Gulfport Energy CEO Resigns, Impacting Investor Confidence

Gulfport Energy Corp's stock fell 5.50% as it hit a 5-day low amid the resignation of CEO John Reinhart, which has raised concerns about the company's leadership stability.

The immediate resignation of CEO John Reinhart, who also left the board, indicates a significant governance shift that may affect investor confidence. The company has formed a committee to select a new CEO, demonstrating swift action to maintain operational stability. Despite these changes, Gulfport is projected to generate over $500 million in free cash flow by 2026, indicating strong financial health that may provide a solid foundation for the incoming CEO.

This leadership change could lead to uncertainty in the company's strategic direction, but the strong financial outlook may help mitigate some investor concerns.

Trade with 70% Backtested Accuracy

Analyst Views on GPOR

About GPOR

About the author

Comparative Analysis of Gulfport and Viper Energy

- Gulfport Energy Growth: Gulfport Energy reported approximately $1.3 billion in revenue for FY 2025, reflecting a 43% year-over-year increase, with net income nearing $427.8 million and a net margin of about 32.3%, indicating strong performance in the natural gas and oil markets.

- Viper Energy Model: Viper Energy achieved nearly $1.4 billion in revenue for FY 2025, a 57% increase year-over-year, but reported a net loss of approximately $69 million, resulting in a negative net margin of -5.1%, highlighting challenges in its reliance on partner production.

- Financial Health Comparison: As of December 2025, Gulfport's debt-to-equity ratio stood at approximately 0.4 with a current ratio of about 0.7, while Viper's debt-to-equity ratio was around 0.5 with a current ratio of 3.7, showcasing significant differences in their financial structures.

- Future Outlook: Gulfport is expected to see a 20% increase in earnings per share to around $26 in 2026, and while neither company pays dividends, Gulfport's profitability and value appeal make it more attractive to investors.

Investment Comparison: Gulfport vs. Viper Energy

- Gulfport Energy Growth: Gulfport Energy reported approximately $1.3 billion in revenue for FY 2025, reflecting a 43% year-over-year increase, with a net income of nearly $427.8 million and a net margin of about 32.3%, showcasing its strong performance in the natural gas and oil markets.

- Viper Energy Challenges: Despite Viper Energy achieving nearly $1.4 billion in revenue for FY 2025, a 57% increase, it reported a net loss of approximately $69 million, resulting in a negative net margin of -5.1%, indicating risks associated with its reliance on partner production activities.

- Financial Health Comparison: As of December 2025, Gulfport's debt-to-equity ratio stood at approximately 0.4, with a current ratio of about 0.7, indicating financial stability; in contrast, Viper's debt-to-equity ratio was 0.5, with a high current ratio of 3.7, reflecting strong short-term debt coverage but a free cash flow of -$1.3 billion, highlighting investment pressures.

- Investment Value Assessment: Gulfport's forward P/E ratio of 7.1x is significantly lower than Viper's 21.3x, suggesting that Gulfport may represent a more value-oriented investment choice, particularly in the context of fluctuating oil and gas prices.

Wall Street's Latest Rating Changes Overview

- Openlane Upgrade: JPMorgan upgraded Openlane from neutral to overweight and raised its December 2026 price target to $38, indicating that the online used car marketplace is experiencing robust growth and has potential for sustainable expansion over the coming years.

- Dollar General Downgrade: Deutsche Bank downgraded Dollar General from buy to hold, citing challenges in its customer base and the widening gap in the K-shaped economy, which may limit same-store sales upside, reflecting a cautious outlook on the company.

- Ecolab Upgrade: UBS upgraded Ecolab from neutral to buy and raised its price target to $325, demonstrating strong demand and positive performance expectations for the chemicals company amid a favorable market environment.

- FedEx Upgrade: JPMorgan upgraded FedEx from neutral to overweight, expressing optimism ahead of its upcoming earnings report, particularly regarding the separation of its freight business, which is seen as an attractive risk-reward opportunity.

Gulfport Energy Shares Show Oversold Signal

- Oversold Indicator: Gulfport Energy Corp.'s relative strength index (RSI) has dropped to 29.8, indicating that the stock may be nearing a bottom after recent heavy selling, prompting investors to consider buying opportunities.

- Price Fluctuation: The stock hit a low of $172.71, with the current trading price at $172.24, suggesting potential for recovery as it remains above the 52-week low of $160.95, indicating market adjustment.

- Market Comparison: Compared to the S&P 500 ETF's RSI of 73.7, GPOR's oversold condition may attract bullish investors, signaling potential rebound opportunities in the near term.

- Historical Performance Analysis: With a 52-week high of $225.78, GPOR's current price reflects a 23.7% downside from its peak, necessitating careful risk-reward assessment by investors.

Gulfport Energy Q1 2026 Earnings Highlights

- Management Transition: Nick Dell'Osso will join Gulfport as the new CEO starting May 28, aiming to enhance the company's strategic execution capabilities and ensure the achievement of set goals for 2026.

