- Active Call Options for Reddit: For Reddit, the $200 strike call option has seen 2,773 contracts traded today, amounting to approximately 277,300 shares, indicating optimistic sentiment regarding its future performance.

See More

Docusign Launches AI Platform to Drive Transformation

- Pandemic Business Support: Docusign's digital agreement management tools enabled thousands of businesses to operate during the pandemic, driving its stock price to an all-time high of $310 in late 2021, a tenfold increase from its IPO price of $29 in 2018.

- Declining Demand Challenge: As social conditions normalized, demand for Docusign's products significantly declined in 2022, resulting in a slowdown in revenue growth and a current stock price of $48, which is 84% below its 2021 peak.

- Launch of AI Platform: In 2024, Docusign launched a new platform called Intelligent Agreement Management (IAM), designed to transform contract management processes through AI technology, which is already showing strong market demand and could serve as a bullish catalyst for the company's long-term turnaround.

- Financial Performance and Growth Potential: In the first quarter of fiscal 2027, Docusign generated $830.2 million in revenue, exceeding management's forecast, although the growth rate was only 9%; IAM's revenue contribution increased from 10.8% to 12.6%, indicating potential for future growth.

See More

Docusign Launches AI-Driven New Platform

- Market Demand Shift: Docusign's stock peaked at $310 in 2021 but now trades at $48, an 84% decline from its peak, reflecting a sharp decrease in demand post-pandemic, prompting the company to reassess its growth strategy.

- New Platform Launch: In 2024, Docusign launched the Intelligent Agreement Management (IAM) platform aimed at addressing the 55 billion hours wasted annually due to inefficient agreement management, which is expected to serve as a bullish catalyst for the company's long-term turnaround.

- Steady Financial Performance: In Q1 of fiscal 2027, Docusign generated $830.2 million in revenue, exceeding management's forecast of $822 million to $826 million, although the growth rate was only 9%, indicating a shift towards prioritizing profitability over top-line growth.

- Attractive Investment Opportunity: Docusign's current price-to-sales ratio of 3.1 is significantly lower than its long-term average of 12.1 since its IPO, and with the growth potential of IAM, the current stock price presents an attractive entry point for long-term investors.

See More