Amazon and Microsoft Data Center Spending Analysis

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Source: Fool

- Market Spending Overview: Amazon and Microsoft are the two largest spenders in the data center market, reflecting their ongoing investment intentions in cloud computing infrastructure aimed at enhancing their competitive positions.

- Stock Performance: As of May 17, 2026, Amazon's stock price was 2.08% and Microsoft's was 1.45%, indicating their relative performance in the market, which may influence investor expectations for future growth.

- Industry Trends: With the continuous growth in cloud computing demand, the spending by Amazon and Microsoft is expected to drive the overall development of the data center industry, further solidifying their leadership in the global market.

- Investment Strategy: The substantial investments by both companies in data centers not only enhance their technological infrastructure but also provide a solid foundation for future business expansion and innovation, signaling ongoing market growth potential.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 421.060

Low

500.00

Averages

631.36

High

678.00

Current: 421.060

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft's AI Investments Drive Strong Growth

- Surge in Capital Expenditure: Microsoft plans to ramp up capital expenditures to $190 billion in the second half of 2026, which has pressured stock prices; however, the company's strong returns on invested capital indicate significant long-term growth potential.

- Azure Revenue Growth: Azure's revenue surged 40% in the most recent quarter, driven by both AI and non-AI services, demonstrating the company's sustained competitiveness in the cloud computing market.

- Strong Microsoft 365 Performance: Commercial software sales rose 19% year-over-year, while consumer version revenue increased by 33%, and Copilot user additions soared 250%, highlighting robust market demand and growth potential for the product.

- Analysts' Optimistic Outlook: Despite shares trading at about 25 times forward earnings expectations, analysts foresee a 30% increase in Microsoft's stock over the next year, reflecting confidence in its ongoing profitability and investment returns.

See More

OpenAI Expected to File for IPO Soon

- Upcoming IPO Filing: OpenAI is expected to file for its initial public offering (IPO) in the coming days or weeks, backed by Microsoft, indicating strong growth potential in the AI sector.

- Valuation Surge: The latest funding round has propelled OpenAI's valuation to $852 billion, with a monthly revenue of $2 billion, showcasing the success of its business model and robust market demand.

- Industry Impact: This news comes just two days after OpenAI CEO Sam Altman won a lawsuit against Tesla CEO Elon Musk, further solidifying its market position.

- Market Frenzy: With OpenAI and Anthropic preparing for IPOs, the investment frenzy in the AI sector is intensifying, attracting increased attention from investors.

See More

Microsoft's Maia Chips Enhance AI Infrastructure Amid Nvidia Dependency Reduction

- Chip Development Strategy: Microsoft is collaborating with Google and Amazon to develop Maia chips aimed at reducing dependence on Nvidia semiconductors, although discussions are still in early stages and may not lead to a final agreement.

- Maia 200 Chip Performance: Launched in January 2026, the Maia 200 chip utilizes TSMC's 3-nanometer process, with Microsoft claiming a 30% improvement in performance per dollar compared to existing systems, and higher memory bandwidth than Amazon and Google's counterparts.

- Collaboration with Anthropic: Anthropic is reportedly in talks with Microsoft to rent custom AI server chips to expand its computing capacity to meet rising demand for AI services, although discussions are still in preliminary stages.

- Market Sentiment Analysis: According to Stocktwits, retail sentiment for Microsoft has shifted from neutral to bullish, despite MSFT stock falling about 14% year-to-date, currently trading at $417, indicating potential market confidence in the Maia chips.

See More

Intuitive Surgical and Microsoft: Long-Term Investment Opportunities

- Financial Challenges for ISRG: Despite facing steep tariffs, Intuitive Surgical reported significant revenue and procedure volume growth in Q1, solidifying its market leadership in robotic-assisted surgery and indicating strong long-term growth potential.

- New Product Momentum: The latest da Vinci model accounted for 54% of the company's system placements in Q1, and its strong market adoption not only enhances technological advantages but also provides valuable feedback for future product improvements.

