Rivian Faces Mixed Outlook Amid EV Market Slowdown

Rivian Automotive Inc's stock has declined 4.57%, hitting a 20-day low, as the electric vehicle market faces significant challenges.

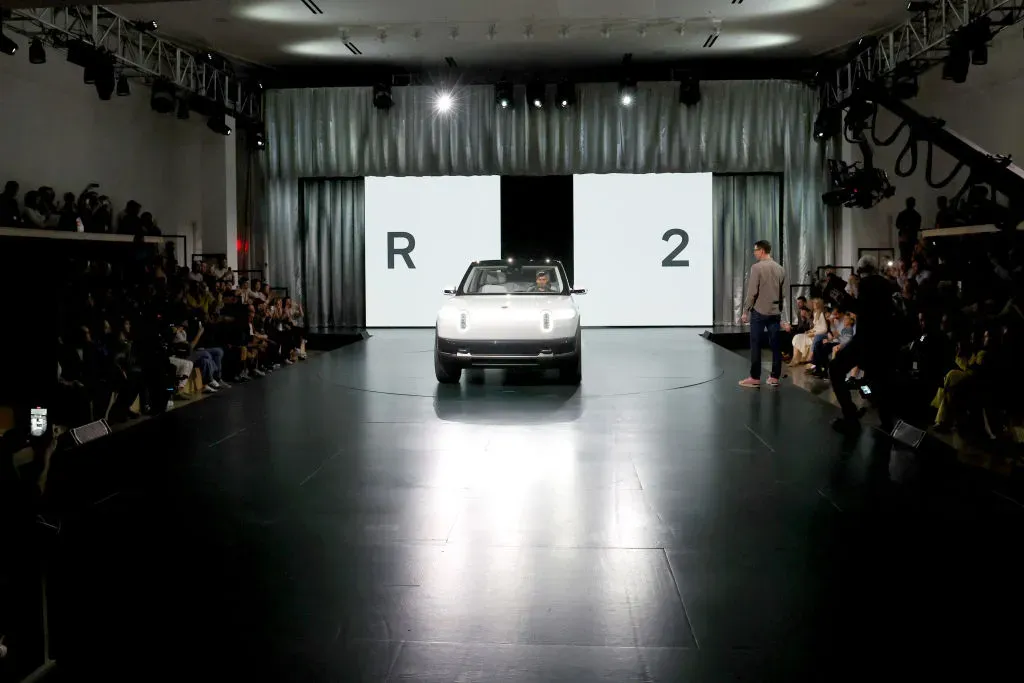

The company is experiencing a mixed outlook amid a 27% year-over-year drop in U.S. EV sales in Q1, leading to a 30% decline in Rivian's stock year-to-date. Despite reporting a revenue increase of 11% year-over-year to $1.4 billion and a 20% rise in deliveries, concerns about profitability persist. Rivian's recent launch of the R2 mass-market model and plans to expand production capacity at its Georgia plant may provide some relief, but the overall market sentiment remains cautious.

The implications of Rivian's current situation highlight the need for strategic adjustments in response to market conditions. The company's efforts to diversify its offerings and improve production efficiency will be crucial in navigating the current downturn in the EV sector.

Trade with 70% Backtested Accuracy

Analyst Views on RIVN

About RIVN

About the author

Rivian R2 Production Ramps Up as Pritzker Calls It the Best EV Maker

- R2 Production Update: Rivian has ramped up R2 production recently after earlier setbacks due to tornado damage, with deliveries expected to start this Spring, marking a significant step in the company's expansion in the EV market.

- Pritzker's Endorsement: Illinois Governor Pritzker praised Rivian as the 'best EV maker in the world,' stating that the R2, priced below $50,000, will democratize electric vehicle access for the middle class, highlighting its market significance.

- Investment and Employment: Rivian's $1.5 billion investment to expand R2 production at the former Mitsubishi plant has created thousands of jobs and plans for a nearby supplier park, further boosting local economic development.

- Delivery Expectations: Rivian now anticipates delivering 62,000 to 67,000 vehicles in 2026, a significant increase from 42,247 in 2025, although R2 deliveries will be 'back-half weighted,' which may impact the company's future market performance.

SpaceX Aims for Record $75 Billion IPO on Nasdaq

- Record IPO Size: SpaceX's planned Nasdaq debut aims to raise approximately $75 billion, more than triple Alibaba's $22 billion IPO in 2014, marking a significant revival for the U.S. IPO market.

- Market Impact: This IPO is expected to inject new life into a market that has seen muted activity since late 2021, with investors hoping SpaceX's success will encourage other tech firms like OpenAI and Anthropic to go public, thus revitalizing the overall market.

- Increased Industry Competition: With SpaceX's unprecedented fundraising, other major tech companies may reassess their IPO timing and funding strategies, particularly in the AI and space exploration sectors, leading to intensified competition.

