First Expert Recommendations for Glucocorticoid Dose Reduction Published

Written by Emily J. Thompson, Senior Investment Analyst

Updated: May 06 2026

0mins

Source: PRnewswire

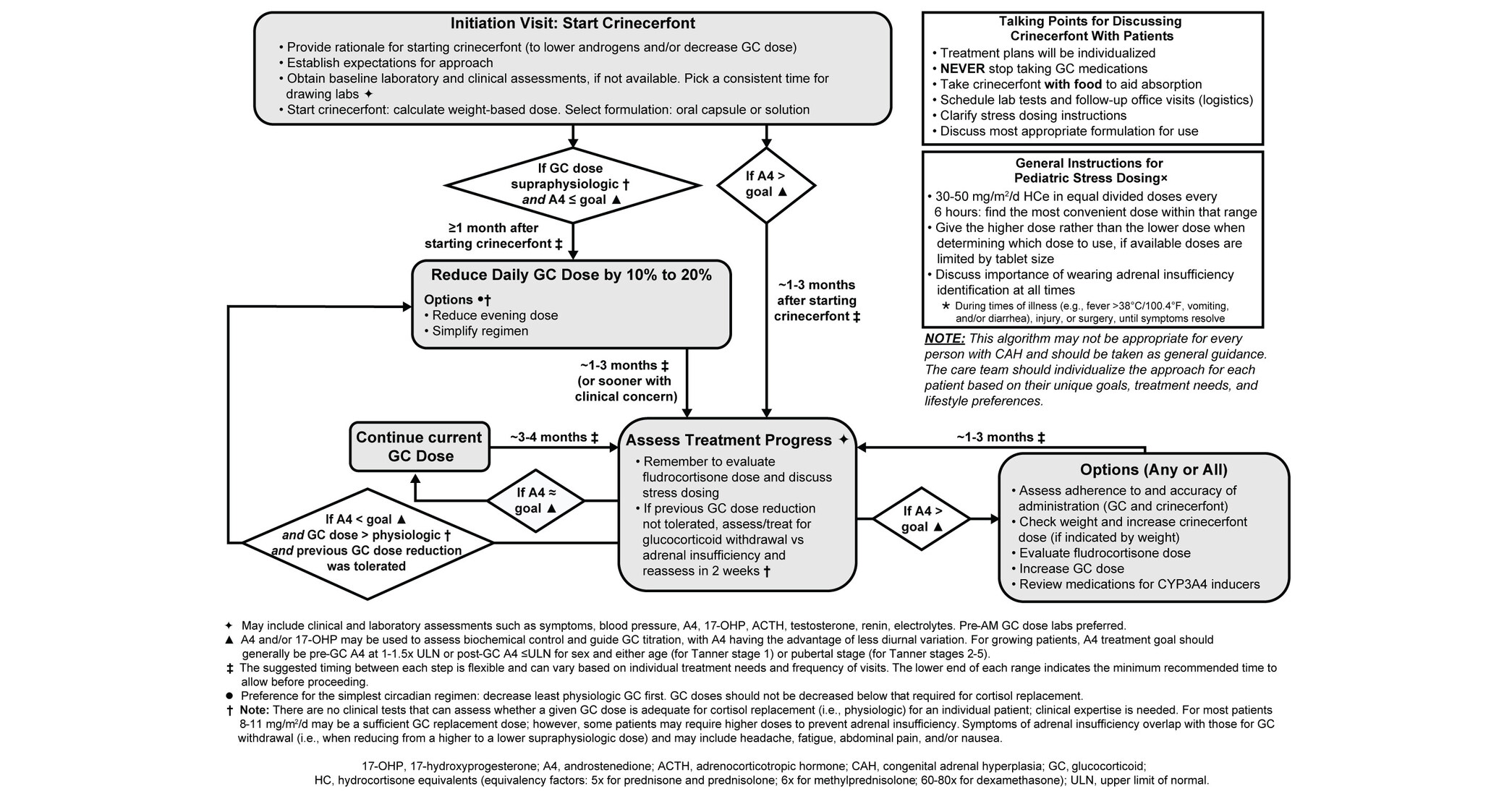

- Expert Recommendations Released: Neurocrine Biosciences has published the first expert recommendations for glucocorticoid dose reduction in patients with classic congenital adrenal hyperplasia, marking a significant advancement in the field.

- Expansion of CRENESSITY® Use: As the real-world application of CRENESSITY® (crinecerfont) expands among pediatric and adult patients, these recommendations address a critical gap in clinical practice, meeting urgent patient needs.

