Brady to Acquire Honeywell's PSS Business, Sees Double-Digit EPS Growth

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 26 2026

0mins

Source: Yahoo Finance

- Acquisition Announcement: Brady has announced plans to acquire Honeywell's Productivity Solutions and Services (PSS) business, which is expected to contribute double-digit accretion to adjusted diluted EPS within the first year post-close, marking a strategic shift into data capture and workforce solutions.

- Financial Expectations: PSS generated approximately $1.1 billion in revenue for the 12 months ending December 31, 2025, and Brady anticipates at least $25 million in annual run-rate cost synergies within three years of closing, primarily through improved operational efficiencies.

- Market Expansion: This acquisition positions Brady to enter the $9 billion technology-enabled data capture and workflow solutions market, enhancing its customer base in verticals such as retail, logistics, and warehousing, thereby driving long-term growth.

- R&D Integration: Brady plans to integrate PSS's R&D team with its own, resulting in an expected combined R&D spend of around $200 million, which will further enhance product innovation capabilities and strengthen market competitiveness.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BRC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BRC

Wall Street analysts forecast BRC stock price to rise

1 Analyst Rating

1 Buy

0 Hold

0 Sell

Moderate Buy

Current: 88.630

Low

96.00

Averages

96.00

High

96.00

Current: 88.630

Low

96.00

Averages

96.00

High

96.00

No data

About BRC

Brady Corporation is a manufacturer and supplier of identification solutions and workplace safety products that identify and protect premises, products and people. Its product categories include Safety and facility identification and protection, which include safety signs, traffic signs and control products, floor-marking tape, pipe markers, labeling systems, spill control products, lockout/tagout devices, first aid products, and software and services for safety compliance auditing, procedures writing and training; Wire identification, which includes handheld printers, wire markers, sleeves, and tags. Healthcare identification, which includes wristbands, labels, printing systems, and other products used in hospital, laboratory, and other healthcare settings; People identification, which includes name tags, badges, lanyards, rigid card printing systems, and access control software; and Product identification. It also provides direct part marking solutions.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Brady Corporation CEO Retirement Sparks 10.4% Stock Drop

- CEO Sudden Retirement: Brady Corporation's announcement of CEO Russell Shaller's immediate retirement led to a 10.4% drop in stock price by 1 p.m., raising investor concerns about the company's upcoming strategic transformation.

- New CEO Background: Board member Vineet Nargolwala will take over as CEO while remaining on the board, bringing nearly a decade of experience from Honeywell, which may facilitate a smooth transition during this critical period.

- Acquisition Impact: The CEO change coincides with Brady's plan to acquire Honeywell's Productivity Solutions and Services business in the second half of 2026, which is expected to enhance its competitive edge in mobile and handheld scanning devices.

- Investment Opportunity Analysis: Despite the stock drop, analysts view this as an attractive buying opportunity, as Brady's potential in AI labeling and acquisition-driven growth could appeal to long-term investors.

See More

Brady Corporation's CEO Transition and Acquisition Impact Analysis

- CEO Transition Impact: Brady Corporation's announcement of CEO Russell Shaller's immediate retirement resulted in a 10.4% drop in stock price by 1 p.m., raising investor concerns about the company's strategic transformation ahead.

- Acquisition Plans: The company is set to acquire Honeywell's Productivity Solutions and Services business in the second half of 2026, which will enhance Brady's expertise in mobile and handheld scanning devices, thereby strengthening its competitive position in the labeling and printing market.

- New CEO Background: Incoming CEO Vineet Nargolwala has nearly a decade of experience at Honeywell, and while the timing of the transition raises concerns, his background may provide stability for the company's future direction.

- Investment Opportunity: Despite the stock price dip, Brady is viewed as an attractive investment opportunity due to its potential exposure to AI-related data center spending and the growth prospects from the acquisition, appealing to investors looking for under-the-radar plays.