- Boosted Investor Confidence: A successful SpaceX IPO will not only enhance investor confidence in high-risk tech stocks but may also draw attention to other potential high-value companies, further stimulating capital flow within the tech industry.

SpaceX Poised to Set Record for Largest IPO in History

- Record-Setting IPO: SpaceX is set to debut on Nasdaq with an anticipated raise of over $75 billion, which would be more than triple the $22 billion raised by Alibaba in 2014, highlighting the company's immense potential and market impact.

- Market Revival Catalyst: Amidst muted IPO activity since late 2021, SpaceX's listing is seen as a crucial factor in restoring investor confidence, potentially activating other tech companies' plans to go public, particularly in the booming AI sector.

- Industry Influence: As a leading rocket manufacturer, SpaceX's successful IPO will not only elevate its market valuation but may also ignite an investment surge in the aerospace industry, attracting more capital into related technologies and innovations.

- Future Outlook: SpaceX's IPO is poised to become the largest initial public offering in Wall Street history, expected to reshape investor perceptions of high-tech companies and potentially trigger a series of subsequent market activities that further drive growth in tech stocks.

Lucid Group Faces Production and Funding Challenges

- Production Issues: Lucid Group's new Gravity SUV has faced slow production acceleration, with a rear-seat defect leading to a recall that significantly impacted February deliveries, forcing the company to suspend its full-year production guidance, highlighting its vulnerabilities in the EV market.

- Funding Risks: The Saudi Public Investment Fund (PIF) has invested approximately $9.5 billion into Lucid, but its recent decision to halt funding for LIV Golf indicates that PIF's financial support is not endless, raising concerns for investors about the potential loss of this critical backer.

- Rising Competition: Rivian Automotive has made significant strides in profitability compared to Lucid, achieving its first quarterly gross profit in Q4 2024, showcasing its success in cost management and software revenue, which intensifies market pressure on Lucid.

- Decreasing Investment Appeal: While Lucid remains an intriguing investment in the EV sector, ongoing production challenges, funding uncertainties, and slow progress towards profitability suggest that it may not be the right time for investors to consider Lucid as a viable investment opportunity.

Lucid Suspends Production Guidance Amid Funding Challenges

- Production Issues Intensify: Lucid has suspended its full-year production guidance due to slower-than-expected production of the newly launched Gravity SUV and a recall caused by a rear-seat defect, highlighting ongoing challenges in production efficiency that have led to a widening net loss in Q1.

- Funding Uncertainty: The Saudi Public Investment Fund (PIF) has invested approximately $9.5 billion into Lucid, but its recent decision to halt funding for LIV Golf suggests that PIF's financial support is not limitless, raising concerns among investors about potential funding withdrawals.

- Competitor Performance: Rivian has made significant strides in gross profitability, achieving its first quarterly gross profit in Q4 2024, which underscores its advantages in cost management and profitability, thereby increasing competitive pressure on Lucid.

- Investor Confidence Shaken: With multiple challenges related to production, funding, and profitability, Lucid's advanced EV technology may not be enough to instill confidence in investors, especially as it fails to make the list of top investment stocks in the current market environment.

Rivian's Transition Potential Attracts Investors

- Market Valuation Analysis: Rivian currently has a market cap of approximately $18.5 billion, with projected revenues of about $7 billion in 2026, resulting in a price-to-sales ratio of only 2.5 times, indicating a relatively low valuation that may attract investor interest in its growth potential.

- Cash Reserves and Partnerships: The company holds $4.8 billion in cash and short-term investments, alongside a partnership with Volkswagen worth up to $5.8 billion aimed at developing next-generation software-defined vehicle architecture, enhancing its competitive position in the market.

- R2 Platform Outlook: The upcoming R2 platform is expected to significantly expand Rivian's addressable market, with management forecasting deliveries of 62,000 to 67,000 vehicles in 2026, while analysts anticipate over 22,000 R2 deliveries this year, which could drive up the company's valuation if successful.

- Software Revenue Growth: In Q1 2026, Rivian's software and services segment generated $473 million in revenue, a 49% year-over-year increase, with software gross profit reaching $181 million, indicating that growth in the software sector could enhance the overall valuation beyond traditional automotive metrics.

Rivian R2 Production Ramps Up as Pritzker Calls It the Best EV Maker

- R2 Production Update: Rivian has ramped up R2 production recently after earlier setbacks due to tornado damage, with deliveries expected to start this Spring, marking a significant step in the company's expansion in the EV market.

- Pritzker's Endorsement: Illinois Governor Pritzker praised Rivian as the 'best EV maker in the world,' stating that the R2, priced below $50,000, will democratize electric vehicle access for the middle class, highlighting its market significance.

- Investment and Employment: Rivian's $1.5 billion investment to expand R2 production at the former Mitsubishi plant has created thousands of jobs and plans for a nearby supplier park, further boosting local economic development.

- Delivery Expectations: Rivian now anticipates delivering 62,000 to 67,000 vehicles in 2026, a significant increase from 42,247 in 2025, although R2 deliveries will be 'back-half weighted,' which may impact the company's future market performance.