- Peer-Reviewed Recognition: The guidelines have been published in The Journal of Clinical Endocrinology & Metabolism, indicating rigorous peer review and enhancing their authority and credibility within the medical community.

- Far-Reaching Clinical Impact: By providing systematic dose reduction recommendations, the guidelines are expected to improve treatment outcomes, reduce the risk of side effects, and ultimately enhance patient quality of life and treatment satisfaction.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NBIX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NBIX

Wall Street analysts forecast NBIX stock price to rise

20 Analyst Rating

17 Buy

3 Hold

0 Sell

Strong Buy

Current: 156.390

Low

143.00

Averages

179.68

High

203.00

Current: 156.390

Low

143.00

Averages

179.68

High

203.00

About NBIX

Neurocrine Biosciences, Inc. is a neuroscience-focused, biopharmaceutical company. It is engaged in discovering, developing, and commercializing life-changing treatments for patients with under-addressed neurological, psychiatric, endocrine, and immunological disorders. Its diverse portfolio includes the United States Food and Drug Administration-approved treatments for tardive dyskinesia, chorea associated with Huntington’s disease, endometriosis and uterine fibroids, as well as a robust pipeline, including multiple compounds in mid-to late-phase clinical development across its core therapeutic areas. Its first-in-class commercial portfolio includes INGREZZA (valbenazine) and CRENESSITY (crinecerfont). It also offers VYKAT XR (diazoxide choline) extended-release tablets, for the treatment of hyperphagia in adults and pediatric patients four years of age and older with Prader-Willi syndrome (PWS). Its pipeline includes direclidine / (M4 Agonist), osavampator॥ / (AMPA PAM) and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Neurocrine Presents INGREZZA Data and Completes Soleno Acquisition

- Clinical Data Presentation: At the American Psychiatric Association 2026 meeting, Neurocrine presented data showing that 96% of patients with mild tardive dyskinesia experienced improvement in uncontrolled movements after starting INGREZZA, with 86% improving within four weeks, indicating significant efficacy in enhancing patient quality of life.

- Functional Status Improvement: Among 315 patients treated with INGREZZA, 96% of the 81 patients with impacted functional status reported overall improvement, and 83% achieved greater independence, highlighting the drug's critical role in restoring daily living capabilities.

- Acquisition Completion: Neurocrine announced the completion of its $2.9 billion acquisition of Soleno Therapeutics, which will strengthen its position in endocrinology and rare diseases, adding the FDA-approved VYKAT XR to its portfolio and expanding treatment options.

- Market Performance: Neurocrine's stock has traded between $117.59 and $162.39 over the past year, closing at $157.21, down 0.76%, but rising 0.50% in after-hours trading, reflecting positive market sentiment towards its new data and acquisition.

See More

Neurocrine Presents New Data on INGREZZA for Mild Tardive Dyskinesia

- Clinical Data Presentation: At the 2026 American Psychiatric Association Annual Meeting, Neurocrine revealed that 96% of patients with mild tardive dyskinesia treated with INGREZZA reported improvements in movement control, with 86% showing effects within four weeks, demonstrating the drug's efficacy and rapid response in real-world settings.

- Significant Functional Improvements: The survey results indicated that treated patients experienced notable enhancements across various daily life domains, with 90% reporting functional status impairment and 84% independence impairment, underscoring the impact of mild TD on quality of life.

- Support for Clinical Guidelines: This analysis supports the American Psychiatric Association's clinical guidelines recommending the consideration of VMAT2 inhibitors for mild TD patients, further solidifying INGREZZA's potential in improving patient functionality and quality of life.

- Rich Research Background: The analysis was based on clinical data from 315 patients, highlighting the importance of INGREZZA in treating mild TD and showcasing Neurocrine's ongoing commitment to research and innovation in the field of neuropsychiatric disorders.

See More

INGREZZA Shows Significant Efficacy in Mild Tardive Dyskinesia Treatment

- Clinical Improvement: Among patients with mild tardive dyskinesia treated with INGREZZA, 96% reported improvement in movement control, with 86% showing effects within four weeks, highlighting the drug's rapid efficacy and clinical applicability.

- Functional Status Enhancement: Following treatment, 96% of 81 patients with impaired functional status experienced improvements, indicating that INGREZZA not only alleviates movement symptoms but also significantly enhances patients' daily living capabilities.

- Increased Independence: Among treated patients, 83% achieved improved independence, with 70% of those employed or in school reporting enhanced ability to work or attend classes, reflecting the positive impact of treatment on quality of life.

