Farewell to Nancy Pelosi's Investment Choices—Discover the Timing and Reasons Behind It

Pelosi's Announcement: Nancy Pelosi has declared she will not seek re-election in 2026, concluding her long tenure in Congress, which began in 1987. She expressed gratitude for her service and confidence in her ability to win another term if she chose to run again.

Impact on Stock Disclosures: With Pelosi's departure, investors will have limited access to her trade disclosures, which have been closely monitored by retail traders. Her trading activities have raised concerns about potential conflicts of interest, particularly regarding stocks related to legislation she has influenced.

Trading Performance: In 2024, Pelosi achieved a 74.9% gain in her stock positions, outperforming the S&P 500, while other members of Congress also reported significant trading gains. This highlights the growing interest in congressional trading activities among investors.

Future of Congressional Trading: Pelosi's exit may shift investor focus to other congressional figures, such as Marjorie Taylor Greene, who has also been active in trading. The landscape of congressional trading, including cryptocurrency investments, may evolve as new candidates emerge.

Trade with 70% Backtested Accuracy

Analyst Views on GOOG

About GOOG

About the author

Wall Street Grows Concern Over Hyperscaler Capital Expenditure

- Surge in Capital Expenditure: In 2024, the combined capital expenditure of the four largest hyperscalers—Amazon, Microsoft, Alphabet, and Meta—exceeded $200 billion, with projections nearing $700 billion by 2026, indicating a strong demand for infrastructure investment in the sector.

- Decline in Free Cash Flow: The free cash flow for these four companies fell to $200 billion last year, down from $237 billion in 2024, highlighting the increasing pressure on financial health due to high spending, raising investor concerns about future profitability.

- Historical Lessons: Historically, AT&T continued to invest in infrastructure during the Great Depression, maintaining a $9 annual dividend despite economic turmoil, a strategy that resonates with modern hyperscalers, although their financial cushions are considerably thinner today.

- Escalating Competitive Risks: Amazon CEO Andy Jassy emphasized that AI represents a “once-in-a-lifetime opportunity,” with hyperscaler capital expenditures now accounting for 2.2% of U.S. GDP, where the risk lies in under-investing to meet future market demands.

Corporate Profits Surge, S&P 500 Hits Record Highs

- Significant Earnings Growth: S&P 500 companies are projected to achieve a 26% year-over-year earnings growth in Q1, surpassing the 12% consensus forecast from April 1, marking the best earnings season since 2021.

- Outperformance: Of the 445 S&P 500 companies that have reported, 64% exceeded both earnings and sales expectations, significantly above the historical average of 42% since 2001, indicating a boost in market confidence.

- Strong Sales Growth: Adjusted for foreign exchange fluctuations and inflation, sales growth is expected to rise by 7%, reflecting companies' resilience and adaptability in the current economic environment, further solidifying investor confidence.

- Complex Economic Outlook: Despite the strong earnings performance in Q1, the economic backdrop remains complicated, with unclear consumer prospects; companies like McDonald's and Planet Fitness indicate weakness among lower-income groups, which could impact future earnings growth.

MNDY Surges on AI-Driven Efficiency Gain

- Earnings Beat: monday.com (MNDY) reported Q1 revenue of $351.3 million, a 24% year-over-year increase that exceeded analyst expectations, showcasing the company's strong performance and growth potential in the market.

- Strategic Shift: Leadership highlighted the transition to consumption-based pricing and the successful rollout of its AI Work Platform as key drivers, which not only enhanced customer satisfaction but also strengthened competitive positioning in the market.

- Operational Leverage: CFO Eliran Glazer noted that internal AI productivity gains allow the company to scale revenue without increasing headcount, indicating a higher operational efficiency achieved in a complex environment.

- Strong Cash Flow: The firm generated over $102 million in adjusted free cash flow, providing substantial capital to further invest in autonomous AI agents, thereby enhancing the sustainability of future growth.

