Lucid Group's Q1 Earnings Preview Highlights Challenges and Opportunities

Lucid Group Inc. saw its stock rise by 6.73% as it crossed above the 5-day SMA, reflecting a positive market reaction despite ongoing challenges.

The company pre-announced Q1 revenue between $280 million and $284 million, significantly below Wall Street's expectation of $433.8 million, indicating severe financial challenges ahead. However, analysts believe that the upcoming earnings call will clarify these issues, potentially leading to a stock rebound and renewed investor interest in Lucid. The company has also resolved delivery issues related to seat quality, reaffirming its production guidance of 25,000 to 27,000 vehicles for 2023, which could improve revenue in the coming months.

Despite the challenges, the resolution of quality issues and the potential for a rebound in stock price suggest that investors may find opportunities in Lucid Group as it navigates its operational hurdles.

Trade with 70% Backtested Accuracy

Analyst Views on LCID

About LCID

About the author

Shareholder Class Action Lawsuit Reminder

- Calix Shareholder Lawsuit: A class action lawsuit against Calix, Inc. alleges that the company failed to disclose material facts between January 28 and April 21, 2026, leading to investor losses; affected investors must apply to be lead plaintiffs by July 27, 2026, to protect their rights.

- AeroVironment Shareholder Lawsuit: The class action lawsuit against AeroVironment, Inc. claims that misleading statements made between June 25, 2025, and March 10, 2026, impacted investor decisions, and affected investors should contact legal counsel by July 27, 2026, for support.

- Lucid Group Shareholder Lawsuit: Lucid Group, Inc. faces a class action lawsuit alleging that it failed to disclose its manufacturing and delivery capabilities between February 25 and April 13, 2026, resulting in investor losses; investors must apply to be lead plaintiffs by July 28, 2026.

- Law Firm Background: Holzer & Holzer, LLC, a top-rated securities litigation firm, has been dedicated to representing shareholders since 2000, recovering hundreds of millions for victims of corporate misconduct, highlighting its expertise and success in securities litigation.