See More

Brady Corp Appoints New CEO Vineet Nargolwala Amid Leadership Transition

- Leadership Change: Brady Corp announced the appointment of current board member Vineet Nargolwala as CEO effective June 8, succeeding Russell Shaller, who will retire after 11 years and remain as a consultant until August 1 to ensure a smooth transition.

- Board Confidence: The board believes Nargolwala's experience over the past four years as a board member positions him well to lead the company as it expands, particularly in light of its planned acquisition of Honeywell's Productivity Solutions and Services business.

- Market Reaction: In pre-market trading, Brady Corp's stock fell 1.47% to $87.35, while Allegro MicroSystems saw a 2.26% increase to $47.44, indicating varied market responses to the leadership change.

- Strategic Expansion: Nargolwala's appointment is viewed as a crucial step for the company to drive growth and market expansion following the acquisition of Honeywell's business, reflecting a positive outlook for future developments.

See More

AI Stocks Show Strong Fundamentals Amid Rising Valuations

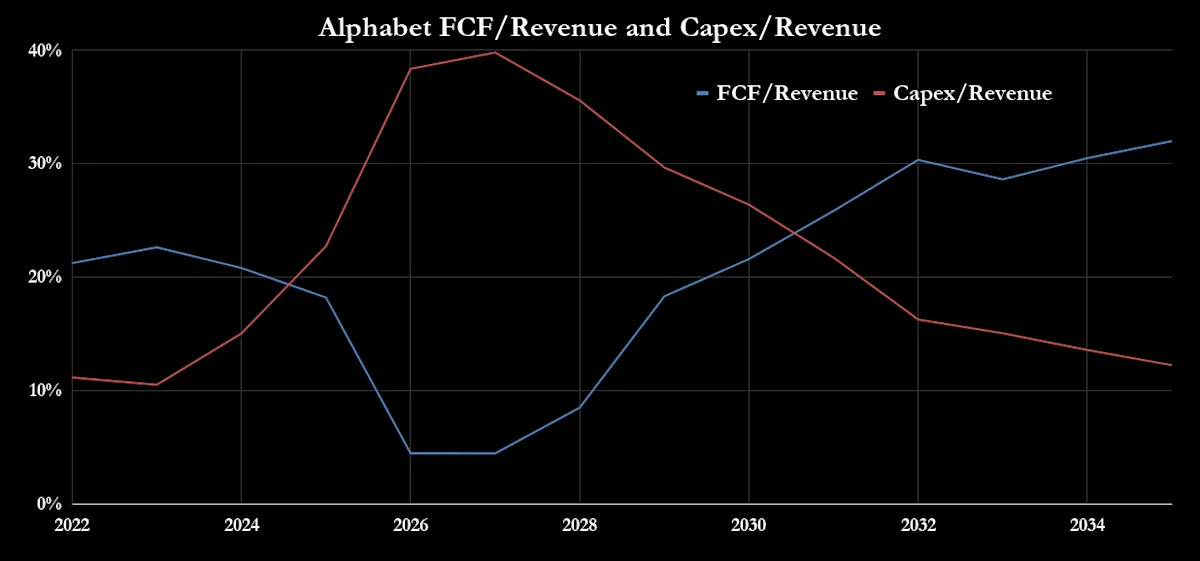

- Alphabet's Capital Surge: Alphabet's capital expenditures are soaring to support future AI growth, with free cash flow (FCF) declining; projections suggest a stable 30% FCF margin and over $1 trillion in revenue by 2030, translating to approximately $333 billion in FCF.

- Brady's Growth Potential: Brady Corporation's wire identification products account for 20% of revenue in the Americas and Asia, and 13% in Europe and Australia, with growth rates of 19% and 13% respectively, significantly outpacing the company's overall growth of 13.8%, highlighting its strong performance in the data center market.

- Belden's Market Opportunities: Belden's connectivity products benefit from rapid data center construction growth, and while trading at a discount to peers like TE Connectivity and Amphenol, its fast-growing exposure positions it as an attractive option for value investors seeking AI upside.

