CrowdStrike: AI Revolution Creates Growth Opportunities

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 2 days ago

0mins

Source: Fool

- Opportunity from AI Revolution: CrowdStrike CEO George Kurtz highlighted that the AI revolution presents a massive growth opportunity for the company, particularly as enterprise AI security needs increase, reinforcing CrowdStrike's position as an industry leader.

- Layered Security Assurance: Kurtz emphasized that CrowdStrike secures every layer from GPU to agent to prompt, and as AI data centers and related technologies proliferate, the demand for cybersecurity services from enterprises is expected to rise significantly.

- Slowing Revenue Growth: Despite CrowdStrike's 5-year compound annual growth rate of 40.6%, its year-over-year growth rate for Q4 of fiscal 2026 was only 23%, indicating a deceleration in revenue growth, leading to cautious market expectations for its future performance.

- Future Outlook: CrowdStrike anticipates reaching $6.49 billion in annual recurring revenue by fiscal 2027; although current figures do not show a significant impact from AI on its performance, the cybersecurity industry is expected to benefit from sustained market demand in the long term.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CRWD?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CRWD

Wall Street analysts forecast CRWD stock price to fall

34 Analyst Rating

23 Buy

11 Hold

0 Sell

Moderate Buy

Current: 768.950

Low

353.00

Averages

559.71

High

640.00

Current: 768.950

Low

353.00

Averages

559.71

High

640.00

About CRWD

CrowdStrike Holdings, Inc. is a global cybersecurity company that provides cloud-delivered protection of endpoints, cloud workloads, identity and data. Its Falcon platform is designed for cybersecurity consolidation, purpose-built to stop breaches. The platforms collect and integrate data from across the enterprise, including endpoints, cloud workloads, identities, and third-party sources. It offers 29 cloud modules on its Falcon platform via a software as a service (SaaS) subscription-based model that spans multiple large markets, including corporate endpoint and cloud workload security, managed security services, security and vulnerability management, information technology (IT) operations management, identity protection, next-generation security information and event management (SIEM) and log management, threat intelligence services, data protection, SaaS security posture management, automation and response (SOAR) and artificial intelligence powered workflow automation, and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

CrowdStrike Set to Report Strong Q1 Earnings Amid AI Demand

- Optimistic Earnings Outlook: CrowdStrike is expected to report Q1 EPS of $1.07, reflecting a 46.6% increase, with revenue projected to grow 23.6% to $1.36 billion, indicating strong performance and rising market demand in the cybersecurity sector.

- Analysts Bullish on Future: Stifel and Cantor Fitzgerald have raised their price targets for CrowdStrike, with Cantor Fitzgerald's analyst noting positive feedback from partners regarding ongoing growth in endpoint markets and solid performance in emerging products, suggesting the company may exceed market expectations.

- AI Integration Advantage: The integration of AI into CrowdStrike's platform enhances its threat detection capabilities, providing a competitive edge in addressing advanced cyberattacks, particularly amid rising enterprise cloud adoption.

- Strong Stock Performance: CrowdStrike's stock has surged over 60% this year, significantly outperforming the S&P 500's 11% increase, reflecting market confidence in its growth potential.

See More

Market Volatility and Tech Stock Performance

- Oil Price Impact: Stocks fell as crude oil prices climbed back above $95 per barrel due to renewed airstrikes between the U.S. and Iran, with financials being the worst-performing sector, indicating pressure on rate-sensitive stocks and a negative market sentiment.

- Cybersecurity Stock Pullback: Despite Palo Alto Networks delivering a strong earnings report, its stock declined over 2%, with Jim Cramer urging investors to hold, while anticipating a potential short-term drop of 7% to 8%, reflecting cautious market sentiment regarding future performance.

- New Semiconductor Position: Jim initiated a new position in Intel on Wednesday, believing that demand for CPUs will continue to grow as AI workloads shift from training to inference, stressing that investors should start small rather than chase the stock higher to mitigate risk.

- Rapid Stock Review: In a quick recap, Jim highlighted stocks such as Honeywell, Macy's, Ulta, AT&T, and Kraft Heinz, indicating a focus on diversified investments while reflecting varying perspectives on individual stock performances.

See More

Palo Alto Networks Shares Drop 4% Despite Strong Earnings

- Earnings Beat: Palo Alto Networks shares fell over 4% despite exceeding quarterly expectations, indicating market concerns about the company's long-term outlook despite strong financial results.

