Goldman Sachs CEO Discusses Consumer Behavior and IPO Market Outlook

Goldman Sachs Group Inc's stock fell 5.02% as it crossed below the 5-day SMA, reflecting broader market weakness with the Nasdaq-100 down 4.72% and the S&P 500 down 2.62%.

CEO David Solomon indicated that rising inflation could lead to significant shifts in consumer behavior, impacting spending and investment decisions. He expressed confidence in the Federal Reserve's ability to maintain interest rates, which may influence market liquidity. Additionally, Solomon highlighted an expected wave of mega IPOs, including SpaceX, which could drive capital into emerging technology sectors, reflecting a positive outlook despite current market conditions.

The implications of Solomon's insights suggest that while there are opportunities in the IPO market, the overall market sentiment remains cautious. Investors may need to navigate potential volatility as inflation concerns loom and consumer behavior shifts.

Trade with 70% Backtested Accuracy

Analyst Views on GS

About GS

About the author

Deposit Account Rates Decline, Lock in Competitive CD Returns

- Current CD Rates: Short-term CDs (6 to 12 months) currently offer rates around 4% APY, with the highest at 4.10% for a 14-month CD from Marcus by Goldman Sachs, indicating opportunities for competitive returns despite declining rates.

- Historical Rate Trends: Since 2009, CD rates have significantly decreased, particularly after the 2008 financial crisis when the average one-year CD rate fell to about 1%, reflecting the impact of economic slowdown and Federal Reserve rate cuts.

- Impact of Economic Policy: The COVID-19 pandemic in 2020 led to emergency rate cuts by the Fed, resulting in record low CD rates; however, subsequent inflation prompted the Fed to hike rates 11 times between 2022 and 2023, driving CD rates higher.

- Choosing the Best CD: When selecting a CD, it’s crucial to consider not only the APY but also the term length, type of financial institution, and account terms to align with personal financial goals and maximize returns.

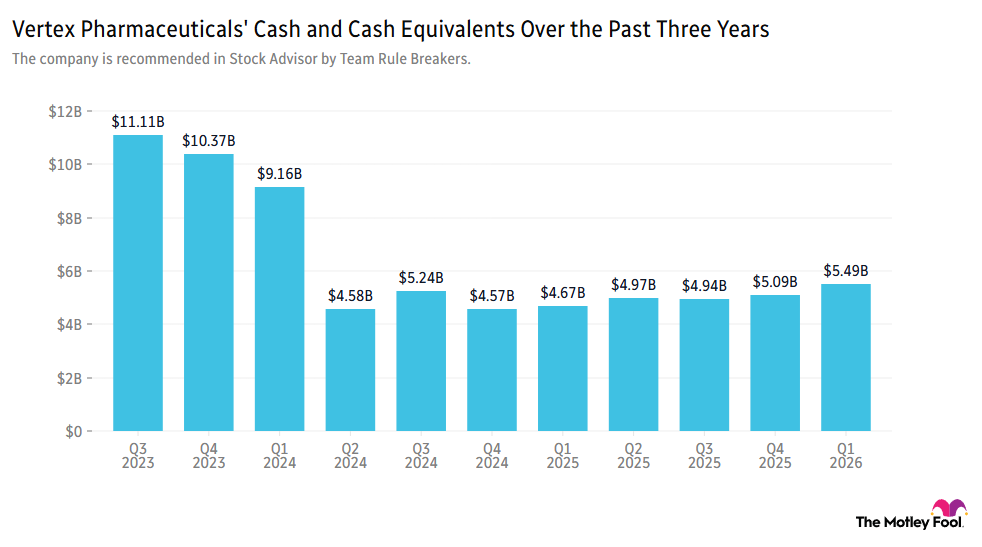

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

Meta's Plans to Compete in Cloud Computing Market Impact Neocloud Providers

- Stock Price Volatility: Following news of Meta's plans to enter the cloud computing market, CoreWeave's stock plummeted nearly 14% in a single day, while Nebius dropped 17%, reflecting market concerns about the future prospects of both companies, especially with Meta as a customer.

- Massive Contract Expansion: CoreWeave expanded its agreement with Meta in April 2023 to provide cloud computing capacity through 2032, valued at $21 billion, while Nebius announced in March it would provide $12 billion in cloud capacity, showcasing the strong collaborative potential in the AI data center sector.

- Sustained Demand Growth: Despite the competitive threat from Meta, demand for AI data centers from CoreWeave and Nebius remains robust, with CoreWeave noting that its 2026 capacity is largely sold out and 30% of its $99.4 billion revenue backlog comes from foundational AI labs, indicating urgent market demand for their services.

- Investment Opportunity Emerges: Although Meta's plans could impact CoreWeave and Nebius, the demand for AI data centers far exceeds supply, making the current stock price pullback a buying opportunity, particularly as CoreWeave's price-to-sales ratio is only 6.6, indicating potential investment value.

Meta Enters AI Data Center Market, Impact on CoreWeave and Nebius

- Increased Competition: Meta's plan to enter the AI data center market led to a 14% and 17% drop in CoreWeave and Nebius shares respectively, indicating market concerns over new competition that could impact future revenue growth for both companies.

- Shifting Customer Dynamics: CoreWeave's agreement with Meta has been extended to 2032, valued at $21 billion, while Nebius has committed to providing $12 billion in cloud computing capacity, highlighting the importance of their business relationships despite increased competition.

