Doximity Shares Plunge 20% After Mixed Quarterly Results and Weak Revenue Outlook

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy DOCS?

Source: seekingalpha

- Disappointing Earnings Report: Doximity's quarterly report revealed a full-year revenue outlook of $664M to $676M, falling short of the $687.04M estimate, resulting in a 20% drop in premarket trading.

- AI Cost Pressures: Management highlighted rising costs associated with AI implementation negatively impacting gross margins, with the CEO warning that increased AI investments will weigh on near-term profitability, affecting overall financial health.

- Policy Uncertainty: The company shifted its Q4 outlook to reflect ongoing softness due to elevated policy uncertainty and increased macro risks, moving away from previous optimism regarding budget releases.

- Pharma AI Demand: The CEO noted that the pharmaceutical sector's appetite for AI is stronger than expected, with some top 20 pharma companies planning to allocate 10% to 20% of their budgets to AI, which could drive market changes over the next 2 to 3 years.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DOCS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DOCS

Wall Street analysts forecast DOCS stock price to rise

18 Analyst Rating

14 Buy

4 Hold

0 Sell

Strong Buy

Current: 26.450

Low

25.00

Averages

42.75

High

63.00

Current: 26.450

Low

25.00

Averages

42.75

High

63.00

About DOCS

Doximity, Inc. provides a digital platform for the United States medical professionals. It offers marketing, hiring, and workflow solutions to pharmaceutical manufacturers, health systems, medical recruiting firms, and other healthcare companies. Its marketing solutions enable its pharmaceutical and health system customers to get the right content, services, and peer connections to the right medical professionals through a variety of modules. Its hiring solutions provide digital recruiting capabilities to health systems and medical recruiting firms, enabling them to identify, connect with, and hire from its network of both active and passive medical professional candidates, who might otherwise be missed through traditional recruiting channels. Its workflow solutions include its telehealth, on-call scheduling, and AI-powered workflow tools, are designed to help clinicians streamline their clinical workflow, reduce their administrative burden, and connect with patients and colleagues.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Doximity Reports Record Cash Flow in Q4, Exceeding Guidance

- Strong Financial Performance: Doximity reported $145 million in revenue for Q4 2026, a 5% year-over-year increase, with full-year revenue reaching $645 million, reflecting the company's robust growth potential in the market.

- Record Cash Flow: The company achieved a record $107 million in free cash flow during Q4, marking its first nine-digit free cash flow quarter, indicating significant improvements in operational efficiency and financial health.

- AI Investment Outlook: While minimal AI revenue contribution is expected for fiscal 2027, the company plans to increase spending on AI computing and go-to-market initiatives, demonstrating long-term confidence in AI technology's potential.

- Leadership Changes: The appointment of new CFO Matt Sonefeldt and new President Dr. Steve Zatz signifies a crucial adjustment in the executive team, aimed at driving the commercialization of AI Search and addressing market uncertainties.

See More

Doximity Shares Plunge 20% After Mixed Quarterly Results and Weak Revenue Outlook

- Disappointing Earnings Report: Doximity's quarterly report revealed a full-year revenue outlook of $664M to $676M, falling short of the $687.04M estimate, resulting in a 20% drop in premarket trading.

- AI Cost Pressures: Management highlighted rising costs associated with AI implementation negatively impacting gross margins, with the CEO warning that increased AI investments will weigh on near-term profitability, affecting overall financial health.

- Policy Uncertainty: The company shifted its Q4 outlook to reflect ongoing softness due to elevated policy uncertainty and increased macro risks, moving away from previous optimism regarding budget releases.

- Pharma AI Demand: The CEO noted that the pharmaceutical sector's appetite for AI is stronger than expected, with some top 20 pharma companies planning to allocate 10% to 20% of their budgets to AI, which could drive market changes over the next 2 to 3 years.

See More

Cisco Surges on Earnings Beat and AI Restructuring Plan

- Earnings Beat: Cisco Systems (CSCO) shares surged 20% following a strong FQ3 earnings report, with revenue guidance of $62.8B to $63B exceeding market expectations, indicating robust demand in the AI infrastructure sector.

- Restructuring Plan: The company announced a workforce reduction of approximately 4,000 employees, or 5% of its total staff, with expected restructuring charges of about $1B spread across fiscal years 2026 and 2027, aimed at reallocating resources towards high-speed networking and next-generation data centers.

- Positive Market Reaction: CEO Chuck Robbins emphasized that the restructuring focuses on talent repositioning rather than mere cost-cutting, with investor sentiment bolstered by an increased AI infrastructure order outlook rising from $5B to $9B, enhancing market confidence.

- Increased Competitive Pressure: Despite Cisco's strong performance, Doximity (DOCS) shares fell 21% due to disappointing earnings, highlighting concerns over advertising and pharmaceutical spending pressures on its healthcare platform, which raises worries about overall growth momentum.

