SentinelOne Reports Revenue Growth Amid Competitive Pressures

SentinelOne Inc's stock fell 5% as it crossed below the 5-day SMA, reflecting investor concerns despite positive financial results.

In fiscal 2026, SentinelOne achieved a 22% revenue increase to $1 billion, demonstrating resilience and sustained customer demand despite competitive pressures from rivals. The company's free cash flow improved significantly to nearly $52 million, indicating a solid financial position that supports future investments. However, the stock's decline may be attributed to sector rotation, as broader market indices like the Nasdaq-100 and S&P 500 are experiencing gains.

The implications of SentinelOne's performance suggest that while the company is showing strong growth metrics, investor sentiment may be influenced by broader market trends and competitive dynamics in the cybersecurity sector.

Trade with 70% Backtested Accuracy

Analyst Views on S

About S

About the author

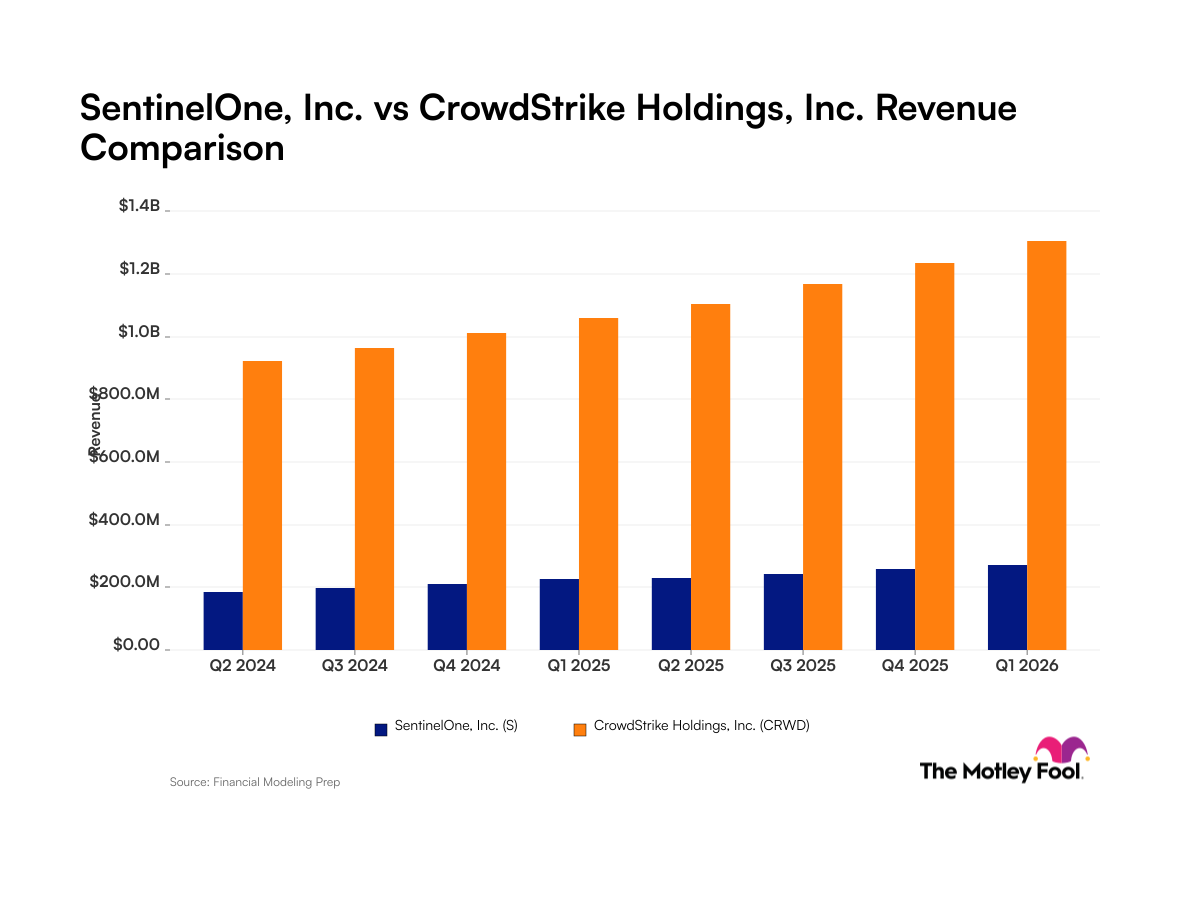

SentinelOne and CrowdStrike Report Steady Revenue Growth

- Revenue Comparison: SentinelOne reported quarterly revenue of $271.2 million for January 2026, reflecting a 20% year-over-year growth, while CrowdStrike's revenue reached $1.3 billion, marking a 23% increase, highlighting CrowdStrike's dominance in the cybersecurity market.