- Guideline Support: These findings support the American Psychiatric Association's clinical guidelines, emphasizing the necessity of using VMAT2 inhibitors for patients with mild tardive dyskinesia, further solidifying INGREZZA's therapeutic position in this area.

See More

Neurocrine Completes Acquisition of Soleno, Strengthening Leadership in Endocrinology

- Acquisition Completed: Neurocrine Biosciences finalized its acquisition of Soleno Therapeutics on May 18, 2026, with a total equity value of $2.9 billion, further solidifying its leadership in endocrinology and rare diseases.

- Portfolio Expansion: The acquisition adds VYKAT™ XR (diazoxide choline) tablets to Neurocrine's portfolio, the first approved treatment for hyperphagia in patients with Prader-Willi syndrome, which is expected to significantly enhance patient quality of life.

- Significant Market Potential: With approximately 10,000 patients affected by Prader-Willi syndrome in the U.S., characterized by chronic hunger and related behavioral issues, the launch of VYKAT XR addresses a substantial unmet medical need, potentially generating considerable market revenue.

- Strategic Integration Plans: Neurocrine aims to leverage collaboration with the Soleno team to promote VYKAT XR's market accessibility and treatment efficacy, thereby enhancing the company's competitive edge in the biopharmaceutical industry.

See More

FDA Grants Orphan Drug Designation to Neurocrine's NBIB-223

- Orphan Drug Status: The FDA has granted orphan drug designation to Neurocrine Biosciences' NBIB-223 (frataxin), which allows for up to seven years of market exclusivity post-approval, significantly enhancing its commercial potential.

- Tax Incentives: With orphan drug status, NBIB-223 will benefit from tax credits for clinical trial expenses, reducing R&D costs and thereby strengthening Neurocrine's competitive position in the Friedreich ataxia treatment landscape.

- Gene Therapy Innovation: NBIB-223 is a gene therapy that employs Voyager Therapeutics' modified AAV capsid to deliver the frataxin gene throughout the body, showcasing Neurocrine's commitment to cutting-edge medical technology and innovation.

- Market Competition: The only approved treatment for Friedreich ataxia is Biogen's Skyclarys (omaveloxolone), and the introduction of NBIB-223 will provide patients with more options while potentially challenging Biogen's market share.

See More

First Expert Recommendations for Glucocorticoid Dose Reduction Published

- Expert Recommendations Released: Neurocrine Biosciences has published the first expert recommendations for glucocorticoid dose reduction in patients with classic congenital adrenal hyperplasia, marking a significant advancement in the field.

- Expansion of CRENESSITY® Use: As the real-world application of CRENESSITY® (crinecerfont) expands among pediatric and adult patients, these recommendations address a critical gap in clinical practice, meeting urgent patient needs.

- Peer-Reviewed Recognition: The guidelines have been published in The Journal of Clinical Endocrinology & Metabolism, indicating rigorous peer review and enhancing their authority and credibility within the medical community.

- Far-Reaching Clinical Impact: By providing systematic dose reduction recommendations, the guidelines are expected to improve treatment outcomes, reduce the risk of side effects, and ultimately enhance patient quality of life and treatment satisfaction.

See More

Neurocrine Presents INGREZZA Data and Completes Soleno Acquisition

- Clinical Data Presentation: At the American Psychiatric Association 2026 meeting, Neurocrine presented data showing that 96% of patients with mild tardive dyskinesia experienced improvement in uncontrolled movements after starting INGREZZA, with 86% improving within four weeks, indicating significant efficacy in enhancing patient quality of life.

- Functional Status Improvement: Among 315 patients treated with INGREZZA, 96% of the 81 patients with impacted functional status reported overall improvement, and 83% achieved greater independence, highlighting the drug's critical role in restoring daily living capabilities.

- Acquisition Completion: Neurocrine announced the completion of its $2.9 billion acquisition of Soleno Therapeutics, which will strengthen its position in endocrinology and rare diseases, adding the FDA-approved VYKAT XR to its portfolio and expanding treatment options.

- Market Performance: Neurocrine's stock has traded between $117.59 and $162.39 over the past year, closing at $157.21, down 0.76%, but rising 0.50% in after-hours trading, reflecting positive market sentiment towards its new data and acquisition.

See More

Neurocrine Presents New Data on INGREZZA for Mild Tardive Dyskinesia

- Clinical Data Presentation: At the 2026 American Psychiatric Association Annual Meeting, Neurocrine revealed that 96% of patients with mild tardive dyskinesia treated with INGREZZA reported improvements in movement control, with 86% showing effects within four weeks, demonstrating the drug's efficacy and rapid response in real-world settings.

