Alphabet Inc. Reports Strong Q1 Earnings, Surpassing Expectations

Alphabet Inc. shares rose 6.52% in pre-market trading, reaching a 52-week high.

The company's Q1 earnings report revealed a GAAP EPS of $5.11, exceeding expectations by $2.44, and total revenue of $109.9 billion, marking a 21.8% year-over-year increase. This strong performance across all business segments, particularly in Google Cloud, which saw a 63% revenue surge, has reinforced market confidence in Alphabet's financial health. Additionally, the company announced a 5% increase in its dividend, reflecting its commitment to shareholder returns.

This robust earnings report not only highlights Alphabet's sustained growth but also positions the company favorably in the competitive tech landscape, particularly in cloud computing and AI investments.

Trade with 70% Backtested Accuracy

Analyst Views on GOOG

About GOOG

About the author

World Cup Drives Record Queries for Google Search

- Record Search Queries: Following Argentina's victory over Egypt, Google Search experienced historic highs in query volume, demonstrating the World Cup's significant impact on search engines and reinforcing Google's dominance in the search market.

- Surge in Real-Time Queries: Google reported that query volume peaked at unprecedented levels right after Argentina's winning goal, indicating a heightened user interest in real-time event information, although specific numbers were not disclosed.

- Stable Market Share: Google maintains a 90% share of the search market, showcasing its ability to remain relevant despite competition from AI chatbots, which highlights the adaptability of its traditional search engine in a changing technological landscape.

- Strong Revenue Growth: The company's stock price has more than doubled in the past year, with the fastest revenue growth in the first quarter since 2022, indicating robust financial performance amid evolving market conditions.

Waymo Launches Driverless Service Expansion

- Driverless Service Expansion: Waymo announced the launch of its driverless vehicle service in San Diego, Las Vegas, Tampa, and Denver, initially available to Alphabet employees before public rollout, indicating a proactive approach in the autonomous ride-hailing market.

- Intensifying Competition: With competitors like Tesla's robotaxi and Amazon's Zoox emerging, Waymo is accelerating its market expansion to address increasing commercialization competition, ensuring its leading position in the autonomous driving sector.

- Funding Support: Waymo completed a $16 billion funding round earlier this year, valuing the company at approximately $126 billion, which provides robust financial backing for its technology development and market expansion, further solidifying its market position.

- Technology Validation Phase: Waymo has begun autonomous driving tests with its Hyundai IONIQ 5 vehicles, equipped with an “autonomous specialist,” aiming to validate its technology for fully autonomous operations and laying the groundwork for offering more travel options in the future.