- Strong Financial Performance: Gulfport generated $264 million in adjusted EBITDA and $119 million in free cash flow in Q1 2026, driven by robust commodity pricing and the continued development of high-quality assets, showcasing the company's competitive position in the market.

- Record Share Buybacks: The company repurchased 866,000 shares of common stock for approximately $172.8 million in Q1, marking the highest quarterly investment in its history, reflecting a strong commitment to shareholder returns and flexible capital allocation.

- Production and Cost Guidance: Gulfport reaffirmed its full-year production guidance of 1.03 to 1.055 billion cubic feet equivalent per day and per-unit operating cost guidance of $1.23 to $1.34 per Mcfe for 2026, ensuring stable production growth under capital discipline.

Gulfport Energy Q1 Performance Analysis

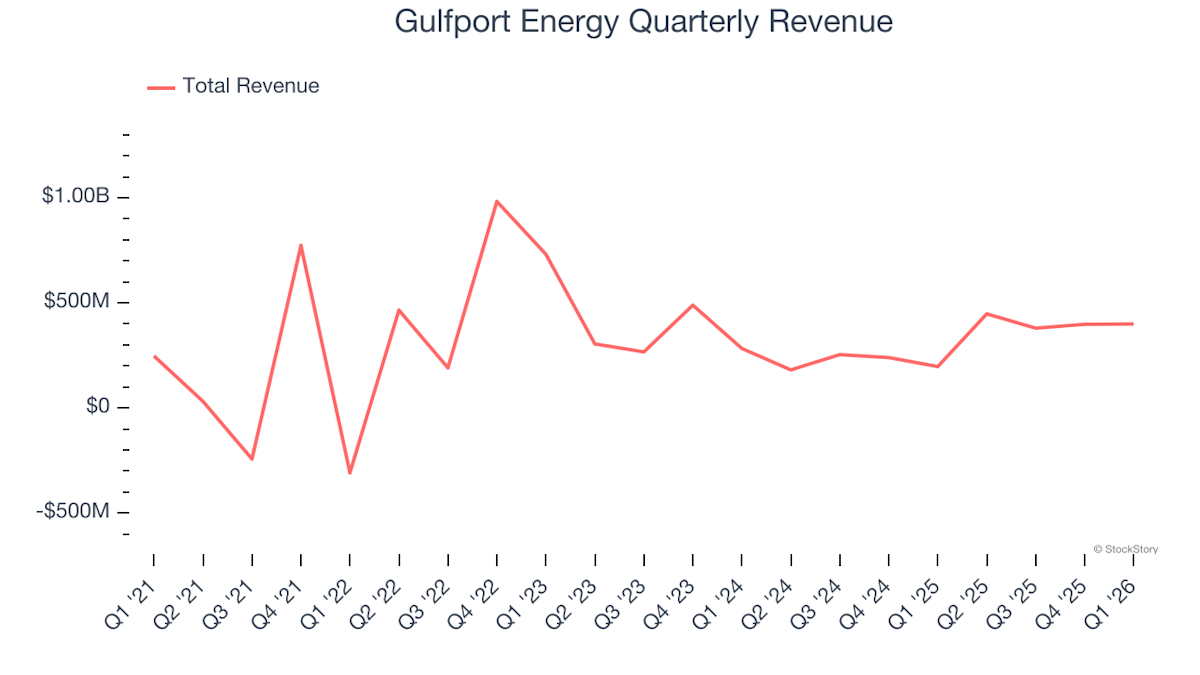

- Significant Revenue Growth: Gulfport Energy achieved $399.5 million in revenue for Q1 2026, marking a 103% year-on-year increase, although it fell short of the market's expectation of $411.3 million, indicating strong competitive positioning in the market.

- Earnings Per Share Beat: The company reported an EPS of $8.87, exceeding analysts' expectations of $7.23 by 22.7%, showcasing robust profitability and operational efficiency.

- Decline in Free Cash Flow: Free cash flow stood at $118.9 million, down 5.3 percentage points from the same quarter last year, although still above the five-year average, indicating seasonal fluctuations in investment needs.

- Production Challenges: Despite revenue growth, Gulfport's oil production fell by 29.2% year-on-year, which may impact its long-term growth potential, prompting investors to monitor production efficiency and cost management closely.

Comparative Analysis of Gulfport and Viper Energy

- Gulfport Energy Growth: Gulfport Energy reported approximately $1.3 billion in revenue for FY 2025, reflecting a 43% year-over-year increase, with net income nearing $427.8 million and a net margin of about 32.3%, indicating strong performance in the natural gas and oil markets.

- Viper Energy Model: Viper Energy achieved nearly $1.4 billion in revenue for FY 2025, a 57% increase year-over-year, but reported a net loss of approximately $69 million, resulting in a negative net margin of -5.1%, highlighting challenges in its reliance on partner production.

- Financial Health Comparison: As of December 2025, Gulfport's debt-to-equity ratio stood at approximately 0.4 with a current ratio of about 0.7, while Viper's debt-to-equity ratio was around 0.5 with a current ratio of 3.7, showcasing significant differences in their financial structures.

