Paysign Q4 Earnings Beat Expectations, Optimistic 2026 Outlook

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 24 2026

0mins

Source: seekingalpha

- Strong Earnings Report: Paysign reported Q4 GAAP EPS of $0.02, meeting expectations, with revenue of $22.76 million reflecting a 45.8% year-over-year increase, exceeding estimates by $1.21 million, indicating robust market performance and growth potential.

- 2026 Outlook: The company anticipates revenue between $106.5 million and $110.5 million for 2026, representing a year-over-year growth of 30% to 35%, with plasma and pharma contributing equally, showcasing strategic success in diversifying revenue streams.

- Margin Improvement: Gross profit margins are expected to range from 60% to 62%, reflecting increased contributions from the pharma patient affordability business, while operating expenses are projected to rise by 20%, indicating ongoing investments in technology and personnel.

- First Quarter Expectations: For Q1 2026, Paysign expects revenue of $27.0 million to $27.5 million, representing a 45.2% to 47.8% growth year-over-year, with operating margins projected between 20% and 22%, demonstrating strong competitive positioning and profitability in the market.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PAYS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PAYS

Wall Street analysts forecast PAYS stock price to rise

4 Analyst Rating

4 Buy

0 Hold

0 Sell

Strong Buy

Current: 7.290

Low

8.50

Averages

9.00

High

10.00

Current: 7.290

Low

8.50

Averages

9.00

High

10.00

About PAYS

Paysign, Inc. is a provider of prepaid card programs, patient affordability offerings, digital banking services and integrated payment processing designed for businesses, consumers and government institutions. The Company’s payment solutions are utilized by its corporate customers to increase customer loyalty, increase patient adherence rates, reduce administration costs and streamline operations. It markets its prepaid card solutions under its Paysign brand. Its end-to-end technologies securely enable digital payout solutions and facilitate the distribution of funds for donor compensation, copay assistance, employee rewards, travel expenses, per diem, reimbursements, rebates, and countless other exchanges of value. It operates on a payments platform with fintech capabilities that can be seamlessly integrated with its clients’ systems. It offers donor engagement app, which integrates seamlessly with existing donor management systems, delivering immediate value to plasma centers.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Paysign Reports Strong Q1 Growth but Conservative Guidance Leads to Stock Drop

- Significant Earnings Growth: Paysign's Q1 revenue surged 50.8% to $28.04 million, with adjusted EPS rising 80% to $0.09, both figures significantly exceeding analyst expectations, showcasing the company's robust performance in payment card processing.

- Pharmaceutical Business Expansion: The pharmaceutical segment grew by 81.9%, adding 45 patient affordability programs and achieving a 50% increase in customer count, indicating Paysign's enhanced market penetration in the pharmaceutical sector and bolstering future revenue potential.

- Plasma Donation Revenue Recovery: Plasma donation revenue increased by 24.9%, with a rise in customer numbers and revenue per donor center rebounding for the first time after a downturn, suggesting a recovery in business performance after a challenging period.

- Negative Market Reaction: Despite strong results, management's decision to maintain guidance without raising expectations led to a stock price decline after a 35% year-to-date increase, reflecting investor caution regarding future growth prospects.

See More

Paysign Reports Strong Q1 2026 Earnings with Pharma Growth

- Significant Revenue Growth: Paysign reported Q1 2026 revenue of $28 million, a 50.8% increase year-over-year, with net income rising 110% to $5.4 million, highlighting strong demand in the patient affordability sector and robust market performance.

- Program Expansion: The company launched four new programs in Q1, bringing total active programs to 135, with expectations to reach 147 to 150 by the end of Q2, indicating a proactive strategy to expand market share and client base.

- Margin Improvement: Gross profit margin increased from 62.9% to 65%, primarily due to a higher revenue mix from pharma, while operating margin rose from 13.4% to 23.8%, demonstrating significant improvements in cost control and profitability.

- Optimistic Outlook: Management expects full-year revenue between $106.5 million and $110.5 million, with net income projected at $13 million to $16 million, reflecting confidence in achieving the upper end of guidance based on a strong start to the year.