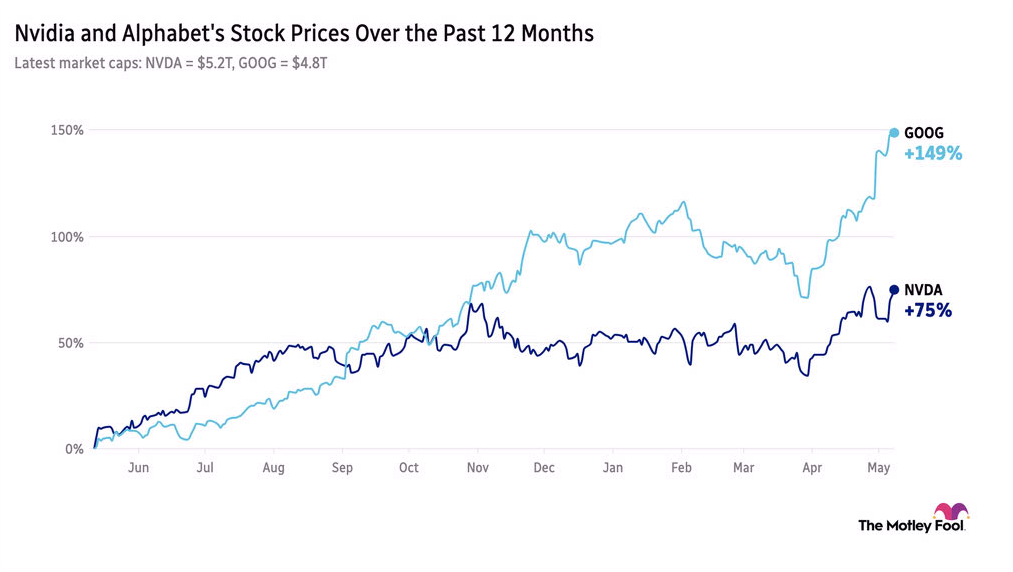

Alphabet's Stock Surge Raises Bubble Concerns

- Alphabet's Stock Surge: Alphabet's stock has surged approximately 150% over the past year, nearly double the rise of current market cap leader Nvidia, indicating its significant role in the AI ecosystem and potential to be the biggest winner in AI.

- Job Data Exceeds Expectations: The addition of 115,000 jobs in April, more than double the expected 53,000, propelled the S&P 500 to a 2.3% weekly gain, showcasing strong economic recovery momentum.

- Impact of Oil Prices on Inflation: The latest Consumer Price Index is expected to rise from 3.3% in March to 3.8%, highlighting the clearer impact of high oil prices on inflation, which may influence future monetary policy decisions.

- Doximity Earnings Report Upcoming: Doximity is set to release its Q4 earnings for fiscal 2025 on Wednesday, with analysts expressing concerns about its ability to fend off AI innovation challenges, reflecting worries about competition in the medical network platform space.

Nvidia and DigitalOcean's AI Market Dynamics

- Nvidia's Market Dominance: Nvidia holds nearly 90% market share in the AI infrastructure sector, and with an annual R&D budget nearing $20 billion and a full-stack strategy, it is projected to see adjusted earnings grow at an annual rate of 53% through fiscal 2028, showcasing its robust competitive edge in AI.

- Upcoming Platform Launch: The upcoming Vera Rubin platform integrates Rubin GPUs and Vera CPUs, achieving up to 35 times more throughput per watt in inference tasks compared to the previous generation Blackwell GPUs, further solidifying Nvidia's leadership position in the market.

- DigitalOcean's Rapid Growth: DigitalOcean's stock has surged 240% in 2023, with the launch of its AI-native cloud service being hailed as the most significant product release in the company's history, and the daily processing of inference tokens is expected to grow tenfold by 2030, indicating strong demand for AI infrastructure.

- Financial Performance and Outlook: DigitalOcean reported a 22% year-over-year revenue increase to $258 million in Q1, and despite a 21% drop in non-GAAP net income due to AI infrastructure spending, management remains optimistic about future revenue growth, forecasting a 26% growth rate in 2026.

Nvidia and DigitalOcean Compete in AI Market

- Nvidia Market Dominance: Nvidia holds nearly 90% market share in the AI infrastructure sector, leveraging an annual R&D budget of nearly $20 billion to drive continuous innovation, with adjusted earnings projected to grow 53% annually through fiscal 2028, underscoring its robust competitive edge in AI.

- DigitalOcean Rapid Growth: DigitalOcean's stock has surged 240% in 2023, with the launch of its AI-Native Cloud platform regarded as the most significant product release in the company's history, expected to substantially enhance its market share among small and medium-sized enterprises amid soaring demand for AI infrastructure.

- Financial Performance Comparison: DigitalOcean reported a 22% year-over-year revenue increase to $258 million in Q1, although its non-GAAP net income fell 21% to $0.44 per share due to significant AI infrastructure spending, yet the company remains optimistic about future revenue growth, forecasting a 26% increase in 2026.

- Market Opportunities and Challenges: With demand for AI inference tokens projected to grow tenfold by 2030, DigitalOcean aims to capitalize on this market opportunity through its AI-Native Cloud platform, while Nvidia faces challenges from custom chip competition, although it maintains a stronghold in AI infrastructure.

Wall Street Grows Concern Over Hyperscaler Capital Expenditure

- Surge in Capital Expenditure: In 2024, the combined capital expenditure of the four largest hyperscalers—Amazon, Microsoft, Alphabet, and Meta—exceeded $200 billion, with projections nearing $700 billion by 2026, indicating a strong demand for infrastructure investment in the sector.

- Decline in Free Cash Flow: The free cash flow for these four companies fell to $200 billion last year, down from $237 billion in 2024, highlighting the increasing pressure on financial health due to high spending, raising investor concerns about future profitability.

- Historical Lessons: Historically, AT&T continued to invest in infrastructure during the Great Depression, maintaining a $9 annual dividend despite economic turmoil, a strategy that resonates with modern hyperscalers, although their financial cushions are considerably thinner today.

- Escalating Competitive Risks: Amazon CEO Andy Jassy emphasized that AI represents a “once-in-a-lifetime opportunity,” with hyperscaler capital expenditures now accounting for 2.2% of U.S. GDP, where the risk lies in under-investing to meet future market demands.