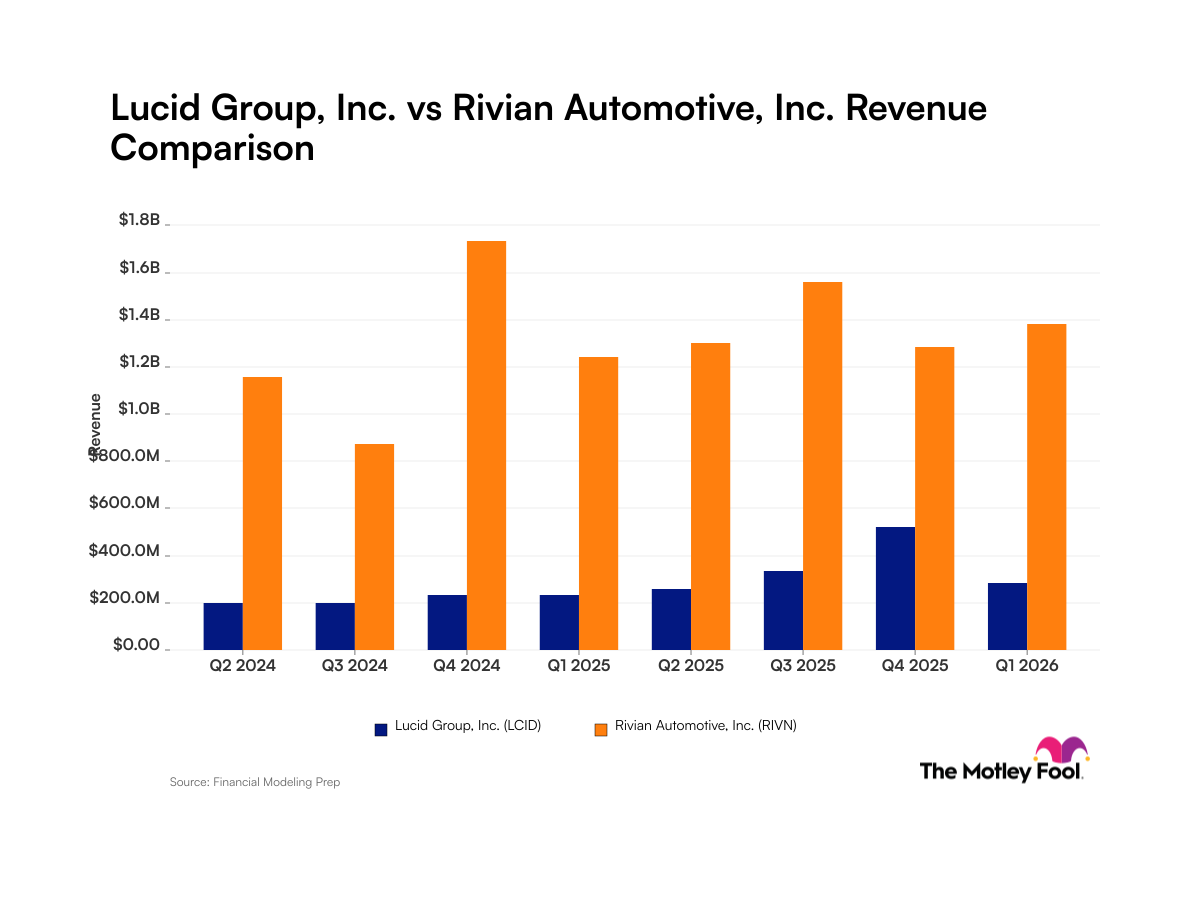

Lucid and Rivian: A Comparative Analysis in the EV Market

- Leadership Transition: Lucid recently announced a leadership change and secured approximately $1.05 billion through public offerings and private investments, despite reporting a -364% net income margin for Q1 2026, indicating ongoing challenges in execution and production scaling.

- Revenue Fluctuations: Lucid reported $200.6 million in revenue for Q2 2024, while Rivian achieved $1.2 billion in the same period, highlighting Rivian's strong performance and larger market share in the electric vehicle sector.

- Production Goals: Rivian expects to deliver between 62,000 and 67,000 EVs in 2026, reflecting nearly 50% growth over 2025, whereas Lucid continues to face persistent difficulties in production and delivery, impacting its revenue stability.

- Strategic Partnerships: Rivian's joint venture with Volkswagen provides billions in funding, while its agreement with Uber for 50,000 robotaxis further solidifies its market position, showcasing its competitive advantage in the electric vehicle landscape.

Lucid Group Faces Class Action Lawsuit Amid Significant Financial Disclosures

- Lawsuit Background: Robbins LLP has initiated a class action lawsuit against Lucid Group, Inc. on behalf of all investors who purchased its securities between February 25 and April 13, 2026, highlighting serious concerns regarding the company's transparency to its shareholders.

- Financial Missteps: Lucid's preliminary Q1 2026 financial results, released on April 14, revealed revenues of only $280 million to $284 million, significantly below the consensus estimate of $433.8 million, alongside operational losses reaching $1.005 billion, indicating severe financial distress.

- Stock Price Reaction: Following the financial disclosures and plans for a $1.05 billion capital raise, Lucid's stock price fell by $0.44, or 4.76%, closing at $8.80 per share, reflecting market pessimism regarding the company's future outlook.

- Investor Action: Shareholders must submit their papers by July 28, 2026, to serve as lead plaintiffs in the class action, underscoring the importance of corporate governance and transparency, which may influence future investment decisions.

Lucid Group Faces Class Action Lawsuit Over Securities Violations

- Lawsuit Background: Bronstein, Gewirtz & Grossman, LLC has filed a class action lawsuit against Lucid Group, alleging that from February 25 to April 13, 2026, the company failed to disclose a supplier quality issue that significantly disrupted deliveries of the Lucid Gravity, which materially impacted the company's business and financial results.

- Legal Basis: The lawsuit claims that the defendants overstated Lucid's manufacturing and delivery capabilities throughout the class period, resulting in public statements that were materially false and misleading, causing investors to suffer losses.

- Investor Action: Affected investors are encouraged to apply to be lead plaintiffs by July 28, 2026, to share in any potential recovery from the lawsuit, with no requirement to serve as lead plaintiff to participate in the compensation.