See More

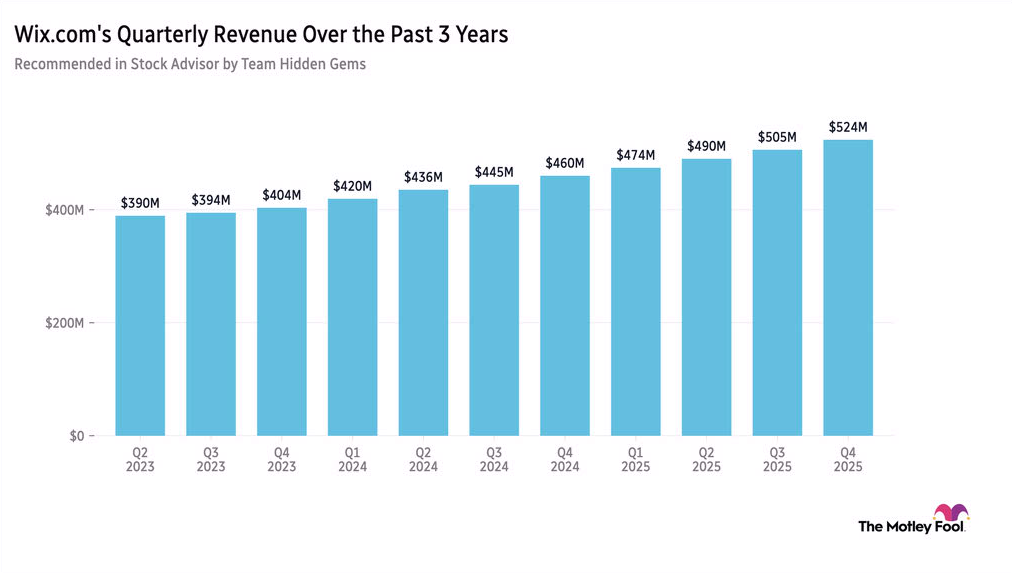

Wix.com Leverages AI Tools to Achieve Revenue Growth

- Significant Revenue Growth: Wix.com reported a 14% year-over-year increase in first-quarter revenue to $541 million, exceeding market expectations and demonstrating resilience amid AI competition, with management forecasting mid-teens growth in revenue and bookings for 2026.

- Share Buyback Strategy: The company repurchased approximately 30% of its outstanding shares in April to counteract a stock price decline of over 10% following the earnings update, indicating management's confidence in the company's long-term value.

- Accelerated AI Innovation: Wix.com recently launched its proprietary LLM, powering its website editor Wix Harmony, showcasing the company's enhanced innovation capabilities in the AI-driven web and app building space.

- Intensifying Market Competition: Despite challenges from AI competitors like Anthropic's Claude Design, Wix.com is striving to maintain market share, with the CEO emphasizing the company's adaptability in a rapidly changing technological landscape.

See More

Paysign Set to Announce Q1 Earnings with Strong Estimates

- Earnings Announcement: Paysign (PAYS) is set to release its Q1 earnings on May 12th after market close, with consensus EPS estimate at $0.07 and revenue estimate at $27.01 million, reflecting a robust 45.2% year-over-year growth.

- Performance Beat: Over the past year, Paysign has exceeded EPS estimates 75% of the time and revenue estimates 100% of the time, indicating a strong track record of reliability and profitability that could bolster investor confidence.

- Estimate Revisions: In the last three months, EPS estimates have seen three upward revisions with no downward adjustments, while revenue estimates have experienced four upward revisions, suggesting increasing analyst confidence in the company's future performance, which may drive stock price appreciation.

- Long-term Growth Target: Paysign has outlined a revenue growth target of 30%-35% for 2026 with ongoing margin expansion, reflecting the company's strategic positioning to capitalize on future market opportunities and providing a positive outlook for investors.

See More

Paysign to Discuss Q1 2026 Earnings on May 12

- Earnings Call Schedule: Paysign, Inc. will discuss its Q1 2026 earnings on May 12, 2026, at 5:00 p.m. Eastern Time, which is expected to provide crucial insights into the company's financial performance that may influence investor decisions.

- Participant Details: U.S. dial-in number is 877.407.2988, and international dial-in is +1.201.389.0923, offering multiple participation options to ensure investors can conveniently access the information.

- Replay Information: The earnings call replay will be available until August 12, 2026, with dial-in numbers 877.660.6853 or +1.201.612.7415, ensuring that investors who cannot participate live can still obtain relevant information.

- Company Overview: Paysign focuses on the intersection of fintech and healthcare, providing patient affordability solutions and donor compensation programs, committed to improving efficiencies, reducing costs, and optimizing payment processing in the life sciences sector.

See More

Surge in Options Trading Volume for Paysign and ASTS

- Options Volume Surge for Paysign: Today, Paysign Inc's options volume reached 4,544 contracts, equivalent to approximately 454,400 shares, representing 89% of its average daily trading volume of 510,355 shares over the past month, indicating strong investor interest in the stock.

- High-Frequency Trading Insight: Notably, the $5 strike call option expiring on April 17, 2026, saw 2,713 contracts traded today, representing about 271,300 shares, suggesting market expectations for future price increases.

- ASTS Options Activity: Concurrently, AST SpaceMobile Inc recorded options trading volume of 114,469 contracts, approximately 11.4 million shares, which is 88.9% of its average daily trading volume of 12.9 million shares over the past month, reflecting sustained market interest in the company.

- Bullish Call Options Trend: Particularly, the $95 strike call option expiring on April 2, 2026, had 7,468 contracts traded today, representing around 746,800 shares, indicating optimistic sentiment among investors regarding ASTS's future performance.

See More

Paysign Reports Strong Q1 Growth but Conservative Guidance Leads to Stock Drop

- Significant Earnings Growth: Paysign's Q1 revenue surged 50.8% to $28.04 million, with adjusted EPS rising 80% to $0.09, both figures significantly exceeding analyst expectations, showcasing the company's robust performance in payment card processing.

- Pharmaceutical Business Expansion: The pharmaceutical segment grew by 81.9%, adding 45 patient affordability programs and achieving a 50% increase in customer count, indicating Paysign's enhanced market penetration in the pharmaceutical sector and bolstering future revenue potential.