- Future Outlook: Gulfport is expected to see a 20% increase in earnings per share to around $26 in 2026, and while neither company pays dividends, Gulfport's profitability and value appeal make it more attractive to investors.

Investment Comparison: Gulfport vs. Viper Energy

- Gulfport Energy Growth: Gulfport Energy reported approximately $1.3 billion in revenue for FY 2025, reflecting a 43% year-over-year increase, with a net income of nearly $427.8 million and a net margin of about 32.3%, showcasing its strong performance in the natural gas and oil markets.

- Viper Energy Challenges: Despite Viper Energy achieving nearly $1.4 billion in revenue for FY 2025, a 57% increase, it reported a net loss of approximately $69 million, resulting in a negative net margin of -5.1%, indicating risks associated with its reliance on partner production activities.

- Financial Health Comparison: As of December 2025, Gulfport's debt-to-equity ratio stood at approximately 0.4, with a current ratio of about 0.7, indicating financial stability; in contrast, Viper's debt-to-equity ratio was 0.5, with a high current ratio of 3.7, reflecting strong short-term debt coverage but a free cash flow of -$1.3 billion, highlighting investment pressures.

- Investment Value Assessment: Gulfport's forward P/E ratio of 7.1x is significantly lower than Viper's 21.3x, suggesting that Gulfport may represent a more value-oriented investment choice, particularly in the context of fluctuating oil and gas prices.

Wall Street's Latest Rating Changes Overview

- Openlane Upgrade: JPMorgan upgraded Openlane from neutral to overweight and raised its December 2026 price target to $38, indicating that the online used car marketplace is experiencing robust growth and has potential for sustainable expansion over the coming years.

- Dollar General Downgrade: Deutsche Bank downgraded Dollar General from buy to hold, citing challenges in its customer base and the widening gap in the K-shaped economy, which may limit same-store sales upside, reflecting a cautious outlook on the company.

- Ecolab Upgrade: UBS upgraded Ecolab from neutral to buy and raised its price target to $325, demonstrating strong demand and positive performance expectations for the chemicals company amid a favorable market environment.

- FedEx Upgrade: JPMorgan upgraded FedEx from neutral to overweight, expressing optimism ahead of its upcoming earnings report, particularly regarding the separation of its freight business, which is seen as an attractive risk-reward opportunity.

Gulfport Energy Shares Show Oversold Signal

- Oversold Indicator: Gulfport Energy Corp.'s relative strength index (RSI) has dropped to 29.8, indicating that the stock may be nearing a bottom after recent heavy selling, prompting investors to consider buying opportunities.

- Price Fluctuation: The stock hit a low of $172.71, with the current trading price at $172.24, suggesting potential for recovery as it remains above the 52-week low of $160.95, indicating market adjustment.

- Market Comparison: Compared to the S&P 500 ETF's RSI of 73.7, GPOR's oversold condition may attract bullish investors, signaling potential rebound opportunities in the near term.

- Historical Performance Analysis: With a 52-week high of $225.78, GPOR's current price reflects a 23.7% downside from its peak, necessitating careful risk-reward assessment by investors.

Gulfport Energy Q1 2026 Earnings Highlights

- Management Transition: Nick Dell'Osso will join Gulfport as the new CEO starting May 28, aiming to enhance the company's strategic execution capabilities and ensure the achievement of set goals for 2026.

- Strong Financial Performance: Gulfport generated $264 million in adjusted EBITDA and $119 million in free cash flow in Q1 2026, driven by robust commodity pricing and the continued development of high-quality assets, showcasing the company's competitive position in the market.

- Record Share Buybacks: The company repurchased 866,000 shares of common stock for approximately $172.8 million in Q1, marking the highest quarterly investment in its history, reflecting a strong commitment to shareholder returns and flexible capital allocation.

- Production and Cost Guidance: Gulfport reaffirmed its full-year production guidance of 1.03 to 1.055 billion cubic feet equivalent per day and per-unit operating cost guidance of $1.23 to $1.34 per Mcfe for 2026, ensuring stable production growth under capital discipline.

Gulfport Energy Q1 Performance Analysis

- Significant Revenue Growth: Gulfport Energy achieved $399.5 million in revenue for Q1 2026, marking a 103% year-on-year increase, although it fell short of the market's expectation of $411.3 million, indicating strong competitive positioning in the market.

- Earnings Per Share Beat: The company reported an EPS of $8.87, exceeding analysts' expectations of $7.23 by 22.7%, showcasing robust profitability and operational efficiency.

- Decline in Free Cash Flow: Free cash flow stood at $118.9 million, down 5.3 percentage points from the same quarter last year, although still above the five-year average, indicating seasonal fluctuations in investment needs.

- Production Challenges: Despite revenue growth, Gulfport's oil production fell by 29.2% year-on-year, which may impact its long-term growth potential, prompting investors to monitor production efficiency and cost management closely.