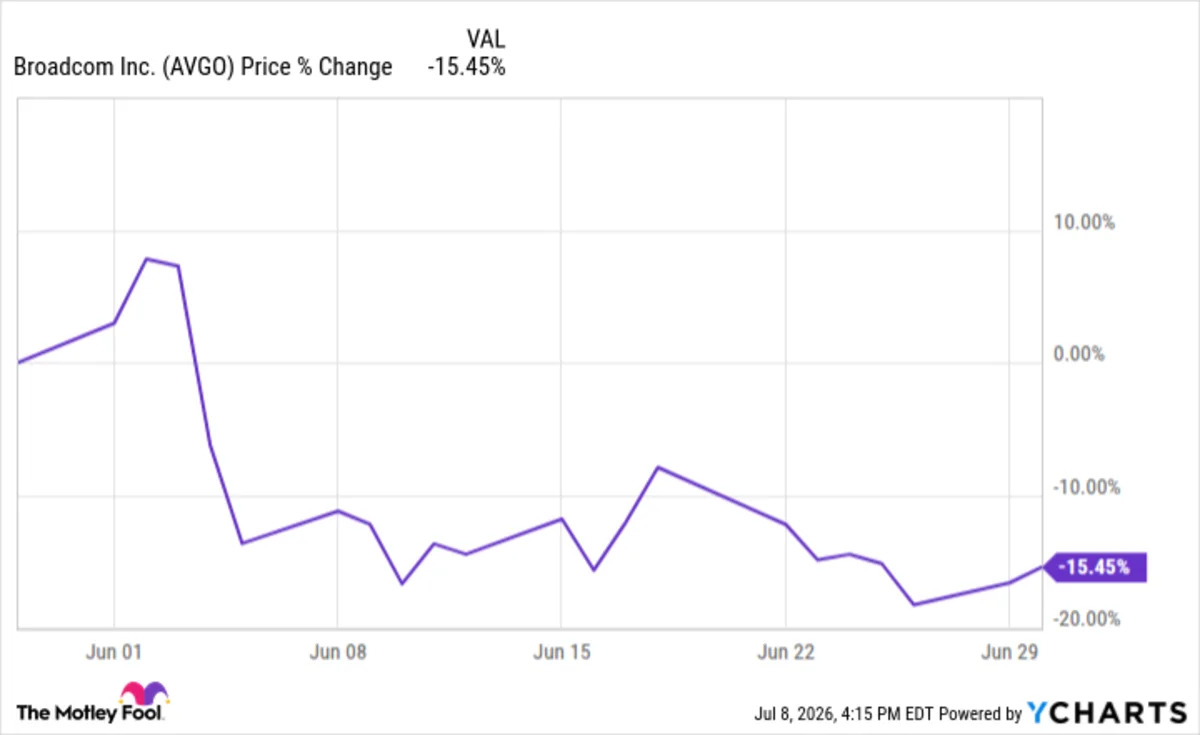

Broadcom Shares Drop 15% in June Amid AI Revenue Concerns

- Earnings Performance: Broadcom reported a 48% revenue increase to $22.2 billion in Q2, with adjusted EPS rising from $1.58 to $2.44, slightly beating expectations; however, concerns arose as AI revenue growth did not meet market forecasts, leading to a stock decline.

- AI Revenue Dynamics: The company's AI-related revenue surged 143% to $10.8 billion, but the forecast for Q3 at $16 billion fell short of the $17 billion expected, indicating market apprehension about future growth prospects.

- Market Reaction: Following the earnings report, Broadcom's stock plummeted 15% due to investor concerns over high valuations and overspending on AI infrastructure, reflecting a diminished confidence in the company's growth trajectory.

- Strategic Partnership: Broadcom signed a $30 billion deal with Apple for chip manufacturing, with Apple investing $1.5 billion to expand a Colorado facility, potentially providing new growth avenues for Broadcom, although the market remains cautious about long-term sustainability.

Google Sets Search Record During World Cup Final

- Record Search Volume: Following Argentina's national team comeback victory in the World Cup final, Google Search achieved its highest usage ever, demonstrating its immense draw during major sporting events.

- Peak Query Moment: Google reported that queries peaked immediately after Argentina's winning goal, highlighting the World Cup's significant impact on search engine traffic, although specific numbers were not disclosed.

- Stable Market Share: Google maintains a 90% share of the search market, proving the relevance of its traditional search engine amidst the rise of AI chatbots, which have become increasingly prevalent in recent years.

- Strong Revenue Growth: The company's stock price has more than doubled over the past year, and its revenue growth in the first quarter was the fastest since 2022, indicating robust performance in the digital advertising sector.

Berkshire's Abel Rapidly Accumulates Alphabet Stake

- Increased Stake in Google: Berkshire Hathaway significantly raised its Alphabet holdings from approximately $550 million to $16.6 billion in Q1 2026, demonstrating CEO Abel's strong confidence in the tech sector and marking a strategic shift for the company.

- Private Placement Investment: Berkshire agreed to a $10 billion private placement to acquire 28.6 million shares of Alphabet, indicating Abel's willingness to make substantial investments in the market to support Alphabet's growth initiatives.

- Cloud Business Growth: Alphabet's cloud segment saw a remarkable 63% year-over-year growth in Q1 2026, generating around $20 billion in revenue and tripling operating income to $6.6 billion, highlighting robust market demand and future growth potential.

- Shift in Investment Strategy: Abel's aggressive investment approach signals a departure from merely hoarding cash, reflecting confidence in Alphabet's future, although it also carries risks related to AI spending and regulatory pressures.

Berkshire Invests Over $20 Billion in Alphabet

- Significant Investment Scale: Berkshire Hathaway has built a position in Alphabet worth over $20 billion, with holdings increasing from approximately $16.6 billion to over $20 billion in Q1 2026, reflecting new CEO Greg Abel's aggressive investment strategy.

- Private Placement Boost: In June 2026, Berkshire agreed to a $10 billion private placement, acquiring 28.6 million shares directly from Alphabet, indicating strong confidence in Alphabet's future growth while also funding its cloud business expansion.

- Rapid Cloud Business Growth: Alphabet's cloud revenue surged 63% year-over-year in Q1 2026, reaching about $20 billion, with operating income tripling to $6.6 billion, showcasing robust market demand and profitability.

- Strategic Shift Signal: Abel's investment decisions suggest that Berkshire will actively seek to deploy cash into quality businesses rather than hoarding it, marking a significant shift in investment strategy that could influence future market performance.

World Cup Drives Record Queries for Google Search

- Record Search Queries: Following Argentina's victory over Egypt, Google Search experienced historic highs in query volume, demonstrating the World Cup's significant impact on search engines and reinforcing Google's dominance in the search market.

- Surge in Real-Time Queries: Google reported that query volume peaked at unprecedented levels right after Argentina's winning goal, indicating a heightened user interest in real-time event information, although specific numbers were not disclosed.

