DuPont Stock Falls for Six Consecutive Days Amid Strategic Developments

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 05 2026

0mins

Should l Buy DD?

Source: seekingalpha

- Stock Decline: DuPont (DD) shares fell 3.62% to $47.21 in afternoon trading on Thursday, marking a six-day decline that reflects market concerns over future growth, particularly with a 5.24% drop compared to a 1.1% decline in the S&P 500 during the same period.

- Improved Financing Terms: Goldman Sachs has improved financing terms related to the sale of one of DuPont's business units, drawing market attention, although near-term growth prospects remain limited, indicating the company's efforts in optimizing asset allocation.

- New Technology Launch: DuPont unveiled a new membrane technology designed to convert factory wastewater into reusable water, aligning with environmental trends and potentially opening new market opportunities in water treatment and industrial applications.

- Analyst Ratings: According to Seeking Alpha's QuantRating system, DuPont is rated a Buy with a score of 3.09, receiving an A+ for profitability but an F for growth, highlighting the challenges and opportunities the company faces during its transformation process.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DD?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DD

Wall Street analysts forecast DD stock price to rise

10 Analyst Rating

8 Buy

2 Hold

0 Sell

Strong Buy

Current: 46.210

Low

44.00

Averages

49.30

High

59.00

Current: 46.210

Low

44.00

Averages

49.30

High

59.00

About DD

DuPont de Nemours, Inc. is engaged in providing advanced solutions that help transform industries. The Company serves various markets, including healthcare, water, construction, and industrial. It operates through two segments, which include Healthcare & Water Technologies and Diversified Industrials. The Healthcare & Water Technologies segment includes packaging, parts and components for medical device and biopharma markets as well as water filtration and purification technologies primarily for industrial wastewater & energy, municipal drinking water & desalination, and life sciences & specialty markets. The Diversified Industrials segment includes building technologies, with a portfolio serving new-build and repair/remodel applications across non-residential and residential construction markets, and industrial technologies, which includes a portfolio of adhesive, wear and friction, and packaging solutions serving aerospace, automotive and printing and packaging markets.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Eli Lilly Receives FDA Approval for New Drug Foundayo

- New Drug Approval: Eli Lilly announced that its once-daily GLP-1 drug Foundayo has received FDA approval and is set to launch on April 6 via the LillyDirect online platform, addressing strong market demand for weight loss medications and further solidifying its position in the obesity treatment market.

- Positive Market Outlook: Analysts forecast Foundayo to generate approximately $1.55 billion in sales this year, with projections growing to about $14.8 billion by 2030, indicating the drug's significant potential in the future market and its capacity to reshape obesity treatment paradigms.

- Significant Competitive Advantage: Compared to rival Novo Nordisk's Wegovy, Foundayo offers greater flexibility in dosing and dietary restrictions, and has demonstrated superior efficacy in clinical studies for diabetes patients, which may attract a broader patient base to choose this medication.

- Accelerated Strategic Transformation: Eli Lilly built up a substantial stockpile of the drug ahead of FDA approval to ensure a swift market response, showcasing the company's foresight and execution in its new drug launch strategy, thereby enhancing its competitiveness in the biopharmaceutical industry.

