General Mills Q3 Earnings Miss Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy GIS?

Source: seekingalpha

- Earnings Performance: General Mills reported a Q3 non-GAAP EPS of $0.64, missing expectations by $0.09, indicating a decline in profitability that may affect investor confidence.

- Revenue Decline: The company posted revenue of $4.4 billion, an 8% year-over-year decrease, falling short of expectations by $30 million, reflecting pressures from weak market demand and increased competition.

- Full-Year Outlook Reaffirmed: Despite challenges, General Mills reaffirmed its fiscal 2026 financial targets, expecting organic net sales to decline by 1.5% to 2%, demonstrating cautious optimism about future performance.

- Stable Cash Flow: Free cash flow conversion is expected to be at least 95% of adjusted after-tax earnings, indicating robust cash management despite overall poor performance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GIS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GIS

Wall Street analysts forecast GIS stock price to rise

15 Analyst Rating

4 Buy

9 Hold

2 Sell

Hold

Current: 38.980

Low

47.00

Averages

52.38

High

63.00

Current: 38.980

Low

47.00

Averages

52.38

High

63.00

About GIS

General Mills, Inc. is a global manufacturer and marketer of branded consumer foods. Its segments include North America Retail; International; North America Pet, and North America Foodservice. The North America Retail segment reflects business with a variety of grocery stores, mass merchandisers, membership stores, natural food chains, drug, dollar and discount chains, convenience stores, and e-commerce grocery providers. The International segment consists of retail and foodservice businesses outside the United States and Canada. Its product categories include super-premium ice cream and frozen desserts, meal kits, salty snacks, snack bars, dessert and baking mixes, and shelf-stable vegetables. The North America Pet segment includes pet food products sold in the United States and Canada in national pet superstore chains, e-commerce retailers, and grocery stores. The North America Foodservice segment product categories include ready-to-eat cereals, snacks, and baking mixes.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

General Mills Set to Announce Q3 Earnings on March 18

- Earnings Announcement Timing: General Mills is set to release its Q3 earnings on March 18 before market open, with consensus EPS estimate at $0.73, reflecting a 27% year-over-year decline, and revenue expected at $4.43 billion, down 8.5% year-over-year, indicating significant profitability challenges ahead.

- Historical Performance Review: Over the past two years, General Mills has beaten EPS estimates 100% of the time, yet only 38% of the time for revenue, suggesting strong earnings capability but potential revenue growth issues that could undermine investor confidence.

- Expectation Revisions: In the last three months, there have been no upward revisions to EPS estimates, with 14 downward adjustments, while revenue estimates also saw no upward revisions and 11 downward changes, reflecting a pessimistic outlook from analysts regarding the company's future performance.

- Strategic Adjustments: General Mills recently sold its Brazil unit to 3corações as part of a strategy to streamline its portfolio and enhance profitability, indicating the company's intent to optimize resource allocation and focus on higher-margin businesses.

See More

General Mills Misses Earnings Estimates, Reaffirms FY26 Outlook

- Earnings Miss: General Mills reported earnings that fell short of market expectations, with both sales and profits below analyst estimates, indicating challenges the company faces in the current economic environment, which may undermine investor confidence.

- Flat Sales Trend: While the company reaffirmed its FY26 outlook, the trend of stagnant sales growth could mask its overvalued stock, intensifying concerns among investors regarding future growth prospects.

- Market Reaction: Following the disappointing earnings report, General Mills' stock may face downward pressure, prompting investors to closely monitor how the company addresses market challenges to restore growth.

- Intensifying Competition: In an increasingly competitive food industry, General Mills must implement effective strategies to maintain market share, particularly as consumer preferences evolve rapidly.

See More

General Mills Misses Earnings Estimates, Reaffirms FY26 Outlook

- Earnings Miss: General Mills (GIS) reported earnings that fell short of market expectations, with both sales and profits below analyst forecasts, highlighting challenges the company faces in the current economic environment.

- Outlook Reaffirmed: Despite the disappointing earnings, General Mills reaffirmed its fiscal year 2026 outlook, indicating confidence in future performance, which may influence investor sentiment positively.

- Negative Market Reaction: The earnings miss could put downward pressure on General Mills' stock price, as investor confidence in the company's future growth may wane, potentially leading to capital outflows.

- Valuation Concerns: Given the current economic climate, General Mills' valuation is seen as overstretched, with historically low valuations no longer serving as a buy signal, prompting investors to reassess the stock's investment value.