- Hardware Growth Outlook: The company raised its hardware growth forecast for the coming quarters, particularly for firewall installations in data centers and enterprise campuses, but management's guidance for fiscal 2030 subscription revenue did not see a significant increase, potentially disappointing investors.

- Market Reaction Analysis: The stock surged approximately 86% over the past two months, yet CEO Nikesh Arora cautioned during the earnings call against expecting substantial earnings growth in the short term, which may have triggered sell-offs from short-term traders.

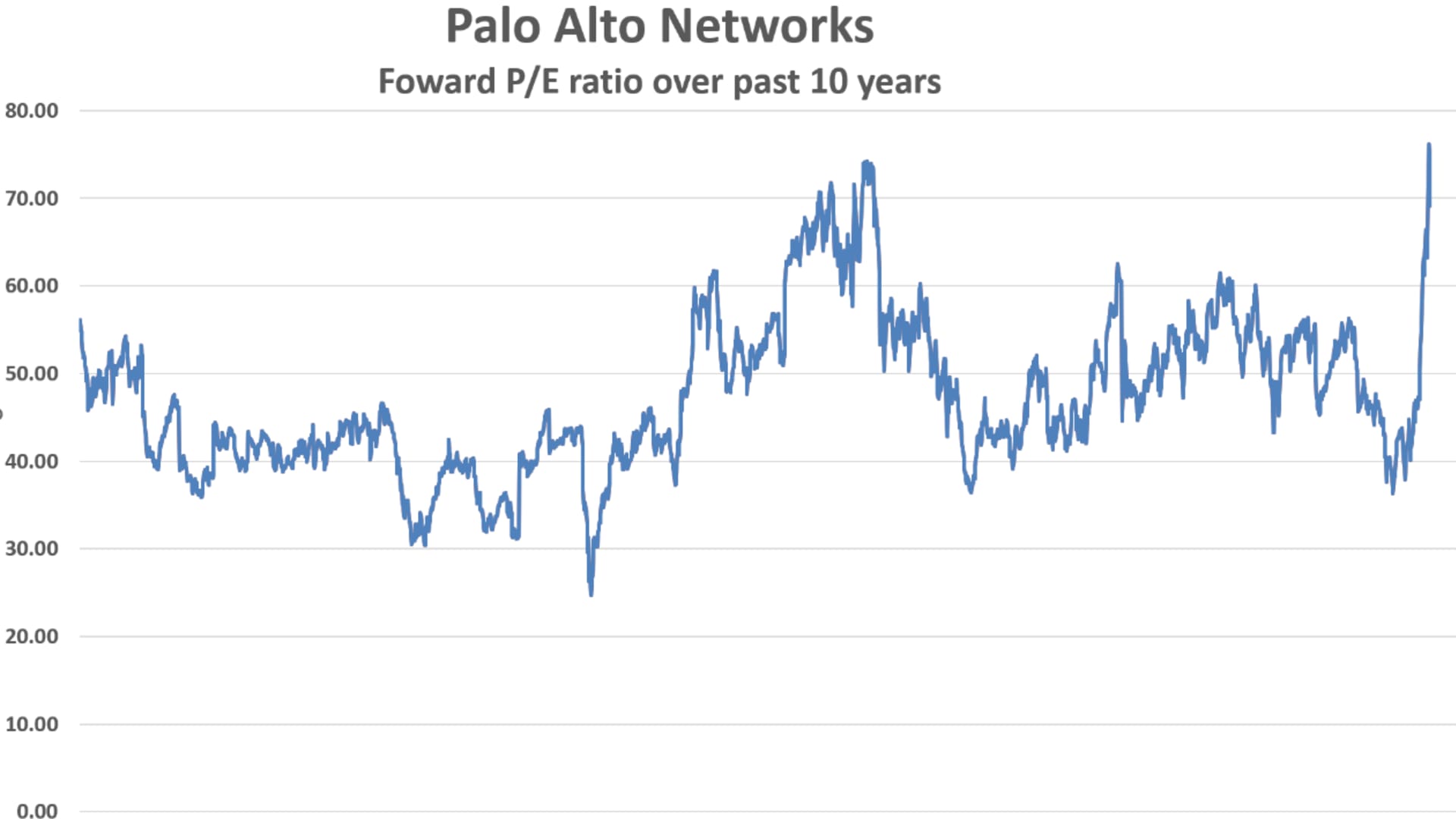

- Valuation Context: With a price-to-earnings ratio nearing 75, the stock is at its highest valuation in a decade, and while future growth is anticipated, the high valuation may lead investors to adopt a cautious stance regarding sustained price increases.

