Analysis of Tilray Brands' 95% Stock Plunge

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy TLRY?

Source: Fool

- Stock Plunge: Tilray Brands' shares have plummeted over 95% in the past five years, causing panic among some investors while others see a potential rebound opportunity; however, cheap stocks can often be value traps.

- Valuation Analysis: Despite a trailing P/E ratio of 57.5, Tilray's price-to-book ratio stands at 0.54, indicating a seemingly attractive valuation, yet half of its book value is goodwill, which the company has previously written off, posing future risks.

- Profitability Issues: Tilray has shown inconsistent profitability and has been consistently losing money; while it ranks first in the Canadian adult-use cannabis market, the oversupply in the market has driven prices down, negatively impacting its financial outlook.

- Potential Catalyst: The U.S. is in the process of reclassifying marijuana, which could lift IRS Section 280E restrictions, potentially improving Tilray's financials; if successful, this could lead to significant growth opportunities in the coming years.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TLRY?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on TLRY

Wall Street analysts forecast TLRY stock price to rise

4 Analyst Rating

1 Buy

3 Hold

0 Sell

Hold

Current: 6.940

Low

8.50

Averages

9.57

High

10.00

Current: 6.940

Low

8.50

Averages

9.57

High

10.00

About TLRY

Tilray Brands, Inc. is a global lifestyle and consumer packaged goods company. It operates through four segments: cannabis operations, beverage operations, distribution operations, and the wellness business. The Cannabis operations, which encompasses the production, distribution, sale, co-manufacturing and advisory services of both medical and adult-use cannabis. The beverage operations, which encompasses the production, marketing and of beverage products. The distribution operations, which encompasses the purchase and resale of pharmaceutical products to customers. The Wellness products, which encompasses wellness and better-for-you foods and beverages. Its brands include Good Supply, RIFF, Broken Coast, Solei, Canaca, HEXO, Redecan, Original Stash, Hop Valley, Revolver, Bake Sale, XMG, Mollo, Chowie Wowie and others. It supports over 40 brands in over 20 countries, including cannabis offerings, hemp-based foods and craft beverages.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Tilray: Value Trap or Value Stock?

- Poor Stock Performance: Tilray's shares have plummeted over 95% in the past five years, which, despite the company's market leadership and improving balance sheet, has deterred some investors, indicating market concerns about its future prospects.

- Valuation Metrics Analysis: With a price-to-book ratio of 0.54, Tilray appears cheap; however, approximately half of its book value ($752 million) consists of goodwill, which has been significantly written off in the past, raising concerns about its future valuation stability.

- Inconsistent Profitability: While Tilray ranks first in the Canadian adult-use cannabis market, its profitability has been inconsistent and it has consistently reported losses, reflecting the company's vulnerability amid changing market dynamics, particularly during periods of supply-demand imbalance.

- Potential Catalyst: The U.S. is in the process of reclassifying marijuana, which could lift IRS Section 280E restrictions, allowing Tilray to deduct most business expenses, potentially leading to significant financial improvements if successfully implemented.

See More

Analysis of Tilray Brands' 95% Stock Plunge

- Stock Plunge: Tilray Brands' shares have plummeted over 95% in the past five years, causing panic among some investors while others see a potential rebound opportunity; however, cheap stocks can often be value traps.

- Valuation Analysis: Despite a trailing P/E ratio of 57.5, Tilray's price-to-book ratio stands at 0.54, indicating a seemingly attractive valuation, yet half of its book value is goodwill, which the company has previously written off, posing future risks.

- Profitability Issues: Tilray has shown inconsistent profitability and has been consistently losing money; while it ranks first in the Canadian adult-use cannabis market, the oversupply in the market has driven prices down, negatively impacting its financial outlook.

- Potential Catalyst: The U.S. is in the process of reclassifying marijuana, which could lift IRS Section 280E restrictions, potentially improving Tilray's financials; if successful, this could lead to significant growth opportunities in the coming years.

