Cybersecurity Industry Accelerates Transition Amid AI Advances

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 5 days ago

0mins

Source: stocktwits

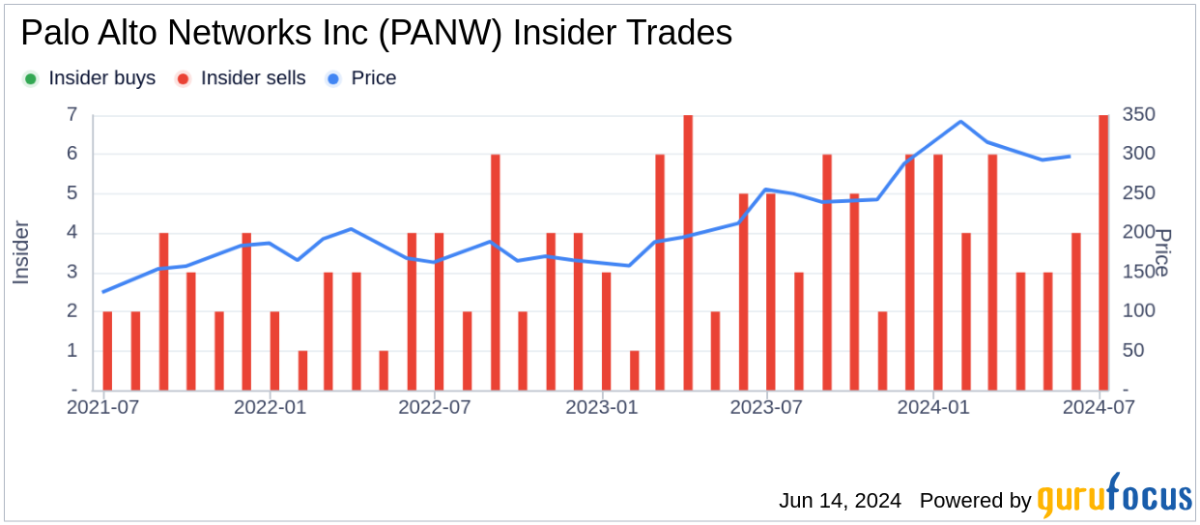

- Strong Earnings Report: Palo Alto Networks reported a 31% revenue increase year-over-year, despite a net loss of $177 million due to acquisitions of CyberArk and Chronosphere, indicating robust growth potential in a rapidly evolving market.

- Price Target Increases: TD Cowen raised its price target for Palo Alto from $225 to $330, reflecting optimistic expectations regarding security demand and AI momentum, suggesting sustained market confidence in the company's future performance.

- Platformization Strategy: CEO Nikesh Arora emphasized the company's implementation of a 'platformization' strategy to tackle increasingly sophisticated AI-driven threats, underscoring Palo Alto's leadership and adaptability in the industry.

- Retail Sentiment Surge: On Stocktwits, retail sentiment around Palo Alto remains 'extremely bullish', with message volume surging 696% in the past 24 hours, indicating strong investor confidence in the company's future prospects.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PANW?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PANW

Wall Street analysts forecast PANW stock price to fall

34 Analyst Rating

28 Buy

5 Hold

1 Sell

Strong Buy

Current: 272.050

Low

157.00

Averages

232.49

High

265.00

Current: 272.050

Low

157.00

Averages

232.49

High

265.00

About PANW

Palo Alto Networks, Inc. is a global artificial intelligence (AI) cybersecurity company, with a comprehensive portfolio of cybersecurity solutions and platforms across network, cloud, security operations, AI and Identity. Its network security platform includes Secure Access Service Edge (SASE), Next-Generation Firewalls, Cloud Delivered Security Services (CDSS), Prisma AIRS, and Strata Cloud Manager (SCM). It delivers security operations capabilities that unifies standalone Security Information and Event Management (SIEM) tools, endpoint security, security automation, cloud detection and response (CDR), as well as attack surface management (ASM) capabilities on its Cortex platform. It delivers comprehensive security across the cloud application development lifecycle through Cortex Cloud. Its Unit 42 brings together expertise across threat research, incident response, and security consulting to deliver intelligence-driven, response-ready outcomes that help customers reduce cyber risk.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Palo Alto Networks Stock Soars 57.1% in May Amid AI Growth

- Stock Performance: Palo Alto Networks saw its stock price soar by 57.1% in May, significantly outperforming the S&P 500's 5.2% and the Nasdaq Composite's 8.4%, reflecting strong investor confidence in the cybersecurity sector amid rapid advancements in artificial intelligence technologies.