- Synergistic Acquisition: Brady's upcoming acquisition of Honeywell's Productivity Solutions and Services, set for integration in fiscal 2027, is expected to yield an EPS of $6.09, showcasing strong investment value driven by data center revenue factors.

See More

Alphabet's Valuation Analysis and AI Investment Outlook

- Data Center Sales Growth: Alphabet's data center-related sales are rapidly increasing, with projections indicating that by 2030, digital network spending will surpass data center infrastructure spending, suggesting sustained revenue growth driven by AI investments.

- Capital Expenditure and Free Cash Flow: Although Alphabet's capital expenditures are soaring, leading to a decline in annual free cash flow, it is expected that as the spending ratio decreases, free cash flow will gradually rebound, potentially reaching $333 billion by the 2030s.

- Brady's Growth Potential: Brady's wire identification products account for 20% of its revenue in the Americas and Asia, with growth rates of 19% and 13% in the third quarter, respectively, indicating strong growth potential in the data center market that will further enhance overall sales.

- Belden's Market Opportunities: Belden's connectivity products benefit from the rapid growth in data center construction, and its acquisition of RUCKUS Networks will enhance its exposure to inference spending, expected to provide substantial long-term growth for the company.

See More

2026 Analysis of AI Stock Investment Opportunities

- Alphabet's Capital Expenditure: Alphabet's capital spending is surging, with projections indicating over $1 trillion in revenue by the 2030s, potentially leading to $333 billion in free cash flow (FCF), highlighting its robust investment potential in AI infrastructure.

- Brady's Growth Potential: Brady Corporation's wire identification products account for 20% of revenue in the Americas and Asia, and 13% in Europe and Australia, with growth rates of 19% and 13% respectively, significantly outpacing the company's overall growth of 13.8%, indicating strong demand in the data center market.

- Belden's Market Outlook: Belden's connectivity products are benefiting from rapid data center build-out, with inference spending expected to surpass data center spending in the 2030s, and its price-to-earnings ratio is significantly lower than peers, making it an attractive value investment.

- Synergistic Acquisition: Brady's upcoming acquisition of Honeywell's Productivity Solutions and Services is expected to enhance its leadership in mobile and handheld scanning devices, combining with its printing and labeling expertise to create substantial growth opportunities in the future.

See More

Brady Corporation CEO Retirement Sparks 10.4% Stock Drop

- CEO Sudden Retirement: Brady Corporation's announcement of CEO Russell Shaller's immediate retirement led to a 10.4% drop in stock price by 1 p.m., raising investor concerns about the company's upcoming strategic transformation.

- New CEO Background: Board member Vineet Nargolwala will take over as CEO while remaining on the board, bringing nearly a decade of experience from Honeywell, which may facilitate a smooth transition during this critical period.

- Acquisition Impact: The CEO change coincides with Brady's plan to acquire Honeywell's Productivity Solutions and Services business in the second half of 2026, which is expected to enhance its competitive edge in mobile and handheld scanning devices.

- Investment Opportunity Analysis: Despite the stock drop, analysts view this as an attractive buying opportunity, as Brady's potential in AI labeling and acquisition-driven growth could appeal to long-term investors.

See More

Brady Corporation's CEO Transition and Acquisition Impact Analysis

- CEO Transition Impact: Brady Corporation's announcement of CEO Russell Shaller's immediate retirement resulted in a 10.4% drop in stock price by 1 p.m., raising investor concerns about the company's strategic transformation ahead.

- Acquisition Plans: The company is set to acquire Honeywell's Productivity Solutions and Services business in the second half of 2026, which will enhance Brady's expertise in mobile and handheld scanning devices, thereby strengthening its competitive position in the labeling and printing market.

- New CEO Background: Incoming CEO Vineet Nargolwala has nearly a decade of experience at Honeywell, and while the timing of the transition raises concerns, his background may provide stability for the company's future direction.

- Investment Opportunity: Despite the stock price dip, Brady is viewed as an attractive investment opportunity due to its potential exposure to AI-related data center spending and the growth prospects from the acquisition, appealing to investors looking for under-the-radar plays.