- Profitability Analysis: With a net income margin of approximately -41% for SentinelOne compared to about 3% for CrowdStrike, the latter demonstrates superior profitability, attracting greater investor interest.

- Market Reaction: Despite both companies experiencing stock price declines in Q1 2026 due to AI-related concerns, their ongoing revenue growth is restoring investor confidence, with CrowdStrike's stock nearing its 52-week high.

- Technological Application Outlook: As one of the first cybersecurity firms to integrate AI into its platform, SentinelOne is leveraging this technology to enhance its market competitiveness, although its growth rate lags behind CrowdStrike, indicating potential investment value.

Quantum Secure Encryption Corp. Launches QPA v2 Platform for Post-Quantum Migration

- Platform Launch: Quantum Secure Encryption Corp. officially launched QPA v2 on March 31, 2026, marking a significant advancement in supporting organizations transitioning to quantum-resilient security architectures, which is expected to enhance market competitiveness.

- Feature Innovation: QPA v2 transforms traditional manual assessment processes into a structured, data-driven workflow with real-time visibility into quantum readiness and migration progress through the introduction of a PQC Planning Wizard, AI-enhanced assessment modules, and a centralized executive dashboard, thereby improving enterprise security and compliance.

- Market Demand: With NIST standards and regulatory deadlines approaching, all custom and legacy applications must migrate by 2030, positioning QSE's QPA v2 platform to meet the urgent needs of enterprises in quantum security migration, presenting a substantial market opportunity.

- Global Expansion: QSE expanded its footprint to 13 countries in Q1 2026 and engaged in several international cybersecurity and post-quantum security conferences, enhancing interactions with global industry, government, and enterprise stakeholders, further solidifying its market position.

Quantum Secure Encryption Corp. Launches QPA v2 Platform for Post-Quantum Migration

- Platform Launch: Quantum Secure Encryption Corp. officially launched the QPA v2 platform on March 31, 2026, marking a significant advancement in supporting organizations transitioning to quantum-resilient architectures, which is expected to accelerate enterprise migration ahead of the 2030 deadline.

- Innovative Features: QPA v2 transforms traditional manual assessment processes by introducing a PQC Planning Wizard, AI-enhanced assessment modules, and a centralized dashboard, enabling organizations to monitor quantum readiness and risk levels in real-time, thereby improving migration efficiency.

- Market Demand: With the global post-quantum cryptography market projected to reach $17.69 billion by 2034 and annual cybercrime costs expected to hit $10.5 trillion in 2026, the launch of QPA v2 addresses the urgent need for practical migration tools in the market.

- Strategic Positioning: QSE's global footprint across 13 countries and its engagement with the public sector, combined with a refreshed long-term equity incentive structure, further solidify its market position in quantum security, ensuring a competitive edge ahead of impending regulatory deadlines.

SentinelOne: A Potential AI Security Stock

- Significant Revenue Growth: In fiscal 2026, SentinelOne achieved a 22% revenue increase to $1 billion, demonstrating resilience and sustained customer demand despite competitive pressures from profitable rivals.

- Improved Cash Flow: The company's free cash flow improved to nearly $52 million in fiscal 2026 from less than $7 million the previous year, indicating a solid financial position that supports future investments and innovation.

- Market Positioning Advantage: With a market cap of $5 billion, SentinelOne is significantly smaller than competitors Palo Alto and CrowdStrike, which have market caps of $149 billion and $119 billion, respectively, providing a lower entry cost and potential for growth with a price-to-sales ratio of 5.

- AI-Driven Innovative Platform: SentinelOne's Singularity platform is built around AI from the ground up, enabling rapid response to cyber threats, which may enhance its competitive edge as AI technology continues to evolve.