See More

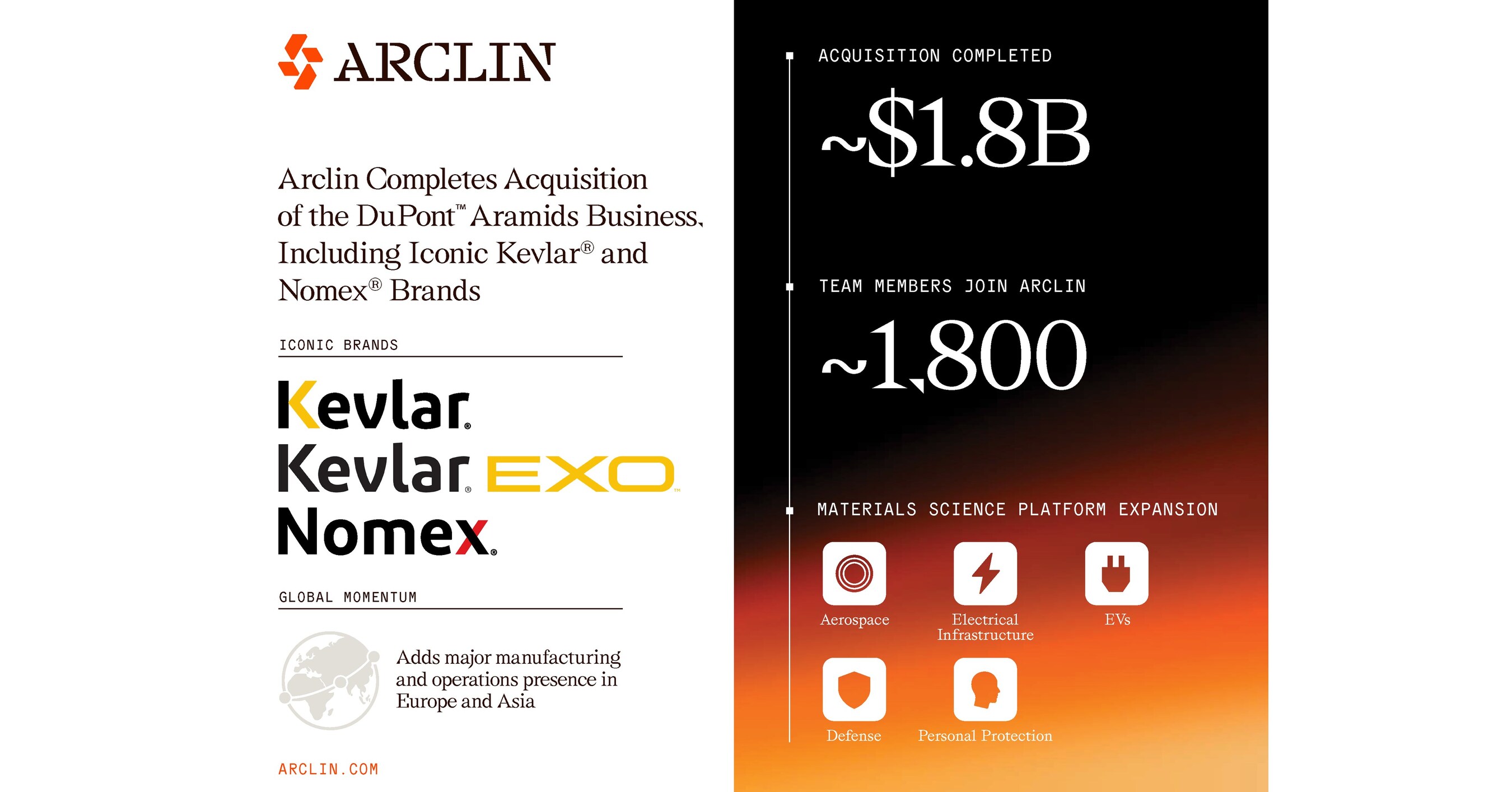

Arclin Completes Acquisition of DuPont's Aramids Business

- Acquisition Scale: Arclin has completed the acquisition of DuPont's Aramids business for approximately $1.8 billion, which includes the renowned Kevlar® and Nomex® brands, marking a significant expansion of Arclin's scale and capabilities in life-critical industries.

- Global Team Expansion: The acquisition adds around 1,800 new team members globally and establishes established manufacturing operations in Europe and Asia, ensuring operational continuity from day one while investing in manufacturing capabilities and innovation to support long-term growth.

- Enhanced Product Portfolio: With the integration of the Aramids brands, Arclin's portfolio now spans aerospace, electrical infrastructure, electric vehicles, and personal protection, further solidifying its leadership position in construction, infrastructure, and protective materials markets.

- Commitment to Innovation: CEO Bradley Bolduc emphasized the company's commitment to investing in technological innovation and strategically deploying Kevlar® and Nomex® across the world's most performance-critical applications to meet the growing demand for advanced protective materials.

See More

DuPont Completes Divestiture of Aramids Business

- Transaction Value: DuPont has completed the divestiture of its Aramids business, including Kevlar® and Nomex®, in a deal valued at approximately $1.8 billion, which is expected to significantly enhance the company's financial position.

- Cash Proceeds: The transaction provides DuPont with pre-tax cash proceeds of about $1.2 billion, further strengthening its liquidity and providing capital for future investments.

- Equity Stake: DuPont also receives a non-controlling common equity interest in Arclin valued at $325 million, representing an approximate 16% stake, which enhances its strategic partnership with Arclin.