- Significant Functional Improvements: The survey results indicated that treated patients experienced notable enhancements across various daily life domains, with 90% reporting functional status impairment and 84% independence impairment, underscoring the impact of mild TD on quality of life.

- Support for Clinical Guidelines: This analysis supports the American Psychiatric Association's clinical guidelines recommending the consideration of VMAT2 inhibitors for mild TD patients, further solidifying INGREZZA's potential in improving patient functionality and quality of life.

- Rich Research Background: The analysis was based on clinical data from 315 patients, highlighting the importance of INGREZZA in treating mild TD and showcasing Neurocrine's ongoing commitment to research and innovation in the field of neuropsychiatric disorders.

See More

INGREZZA Shows Significant Efficacy in Mild Tardive Dyskinesia Treatment

- Clinical Improvement: Among patients with mild tardive dyskinesia treated with INGREZZA, 96% reported improvement in movement control, with 86% showing effects within four weeks, highlighting the drug's rapid efficacy and clinical applicability.

- Functional Status Enhancement: Following treatment, 96% of 81 patients with impaired functional status experienced improvements, indicating that INGREZZA not only alleviates movement symptoms but also significantly enhances patients' daily living capabilities.

- Increased Independence: Among treated patients, 83% achieved improved independence, with 70% of those employed or in school reporting enhanced ability to work or attend classes, reflecting the positive impact of treatment on quality of life.

- Guideline Support: These findings support the American Psychiatric Association's clinical guidelines, emphasizing the necessity of using VMAT2 inhibitors for patients with mild tardive dyskinesia, further solidifying INGREZZA's therapeutic position in this area.

See More

Neurocrine Completes Acquisition of Soleno, Strengthening Leadership in Endocrinology

- Acquisition Completed: Neurocrine Biosciences finalized its acquisition of Soleno Therapeutics on May 18, 2026, with a total equity value of $2.9 billion, further solidifying its leadership in endocrinology and rare diseases.

- Portfolio Expansion: The acquisition adds VYKAT™ XR (diazoxide choline) tablets to Neurocrine's portfolio, the first approved treatment for hyperphagia in patients with Prader-Willi syndrome, which is expected to significantly enhance patient quality of life.

- Significant Market Potential: With approximately 10,000 patients affected by Prader-Willi syndrome in the U.S., characterized by chronic hunger and related behavioral issues, the launch of VYKAT XR addresses a substantial unmet medical need, potentially generating considerable market revenue.

- Strategic Integration Plans: Neurocrine aims to leverage collaboration with the Soleno team to promote VYKAT XR's market accessibility and treatment efficacy, thereby enhancing the company's competitive edge in the biopharmaceutical industry.

See More

FDA Grants Orphan Drug Designation to Neurocrine's NBIB-223

- Orphan Drug Status: The FDA has granted orphan drug designation to Neurocrine Biosciences' NBIB-223 (frataxin), which allows for up to seven years of market exclusivity post-approval, significantly enhancing its commercial potential.

- Tax Incentives: With orphan drug status, NBIB-223 will benefit from tax credits for clinical trial expenses, reducing R&D costs and thereby strengthening Neurocrine's competitive position in the Friedreich ataxia treatment landscape.

- Gene Therapy Innovation: NBIB-223 is a gene therapy that employs Voyager Therapeutics' modified AAV capsid to deliver the frataxin gene throughout the body, showcasing Neurocrine's commitment to cutting-edge medical technology and innovation.

- Market Competition: The only approved treatment for Friedreich ataxia is Biogen's Skyclarys (omaveloxolone), and the introduction of NBIB-223 will provide patients with more options while potentially challenging Biogen's market share.

See More

First Expert Recommendations for Glucocorticoid Dose Reduction Published

- Expert Recommendations Released: Neurocrine Biosciences has published the first expert recommendations for glucocorticoid dose reduction in patients with classic congenital adrenal hyperplasia, marking a significant advancement in the field.

- Expansion of CRENESSITY® Use: As the real-world application of CRENESSITY® (crinecerfont) expands among pediatric and adult patients, these recommendations address a critical gap in clinical practice, meeting urgent patient needs.

- Peer-Reviewed Recognition: The guidelines have been published in The Journal of Clinical Endocrinology & Metabolism, indicating rigorous peer review and enhancing their authority and credibility within the medical community.

- Far-Reaching Clinical Impact: By providing systematic dose reduction recommendations, the guidelines are expected to improve treatment outcomes, reduce the risk of side effects, and ultimately enhance patient quality of life and treatment satisfaction.

See More