- Strong Demand Continues: CoreWeave's AI cloud platform demand is nearing saturation for 2026, with 30% of its $99.4 billion revenue backlog coming from foundational AI labs, showcasing its robust market position and growth potential.

- Optimistic Industry Outlook: According to Goldman Sachs, U.S. data center power demand is projected to double to 66GW by 2027, indicating that the demand for AI data centers will continue to grow, positioning CoreWeave and Nebius to benefit from this trend.

BlackRock: U.S. Stocks to Dominate AI Race

- Investment Preference: BlackRock Investment Institute maintains a neutral stance on Chinese stocks while staying overweight on U.S. equities, indicating a belief that U.S. companies will dominate the AI race, reflecting confidence in the U.S. market.

- Market Performance Comparison: While the Nasdaq Composite has gained over 12% this year, China's ChiNext index has surged more than 20%, indicating strong short-term performance of Chinese tech stocks; however, the overall MSCI China index has fallen over 10%, reflecting market uncertainty.

- Policy Support and Challenges: Beijing has rolled out policies to support domestic AI development amid U.S. restrictions on high-end technology, yet the unclear profitability of companies in the context of slower economic growth and fierce competition highlights market complexities.

- Investment Opportunities: BlackRock analysts see potential in physical AI, emphasizing the integration of AI technology into hardware, while recommending stocks exposed to scarce industry inputs, showcasing a focus on infrastructure investments.

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

Deposit Account Rates Decline, Lock in Competitive CD Returns

- Current CD Rates: Short-term CDs (6 to 12 months) currently offer rates around 4% APY, with the highest at 4.10% for a 14-month CD from Marcus by Goldman Sachs, indicating opportunities for competitive returns despite declining rates.

- Historical Rate Trends: Since 2009, CD rates have significantly decreased, particularly after the 2008 financial crisis when the average one-year CD rate fell to about 1%, reflecting the impact of economic slowdown and Federal Reserve rate cuts.

- Impact of Economic Policy: The COVID-19 pandemic in 2020 led to emergency rate cuts by the Fed, resulting in record low CD rates; however, subsequent inflation prompted the Fed to hike rates 11 times between 2022 and 2023, driving CD rates higher.

- Choosing the Best CD: When selecting a CD, it’s crucial to consider not only the APY but also the term length, type of financial institution, and account terms to align with personal financial goals and maximize returns.

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

Meta's Plans to Compete in Cloud Computing Market Impact Neocloud Providers

- Stock Price Volatility: Following news of Meta's plans to enter the cloud computing market, CoreWeave's stock plummeted nearly 14% in a single day, while Nebius dropped 17%, reflecting market concerns about the future prospects of both companies, especially with Meta as a customer.

- Massive Contract Expansion: CoreWeave expanded its agreement with Meta in April 2023 to provide cloud computing capacity through 2032, valued at $21 billion, while Nebius announced in March it would provide $12 billion in cloud capacity, showcasing the strong collaborative potential in the AI data center sector.

- Sustained Demand Growth: Despite the competitive threat from Meta, demand for AI data centers from CoreWeave and Nebius remains robust, with CoreWeave noting that its 2026 capacity is largely sold out and 30% of its $99.4 billion revenue backlog comes from foundational AI labs, indicating urgent market demand for their services.

- Investment Opportunity Emerges: Although Meta's plans could impact CoreWeave and Nebius, the demand for AI data centers far exceeds supply, making the current stock price pullback a buying opportunity, particularly as CoreWeave's price-to-sales ratio is only 6.6, indicating potential investment value.

Meta Enters AI Data Center Market, Impact on CoreWeave and Nebius

- Increased Competition: Meta's plan to enter the AI data center market led to a 14% and 17% drop in CoreWeave and Nebius shares respectively, indicating market concerns over new competition that could impact future revenue growth for both companies.

- Shifting Customer Dynamics: CoreWeave's agreement with Meta has been extended to 2032, valued at $21 billion, while Nebius has committed to providing $12 billion in cloud computing capacity, highlighting the importance of their business relationships despite increased competition.

- Strong Demand Continues: CoreWeave's AI cloud platform demand is nearing saturation for 2026, with 30% of its $99.4 billion revenue backlog coming from foundational AI labs, showcasing its robust market position and growth potential.

- Optimistic Industry Outlook: According to Goldman Sachs, U.S. data center power demand is projected to double to 66GW by 2027, indicating that the demand for AI data centers will continue to grow, positioning CoreWeave and Nebius to benefit from this trend.

BlackRock: U.S. Stocks to Dominate AI Race

- Investment Preference: BlackRock Investment Institute maintains a neutral stance on Chinese stocks while staying overweight on U.S. equities, indicating a belief that U.S. companies will dominate the AI race, reflecting confidence in the U.S. market.

- Market Performance Comparison: While the Nasdaq Composite has gained over 12% this year, China's ChiNext index has surged more than 20%, indicating strong short-term performance of Chinese tech stocks; however, the overall MSCI China index has fallen over 10%, reflecting market uncertainty.

- Policy Support and Challenges: Beijing has rolled out policies to support domestic AI development amid U.S. restrictions on high-end technology, yet the unclear profitability of companies in the context of slower economic growth and fierce competition highlights market complexities.

- Investment Opportunities: BlackRock analysts see potential in physical AI, emphasizing the integration of AI technology into hardware, while recommending stocks exposed to scarce industry inputs, showcasing a focus on infrastructure investments.

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.