Carnival Corp Reports Record Revenue Amid Market Decline

Carnival Corp's stock fell 3.53% and hit a 20-day low amid a broader market decline, with the Nasdaq-100 down 1.73% and the S&P 500 down 1.47%.

Despite the stock's decline, Carnival reported record revenue of $26.6 billion and adjusted net income of $3.1 billion for fiscal 2025, demonstrating robust financial recovery and boosting investor confidence. The company also ended Q4 with $7.2 billion in customer deposits, indicating strong future demand for cruises, which are more affordable than land resorts. This positive financial performance suggests significant stock potential, with analysts projecting a price increase to $40 within 11 months.

The strong financial results and high customer deposits position Carnival favorably for future growth, even as the stock experiences short-term volatility in a challenging market environment.

Trade with 70% Backtested Accuracy

Analyst Views on CCL

About CCL

About the author

Holland America Line Launches Anniversary Sale with Major Discounts

- Anniversary Sale Launch: Holland America Line is celebrating its 153rd anniversary with a month-long sale from April 2 to 30, 2026, offering up to 30% off cruise fares and onboard credits up to $400 per stateroom, aimed at enticing both loyal and new travelers to experience their thoughtfully crafted itineraries.

- Family Travel Incentives: The promotion allows third and fourth guests aged 18 and under to cruise for free on select sailings, significantly reducing costs for family vacations and enhancing Holland America's appeal in the family travel segment.

- Combination Offer Policy: The Anniversary Sale can be combined with the

Royal Caribbean vs. Carnival: Profitability Comparison

- Profitability Analysis: Royal Caribbean achieved $4.3 billion in adjusted net income on $17.9 billion in revenue last year, resulting in a profit margin of 24%, showcasing its strong pricing power and profitability in the market.

- Future Growth Expectations: Royal Caribbean anticipates an annualized earnings growth of 20% through 2027, compared to Carnival's 12%, indicating that Royal Caribbean has a stronger potential for long-term investment returns.

- Market Performance Discrepancy: While both companies' stocks performed similarly over the past year, Royal Caribbean's stock surged 309% over the past three years, compared to Carnival's 142% increase, highlighting Royal Caribbean's advantage in long-term investments.

- Strategic Investment Direction: Royal Caribbean is investing in new ships and unique destinations to expand its customer base and enhance profitability, while Carnival's strategy focuses on price competition to attract a broader customer base, which may impact its long-term profitability.

Royal Caribbean vs. Carnival: Performance Comparison

- Profitability Comparison: Royal Caribbean achieved an adjusted net income of $4.3 billion on $17.9 billion in revenue last year, boasting a profit margin of 24%, while Carnival's margin stands at only 11%, providing Royal Caribbean with a stronger capacity for reinvestment and risk management in the competitive landscape.

- Future Growth Expectations: Royal Caribbean anticipates an annualized earnings growth of 20% through 2027, compared to Carnival's plan for a cumulative 50% adjusted earnings growth from 2025 to 2029, highlighting Royal Caribbean's superior profitability and market positioning.

- Stock Performance Discrepancy: Although both companies have shown similar stock performance over the past year, Royal Caribbean's shares surged 309% over the last three years, while Carnival's increased by only 142%, indicating Royal Caribbean's attractiveness for long-term investment returns.

- Market Positioning Strategy: Royal Caribbean focuses on the premium market, investing in new ships and unique destinations, which is expected to expand its customer base, while Carnival competes aggressively on price to attract a broader audience, a strategy that may drive volume but could compromise long-term profitability compared to Royal Caribbean.

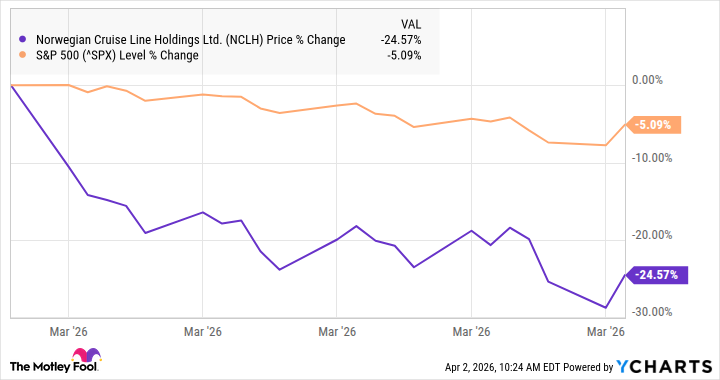

Norwegian Cruise Line's Poor Performance Leads to Stock Decline

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, driven by higher capacity days, yet fell short of the $2.34 billion estimate, indicating management execution gaps that led to decreased market confidence.

- Significant Stock Decline: The stock plummeted 24% last month due to disappointing earnings and geopolitical instability from the Iran war, reflecting investor concerns about the company's future prospects amidst rising oil prices.

- Improved Profitability: Despite missing revenue expectations, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, demonstrating effective cost control, yet failing to reverse the overall negative trend.

- Board Changes: Following pressure from activist investor Elliott Investment Management, Norwegian has appointed five new board members, which, while not immediately boosting stock prices, may lay the groundwork for future strategic adjustments and improvements.