- Product Launch: On May 12, Palo Alto unveiled its Idira identity security platform, which offers a substantial upgrade for CyberArk customers, aimed at addressing security threats posed by AI, thereby enhancing the company's competitive edge in the cybersecurity landscape.

- Acquisition Strengthens Position: The company completed its acquisition of Portkey on May 29, which specializes in AI gateway technologies that effectively regulate AI interactions, thereby bolstering Palo Alto's technological capabilities and solidifying its position in the cybersecurity market.

- Earnings Beat Expectations: Despite a pullback in June, Palo Alto reported adjusted earnings of $0.85 per share and revenue of $3 billion for Q3 of fiscal 2026, both exceeding Wall Street estimates; however, the high market expectations led to a decline in stock price following the earnings report.

See More

Redwood AI Corp. Expands Strategic Positioning in AI and Cybersecurity

- Growing Market Demand: As investments in AI-powered operational intelligence systems accelerate across government, healthcare, and enterprise sectors, global defense spending is projected to rise from $2.7 trillion to $6.38 trillion by 2035, with an annual growth rate of approximately 8.13%, driving demand for advanced analytics and chemical intelligence systems.

- Acquisition Potential: Redwood AI has signed a non-binding letter of intent to explore the acquisition of Quantum.IQ, a quantum cybersecurity company, which, if successful, would transform Redwood from a specialized AI and chemical intelligence platform into a vertically integrated intelligence and cybersecurity company, significantly enhancing its market opportunities.

- Government Collaboration Projects: As a core technology contributor to the Track and Trace initiative, Redwood AI is receiving $300,000 annually from the British Columbia government to leverage AI technology in combating illicit drug supply, showcasing its influence and government validation in the public safety sector.

- Support for Technological Innovation: Redwood AI's Q-SAFE initiative has received support from the National Research Council of Canada, securing up to C$240,000 in funding aimed at improving hazardous chemical risk classification by combining chemical AI capabilities with optimization methods, further solidifying its competitive position in defense and public safety markets.

See More

Palo Alto Networks Sees Strong Growth Amid AI Cybersecurity Surge

- Stock Surge: Palo Alto Networks' stock soared by 57.1% in May, significantly outperforming the S&P 500's 5.2% and Nasdaq's 8.4%, indicating strong investor confidence in the cybersecurity sector.

- Product Launch: On May 12, the company unveiled its Idira identity security platform, designed to provide significant upgrades for CyberArk customers, thereby enhancing its capability to address AI-driven threats and improving competitive positioning.

- Acquisition Completion: Palo Alto completed its acquisition of Portkey on May 29, a company specializing in AI gateway technologies, which will further strengthen its security product offerings to meet the growing demand for AI security solutions.

- Earnings Beat Expectations: In its Q3 fiscal 2026 report, Palo Alto posted adjusted earnings of $0.85 per share and revenue of $3 billion, both exceeding Wall Street estimates, although the stock experienced a pullback post-earnings, reflecting market concerns about future growth prospects.

See More

Investment Outlook for Netskope Stock

- Market Growth Potential: Netskope, Inc. is positioned in a rapidly expanding SASE market, expected to grow at an annual rate of 23% through 2030, providing a long-term investment opportunity as enterprises replace legacy VPNs and firewalls.

- Improved Financial Performance: The company has reached free cash flow breakeven with approximately 40% incremental EBITDA margins, targeting a 23% revenue growth rate for FY26, indicating ongoing improvements in operating leverage and execution strength that bolster investor confidence.

- Competitive Advantage: Netskope differentiates itself from competitors like Zscaler and Palo Alto Networks through its leadership in CASB and DLP for data-sensitive enterprises, enabling it to deliver effective security solutions at scale for large regulated customers globally, further solidifying its market position.

- Valuation Attractiveness: The stock currently trades at about 3x revenue, reflecting market pessimism, but if the company sustains its growth trajectory, it could rerate to 5-8x forward revenue, especially if AI security demand accelerates over time.