- Microsoft's AI Revenue Surge: Microsoft plans to invest $190 billion in AI-related capital expenditures by 2026, with its AI business already achieving an annual revenue run rate of $37 billion, reflecting a 123% year-over-year growth and showcasing the company's robust performance in the AI revolution.

- Cloud Computing Leadership: Microsoft's cloud backlog surged 99% year-over-year to $627 billion in the latest quarter, and combined with its AAA credit rating and a 153% dividend increase over the past decade, this further solidifies its appeal as a long-term investment.

See More

Market Outlook for Intuitive Surgical and Microsoft

- Solid Financial Performance: Despite facing steep tariffs, Intuitive Surgical achieved significant revenue and procedure volume growth in Q1, further solidifying its market leadership in robotic-assisted surgery, demonstrating the company's strong competitive position in the medical device sector.

- Sustained Technological Edge: The latest da Vinci 5 model accounted for nearly 54% of the company's installed systems in Q1, and this strong market acceptance not only enhances the company's technological advantage but also provides valuable feedback for future product improvements.

- AI-Driven Growth Potential: Microsoft plans to invest $190 billion by 2026 to support its AI-related strategies; despite concerns about its services being replaced by AI, the company has already achieved an annual revenue run rate of $37 billion in its AI business, reflecting a 123% year-over-year growth and showcasing its adaptability in technological transformation.

- Cloud Market Leadership: Microsoft's cloud backlog surged 99% year-over-year to $627 billion in the most recent quarter, and combined with its AAA credit rating and a 153% dividend increase over the past decade, this further underscores its attractiveness as a long-term investment.