- Law Firm Advantage: Bronstein, Gewirtz & Grossman, LLC is a nationally recognized firm specializing in investor rights and securities fraud class actions, having recovered hundreds of millions for investors nationwide, emphasizing its expertise in restoring investor capital and ensuring corporate accountability.

Lucid Group Faces Class Action Lawsuit from Shareholders

- Class Action Initiated: Bernstein Liebhard LLP announces a class action lawsuit on behalf of investors who purchased Lucid Group securities between February 25 and April 13, 2026, alleging that the company made materially false and misleading statements that inflated stock prices during this period.

- Lawsuit Details Revealed: The lawsuit claims that Lucid Group misrepresented its business operations, growth prospects, and financial stability, resulting in significant investor losses when the truth was disclosed, highlighting serious issues in corporate governance and transparency.

- Investor Action Recommended: Investors are encouraged to promptly submit forms to participate in the lawsuit, and those wishing to serve as lead plaintiffs must file by July 28, 2026, indicating the company's commitment to shareholder rights.

- Law Firm Background: Bernstein Liebhard LLP has recovered over $3.5 billion for clients since 1993 and has extensive experience in handling class actions, demonstrating its strong capability and reputation in protecting investor interests.

Lucid Group Faces Shareholder Class Action Lawsuit

- Lawsuit Background: Lucid Group, Inc. (NASDAQ: LCID) is facing a shareholder class action lawsuit alleging that it made false and misleading statements while failing to disclose material adverse facts regarding its business, operations, and prospects.

- Delivery Issues: The lawsuit claims that a supplier quality issue significantly disrupted deliveries of the Lucid Gravity, which not only impacted the company's operations but also had a material negative effect on its financial results.

- Financial Impact: As a result of these issues, the purported enhancements to Lucid's manufacturing and delivery capabilities were overstated, leading to losses for investors who purchased shares between February 25, 2026, and April 13, 2026, prompting plaintiffs to encourage affected investors to seek legal counsel.

- Legal Consultation: Holzer & Holzer, LLC, a law firm dedicated to shareholder rights, urges affected investors to apply to be lead plaintiffs in the case by July 28, 2026, to secure better legal representation in the lawsuit.

Shareholder Class Action Lawsuit Reminder

- Calix Shareholder Lawsuit: A class action lawsuit against Calix, Inc. alleges that the company failed to disclose material facts between January 28 and April 21, 2026, leading to investor losses; affected investors must apply to be lead plaintiffs by July 27, 2026, to protect their rights.

- AeroVironment Shareholder Lawsuit: The class action lawsuit against AeroVironment, Inc. claims that misleading statements made between June 25, 2025, and March 10, 2026, impacted investor decisions, and affected investors should contact legal counsel by July 27, 2026, for support.

- Lucid Group Shareholder Lawsuit: Lucid Group, Inc. faces a class action lawsuit alleging that it failed to disclose its manufacturing and delivery capabilities between February 25 and April 13, 2026, resulting in investor losses; investors must apply to be lead plaintiffs by July 28, 2026.

- Law Firm Background: Holzer & Holzer, LLC, a top-rated securities litigation firm, has been dedicated to representing shareholders since 2000, recovering hundreds of millions for victims of corporate misconduct, highlighting its expertise and success in securities litigation.

Lucid and Rivian: A Comparative Analysis in the EV Market

- Leadership Transition: Lucid recently announced a leadership change and secured approximately $1.05 billion through public offerings and private investments, despite reporting a -364% net income margin for Q1 2026, indicating ongoing challenges in execution and production scaling.

- Revenue Fluctuations: Lucid reported $200.6 million in revenue for Q2 2024, while Rivian achieved $1.2 billion in the same period, highlighting Rivian's strong performance and larger market share in the electric vehicle sector.

- Production Goals: Rivian expects to deliver between 62,000 and 67,000 EVs in 2026, reflecting nearly 50% growth over 2025, whereas Lucid continues to face persistent difficulties in production and delivery, impacting its revenue stability.