SpaceX Aims for Record $75 Billion IPO on Nasdaq

- Record IPO Size: SpaceX's planned Nasdaq debut aims to raise approximately $75 billion, more than triple Alibaba's $22 billion IPO in 2014, marking a significant revival for the U.S. IPO market.

- Market Impact: This IPO is expected to inject new life into a market that has seen muted activity since late 2021, with investors hoping SpaceX's success will encourage other tech firms like OpenAI and Anthropic to go public, thus revitalizing the overall market.

- Increased Industry Competition: With SpaceX's unprecedented fundraising, other major tech companies may reassess their IPO timing and funding strategies, particularly in the AI and space exploration sectors, leading to intensified competition.

- Boosted Investor Confidence: A successful SpaceX IPO will not only enhance investor confidence in high-risk tech stocks but may also draw attention to other potential high-value companies, further stimulating capital flow within the tech industry.

SpaceX Poised to Set Record for Largest IPO in History

- Record-Setting IPO: SpaceX is set to debut on Nasdaq with an anticipated raise of over $75 billion, which would be more than triple the $22 billion raised by Alibaba in 2014, highlighting the company's immense potential and market impact.

- Market Revival Catalyst: Amidst muted IPO activity since late 2021, SpaceX's listing is seen as a crucial factor in restoring investor confidence, potentially activating other tech companies' plans to go public, particularly in the booming AI sector.

- Industry Influence: As a leading rocket manufacturer, SpaceX's successful IPO will not only elevate its market valuation but may also ignite an investment surge in the aerospace industry, attracting more capital into related technologies and innovations.

- Future Outlook: SpaceX's IPO is poised to become the largest initial public offering in Wall Street history, expected to reshape investor perceptions of high-tech companies and potentially trigger a series of subsequent market activities that further drive growth in tech stocks.

Lucid Group Faces Production and Funding Challenges

- Production Issues: Lucid Group's new Gravity SUV has faced slow production acceleration, with a rear-seat defect leading to a recall that significantly impacted February deliveries, forcing the company to suspend its full-year production guidance, highlighting its vulnerabilities in the EV market.

- Funding Risks: The Saudi Public Investment Fund (PIF) has invested approximately $9.5 billion into Lucid, but its recent decision to halt funding for LIV Golf indicates that PIF's financial support is not endless, raising concerns for investors about the potential loss of this critical backer.

- Rising Competition: Rivian Automotive has made significant strides in profitability compared to Lucid, achieving its first quarterly gross profit in Q4 2024, showcasing its success in cost management and software revenue, which intensifies market pressure on Lucid.

- Decreasing Investment Appeal: While Lucid remains an intriguing investment in the EV sector, ongoing production challenges, funding uncertainties, and slow progress towards profitability suggest that it may not be the right time for investors to consider Lucid as a viable investment opportunity.

Lucid Suspends Production Guidance Amid Funding Challenges

- Production Issues Intensify: Lucid has suspended its full-year production guidance due to slower-than-expected production of the newly launched Gravity SUV and a recall caused by a rear-seat defect, highlighting ongoing challenges in production efficiency that have led to a widening net loss in Q1.

- Funding Uncertainty: The Saudi Public Investment Fund (PIF) has invested approximately $9.5 billion into Lucid, but its recent decision to halt funding for LIV Golf suggests that PIF's financial support is not limitless, raising concerns among investors about potential funding withdrawals.

- Competitor Performance: Rivian has made significant strides in gross profitability, achieving its first quarterly gross profit in Q4 2024, which underscores its advantages in cost management and profitability, thereby increasing competitive pressure on Lucid.

- Investor Confidence Shaken: With multiple challenges related to production, funding, and profitability, Lucid's advanced EV technology may not be enough to instill confidence in investors, especially as it fails to make the list of top investment stocks in the current market environment.

Rivian's Transition Potential Attracts Investors

- Market Valuation Analysis: Rivian currently has a market cap of approximately $18.5 billion, with projected revenues of about $7 billion in 2026, resulting in a price-to-sales ratio of only 2.5 times, indicating a relatively low valuation that may attract investor interest in its growth potential.

- Cash Reserves and Partnerships: The company holds $4.8 billion in cash and short-term investments, alongside a partnership with Volkswagen worth up to $5.8 billion aimed at developing next-generation software-defined vehicle architecture, enhancing its competitive position in the market.

- R2 Platform Outlook: The upcoming R2 platform is expected to significantly expand Rivian's addressable market, with management forecasting deliveries of 62,000 to 67,000 vehicles in 2026, while analysts anticipate over 22,000 R2 deliveries this year, which could drive up the company's valuation if successful.

- Software Revenue Growth: In Q1 2026, Rivian's software and services segment generated $473 million in revenue, a 49% year-over-year increase, with software gross profit reaching $181 million, indicating that growth in the software sector could enhance the overall valuation beyond traditional automotive metrics.