See More

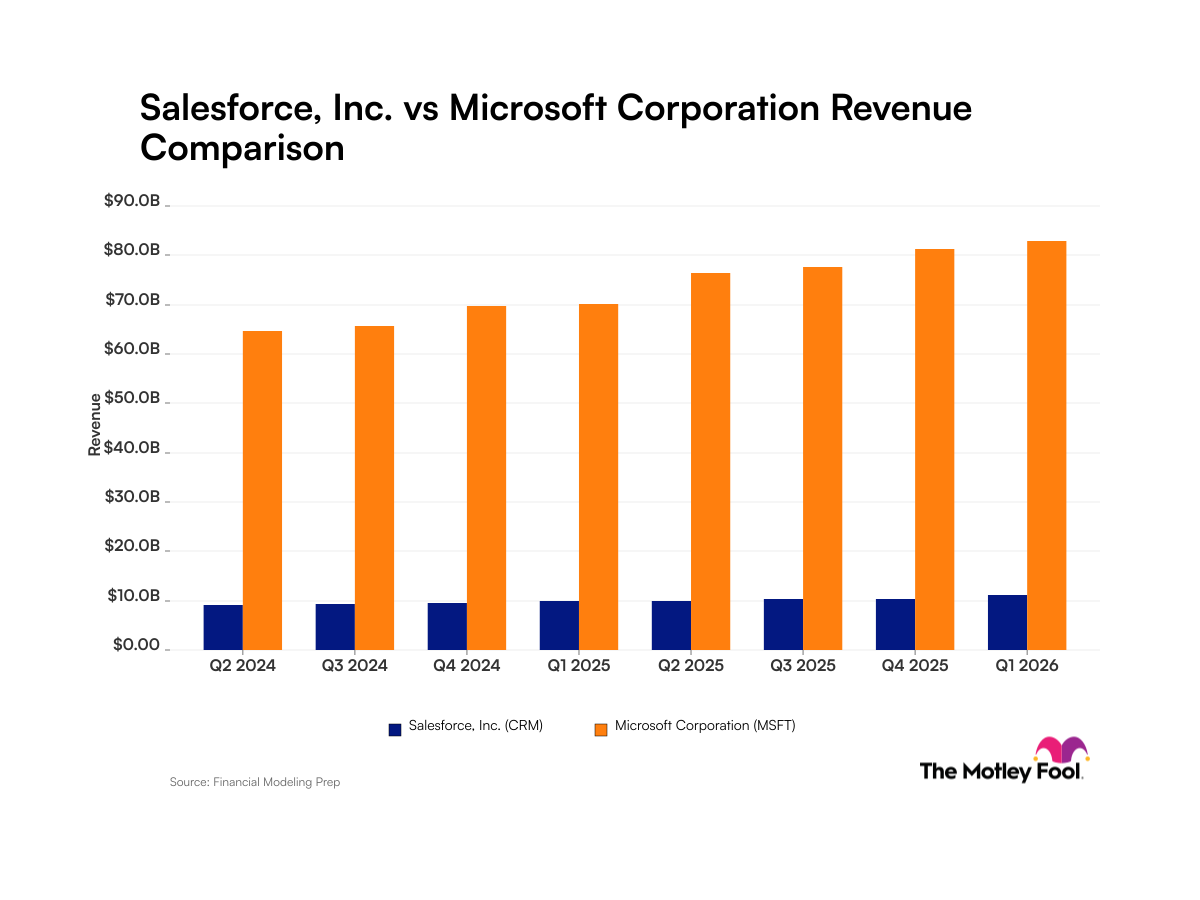

Salesforce and Microsoft Revenue Analysis

- Salesforce Revenue Growth: Salesforce reported a revenue of $41.5 billion for the fiscal year 2026, marking a 10% year-over-year increase, with projections for fiscal 2027 sales between $45.8 billion and $46.2 billion, indicating resilience against AI competition and boosting investor confidence.

- Microsoft Financial Performance: Microsoft achieved sales of $82.9 billion in its fiscal third quarter ending March 31, 2026, reflecting an 18% year-over-year growth, and despite concerns over capital expenditures, the strong growth suggests necessary infrastructure expansion to meet AI demand.

- Net Margin Comparison: Salesforce reported a net income margin of approximately 17% for the quarter ending January 31, 2026, while Microsoft achieved about 38% for the quarter ending March 31, 2026, highlighting a significant disparity in profitability between the two companies.

- Market Valuation Analysis: Salesforce's forward price-to-earnings ratio stands at 14, near a low point over the past year, indicating attractive stock valuation, while Microsoft's forward P/E ratio of 22, though not as cheap as Salesforce, is still lower than a year ago, suggesting it also presents investment value.

See More

Microsoft's AI Investments Drive Strong Growth

- Surge in Capital Expenditure: Microsoft plans to ramp up capital expenditures to $190 billion in the second half of 2026, which has pressured stock prices; however, the company's strong returns on invested capital indicate significant long-term growth potential.

- Azure Revenue Growth: Azure's revenue surged 40% in the most recent quarter, driven by both AI and non-AI services, demonstrating the company's sustained competitiveness in the cloud computing market.

- Strong Microsoft 365 Performance: Commercial software sales rose 19% year-over-year, while consumer version revenue increased by 33%, and Copilot user additions soared 250%, highlighting robust market demand and growth potential for the product.

- Analysts' Optimistic Outlook: Despite shares trading at about 25 times forward earnings expectations, analysts foresee a 30% increase in Microsoft's stock over the next year, reflecting confidence in its ongoing profitability and investment returns.

See More

OpenAI Expected to File for IPO Soon

- Upcoming IPO Filing: OpenAI is expected to file for its initial public offering (IPO) in the coming days or weeks, backed by Microsoft, indicating strong growth potential in the AI sector.

- Valuation Surge: The latest funding round has propelled OpenAI's valuation to $852 billion, with a monthly revenue of $2 billion, showcasing the success of its business model and robust market demand.

- Industry Impact: This news comes just two days after OpenAI CEO Sam Altman won a lawsuit against Tesla CEO Elon Musk, further solidifying its market position.

- Market Frenzy: With OpenAI and Anthropic preparing for IPOs, the investment frenzy in the AI sector is intensifying, attracting increased attention from investors.

See More

Microsoft's Maia Chips Enhance AI Infrastructure Amid Nvidia Dependency Reduction

- Chip Development Strategy: Microsoft is collaborating with Google and Amazon to develop Maia chips aimed at reducing dependence on Nvidia semiconductors, although discussions are still in early stages and may not lead to a final agreement.