See More

Dell Technologies Emerges as a Leader in AI Infrastructure

- Impressive Earnings: Dell Technologies reported fiscal Q1 2027 results with an 88% year-over-year revenue increase to $43.8 billion, significantly surpassing the $35.5 billion consensus estimate, highlighting its strong performance in the AI infrastructure sector.

- Profitability Surge: The company's non-GAAP earnings reached a record $4.86 per share, up 214% from the previous year and exceeding analyst expectations of $2.99, indicating substantial profit growth amid surging demand for AI servers.

- Order Surge: Dell booked $24.4 billion in new AI server orders last quarter while shipping $16.6 billion, resulting in a massive AI server backlog of $51.3 billion, reflecting strong market demand for its products.

- Optimistic Market Outlook: Dell raised its fiscal 2027 revenue guidance to $167 billion, well above the prior estimate of $140 billion, with the AI server market expected to grow at a 35% annual rate from 2026 to 2034, providing a solid foundation for long-term growth.

See More

Dell Technologies Sees Surge in AI Server Demand

- Impressive Earnings: Dell Technologies reported a record revenue of $43.8 billion for Q1 FY2027, marking an 88% year-over-year increase, significantly exceeding the $35.5 billion consensus estimate, showcasing its robust performance in the AI server market.

- Profitability Surge: The company's non-GAAP earnings per share soared to $4.86, up 214% from the previous year, surpassing analysts' expectations of $2.99, indicating a substantial enhancement in profitability.

- Order Surge: Dell booked $24.4 billion in new AI server orders last quarter, while shipping $16.6 billion, resulting in a massive AI server backlog of $51.3 billion, illustrating that demand is far outpacing supply.

- Optimistic Market Outlook: Dell anticipates FY2027 revenue to reach $167 billion, well above the prior estimate of $140 billion, with projected AI server revenue of $60 billion, reflecting its growing share in the rapidly expanding AI market.

See More

CrowdStrike Appoints New Chief AI Officer

- Executive Appointment: CrowdStrike announced the appointment of Bartley Richardson as Chief AI and Autonomous Systems Officer, who previously led engineering for agentic AI and cybersecurity AI at NVIDIA, showcasing his extensive experience in solving large-scale data challenges.

- Technical Leadership: At NVIDIA, Richardson spearheaded the development of foundational technologies for AI agents, including the NeMo Agent Toolkit and AI-Q research assistant, enabling organizations to operationalize AI at scale, thereby enhancing competitiveness in the cybersecurity sector.

- Strategic Advancement: Richardson now leads CrowdStrike's AI strategy, aiming to transform the company's structural data advantage into more autonomous and deterministic security outcomes, thereby enhancing its ability to prevent data breaches.

- AGI Ambition: CrowdStrike stated that Richardson's addition will accelerate the company's leadership in the field of Artificial General Intelligence (AGI), driving innovation and development in cybersecurity.

See More

CrowdStrike Set to Report Strong Q1 Earnings Amid AI Demand

- Optimistic Earnings Outlook: CrowdStrike is expected to report Q1 EPS of $1.07, reflecting a 46.6% increase, with revenue projected to grow 23.6% to $1.36 billion, indicating strong performance and rising market demand in the cybersecurity sector.

- Analysts Bullish on Future: Stifel and Cantor Fitzgerald have raised their price targets for CrowdStrike, with Cantor Fitzgerald's analyst noting positive feedback from partners regarding ongoing growth in endpoint markets and solid performance in emerging products, suggesting the company may exceed market expectations.

- AI Integration Advantage: The integration of AI into CrowdStrike's platform enhances its threat detection capabilities, providing a competitive edge in addressing advanced cyberattacks, particularly amid rising enterprise cloud adoption.

- Strong Stock Performance: CrowdStrike's stock has surged over 60% this year, significantly outperforming the S&P 500's 11% increase, reflecting market confidence in its growth potential.

See More

Market Volatility and Tech Stock Performance

- Oil Price Impact: Stocks fell as crude oil prices climbed back above $95 per barrel due to renewed airstrikes between the U.S. and Iran, with financials being the worst-performing sector, indicating pressure on rate-sensitive stocks and a negative market sentiment.