- Plasma Donation Revenue Recovery: Plasma donation revenue increased by 24.9%, with a rise in customer numbers and revenue per donor center rebounding for the first time after a downturn, suggesting a recovery in business performance after a challenging period.

- Negative Market Reaction: Despite strong results, management's decision to maintain guidance without raising expectations led to a stock price decline after a 35% year-to-date increase, reflecting investor caution regarding future growth prospects.

See More

Paysign Reports Strong Q1 2026 Earnings with Pharma Growth

- Significant Revenue Growth: Paysign reported Q1 2026 revenue of $28 million, a 50.8% increase year-over-year, with net income rising 110% to $5.4 million, highlighting strong demand in the patient affordability sector and robust market performance.

- Program Expansion: The company launched four new programs in Q1, bringing total active programs to 135, with expectations to reach 147 to 150 by the end of Q2, indicating a proactive strategy to expand market share and client base.

- Margin Improvement: Gross profit margin increased from 62.9% to 65%, primarily due to a higher revenue mix from pharma, while operating margin rose from 13.4% to 23.8%, demonstrating significant improvements in cost control and profitability.

- Optimistic Outlook: Management expects full-year revenue between $106.5 million and $110.5 million, with net income projected at $13 million to $16 million, reflecting confidence in achieving the upper end of guidance based on a strong start to the year.

See More

Wix.com Leverages AI Tools to Achieve Revenue Growth

- Significant Revenue Growth: Wix.com reported a 14% year-over-year increase in first-quarter revenue to $541 million, exceeding market expectations and demonstrating resilience amid AI competition, with management forecasting mid-teens growth in revenue and bookings for 2026.

- Share Buyback Strategy: The company repurchased approximately 30% of its outstanding shares in April to counteract a stock price decline of over 10% following the earnings update, indicating management's confidence in the company's long-term value.

- Accelerated AI Innovation: Wix.com recently launched its proprietary LLM, powering its website editor Wix Harmony, showcasing the company's enhanced innovation capabilities in the AI-driven web and app building space.

- Intensifying Market Competition: Despite challenges from AI competitors like Anthropic's Claude Design, Wix.com is striving to maintain market share, with the CEO emphasizing the company's adaptability in a rapidly changing technological landscape.

See More

Paysign Set to Announce Q1 Earnings with Strong Estimates

- Earnings Announcement: Paysign (PAYS) is set to release its Q1 earnings on May 12th after market close, with consensus EPS estimate at $0.07 and revenue estimate at $27.01 million, reflecting a robust 45.2% year-over-year growth.

- Performance Beat: Over the past year, Paysign has exceeded EPS estimates 75% of the time and revenue estimates 100% of the time, indicating a strong track record of reliability and profitability that could bolster investor confidence.

- Estimate Revisions: In the last three months, EPS estimates have seen three upward revisions with no downward adjustments, while revenue estimates have experienced four upward revisions, suggesting increasing analyst confidence in the company's future performance, which may drive stock price appreciation.

- Long-term Growth Target: Paysign has outlined a revenue growth target of 30%-35% for 2026 with ongoing margin expansion, reflecting the company's strategic positioning to capitalize on future market opportunities and providing a positive outlook for investors.

See More

Paysign to Discuss Q1 2026 Earnings on May 12

- Earnings Call Schedule: Paysign, Inc. will discuss its Q1 2026 earnings on May 12, 2026, at 5:00 p.m. Eastern Time, which is expected to provide crucial insights into the company's financial performance that may influence investor decisions.

- Participant Details: U.S. dial-in number is 877.407.2988, and international dial-in is +1.201.389.0923, offering multiple participation options to ensure investors can conveniently access the information.

- Replay Information: The earnings call replay will be available until August 12, 2026, with dial-in numbers 877.660.6853 or +1.201.612.7415, ensuring that investors who cannot participate live can still obtain relevant information.

- Company Overview: Paysign focuses on the intersection of fintech and healthcare, providing patient affordability solutions and donor compensation programs, committed to improving efficiencies, reducing costs, and optimizing payment processing in the life sciences sector.

See More

Surge in Options Trading Volume for Paysign and ASTS

- Options Volume Surge for Paysign: Today, Paysign Inc's options volume reached 4,544 contracts, equivalent to approximately 454,400 shares, representing 89% of its average daily trading volume of 510,355 shares over the past month, indicating strong investor interest in the stock.

- High-Frequency Trading Insight: Notably, the $5 strike call option expiring on April 17, 2026, saw 2,713 contracts traded today, representing about 271,300 shares, suggesting market expectations for future price increases.

- ASTS Options Activity: Concurrently, AST SpaceMobile Inc recorded options trading volume of 114,469 contracts, approximately 11.4 million shares, which is 88.9% of its average daily trading volume of 12.9 million shares over the past month, reflecting sustained market interest in the company.

- Bullish Call Options Trend: Particularly, the $95 strike call option expiring on April 2, 2026, had 7,468 contracts traded today, representing around 746,800 shares, indicating optimistic sentiment among investors regarding ASTS's future performance.

See More