- Maia 200 Chip Performance: Launched in January 2026, the Maia 200 chip utilizes TSMC's 3-nanometer process, with Microsoft claiming a 30% improvement in performance per dollar compared to existing systems, and higher memory bandwidth than Amazon and Google's counterparts.

- Collaboration with Anthropic: Anthropic is reportedly in talks with Microsoft to rent custom AI server chips to expand its computing capacity to meet rising demand for AI services, although discussions are still in preliminary stages.

- Market Sentiment Analysis: According to Stocktwits, retail sentiment for Microsoft has shifted from neutral to bullish, despite MSFT stock falling about 14% year-to-date, currently trading at $417, indicating potential market confidence in the Maia chips.

See More

Intuitive Surgical and Microsoft: Long-Term Investment Opportunities

- Financial Challenges for ISRG: Despite facing steep tariffs, Intuitive Surgical reported significant revenue and procedure volume growth in Q1, solidifying its market leadership in robotic-assisted surgery and indicating strong long-term growth potential.

- New Product Momentum: The latest da Vinci model accounted for 54% of the company's system placements in Q1, and its strong market adoption not only enhances technological advantages but also provides valuable feedback for future product improvements.

- Microsoft's AI Revenue Surge: Microsoft plans to invest $190 billion in AI-related capital expenditures by 2026, with its AI business already achieving an annual revenue run rate of $37 billion, reflecting a 123% year-over-year growth and showcasing the company's robust performance in the AI revolution.

- Cloud Computing Leadership: Microsoft's cloud backlog surged 99% year-over-year to $627 billion in the latest quarter, and combined with its AAA credit rating and a 153% dividend increase over the past decade, this further solidifies its appeal as a long-term investment.

See More

Market Outlook for Intuitive Surgical and Microsoft

- Solid Financial Performance: Despite facing steep tariffs, Intuitive Surgical achieved significant revenue and procedure volume growth in Q1, further solidifying its market leadership in robotic-assisted surgery, demonstrating the company's strong competitive position in the medical device sector.

- Sustained Technological Edge: The latest da Vinci 5 model accounted for nearly 54% of the company's installed systems in Q1, and this strong market acceptance not only enhances the company's technological advantage but also provides valuable feedback for future product improvements.

- AI-Driven Growth Potential: Microsoft plans to invest $190 billion by 2026 to support its AI-related strategies; despite concerns about its services being replaced by AI, the company has already achieved an annual revenue run rate of $37 billion in its AI business, reflecting a 123% year-over-year growth and showcasing its adaptability in technological transformation.

- Cloud Market Leadership: Microsoft's cloud backlog surged 99% year-over-year to $627 billion in the most recent quarter, and combined with its AAA credit rating and a 153% dividend increase over the past decade, this further underscores its attractiveness as a long-term investment.

See More

Salesforce and Microsoft Revenue Analysis

- Salesforce Revenue Growth: Salesforce reported a revenue of $41.5 billion for the fiscal year 2026, marking a 10% year-over-year increase, with projections for fiscal 2027 sales between $45.8 billion and $46.2 billion, indicating resilience against AI competition and boosting investor confidence.

- Microsoft Financial Performance: Microsoft achieved sales of $82.9 billion in its fiscal third quarter ending March 31, 2026, reflecting an 18% year-over-year growth, and despite concerns over capital expenditures, the strong growth suggests necessary infrastructure expansion to meet AI demand.

- Net Margin Comparison: Salesforce reported a net income margin of approximately 17% for the quarter ending January 31, 2026, while Microsoft achieved about 38% for the quarter ending March 31, 2026, highlighting a significant disparity in profitability between the two companies.

- Market Valuation Analysis: Salesforce's forward price-to-earnings ratio stands at 14, near a low point over the past year, indicating attractive stock valuation, while Microsoft's forward P/E ratio of 22, though not as cheap as Salesforce, is still lower than a year ago, suggesting it also presents investment value.

See More