SentinelOne: Potential in AI Cybersecurity

- Financial Performance: In fiscal 2026, SentinelOne achieved a 22% revenue increase to $1 billion, despite posting a quarterly loss of $451 million; however, its positive free cash flow improved to $52 million, indicating resilience in a competitive cybersecurity market.

- Market Positioning: With its stock price down 80% from its 2021 peak and a market cap of $5 billion, significantly lower than competitors Palo Alto and CrowdStrike at $149 billion and $119 billion respectively, SentinelOne's undervaluation may present a compelling entry point for investors.

- Technological Edge: SentinelOne's Singularity platform, built around AI from the ground up, offers rapid response capabilities against cyber threats, particularly with its decentralized Purple AI system that effectively addresses various security challenges posed by AI-driven threats.

- Investment Outlook: Despite skepticism surrounding the cybersecurity sector, SentinelOne's ongoing revenue growth and a price-to-sales ratio of 5 limit downside risk, making a $3,000 investment potentially lucrative over time.

Analysis of Investment Opportunities in Artificial Intelligence

- Figma Competitive Edge: Figma's net dollar retention rate reached 136% in Q4 2025, indicating a 36% increase in spending from long-term customers, and despite competition from lower-cost AI tools, it is likely to maintain loyalty among professional designers, thereby solidifying its market position.

- SentinelOne Revenue Growth: SentinelOne's annual recurring revenue (ARR) grew by 22% in Q4 of fiscal 2026, with an 18% increase among customers spending over $100,000, demonstrating strong demand despite challenges to confidence in cybersecurity, reflecting the effectiveness of its early AI integration.

- Meta Platforms Investment: Meta Platforms plans to raise capital expenditures to between $125 billion and $145 billion in 2026, and although this announcement caused a stock drop, its Q1 revenue grew by 33% year-over-year to $56.3 billion, indicating strong financial capacity for AI investments.

- Market Valuation Opportunities: With Figma's price-to-sales (P/S) ratio dropping to 9 and SentinelOne's at 5, both companies' significant stock price declines present investors with opportunities to enter AI-related stocks at relatively low prices, potentially leading to substantial recoveries in the future.

SentinelOne and CrowdStrike Report Steady Revenue Growth

- Revenue Comparison: SentinelOne reported quarterly revenue of $271.2 million for January 2026, reflecting a 20% year-over-year growth, while CrowdStrike's revenue reached $1.3 billion, marking a 23% increase, highlighting CrowdStrike's dominance in the cybersecurity market.

- Profitability Analysis: With a net income margin of approximately -41% for SentinelOne compared to about 3% for CrowdStrike, the latter demonstrates superior profitability, attracting greater investor interest.

- Market Reaction: Despite both companies experiencing stock price declines in Q1 2026 due to AI-related concerns, their ongoing revenue growth is restoring investor confidence, with CrowdStrike's stock nearing its 52-week high.

- Technological Application Outlook: As one of the first cybersecurity firms to integrate AI into its platform, SentinelOne is leveraging this technology to enhance its market competitiveness, although its growth rate lags behind CrowdStrike, indicating potential investment value.

Quantum Secure Encryption Corp. Launches QPA v2 Platform for Post-Quantum Migration

- Platform Launch: Quantum Secure Encryption Corp. officially launched QPA v2 on March 31, 2026, marking a significant advancement in supporting organizations transitioning to quantum-resilient security architectures, which is expected to enhance market competitiveness.

- Feature Innovation: QPA v2 transforms traditional manual assessment processes into a structured, data-driven workflow with real-time visibility into quantum readiness and migration progress through the introduction of a PQC Planning Wizard, AI-enhanced assessment modules, and a centralized executive dashboard, thereby improving enterprise security and compliance.

- Market Demand: With NIST standards and regulatory deadlines approaching, all custom and legacy applications must migrate by 2030, positioning QSE's QPA v2 platform to meet the urgent needs of enterprises in quantum security migration, presenting a substantial market opportunity.

- Global Expansion: QSE expanded its footprint to 13 countries in Q1 2026 and engaged in several international cybersecurity and post-quantum security conferences, enhancing interactions with global industry, government, and enterprise stakeholders, further solidifying its market position.