See More

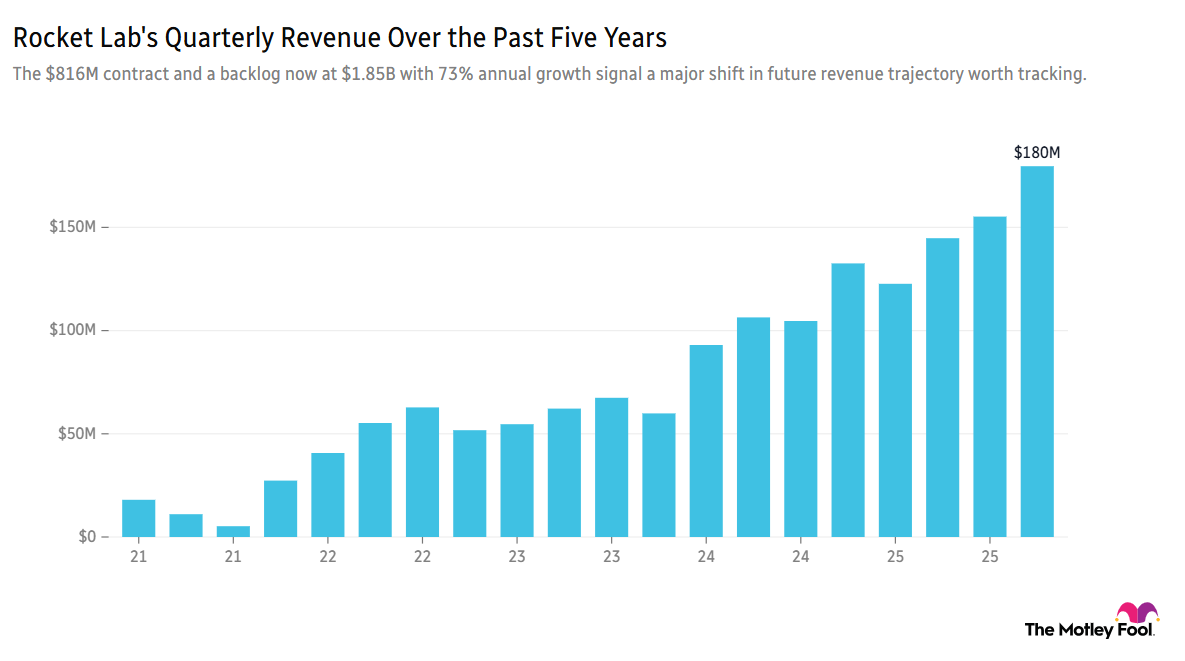

Rocket Lab Shares Surge 10% on New $816M Defense Contract

- Contract Boosts Stock: Rocket Lab (RKLB) shares surged 10.21% after securing an $816 million defense contract with the U.S. Space Development Agency, reflecting investor optimism ahead of upcoming launches dubbed 'Eight Days A Week' and 'Daughter of the Stars'.

- Market Volatility Impact: Despite a 3% pre-market dip due to a newly announced equity offering valued at up to $1 billion, Rocket Lab's stock performance remains 55% ahead of the S&P 500 since August 2025, indicating strong market resilience.

- AI Chip Competition Intensifies: Nvidia has received approval to ship its H200 processors to customers in China, as CEO Jensen Huang announced at the GTC conference, with the export deal cleared by both U.S. and Chinese authorities, further heating up the AI sector competition.

- Lululemon Earnings Impact: Lululemon (LULU) shares fell about 2% following its fourth-quarter earnings report, which showed an 18% year-over-year decline in EPS, although it still surpassed Wall Street expectations, highlighting the brand's strong customer loyalty in a challenging market.

See More

General Mills Q3 Earnings Outlook Highlights Challenges and Strategic Investments

- Earnings Downgrade: General Mills projects a 16% to 20% decline in adjusted earnings per share for fiscal 2026, primarily due to a 1.5% to 2% drop in organic net sales, reflecting challenges in the current consumer environment.

- Sales Growth Strategy: The company plans to restore long-term organic net sales growth by increasing investments in consumer value, product innovation, and brand building, demonstrating its commitment to enhancing market share.

- New Product Launch: General Mills is making a strategic investment to launch the Blue Buffalo brand into the fast-growing U.S. fresh pet food sub-category, aiming to boost its competitiveness and market presence in this segment.

- Quarterly Performance Outlook: Despite challenges, the company expects significant improvements in net sales, operating profit, and earnings per share in the fourth quarter due to benefits from the 53rd week and favorable timing comparisons, showcasing resilience in adversity.

See More

General Mills Reports Decline in Q3 Profit

- Profit Decline: General Mills reported a net profit of $303.1 million for Q3, translating to $0.56 per share, which represents a significant drop from last year's $625.6 million and $1.12 per share, indicating a marked decline in the company's profitability.

- Adjusted Earnings: Excluding items, General Mills reported adjusted earnings of $342.5 million or $0.64 per share, which, while lower than previous periods, still exceeds GAAP figures, suggesting efforts in cost control.

- Revenue Drop: The company's revenue fell to $4.43 billion, an 8.5% decrease from $4.84 billion last year, reflecting weakened market demand and intensified competition.

- Market Outlook Challenges: With both profit and revenue declining, General Mills faces increased market pressure, necessitating a reassessment of its strategies to navigate future economic challenges.

See More

General Mills Set to Announce Q3 Earnings on March 18

- Earnings Announcement Timing: General Mills is set to release its Q3 earnings on March 18 before market open, with consensus EPS estimate at $0.73, reflecting a 27% year-over-year decline, and revenue expected at $4.43 billion, down 8.5% year-over-year, indicating significant profitability challenges ahead.