- Cybersecurity Stock Pullback: Despite Palo Alto Networks delivering a strong earnings report, its stock declined over 2%, with Jim Cramer urging investors to hold, while anticipating a potential short-term drop of 7% to 8%, reflecting cautious market sentiment regarding future performance.

- New Semiconductor Position: Jim initiated a new position in Intel on Wednesday, believing that demand for CPUs will continue to grow as AI workloads shift from training to inference, stressing that investors should start small rather than chase the stock higher to mitigate risk.

- Rapid Stock Review: In a quick recap, Jim highlighted stocks such as Honeywell, Macy's, Ulta, AT&T, and Kraft Heinz, indicating a focus on diversified investments while reflecting varying perspectives on individual stock performances.

See More

Palo Alto Networks Shares Drop 4% Despite Strong Earnings

- Earnings Beat: Palo Alto Networks shares fell over 4% despite exceeding quarterly expectations, indicating market concerns about the company's long-term outlook despite strong financial results.

- Hardware Growth Outlook: The company raised its hardware growth forecast for the coming quarters, particularly for firewall installations in data centers and enterprise campuses, but management's guidance for fiscal 2030 subscription revenue did not see a significant increase, potentially disappointing investors.

- Market Reaction Analysis: The stock surged approximately 86% over the past two months, yet CEO Nikesh Arora cautioned during the earnings call against expecting substantial earnings growth in the short term, which may have triggered sell-offs from short-term traders.

- Valuation Context: With a price-to-earnings ratio nearing 75, the stock is at its highest valuation in a decade, and while future growth is anticipated, the high valuation may lead investors to adopt a cautious stance regarding sustained price increases.

See More

Dell Technologies Emerges as a Leader in AI Infrastructure

- Impressive Earnings: Dell Technologies reported fiscal Q1 2027 results with an 88% year-over-year revenue increase to $43.8 billion, significantly surpassing the $35.5 billion consensus estimate, highlighting its strong performance in the AI infrastructure sector.

- Profitability Surge: The company's non-GAAP earnings reached a record $4.86 per share, up 214% from the previous year and exceeding analyst expectations of $2.99, indicating substantial profit growth amid surging demand for AI servers.

- Order Surge: Dell booked $24.4 billion in new AI server orders last quarter while shipping $16.6 billion, resulting in a massive AI server backlog of $51.3 billion, reflecting strong market demand for its products.

- Optimistic Market Outlook: Dell raised its fiscal 2027 revenue guidance to $167 billion, well above the prior estimate of $140 billion, with the AI server market expected to grow at a 35% annual rate from 2026 to 2034, providing a solid foundation for long-term growth.

See More

Dell Technologies Sees Surge in AI Server Demand

- Impressive Earnings: Dell Technologies reported a record revenue of $43.8 billion for Q1 FY2027, marking an 88% year-over-year increase, significantly exceeding the $35.5 billion consensus estimate, showcasing its robust performance in the AI server market.

- Profitability Surge: The company's non-GAAP earnings per share soared to $4.86, up 214% from the previous year, surpassing analysts' expectations of $2.99, indicating a substantial enhancement in profitability.

- Order Surge: Dell booked $24.4 billion in new AI server orders last quarter, while shipping $16.6 billion, resulting in a massive AI server backlog of $51.3 billion, illustrating that demand is far outpacing supply.

- Optimistic Market Outlook: Dell anticipates FY2027 revenue to reach $167 billion, well above the prior estimate of $140 billion, with projected AI server revenue of $60 billion, reflecting its growing share in the rapidly expanding AI market.

See More

CrowdStrike Appoints New Chief AI Officer

- Executive Appointment: CrowdStrike announced the appointment of Bartley Richardson as Chief AI and Autonomous Systems Officer, who previously led engineering for agentic AI and cybersecurity AI at NVIDIA, showcasing his extensive experience in solving large-scale data challenges.

- Technical Leadership: At NVIDIA, Richardson spearheaded the development of foundational technologies for AI agents, including the NeMo Agent Toolkit and AI-Q research assistant, enabling organizations to operationalize AI at scale, thereby enhancing competitiveness in the cybersecurity sector.

- Strategic Advancement: Richardson now leads CrowdStrike's AI strategy, aiming to transform the company's structural data advantage into more autonomous and deterministic security outcomes, thereby enhancing its ability to prevent data breaches.

- AGI Ambition: CrowdStrike stated that Richardson's addition will accelerate the company's leadership in the field of Artificial General Intelligence (AGI), driving innovation and development in cybersecurity.

See More