Quantum Secure Encryption Corp. Launches QPA v2 Platform for Post-Quantum Migration

- Platform Launch: Quantum Secure Encryption Corp. officially launched the QPA v2 platform on March 31, 2026, marking a significant advancement in supporting organizations transitioning to quantum-resilient architectures, which is expected to accelerate enterprise migration ahead of the 2030 deadline.

- Innovative Features: QPA v2 transforms traditional manual assessment processes by introducing a PQC Planning Wizard, AI-enhanced assessment modules, and a centralized dashboard, enabling organizations to monitor quantum readiness and risk levels in real-time, thereby improving migration efficiency.

- Market Demand: With the global post-quantum cryptography market projected to reach $17.69 billion by 2034 and annual cybercrime costs expected to hit $10.5 trillion in 2026, the launch of QPA v2 addresses the urgent need for practical migration tools in the market.

- Strategic Positioning: QSE's global footprint across 13 countries and its engagement with the public sector, combined with a refreshed long-term equity incentive structure, further solidify its market position in quantum security, ensuring a competitive edge ahead of impending regulatory deadlines.

SentinelOne: A Potential AI Security Stock

- Significant Revenue Growth: In fiscal 2026, SentinelOne achieved a 22% revenue increase to $1 billion, demonstrating resilience and sustained customer demand despite competitive pressures from profitable rivals.

- Improved Cash Flow: The company's free cash flow improved to nearly $52 million in fiscal 2026 from less than $7 million the previous year, indicating a solid financial position that supports future investments and innovation.

- Market Positioning Advantage: With a market cap of $5 billion, SentinelOne is significantly smaller than competitors Palo Alto and CrowdStrike, which have market caps of $149 billion and $119 billion, respectively, providing a lower entry cost and potential for growth with a price-to-sales ratio of 5.

- AI-Driven Innovative Platform: SentinelOne's Singularity platform is built around AI from the ground up, enabling rapid response to cyber threats, which may enhance its competitive edge as AI technology continues to evolve.

SentinelOne: Potential in AI Cybersecurity

- Financial Performance: In fiscal 2026, SentinelOne achieved a 22% revenue increase to $1 billion, despite posting a quarterly loss of $451 million; however, its positive free cash flow improved to $52 million, indicating resilience in a competitive cybersecurity market.

- Market Positioning: With its stock price down 80% from its 2021 peak and a market cap of $5 billion, significantly lower than competitors Palo Alto and CrowdStrike at $149 billion and $119 billion respectively, SentinelOne's undervaluation may present a compelling entry point for investors.

- Technological Edge: SentinelOne's Singularity platform, built around AI from the ground up, offers rapid response capabilities against cyber threats, particularly with its decentralized Purple AI system that effectively addresses various security challenges posed by AI-driven threats.

- Investment Outlook: Despite skepticism surrounding the cybersecurity sector, SentinelOne's ongoing revenue growth and a price-to-sales ratio of 5 limit downside risk, making a $3,000 investment potentially lucrative over time.

Analysis of Investment Opportunities in Artificial Intelligence

- Figma Competitive Edge: Figma's net dollar retention rate reached 136% in Q4 2025, indicating a 36% increase in spending from long-term customers, and despite competition from lower-cost AI tools, it is likely to maintain loyalty among professional designers, thereby solidifying its market position.

- SentinelOne Revenue Growth: SentinelOne's annual recurring revenue (ARR) grew by 22% in Q4 of fiscal 2026, with an 18% increase among customers spending over $100,000, demonstrating strong demand despite challenges to confidence in cybersecurity, reflecting the effectiveness of its early AI integration.

- Meta Platforms Investment: Meta Platforms plans to raise capital expenditures to between $125 billion and $145 billion in 2026, and although this announcement caused a stock drop, its Q1 revenue grew by 33% year-over-year to $56.3 billion, indicating strong financial capacity for AI investments.

- Market Valuation Opportunities: With Figma's price-to-sales (P/S) ratio dropping to 9 and SentinelOne's at 5, both companies' significant stock price declines present investors with opportunities to enter AI-related stocks at relatively low prices, potentially leading to substantial recoveries in the future.