Corporate Profits Surge, S&P 500 Hits Record Highs

- Significant Earnings Growth: S&P 500 companies are projected to achieve a 26% year-over-year earnings growth in Q1, surpassing the 12% consensus forecast from April 1, marking the best earnings season since 2021.

- Outperformance: Of the 445 S&P 500 companies that have reported, 64% exceeded both earnings and sales expectations, significantly above the historical average of 42% since 2001, indicating a boost in market confidence.

- Strong Sales Growth: Adjusted for foreign exchange fluctuations and inflation, sales growth is expected to rise by 7%, reflecting companies' resilience and adaptability in the current economic environment, further solidifying investor confidence.

- Complex Economic Outlook: Despite the strong earnings performance in Q1, the economic backdrop remains complicated, with unclear consumer prospects; companies like McDonald's and Planet Fitness indicate weakness among lower-income groups, which could impact future earnings growth.

MNDY Surges on AI-Driven Efficiency Gain

- Earnings Beat: monday.com (MNDY) reported Q1 revenue of $351.3 million, a 24% year-over-year increase that exceeded analyst expectations, showcasing the company's strong performance and growth potential in the market.

- Strategic Shift: Leadership highlighted the transition to consumption-based pricing and the successful rollout of its AI Work Platform as key drivers, which not only enhanced customer satisfaction but also strengthened competitive positioning in the market.

- Operational Leverage: CFO Eliran Glazer noted that internal AI productivity gains allow the company to scale revenue without increasing headcount, indicating a higher operational efficiency achieved in a complex environment.

- Strong Cash Flow: The firm generated over $102 million in adjusted free cash flow, providing substantial capital to further invest in autonomous AI agents, thereby enhancing the sustainability of future growth.

Alphabet's Stock Surge Raises Bubble Concerns

- Alphabet's Stock Surge: Alphabet's stock has surged approximately 150% over the past year, nearly double the rise of current market cap leader Nvidia, indicating its significant role in the AI ecosystem and potential to be the biggest winner in AI.

- Job Data Exceeds Expectations: The addition of 115,000 jobs in April, more than double the expected 53,000, propelled the S&P 500 to a 2.3% weekly gain, showcasing strong economic recovery momentum.

- Impact of Oil Prices on Inflation: The latest Consumer Price Index is expected to rise from 3.3% in March to 3.8%, highlighting the clearer impact of high oil prices on inflation, which may influence future monetary policy decisions.

- Doximity Earnings Report Upcoming: Doximity is set to release its Q4 earnings for fiscal 2025 on Wednesday, with analysts expressing concerns about its ability to fend off AI innovation challenges, reflecting worries about competition in the medical network platform space.

Nvidia and DigitalOcean's AI Market Dynamics

- Nvidia's Market Dominance: Nvidia holds nearly 90% market share in the AI infrastructure sector, and with an annual R&D budget nearing $20 billion and a full-stack strategy, it is projected to see adjusted earnings grow at an annual rate of 53% through fiscal 2028, showcasing its robust competitive edge in AI.

- Upcoming Platform Launch: The upcoming Vera Rubin platform integrates Rubin GPUs and Vera CPUs, achieving up to 35 times more throughput per watt in inference tasks compared to the previous generation Blackwell GPUs, further solidifying Nvidia's leadership position in the market.

- DigitalOcean's Rapid Growth: DigitalOcean's stock has surged 240% in 2023, with the launch of its AI-native cloud service being hailed as the most significant product release in the company's history, and the daily processing of inference tokens is expected to grow tenfold by 2030, indicating strong demand for AI infrastructure.

- Financial Performance and Outlook: DigitalOcean reported a 22% year-over-year revenue increase to $258 million in Q1, and despite a 21% drop in non-GAAP net income due to AI infrastructure spending, management remains optimistic about future revenue growth, forecasting a 26% growth rate in 2026.

Nvidia and DigitalOcean Compete in AI Market

- Nvidia Market Dominance: Nvidia holds nearly 90% market share in the AI infrastructure sector, leveraging an annual R&D budget of nearly $20 billion to drive continuous innovation, with adjusted earnings projected to grow 53% annually through fiscal 2028, underscoring its robust competitive edge in AI.

- DigitalOcean Rapid Growth: DigitalOcean's stock has surged 240% in 2023, with the launch of its AI-Native Cloud platform regarded as the most significant product release in the company's history, expected to substantially enhance its market share among small and medium-sized enterprises amid soaring demand for AI infrastructure.

- Financial Performance Comparison: DigitalOcean reported a 22% year-over-year revenue increase to $258 million in Q1, although its non-GAAP net income fell 21% to $0.44 per share due to significant AI infrastructure spending, yet the company remains optimistic about future revenue growth, forecasting a 26% increase in 2026.

- Market Opportunities and Challenges: With demand for AI inference tokens projected to grow tenfold by 2030, DigitalOcean aims to capitalize on this market opportunity through its AI-Native Cloud platform, while Nvidia faces challenges from custom chip competition, although it maintains a stronghold in AI infrastructure.