See More

Stock Market Plummets as Tech Stocks Take a Hit

- Market Turmoil: The stock market faced a massive sell-off on Friday, with the S&P 500 and Nasdaq dropping 2.6% and 4.2%, respectively, breaking a nine-week winning streak and indicating investor anxiety over the Federal Reserve's interest rate policies.

- Tech Stock Struggles: Broadcom's stock plummeted 12.6% post-earnings, failing to meet high market expectations, which undermined investor confidence and exacerbated the overall decline in tech stocks.

- IPO Surge: SpaceX plans to issue 555.6 million shares at $135 each, raising approximately $75 billion and achieving a market value of $1.8 trillion, highlighting strong demand for high-tech companies but raising concerns about market oversupply.

- Investor Sentiment Dips: Following Alphabet's announcement of an $85 billion stock sale to fund AI investments, the market reacted negatively, with Meta Platforms also dropping over 6% due to potential dilution fears, reflecting investor apprehension about equity dilution.

See More

Hewlett Packard Enterprise Surges 14% Following Record Earnings Report

- Earnings Beat: Hewlett Packard Enterprise reported an adjusted earnings per share of 79 cents and revenue of $10.68 billion for Q2, surpassing analyst expectations of 53 cents and $9.79 billion, marking the largest earnings beat since 2018 and highlighting robust growth in cloud and AI sectors.

- Stock Surge: Following the strong earnings report, HPE's stock surged 14% this week, with a relative strength index (RSI) of 73 indicating it is in overbought territory, suggesting a potential pullback could be imminent, yet reflecting investor confidence in its future growth.

- Analyst Upgrade: Loop Capital upgraded HPE from hold to buy, raising its price target from $23 to $75, implying a 52% upside from Friday's close, indicating strong market optimism regarding the company's future performance.

- Industry Trends: HPE's success is closely tied to its accelerated investment in commercial inference, with analyst Ananda Baruah noting that the adoption of Agentic and Inferencing could trigger significant growth expansion over the next 3-5 years, further solidifying its market position.

See More

Palo Alto Networks Stock Soars 57.1% in May Amid AI Growth

- Stock Performance: Palo Alto Networks saw its stock price soar by 57.1% in May, significantly outperforming the S&P 500's 5.2% and the Nasdaq Composite's 8.4%, reflecting strong investor confidence in the cybersecurity sector amid rapid advancements in artificial intelligence technologies.

- Product Launch: On May 12, Palo Alto unveiled its Idira identity security platform, which offers a substantial upgrade for CyberArk customers, aimed at addressing security threats posed by AI, thereby enhancing the company's competitive edge in the cybersecurity landscape.

- Acquisition Strengthens Position: The company completed its acquisition of Portkey on May 29, which specializes in AI gateway technologies that effectively regulate AI interactions, thereby bolstering Palo Alto's technological capabilities and solidifying its position in the cybersecurity market.

- Earnings Beat Expectations: Despite a pullback in June, Palo Alto reported adjusted earnings of $0.85 per share and revenue of $3 billion for Q3 of fiscal 2026, both exceeding Wall Street estimates; however, the high market expectations led to a decline in stock price following the earnings report.

See More

Redwood AI Corp. Expands Strategic Positioning in AI and Cybersecurity

- Growing Market Demand: As investments in AI-powered operational intelligence systems accelerate across government, healthcare, and enterprise sectors, global defense spending is projected to rise from $2.7 trillion to $6.38 trillion by 2035, with an annual growth rate of approximately 8.13%, driving demand for advanced analytics and chemical intelligence systems.

- Acquisition Potential: Redwood AI has signed a non-binding letter of intent to explore the acquisition of Quantum.IQ, a quantum cybersecurity company, which, if successful, would transform Redwood from a specialized AI and chemical intelligence platform into a vertically integrated intelligence and cybersecurity company, significantly enhancing its market opportunities.

- Government Collaboration Projects: As a core technology contributor to the Track and Trace initiative, Redwood AI is receiving $300,000 annually from the British Columbia government to leverage AI technology in combating illicit drug supply, showcasing its influence and government validation in the public safety sector.