Norwegian Cruise Line Misses Q4 Revenue Estimates

- Revenue Miss: Norwegian Cruise Line's Q4 revenue rose 6% to $2.2 billion, falling short of the $2.34 billion estimate, as higher capacity days contributed to growth but execution gaps significantly impacted performance.

- Profitability Improvement: Adjusted EBITDA increased by 11% to $2.73 billion, while adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, indicating effective cost management despite revenue challenges.

- Bleak Outlook: The company forecasts flat net yields for 2026, with cruise costs expected to rise by 0.9%, which will pressure profitability; adjusted EPS guidance of $2.38 is below the consensus of $2.60, reflecting ongoing challenges.

- Board Changes: Following pressure from activist investor Elliott Management, Norwegian appointed five new board members, which, while not boosting stock prices immediately, may set the stage for future improvements in governance and performance.

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

Holland America Line Launches Anniversary Sale with Major Discounts

- Anniversary Sale Launch: Holland America Line is celebrating its 153rd anniversary with a month-long sale from April 2 to 30, 2026, offering up to 30% off cruise fares and onboard credits up to $400 per stateroom, aimed at enticing both loyal and new travelers to experience their thoughtfully crafted itineraries.

- Family Travel Incentives: The promotion allows third and fourth guests aged 18 and under to cruise for free on select sailings, significantly reducing costs for family vacations and enhancing Holland America's appeal in the family travel segment.

- Combination Offer Policy: The Anniversary Sale can be combined with the

Royal Caribbean vs. Carnival: Profitability Comparison

- Profitability Analysis: Royal Caribbean achieved $4.3 billion in adjusted net income on $17.9 billion in revenue last year, resulting in a profit margin of 24%, showcasing its strong pricing power and profitability in the market.

- Future Growth Expectations: Royal Caribbean anticipates an annualized earnings growth of 20% through 2027, compared to Carnival's 12%, indicating that Royal Caribbean has a stronger potential for long-term investment returns.

- Market Performance Discrepancy: While both companies' stocks performed similarly over the past year, Royal Caribbean's stock surged 309% over the past three years, compared to Carnival's 142% increase, highlighting Royal Caribbean's advantage in long-term investments.

- Strategic Investment Direction: Royal Caribbean is investing in new ships and unique destinations to expand its customer base and enhance profitability, while Carnival's strategy focuses on price competition to attract a broader customer base, which may impact its long-term profitability.

Royal Caribbean vs. Carnival: Performance Comparison

- Profitability Comparison: Royal Caribbean achieved an adjusted net income of $4.3 billion on $17.9 billion in revenue last year, boasting a profit margin of 24%, while Carnival's margin stands at only 11%, providing Royal Caribbean with a stronger capacity for reinvestment and risk management in the competitive landscape.

- Future Growth Expectations: Royal Caribbean anticipates an annualized earnings growth of 20% through 2027, compared to Carnival's plan for a cumulative 50% adjusted earnings growth from 2025 to 2029, highlighting Royal Caribbean's superior profitability and market positioning.

- Stock Performance Discrepancy: Although both companies have shown similar stock performance over the past year, Royal Caribbean's shares surged 309% over the last three years, while Carnival's increased by only 142%, indicating Royal Caribbean's attractiveness for long-term investment returns.

- Market Positioning Strategy: Royal Caribbean focuses on the premium market, investing in new ships and unique destinations, which is expected to expand its customer base, while Carnival competes aggressively on price to attract a broader audience, a strategy that may drive volume but could compromise long-term profitability compared to Royal Caribbean.

Norwegian Cruise Line's Poor Performance Leads to Stock Decline

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, driven by higher capacity days, yet fell short of the $2.34 billion estimate, indicating management execution gaps that led to decreased market confidence.

- Significant Stock Decline: The stock plummeted 24% last month due to disappointing earnings and geopolitical instability from the Iran war, reflecting investor concerns about the company's future prospects amidst rising oil prices.

- Improved Profitability: Despite missing revenue expectations, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, demonstrating effective cost control, yet failing to reverse the overall negative trend.

- Board Changes: Following pressure from activist investor Elliott Investment Management, Norwegian has appointed five new board members, which, while not immediately boosting stock prices, may lay the groundwork for future strategic adjustments and improvements.

Norwegian Cruise Line Misses Q4 Revenue Estimates

- Revenue Miss: Norwegian Cruise Line's Q4 revenue rose 6% to $2.2 billion, falling short of the $2.34 billion estimate, as higher capacity days contributed to growth but execution gaps significantly impacted performance.

- Profitability Improvement: Adjusted EBITDA increased by 11% to $2.73 billion, while adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, indicating effective cost management despite revenue challenges.

- Bleak Outlook: The company forecasts flat net yields for 2026, with cruise costs expected to rise by 0.9%, which will pressure profitability; adjusted EPS guidance of $2.38 is below the consensus of $2.60, reflecting ongoing challenges.

- Board Changes: Following pressure from activist investor Elliott Management, Norwegian appointed five new board members, which, while not boosting stock prices immediately, may set the stage for future improvements in governance and performance.

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.