See More

Doximity Q4 Earnings Beat Expectations Despite EPS Miss

- Earnings Highlights: Doximity reported a Q4 non-GAAP EPS of $0.26, missing expectations by $0.02, yet its revenue of $145.4 million, reflecting a 5.1% year-over-year increase, surpassed estimates by $1.49 million, indicating stable growth in the healthcare sector.

- Financial Outlook: For the fiscal first quarter ending June 30, 2026, Doximity projects revenue between $151 million and $152 million, with adjusted EBITDA expected to range from $68.5 million to $69.5 million, suggesting a positive outlook for future performance.

- Annual Guidance: The company anticipates revenue for the fiscal year ending March 31, 2027, to be between $664 million and $676 million, with adjusted EBITDA projected between $323 million and $335 million, reflecting confidence in long-term growth.

- Market Reaction: Despite the resignation of the CFO and prevailing market panic, Doximity is viewed as a compelling investment opportunity, highlighting potential value amidst uncertainty.

See More

Doximity to Release Earnings on May 13

- Earnings Release Date: Doximity, Inc is set to release its Q1 2023 earnings on May 13, with significant market attention expected, which may impact the company's stock performance.

- Earnings Per Share Forecast: Analysts predict that Doximity's earnings per share will be 28 cents, a 26.3% decline from 38 cents in the same quarter last year, indicating profitability challenges for the company.

- Stock Price Movement: Ahead of the earnings report, Doximity's shares rose by 0.7% on Tuesday, reflecting a cautiously optimistic market sentiment regarding the upcoming financial results and potential future performance.

- Market Reaction Analysis: Despite the expected decline in earnings per share, the slight increase in stock price may suggest investor confidence in the company's long-term prospects, particularly against the backdrop of ongoing growth in the healthcare technology sector.

See More

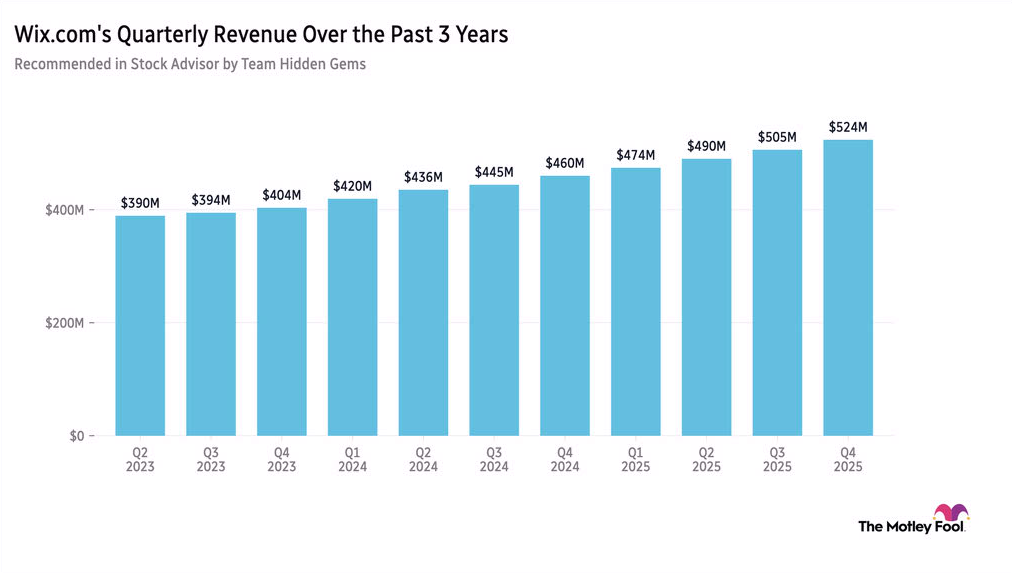

Wix.com Leverages AI Tools to Achieve Revenue Growth

- Significant Revenue Growth: Wix.com reported a 14% year-over-year increase in first-quarter revenue to $541 million, exceeding market expectations and demonstrating resilience amid AI competition, with management forecasting mid-teens growth in revenue and bookings for 2026.

- Share Buyback Strategy: The company repurchased approximately 30% of its outstanding shares in April to counteract a stock price decline of over 10% following the earnings update, indicating management's confidence in the company's long-term value.

- Accelerated AI Innovation: Wix.com recently launched its proprietary LLM, powering its website editor Wix Harmony, showcasing the company's enhanced innovation capabilities in the AI-driven web and app building space.

- Intensifying Market Competition: Despite challenges from AI competitors like Anthropic's Claude Design, Wix.com is striving to maintain market share, with the CEO emphasizing the company's adaptability in a rapidly changing technological landscape.

See More

Doximity Reports Record Cash Flow in Q4, Exceeding Guidance

- Strong Financial Performance: Doximity reported $145 million in revenue for Q4 2026, a 5% year-over-year increase, with full-year revenue reaching $645 million, reflecting the company's robust growth potential in the market.

- Record Cash Flow: The company achieved a record $107 million in free cash flow during Q4, marking its first nine-digit free cash flow quarter, indicating significant improvements in operational efficiency and financial health.