See More

Meta Strikes Major Chip Deal with AWS to Enhance AI Infrastructure

- Infrastructure Investment: Meta has signed a three-year deal with AWS to deploy hundreds of thousands of Graviton chips, aiming to enhance AI performance with an expected 60% better energy efficiency than traditional systems, showcasing Meta's strategic commitment to AI.

- Workforce Adjustment: Despite the massive infrastructure investment, Meta announced a 10% workforce reduction, indicating a shift in capital allocation from human resources to high-performance silicon, reflecting the company's focus on future technology demands.

- Intensifying Market Competition: This move by Meta comes as competitors like Alphabet and Microsoft accelerate their internal hardware development, highlighting the urgency for Meta to secure computing capacity, which could reshape the industry landscape.

- CPU Renaissance: Intel has noted that central processors are re-emerging as the foundation for AI, and Meta's choice of Graviton chips over specialized accelerators indicates confidence in general-purpose processors, potentially driving growth across the semiconductor sector.

See More

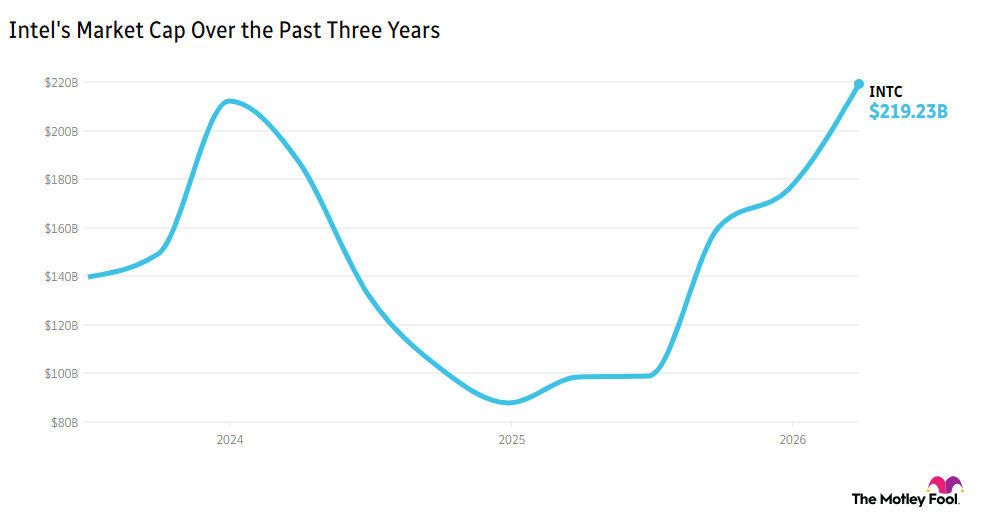

Intel CEO Tan Highlights Promising AI Future

- AI Business Growth: Intel (INTC) shares surged over 25% ahead of market open as CEO Lip-Bu Tan highlighted the company's pivot to AI, with financial outlook upgraded, projecting next quarter's revenue to rise from $13 billion to between $13.8 billion and $14.8 billion, indicating strong market demand and successful strategic transformation.

- Capacity Enhancement Plans: CFO David Zinsner stated that in response to soaring demand for data center processors, Intel is focused on rapidly increasing capacity to meet customer needs and avoid supply shortages, thereby enhancing its competitive position in the market.

- Strengthening Industry Position: Tan emphasized that as AI systems become more complex, Intel's CPUs remain the backbone of AI computing architecture, a trend that will further drive the company's market share and revenue growth in the future, showcasing its leadership in technological innovation.

- Positive Market Reaction: The market reacted enthusiastically to Intel's positive outlook and strong performance, reflecting investor confidence in the company's future development and further solidifying Intel's position in the tech industry.

See More

U.S. Places Medical Cannabis Products in Schedule III

- Policy Impact: The U.S. government's decision to place FDA-approved marijuana products and state-licensed medical cannabis programs into Schedule III is expected to facilitate clinical research and broaden treatment access, thereby enhancing the legitimacy of medical cannabis in modern healthcare.