- Stable Market Share: Google maintains a 90% share of the search market, showcasing its ability to remain relevant despite competition from AI chatbots, which highlights the adaptability of its traditional search engine in a changing technological landscape.

- Strong Revenue Growth: The company's stock price has more than doubled in the past year, with the fastest revenue growth in the first quarter since 2022, indicating robust financial performance amid evolving market conditions.

Waymo Launches Driverless Service Expansion

- Driverless Service Expansion: Waymo announced the launch of its driverless vehicle service in San Diego, Las Vegas, Tampa, and Denver, initially available to Alphabet employees before public rollout, indicating a proactive approach in the autonomous ride-hailing market.

- Intensifying Competition: With competitors like Tesla's robotaxi and Amazon's Zoox emerging, Waymo is accelerating its market expansion to address increasing commercialization competition, ensuring its leading position in the autonomous driving sector.

- Funding Support: Waymo completed a $16 billion funding round earlier this year, valuing the company at approximately $126 billion, which provides robust financial backing for its technology development and market expansion, further solidifying its market position.

- Technology Validation Phase: Waymo has begun autonomous driving tests with its Hyundai IONIQ 5 vehicles, equipped with an “autonomous specialist,” aiming to validate its technology for fully autonomous operations and laying the groundwork for offering more travel options in the future.

Broadcom Shares Drop 15% in June Amid AI Revenue Concerns

- Earnings Performance: Broadcom reported a 48% revenue increase to $22.2 billion in Q2, with adjusted EPS rising from $1.58 to $2.44, slightly beating expectations; however, concerns arose as AI revenue growth did not meet market forecasts, leading to a stock decline.

- AI Revenue Dynamics: The company's AI-related revenue surged 143% to $10.8 billion, but the forecast for Q3 at $16 billion fell short of the $17 billion expected, indicating market apprehension about future growth prospects.

- Market Reaction: Following the earnings report, Broadcom's stock plummeted 15% due to investor concerns over high valuations and overspending on AI infrastructure, reflecting a diminished confidence in the company's growth trajectory.

- Strategic Partnership: Broadcom signed a $30 billion deal with Apple for chip manufacturing, with Apple investing $1.5 billion to expand a Colorado facility, potentially providing new growth avenues for Broadcom, although the market remains cautious about long-term sustainability.

Google Sets Search Record During World Cup Final

- Record Search Volume: Following Argentina's national team comeback victory in the World Cup final, Google Search achieved its highest usage ever, demonstrating its immense draw during major sporting events.

- Peak Query Moment: Google reported that queries peaked immediately after Argentina's winning goal, highlighting the World Cup's significant impact on search engine traffic, although specific numbers were not disclosed.

- Stable Market Share: Google maintains a 90% share of the search market, proving the relevance of its traditional search engine amidst the rise of AI chatbots, which have become increasingly prevalent in recent years.

- Strong Revenue Growth: The company's stock price has more than doubled over the past year, and its revenue growth in the first quarter was the fastest since 2022, indicating robust performance in the digital advertising sector.

Berkshire's Abel Rapidly Accumulates Alphabet Stake

- Increased Stake in Google: Berkshire Hathaway significantly raised its Alphabet holdings from approximately $550 million to $16.6 billion in Q1 2026, demonstrating CEO Abel's strong confidence in the tech sector and marking a strategic shift for the company.

- Private Placement Investment: Berkshire agreed to a $10 billion private placement to acquire 28.6 million shares of Alphabet, indicating Abel's willingness to make substantial investments in the market to support Alphabet's growth initiatives.

- Cloud Business Growth: Alphabet's cloud segment saw a remarkable 63% year-over-year growth in Q1 2026, generating around $20 billion in revenue and tripling operating income to $6.6 billion, highlighting robust market demand and future growth potential.

- Shift in Investment Strategy: Abel's aggressive investment approach signals a departure from merely hoarding cash, reflecting confidence in Alphabet's future, although it also carries risks related to AI spending and regulatory pressures.

Berkshire Invests Over $20 Billion in Alphabet

- Significant Investment Scale: Berkshire Hathaway has built a position in Alphabet worth over $20 billion, with holdings increasing from approximately $16.6 billion to over $20 billion in Q1 2026, reflecting new CEO Greg Abel's aggressive investment strategy.

- Private Placement Boost: In June 2026, Berkshire agreed to a $10 billion private placement, acquiring 28.6 million shares directly from Alphabet, indicating strong confidence in Alphabet's future growth while also funding its cloud business expansion.

- Rapid Cloud Business Growth: Alphabet's cloud revenue surged 63% year-over-year in Q1 2026, reaching about $20 billion, with operating income tripling to $6.6 billion, showcasing robust market demand and profitability.

- Strategic Shift Signal: Abel's investment decisions suggest that Berkshire will actively seek to deploy cash into quality businesses rather than hoarding it, marking a significant shift in investment strategy that could influence future market performance.