- AI Investment Outlook: While minimal AI revenue contribution is expected for fiscal 2027, the company plans to increase spending on AI computing and go-to-market initiatives, demonstrating long-term confidence in AI technology's potential.

- Leadership Changes: The appointment of new CFO Matt Sonefeldt and new President Dr. Steve Zatz signifies a crucial adjustment in the executive team, aimed at driving the commercialization of AI Search and addressing market uncertainties.

See More

Doximity Shares Plunge 20% After Mixed Quarterly Results and Weak Revenue Outlook

- Disappointing Earnings Report: Doximity's quarterly report revealed a full-year revenue outlook of $664M to $676M, falling short of the $687.04M estimate, resulting in a 20% drop in premarket trading.

- AI Cost Pressures: Management highlighted rising costs associated with AI implementation negatively impacting gross margins, with the CEO warning that increased AI investments will weigh on near-term profitability, affecting overall financial health.

- Policy Uncertainty: The company shifted its Q4 outlook to reflect ongoing softness due to elevated policy uncertainty and increased macro risks, moving away from previous optimism regarding budget releases.

- Pharma AI Demand: The CEO noted that the pharmaceutical sector's appetite for AI is stronger than expected, with some top 20 pharma companies planning to allocate 10% to 20% of their budgets to AI, which could drive market changes over the next 2 to 3 years.

See More

Cisco Surges on Earnings Beat and AI Restructuring Plan

- Earnings Beat: Cisco Systems (CSCO) shares surged 20% following a strong FQ3 earnings report, with revenue guidance of $62.8B to $63B exceeding market expectations, indicating robust demand in the AI infrastructure sector.

- Restructuring Plan: The company announced a workforce reduction of approximately 4,000 employees, or 5% of its total staff, with expected restructuring charges of about $1B spread across fiscal years 2026 and 2027, aimed at reallocating resources towards high-speed networking and next-generation data centers.

- Positive Market Reaction: CEO Chuck Robbins emphasized that the restructuring focuses on talent repositioning rather than mere cost-cutting, with investor sentiment bolstered by an increased AI infrastructure order outlook rising from $5B to $9B, enhancing market confidence.

- Increased Competitive Pressure: Despite Cisco's strong performance, Doximity (DOCS) shares fell 21% due to disappointing earnings, highlighting concerns over advertising and pharmaceutical spending pressures on its healthcare platform, which raises worries about overall growth momentum.

See More

Doximity Q4 Earnings Beat Expectations Despite EPS Miss

- Earnings Highlights: Doximity reported a Q4 non-GAAP EPS of $0.26, missing expectations by $0.02, yet its revenue of $145.4 million, reflecting a 5.1% year-over-year increase, surpassed estimates by $1.49 million, indicating stable growth in the healthcare sector.

- Financial Outlook: For the fiscal first quarter ending June 30, 2026, Doximity projects revenue between $151 million and $152 million, with adjusted EBITDA expected to range from $68.5 million to $69.5 million, suggesting a positive outlook for future performance.

- Annual Guidance: The company anticipates revenue for the fiscal year ending March 31, 2027, to be between $664 million and $676 million, with adjusted EBITDA projected between $323 million and $335 million, reflecting confidence in long-term growth.

- Market Reaction: Despite the resignation of the CFO and prevailing market panic, Doximity is viewed as a compelling investment opportunity, highlighting potential value amidst uncertainty.

See More

Doximity to Release Earnings on May 13

- Earnings Release Date: Doximity, Inc is set to release its Q1 2023 earnings on May 13, with significant market attention expected, which may impact the company's stock performance.

- Earnings Per Share Forecast: Analysts predict that Doximity's earnings per share will be 28 cents, a 26.3% decline from 38 cents in the same quarter last year, indicating profitability challenges for the company.

- Stock Price Movement: Ahead of the earnings report, Doximity's shares rose by 0.7% on Tuesday, reflecting a cautiously optimistic market sentiment regarding the upcoming financial results and potential future performance.

- Market Reaction Analysis: Despite the expected decline in earnings per share, the slight increase in stock price may suggest investor confidence in the company's long-term prospects, particularly against the backdrop of ongoing growth in the healthcare technology sector.

See More

Wix.com Leverages AI Tools to Achieve Revenue Growth

- Significant Revenue Growth: Wix.com reported a 14% year-over-year increase in first-quarter revenue to $541 million, exceeding market expectations and demonstrating resilience amid AI competition, with management forecasting mid-teens growth in revenue and bookings for 2026.

- Share Buyback Strategy: The company repurchased approximately 30% of its outstanding shares in April to counteract a stock price decline of over 10% following the earnings update, indicating management's confidence in the company's long-term value.

- Accelerated AI Innovation: Wix.com recently launched its proprietary LLM, powering its website editor Wix Harmony, showcasing the company's enhanced innovation capabilities in the AI-driven web and app building space.

- Intensifying Market Competition: Despite challenges from AI competitors like Anthropic's Claude Design, Wix.com is striving to maintain market share, with the CEO emphasizing the company's adaptability in a rapidly changing technological landscape.

See More