- Historical Performance Review: Over the past two years, General Mills has beaten EPS estimates 100% of the time, yet only 38% of the time for revenue, suggesting strong earnings capability but potential revenue growth issues that could undermine investor confidence.

- Expectation Revisions: In the last three months, there have been no upward revisions to EPS estimates, with 14 downward adjustments, while revenue estimates also saw no upward revisions and 11 downward changes, reflecting a pessimistic outlook from analysts regarding the company's future performance.

- Strategic Adjustments: General Mills recently sold its Brazil unit to 3corações as part of a strategy to streamline its portfolio and enhance profitability, indicating the company's intent to optimize resource allocation and focus on higher-margin businesses.

See More

General Mills Misses Earnings Estimates, Reaffirms FY26 Outlook

- Earnings Miss: General Mills reported earnings that fell short of market expectations, with both sales and profits below analyst estimates, indicating challenges the company faces in the current economic environment, which may undermine investor confidence.

- Flat Sales Trend: While the company reaffirmed its FY26 outlook, the trend of stagnant sales growth could mask its overvalued stock, intensifying concerns among investors regarding future growth prospects.

- Market Reaction: Following the disappointing earnings report, General Mills' stock may face downward pressure, prompting investors to closely monitor how the company addresses market challenges to restore growth.

- Intensifying Competition: In an increasingly competitive food industry, General Mills must implement effective strategies to maintain market share, particularly as consumer preferences evolve rapidly.

See More

General Mills Misses Earnings Estimates, Reaffirms FY26 Outlook

- Earnings Miss: General Mills (GIS) reported earnings that fell short of market expectations, with both sales and profits below analyst forecasts, highlighting challenges the company faces in the current economic environment.

- Outlook Reaffirmed: Despite the disappointing earnings, General Mills reaffirmed its fiscal year 2026 outlook, indicating confidence in future performance, which may influence investor sentiment positively.

- Negative Market Reaction: The earnings miss could put downward pressure on General Mills' stock price, as investor confidence in the company's future growth may wane, potentially leading to capital outflows.

- Valuation Concerns: Given the current economic climate, General Mills' valuation is seen as overstretched, with historically low valuations no longer serving as a buy signal, prompting investors to reassess the stock's investment value.

See More

Rocket Lab Shares Surge 10% on New $816M Defense Contract

- Contract Boosts Stock: Rocket Lab (RKLB) shares surged 10.21% after securing an $816 million defense contract with the U.S. Space Development Agency, reflecting investor optimism ahead of upcoming launches dubbed 'Eight Days A Week' and 'Daughter of the Stars'.

- Market Volatility Impact: Despite a 3% pre-market dip due to a newly announced equity offering valued at up to $1 billion, Rocket Lab's stock performance remains 55% ahead of the S&P 500 since August 2025, indicating strong market resilience.

- AI Chip Competition Intensifies: Nvidia has received approval to ship its H200 processors to customers in China, as CEO Jensen Huang announced at the GTC conference, with the export deal cleared by both U.S. and Chinese authorities, further heating up the AI sector competition.

- Lululemon Earnings Impact: Lululemon (LULU) shares fell about 2% following its fourth-quarter earnings report, which showed an 18% year-over-year decline in EPS, although it still surpassed Wall Street expectations, highlighting the brand's strong customer loyalty in a challenging market.

See More

General Mills Q3 Earnings Outlook Highlights Challenges and Strategic Investments

- Earnings Downgrade: General Mills projects a 16% to 20% decline in adjusted earnings per share for fiscal 2026, primarily due to a 1.5% to 2% drop in organic net sales, reflecting challenges in the current consumer environment.

- Sales Growth Strategy: The company plans to restore long-term organic net sales growth by increasing investments in consumer value, product innovation, and brand building, demonstrating its commitment to enhancing market share.

- New Product Launch: General Mills is making a strategic investment to launch the Blue Buffalo brand into the fast-growing U.S. fresh pet food sub-category, aiming to boost its competitiveness and market presence in this segment.

- Quarterly Performance Outlook: Despite challenges, the company expects significant improvements in net sales, operating profit, and earnings per share in the fourth quarter due to benefits from the 53rd week and favorable timing comparisons, showcasing resilience in adversity.

See More

General Mills Reports Decline in Q3 Profit

- Profit Decline: General Mills reported a net profit of $303.1 million for Q3, translating to $0.56 per share, which represents a significant drop from last year's $625.6 million and $1.12 per share, indicating a marked decline in the company's profitability.

- Adjusted Earnings: Excluding items, General Mills reported adjusted earnings of $342.5 million or $0.64 per share, which, while lower than previous periods, still exceeds GAAP figures, suggesting efforts in cost control.

- Revenue Drop: The company's revenue fell to $4.43 billion, an 8.5% decrease from $4.84 billion last year, reflecting weakened market demand and intensified competition.

- Market Outlook Challenges: With both profit and revenue declining, General Mills faces increased market pressure, necessitating a reassessment of its strategies to navigate future economic challenges.

See More