- Business Reclassification: Beginning in the third quarter of 2025, the results of the Aramids business were reclassified as discontinued operations, a move that will help DuPont focus on its core operations and optimize resource allocation.

See More

DuPont Completes Divestiture of Aramids Business

- Transaction Value: DuPont has completed the divestiture of its Aramids business (Kevlar® and Nomex®) for approximately $1.8 billion, reflecting the market value and attractiveness of this segment.

- Cash Proceeds: The transaction provides DuPont with about $1.2 billion in pre-tax cash proceeds, enhancing the company's liquidity and financial flexibility, which is crucial for future investments and strategic initiatives.

- Equity Stake: DuPont also secured a non-controlling common equity interest in Arclin valued at $325 million, representing an approximate 16% stake, which offers ongoing revenue potential and market engagement opportunities.

- Business Reclassification: Beginning in Q3 2025, the results of the Aramids business were reclassified as discontinued operations, a move that allows DuPont to focus on its core operations and optimize resource allocation to improve overall operational efficiency.

See More

New Water Plant in Baringo, Kenya Launched

- Water Quality Improvement: DuPont's newly commissioned multi-tech water treatment plant in Baringo, Kenya, provides the Kampi Ya Samaki community with its first reliable drinking water source, utilizing DuPont's ultrafiltration modules and reverse osmosis elements to remove fluoride and other contaminants, significantly enhancing residents' drinking safety.

- Community Benefits: The project is expected to benefit up to 20,000 residents by supplying clean water to 1,500 households, three schools, and a health facility through an expanded distribution network, directly improving public health, particularly for women and children.

- Collaborative Model: The initiative is delivered in partnership with the Baringo County Government and various agencies, ensuring alignment with public health priorities and long-term water planning, showcasing the power of coordinated investment and shared expertise in transforming long-standing public health challenges.

- Sustainable Development: DuPont Water Solutions technologies purify over 50 million gallons of water every minute across 112 countries, demonstrating their global impact and promoting sustainable community-led water treatment solutions that help more communities gain access to clean drinking water.

See More

New Water Plant in Baringo, Kenya Launched

- Water Quality Improvement: DuPont's newly commissioned water treatment plant in Baringo, Kenya, provides the Kampi Ya Samaki community with its first reliable drinking water source, utilizing DuPont's ultrafiltration modules and reverse osmosis elements to effectively remove fluoride and other contaminants, significantly enhancing residents' drinking safety.

- Community Benefits: The project is expected to benefit up to 20,000 people by supplying clean water to 1,500 households, three schools, and a health facility through an expanded distribution network, directly improving the quality of life and health standards for local residents.

- Collaborative Model: Implemented in partnership with ChildFund and other organizations, the project aligns with public health priorities and long-term water resource planning, showcasing the importance of multi-stakeholder collaboration in addressing public health challenges.

- Socioeconomic Impact: Beyond providing safe drinking water, the project is anticipated to yield better health outcomes and reduced medical costs, particularly enhancing school attendance for women and girls, thereby promoting sustainable community development.

See More

Eli Lilly Receives FDA Approval for New Drug Foundayo

- New Drug Approval: Eli Lilly announced that its once-daily GLP-1 drug Foundayo has received FDA approval and is set to launch on April 6 via the LillyDirect online platform, addressing strong market demand for weight loss medications and further solidifying its position in the obesity treatment market.

- Positive Market Outlook: Analysts forecast Foundayo to generate approximately $1.55 billion in sales this year, with projections growing to about $14.8 billion by 2030, indicating the drug's significant potential in the future market and its capacity to reshape obesity treatment paradigms.

- Significant Competitive Advantage: Compared to rival Novo Nordisk's Wegovy, Foundayo offers greater flexibility in dosing and dietary restrictions, and has demonstrated superior efficacy in clinical studies for diabetes patients, which may attract a broader patient base to choose this medication.

- Accelerated Strategic Transformation: Eli Lilly built up a substantial stockpile of the drug ahead of FDA approval to ensure a swift market response, showcasing the company's foresight and execution in its new drug launch strategy, thereby enhancing its competitiveness in the biopharmaceutical industry.

See More

Arclin Completes Acquisition of DuPont's Aramids Business

- Acquisition Scale: Arclin has completed the acquisition of DuPont's Aramids business for approximately $1.8 billion, which includes the renowned Kevlar® and Nomex® brands, marking a significant expansion of Arclin's scale and capabilities in life-critical industries.