See More

Brady Corp Appoints New CEO Vineet Nargolwala Amid Leadership Transition

- Leadership Change: Brady Corp announced the appointment of current board member Vineet Nargolwala as CEO effective June 8, succeeding Russell Shaller, who will retire after 11 years and remain as a consultant until August 1 to ensure a smooth transition.

- Board Confidence: The board believes Nargolwala's experience over the past four years as a board member positions him well to lead the company as it expands, particularly in light of its planned acquisition of Honeywell's Productivity Solutions and Services business.

- Market Reaction: In pre-market trading, Brady Corp's stock fell 1.47% to $87.35, while Allegro MicroSystems saw a 2.26% increase to $47.44, indicating varied market responses to the leadership change.

- Strategic Expansion: Nargolwala's appointment is viewed as a crucial step for the company to drive growth and market expansion following the acquisition of Honeywell's business, reflecting a positive outlook for future developments.

See More

AI Stocks Show Strong Fundamentals Amid Rising Valuations

- Alphabet's Capital Surge: Alphabet's capital expenditures are soaring to support future AI growth, with free cash flow (FCF) declining; projections suggest a stable 30% FCF margin and over $1 trillion in revenue by 2030, translating to approximately $333 billion in FCF.

- Brady's Growth Potential: Brady Corporation's wire identification products account for 20% of revenue in the Americas and Asia, and 13% in Europe and Australia, with growth rates of 19% and 13% respectively, significantly outpacing the company's overall growth of 13.8%, highlighting its strong performance in the data center market.

- Belden's Market Opportunities: Belden's connectivity products benefit from rapid data center construction growth, and while trading at a discount to peers like TE Connectivity and Amphenol, its fast-growing exposure positions it as an attractive option for value investors seeking AI upside.

- Synergistic Acquisition: Brady's upcoming acquisition of Honeywell's Productivity Solutions and Services, set for integration in fiscal 2027, is expected to yield an EPS of $6.09, showcasing strong investment value driven by data center revenue factors.

See More

Alphabet's Valuation Analysis and AI Investment Outlook

- Data Center Sales Growth: Alphabet's data center-related sales are rapidly increasing, with projections indicating that by 2030, digital network spending will surpass data center infrastructure spending, suggesting sustained revenue growth driven by AI investments.

- Capital Expenditure and Free Cash Flow: Although Alphabet's capital expenditures are soaring, leading to a decline in annual free cash flow, it is expected that as the spending ratio decreases, free cash flow will gradually rebound, potentially reaching $333 billion by the 2030s.

- Brady's Growth Potential: Brady's wire identification products account for 20% of its revenue in the Americas and Asia, with growth rates of 19% and 13% in the third quarter, respectively, indicating strong growth potential in the data center market that will further enhance overall sales.

- Belden's Market Opportunities: Belden's connectivity products benefit from the rapid growth in data center construction, and its acquisition of RUCKUS Networks will enhance its exposure to inference spending, expected to provide substantial long-term growth for the company.

See More

2026 Analysis of AI Stock Investment Opportunities

- Alphabet's Capital Expenditure: Alphabet's capital spending is surging, with projections indicating over $1 trillion in revenue by the 2030s, potentially leading to $333 billion in free cash flow (FCF), highlighting its robust investment potential in AI infrastructure.

- Brady's Growth Potential: Brady Corporation's wire identification products account for 20% of revenue in the Americas and Asia, and 13% in Europe and Australia, with growth rates of 19% and 13% respectively, significantly outpacing the company's overall growth of 13.8%, indicating strong demand in the data center market.

- Belden's Market Outlook: Belden's connectivity products are benefiting from rapid data center build-out, with inference spending expected to surpass data center spending in the 2030s, and its price-to-earnings ratio is significantly lower than peers, making it an attractive value investment.

- Synergistic Acquisition: Brady's upcoming acquisition of Honeywell's Productivity Solutions and Services is expected to enhance its leadership in mobile and handheld scanning devices, combining with its printing and labeling expertise to create substantial growth opportunities in the future.

See More