- Tilray's Expansion Plans: Tilray is exploring participation in a federal pilot program run by the Center for Medicare and Medicaid Innovation, aiming to supply hemp-derived medical cannabis through cancer clinics, which is intended to improve services for underserved patients.

- Market Reaction Volatility: Although Tilray's stock surged by 19% following the policy announcement, it ultimately closed down 12%, reflecting investor concerns over the limited scope of the order, which also negatively impacted other cannabis companies' stock prices.

- Optimistic Industry Outlook: Roth Capital Partners views the partial rescheduling order as “extremely favorable,” potentially alleviating Section 280E tax restrictions, improving import and export prospects, and paving the way for eventual adult-use rescheduling, thus enhancing overall sector investability.

See More

DOJ Updates Marijuana Classification Policy

- Policy Change Context: The U.S. Department of Justice has formally proposed reclassifying state-licensed medical marijuana from Schedule I to Schedule III, which, while not legalizing marijuana, reduces regulatory hurdles and offers tax relief for licensed operators, expected to enhance medical research and expand access to treatments.

- Market Reaction: Following the announcement, shares of Tilray (TLRY), Canopy Growth (CGC), Aurora Cannabis (ACB), and IGC Pharma (IGC) fell between 2-5% in morning trading despite previous gains, indicating a cautious market response to the policy change.

- Investor Sentiment: Retail sentiment on Stocktwits for TLRY, CGC, ACB, and IGC turned ‘extremely bullish’ with message volumes surging, reflecting optimistic expectations for the cannabis industry's revival, with some users claiming Tilray will become the “king of the U.S. cannabis market.”

- Akanda Corp. Outperformance: In contrast to major cannabis stocks, Akanda Corp. (AKAN) saw a 6% increase, extending a remarkable 215% surge from the previous session, with investors debating whether this explosive rally is driven by optimism over cannabis reclassification or the stock's low float.

See More

Tilray: Value Trap or Value Stock?

- Poor Stock Performance: Tilray's shares have plummeted over 95% in the past five years, which, despite the company's market leadership and improving balance sheet, has deterred some investors, indicating market concerns about its future prospects.

- Valuation Metrics Analysis: With a price-to-book ratio of 0.54, Tilray appears cheap; however, approximately half of its book value ($752 million) consists of goodwill, which has been significantly written off in the past, raising concerns about its future valuation stability.

- Inconsistent Profitability: While Tilray ranks first in the Canadian adult-use cannabis market, its profitability has been inconsistent and it has consistently reported losses, reflecting the company's vulnerability amid changing market dynamics, particularly during periods of supply-demand imbalance.

- Potential Catalyst: The U.S. is in the process of reclassifying marijuana, which could lift IRS Section 280E restrictions, allowing Tilray to deduct most business expenses, potentially leading to significant financial improvements if successfully implemented.

See More

Analysis of Tilray Brands' 95% Stock Plunge

- Stock Plunge: Tilray Brands' shares have plummeted over 95% in the past five years, causing panic among some investors while others see a potential rebound opportunity; however, cheap stocks can often be value traps.

- Valuation Analysis: Despite a trailing P/E ratio of 57.5, Tilray's price-to-book ratio stands at 0.54, indicating a seemingly attractive valuation, yet half of its book value is goodwill, which the company has previously written off, posing future risks.

- Profitability Issues: Tilray has shown inconsistent profitability and has been consistently losing money; while it ranks first in the Canadian adult-use cannabis market, the oversupply in the market has driven prices down, negatively impacting its financial outlook.

- Potential Catalyst: The U.S. is in the process of reclassifying marijuana, which could lift IRS Section 280E restrictions, potentially improving Tilray's financials; if successful, this could lead to significant growth opportunities in the coming years.

See More

Meta Strikes Major Chip Deal with AWS to Enhance AI Infrastructure

- Infrastructure Investment: Meta has signed a three-year deal with AWS to deploy hundreds of thousands of Graviton chips, aiming to enhance AI performance with an expected 60% better energy efficiency than traditional systems, showcasing Meta's strategic commitment to AI.