- Support for Technological Innovation: Redwood AI's Q-SAFE initiative has received support from the National Research Council of Canada, securing up to C$240,000 in funding aimed at improving hazardous chemical risk classification by combining chemical AI capabilities with optimization methods, further solidifying its competitive position in defense and public safety markets.

See More

Palo Alto Networks Sees Strong Growth Amid AI Cybersecurity Surge

- Stock Surge: Palo Alto Networks' stock soared by 57.1% in May, significantly outperforming the S&P 500's 5.2% and Nasdaq's 8.4%, indicating strong investor confidence in the cybersecurity sector.

- Product Launch: On May 12, the company unveiled its Idira identity security platform, designed to provide significant upgrades for CyberArk customers, thereby enhancing its capability to address AI-driven threats and improving competitive positioning.

- Acquisition Completion: Palo Alto completed its acquisition of Portkey on May 29, a company specializing in AI gateway technologies, which will further strengthen its security product offerings to meet the growing demand for AI security solutions.

- Earnings Beat Expectations: In its Q3 fiscal 2026 report, Palo Alto posted adjusted earnings of $0.85 per share and revenue of $3 billion, both exceeding Wall Street estimates, although the stock experienced a pullback post-earnings, reflecting market concerns about future growth prospects.

See More

Investment Outlook for Netskope Stock

- Market Growth Potential: Netskope, Inc. is positioned in a rapidly expanding SASE market, expected to grow at an annual rate of 23% through 2030, providing a long-term investment opportunity as enterprises replace legacy VPNs and firewalls.

- Improved Financial Performance: The company has reached free cash flow breakeven with approximately 40% incremental EBITDA margins, targeting a 23% revenue growth rate for FY26, indicating ongoing improvements in operating leverage and execution strength that bolster investor confidence.

- Competitive Advantage: Netskope differentiates itself from competitors like Zscaler and Palo Alto Networks through its leadership in CASB and DLP for data-sensitive enterprises, enabling it to deliver effective security solutions at scale for large regulated customers globally, further solidifying its market position.

- Valuation Attractiveness: The stock currently trades at about 3x revenue, reflecting market pessimism, but if the company sustains its growth trajectory, it could rerate to 5-8x forward revenue, especially if AI security demand accelerates over time.

See More

Stock Market Plummets as Tech Stocks Take a Hit

- Market Turmoil: The stock market faced a massive sell-off on Friday, with the S&P 500 and Nasdaq dropping 2.6% and 4.2%, respectively, breaking a nine-week winning streak and indicating investor anxiety over the Federal Reserve's interest rate policies.

- Tech Stock Struggles: Broadcom's stock plummeted 12.6% post-earnings, failing to meet high market expectations, which undermined investor confidence and exacerbated the overall decline in tech stocks.

- IPO Surge: SpaceX plans to issue 555.6 million shares at $135 each, raising approximately $75 billion and achieving a market value of $1.8 trillion, highlighting strong demand for high-tech companies but raising concerns about market oversupply.

- Investor Sentiment Dips: Following Alphabet's announcement of an $85 billion stock sale to fund AI investments, the market reacted negatively, with Meta Platforms also dropping over 6% due to potential dilution fears, reflecting investor apprehension about equity dilution.

See More

Hewlett Packard Enterprise Surges 14% Following Record Earnings Report

- Earnings Beat: Hewlett Packard Enterprise reported an adjusted earnings per share of 79 cents and revenue of $10.68 billion for Q2, surpassing analyst expectations of 53 cents and $9.79 billion, marking the largest earnings beat since 2018 and highlighting robust growth in cloud and AI sectors.

- Stock Surge: Following the strong earnings report, HPE's stock surged 14% this week, with a relative strength index (RSI) of 73 indicating it is in overbought territory, suggesting a potential pullback could be imminent, yet reflecting investor confidence in its future growth.

- Analyst Upgrade: Loop Capital upgraded HPE from hold to buy, raising its price target from $23 to $75, implying a 52% upside from Friday's close, indicating strong market optimism regarding the company's future performance.

- Industry Trends: HPE's success is closely tied to its accelerated investment in commercial inference, with analyst Ananda Baruah noting that the adoption of Agentic and Inferencing could trigger significant growth expansion over the next 3-5 years, further solidifying its market position.

See More