- Strategic Partnerships: Rivian's joint venture with Volkswagen provides billions in funding, while its agreement with Uber for 50,000 robotaxis further solidifies its market position, showcasing its competitive advantage in the electric vehicle landscape.

Lucid Group Faces Class Action Lawsuit Amid Significant Financial Disclosures

- Lawsuit Background: Robbins LLP has initiated a class action lawsuit against Lucid Group, Inc. on behalf of all investors who purchased its securities between February 25 and April 13, 2026, highlighting serious concerns regarding the company's transparency to its shareholders.

- Financial Missteps: Lucid's preliminary Q1 2026 financial results, released on April 14, revealed revenues of only $280 million to $284 million, significantly below the consensus estimate of $433.8 million, alongside operational losses reaching $1.005 billion, indicating severe financial distress.

- Stock Price Reaction: Following the financial disclosures and plans for a $1.05 billion capital raise, Lucid's stock price fell by $0.44, or 4.76%, closing at $8.80 per share, reflecting market pessimism regarding the company's future outlook.

- Investor Action: Shareholders must submit their papers by July 28, 2026, to serve as lead plaintiffs in the class action, underscoring the importance of corporate governance and transparency, which may influence future investment decisions.

Lucid Group Faces Class Action Lawsuit Over Securities Violations

- Lawsuit Background: Bronstein, Gewirtz & Grossman, LLC has filed a class action lawsuit against Lucid Group, alleging that from February 25 to April 13, 2026, the company failed to disclose a supplier quality issue that significantly disrupted deliveries of the Lucid Gravity, which materially impacted the company's business and financial results.

- Legal Basis: The lawsuit claims that the defendants overstated Lucid's manufacturing and delivery capabilities throughout the class period, resulting in public statements that were materially false and misleading, causing investors to suffer losses.

- Investor Action: Affected investors are encouraged to apply to be lead plaintiffs by July 28, 2026, to share in any potential recovery from the lawsuit, with no requirement to serve as lead plaintiff to participate in the compensation.

- Law Firm Advantage: Bronstein, Gewirtz & Grossman, LLC is a nationally recognized firm specializing in investor rights and securities fraud class actions, having recovered hundreds of millions for investors nationwide, emphasizing its expertise in restoring investor capital and ensuring corporate accountability.

Lucid Group Faces Class Action Lawsuit from Shareholders

- Class Action Initiated: Bernstein Liebhard LLP announces a class action lawsuit on behalf of investors who purchased Lucid Group securities between February 25 and April 13, 2026, alleging that the company made materially false and misleading statements that inflated stock prices during this period.

- Lawsuit Details Revealed: The lawsuit claims that Lucid Group misrepresented its business operations, growth prospects, and financial stability, resulting in significant investor losses when the truth was disclosed, highlighting serious issues in corporate governance and transparency.

- Investor Action Recommended: Investors are encouraged to promptly submit forms to participate in the lawsuit, and those wishing to serve as lead plaintiffs must file by July 28, 2026, indicating the company's commitment to shareholder rights.

- Law Firm Background: Bernstein Liebhard LLP has recovered over $3.5 billion for clients since 1993 and has extensive experience in handling class actions, demonstrating its strong capability and reputation in protecting investor interests.

Lucid Group Faces Shareholder Class Action Lawsuit

- Lawsuit Background: Lucid Group, Inc. (NASDAQ: LCID) is facing a shareholder class action lawsuit alleging that it made false and misleading statements while failing to disclose material adverse facts regarding its business, operations, and prospects.

- Delivery Issues: The lawsuit claims that a supplier quality issue significantly disrupted deliveries of the Lucid Gravity, which not only impacted the company's operations but also had a material negative effect on its financial results.

- Financial Impact: As a result of these issues, the purported enhancements to Lucid's manufacturing and delivery capabilities were overstated, leading to losses for investors who purchased shares between February 25, 2026, and April 13, 2026, prompting plaintiffs to encourage affected investors to seek legal counsel.

- Legal Consultation: Holzer & Holzer, LLC, a law firm dedicated to shareholder rights, urges affected investors to apply to be lead plaintiffs in the case by July 28, 2026, to secure better legal representation in the lawsuit.