- Workforce Adjustment: Despite the massive infrastructure investment, Meta announced a 10% workforce reduction, indicating a shift in capital allocation from human resources to high-performance silicon, reflecting the company's focus on future technology demands.

- Intensifying Market Competition: This move by Meta comes as competitors like Alphabet and Microsoft accelerate their internal hardware development, highlighting the urgency for Meta to secure computing capacity, which could reshape the industry landscape.

- CPU Renaissance: Intel has noted that central processors are re-emerging as the foundation for AI, and Meta's choice of Graviton chips over specialized accelerators indicates confidence in general-purpose processors, potentially driving growth across the semiconductor sector.

See More

Intel CEO Tan Highlights Promising AI Future

- AI Business Growth: Intel (INTC) shares surged over 25% ahead of market open as CEO Lip-Bu Tan highlighted the company's pivot to AI, with financial outlook upgraded, projecting next quarter's revenue to rise from $13 billion to between $13.8 billion and $14.8 billion, indicating strong market demand and successful strategic transformation.

- Capacity Enhancement Plans: CFO David Zinsner stated that in response to soaring demand for data center processors, Intel is focused on rapidly increasing capacity to meet customer needs and avoid supply shortages, thereby enhancing its competitive position in the market.

- Strengthening Industry Position: Tan emphasized that as AI systems become more complex, Intel's CPUs remain the backbone of AI computing architecture, a trend that will further drive the company's market share and revenue growth in the future, showcasing its leadership in technological innovation.

- Positive Market Reaction: The market reacted enthusiastically to Intel's positive outlook and strong performance, reflecting investor confidence in the company's future development and further solidifying Intel's position in the tech industry.

See More

U.S. Places Medical Cannabis Products in Schedule III

- Policy Impact: The U.S. government's decision to place FDA-approved marijuana products and state-licensed medical cannabis programs into Schedule III is expected to facilitate clinical research and broaden treatment access, thereby enhancing the legitimacy of medical cannabis in modern healthcare.

- Tilray's Expansion Plans: Tilray is exploring participation in a federal pilot program run by the Center for Medicare and Medicaid Innovation, aiming to supply hemp-derived medical cannabis through cancer clinics, which is intended to improve services for underserved patients.

- Market Reaction Volatility: Although Tilray's stock surged by 19% following the policy announcement, it ultimately closed down 12%, reflecting investor concerns over the limited scope of the order, which also negatively impacted other cannabis companies' stock prices.

- Optimistic Industry Outlook: Roth Capital Partners views the partial rescheduling order as “extremely favorable,” potentially alleviating Section 280E tax restrictions, improving import and export prospects, and paving the way for eventual adult-use rescheduling, thus enhancing overall sector investability.

See More

DOJ Updates Marijuana Classification Policy

- Policy Change Context: The U.S. Department of Justice has formally proposed reclassifying state-licensed medical marijuana from Schedule I to Schedule III, which, while not legalizing marijuana, reduces regulatory hurdles and offers tax relief for licensed operators, expected to enhance medical research and expand access to treatments.

- Market Reaction: Following the announcement, shares of Tilray (TLRY), Canopy Growth (CGC), Aurora Cannabis (ACB), and IGC Pharma (IGC) fell between 2-5% in morning trading despite previous gains, indicating a cautious market response to the policy change.

- Investor Sentiment: Retail sentiment on Stocktwits for TLRY, CGC, ACB, and IGC turned ‘extremely bullish’ with message volumes surging, reflecting optimistic expectations for the cannabis industry's revival, with some users claiming Tilray will become the “king of the U.S. cannabis market.”

- Akanda Corp. Outperformance: In contrast to major cannabis stocks, Akanda Corp. (AKAN) saw a 6% increase, extending a remarkable 215% surge from the previous session, with investors debating whether this explosive rally is driven by optimism over cannabis reclassification or the stock's low float.

See More