- Global Team Expansion: The acquisition adds around 1,800 new team members globally and establishes established manufacturing operations in Europe and Asia, ensuring operational continuity from day one while investing in manufacturing capabilities and innovation to support long-term growth.

- Enhanced Product Portfolio: With the integration of the Aramids brands, Arclin's portfolio now spans aerospace, electrical infrastructure, electric vehicles, and personal protection, further solidifying its leadership position in construction, infrastructure, and protective materials markets.

- Commitment to Innovation: CEO Bradley Bolduc emphasized the company's commitment to investing in technological innovation and strategically deploying Kevlar® and Nomex® across the world's most performance-critical applications to meet the growing demand for advanced protective materials.

See More

DuPont Completes Divestiture of Aramids Business

- Transaction Value: DuPont has completed the divestiture of its Aramids business, including Kevlar® and Nomex®, in a deal valued at approximately $1.8 billion, which is expected to significantly enhance the company's financial position.

- Cash Proceeds: The transaction provides DuPont with pre-tax cash proceeds of about $1.2 billion, further strengthening its liquidity and providing capital for future investments.

- Equity Stake: DuPont also receives a non-controlling common equity interest in Arclin valued at $325 million, representing an approximate 16% stake, which enhances its strategic partnership with Arclin.

- Business Reclassification: Beginning in the third quarter of 2025, the results of the Aramids business were reclassified as discontinued operations, a move that will help DuPont focus on its core operations and optimize resource allocation.

See More

DuPont Completes Divestiture of Aramids Business

- Transaction Value: DuPont has completed the divestiture of its Aramids business (Kevlar® and Nomex®) for approximately $1.8 billion, reflecting the market value and attractiveness of this segment.

- Cash Proceeds: The transaction provides DuPont with about $1.2 billion in pre-tax cash proceeds, enhancing the company's liquidity and financial flexibility, which is crucial for future investments and strategic initiatives.

- Equity Stake: DuPont also secured a non-controlling common equity interest in Arclin valued at $325 million, representing an approximate 16% stake, which offers ongoing revenue potential and market engagement opportunities.

- Business Reclassification: Beginning in Q3 2025, the results of the Aramids business were reclassified as discontinued operations, a move that allows DuPont to focus on its core operations and optimize resource allocation to improve overall operational efficiency.

See More

New Water Plant in Baringo, Kenya Launched

- Water Quality Improvement: DuPont's newly commissioned multi-tech water treatment plant in Baringo, Kenya, provides the Kampi Ya Samaki community with its first reliable drinking water source, utilizing DuPont's ultrafiltration modules and reverse osmosis elements to remove fluoride and other contaminants, significantly enhancing residents' drinking safety.

- Community Benefits: The project is expected to benefit up to 20,000 residents by supplying clean water to 1,500 households, three schools, and a health facility through an expanded distribution network, directly improving public health, particularly for women and children.

- Collaborative Model: The initiative is delivered in partnership with the Baringo County Government and various agencies, ensuring alignment with public health priorities and long-term water planning, showcasing the power of coordinated investment and shared expertise in transforming long-standing public health challenges.

- Sustainable Development: DuPont Water Solutions technologies purify over 50 million gallons of water every minute across 112 countries, demonstrating their global impact and promoting sustainable community-led water treatment solutions that help more communities gain access to clean drinking water.

See More

New Water Plant in Baringo, Kenya Launched

- Water Quality Improvement: DuPont's newly commissioned water treatment plant in Baringo, Kenya, provides the Kampi Ya Samaki community with its first reliable drinking water source, utilizing DuPont's ultrafiltration modules and reverse osmosis elements to effectively remove fluoride and other contaminants, significantly enhancing residents' drinking safety.

- Community Benefits: The project is expected to benefit up to 20,000 people by supplying clean water to 1,500 households, three schools, and a health facility through an expanded distribution network, directly improving the quality of life and health standards for local residents.

- Collaborative Model: Implemented in partnership with ChildFund and other organizations, the project aligns with public health priorities and long-term water resource planning, showcasing the importance of multi-stakeholder collaboration in addressing public health challenges.

- Socioeconomic Impact: Beyond providing safe drinking water, the project is anticipated to yield better health outcomes and reduced medical costs, particularly enhancing school attendance for women and girls, thereby promoting sustainable community development.

See More