Cellebrite Acquires Corellium for $170 Million, Enhancing Digital Investigation Capabilities

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Dec 02 2025

0mins

Source: Newsfilter

- Acquisition Expansion: Cellebrite has acquired Corellium for $170 million, with $150 million paid in cash, significantly enhancing its technological leadership in the digital investigation space, thereby improving its competitive position in the market.

- Technology Integration: Corellium's virtualization software enables investigators to work without physical device constraints, dramatically accelerating evidence acquisition and threat detection, which meets defense and intelligence customers' needs for secure mobile application development.

- Customer Value Enhancement: By integrating Corellium's technology, Cellebrite can provide enterprise development and security operations teams with more efficient design and validation capabilities for next-generation mobile applications, thereby increasing customer satisfaction and market share.

- Leadership Change: Corellium co-founder Chris Wade has joined Cellebrite as Chief Technology Officer, which is expected to drive customer-focused innovation and further enhance the company's technological strength and market influence.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CLBT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CLBT

Wall Street analysts forecast CLBT stock price to rise

7 Analyst Rating

7 Buy

0 Hold

0 Sell

Strong Buy

Current: 13.200

Low

23.00

Averages

24.83

High

28.00

Current: 13.200

Low

23.00

Averages

24.83

High

28.00

About CLBT

Cellebrite DI Ltd is an Israel-based company engaged primarily in the software sector. The Company is committed to providing a Digital Intelligence (DI) platform for managing DI in legally sanctioned investigations. The Company provides solutions for the public and private sectors, enabling organizations in mastering the complexities of legally sanctioned digital investigations by streamlining intelligence processes. The Company's platform and solutions transform how customers collect, review, analyze and manage data in legally sanctioned investigations. The Company aims to enable its customers to protect and save lives, accelerate justice, and preserve privacy in communities around the world.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Wall Street's Latest Rating Changes Overview

- Openlane Upgrade: JPMorgan upgraded Openlane from neutral to overweight and raised its December 2026 price target to $38, indicating that the online used car marketplace is experiencing robust growth and has potential for sustainable expansion over the coming years.

- Dollar General Downgrade: Deutsche Bank downgraded Dollar General from buy to hold, citing challenges in its customer base and the widening gap in the K-shaped economy, which may limit same-store sales upside, reflecting a cautious outlook on the company.

- Ecolab Upgrade: UBS upgraded Ecolab from neutral to buy and raised its price target to $325, demonstrating strong demand and positive performance expectations for the chemicals company amid a favorable market environment.

- FedEx Upgrade: JPMorgan upgraded FedEx from neutral to overweight, expressing optimism ahead of its upcoming earnings report, particularly regarding the separation of its freight business, which is seen as an attractive risk-reward opportunity.

See More

Cellebrite Exceeds Q1 2026 Earnings Expectations

- Annual Recurring Revenue Growth: Cellebrite's annual recurring revenue (ARR) increased by 21% year-over-year to $493 million, exceeding expectations and demonstrating the company's strong market performance and sustained customer demand.

- Significant EBITDA Improvement: The adjusted EBITDA for Q1 reached $30.6 million, a 29% increase from the previous year, reflecting the company's success in cost control and operational efficiency, which further boosts investor confidence.

- Market Potential of AI Solution Genesis: Following the launch of the next-gen AI solution Genesis, Cellebrite registered over 500 users within eight weeks, which is expected to drive future revenue growth and could tap into a $12.5 billion market opportunity over the next four years.

- New Opportunities from Federal Authorization: Cellebrite announced on May 6 that it received FedRAMP high authorization, which is expected to provide a unique advantage for the company's expansion into the U.S. federal market, supporting revenue growth in the coming quarters.

See More

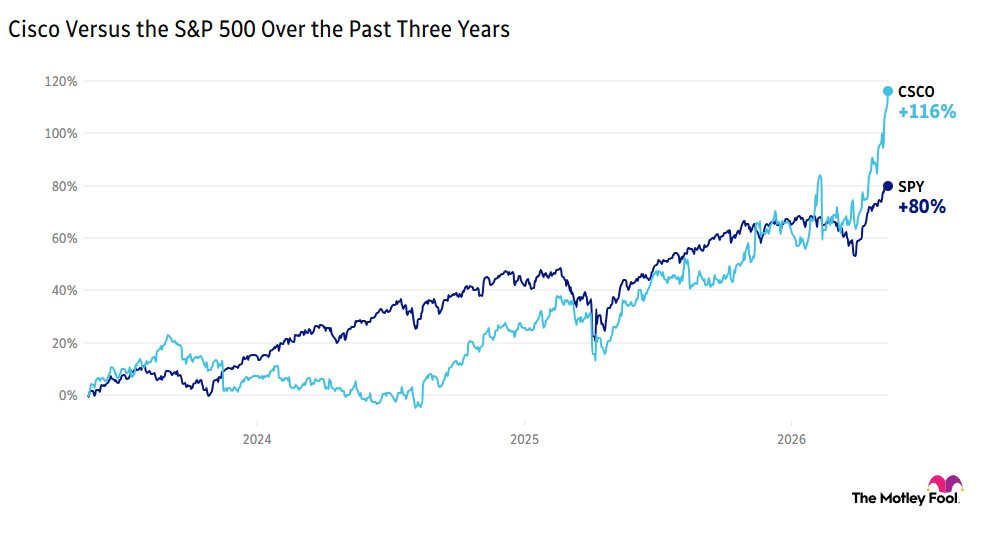

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

Cellebrite Reports 21% ARR Growth in Q1 2026

- Strong Financial Performance: Cellebrite reported Q1 2026 revenue of $128.3 million, a 19.2% year-over-year increase, reflecting robust demand for its digital investigative solutions and reinforcing its market leadership.

- Accelerated ARR Growth: The company achieved an annual recurring revenue (ARR) of $510 million to $513 million in Q1, with a year-over-year growth rate of 22% to 23%, indicating a sustained increase in customer demand following the launch of new products.

- Free Cash Flow Performance: The first quarter saw a free cash flow of $16.8 million, with a free cash flow margin of 13.1%, demonstrating the company's ability to generate cash from operations, despite a decline from the previous year, supporting future strategic investments.

- Positive Future Outlook: Cellebrite anticipates Q2 2026 revenue between $130 million and $133 million, with a growth rate of 15% to 17%, suggesting optimism regarding market response to new products and a commitment to driving future growth through continuous innovation.

See More

Cellebrite Q1 Earnings Exceed Expectations

- Strong Earnings Report: Cellebrite's Q1 non-GAAP EPS of $0.12 surpassed expectations by $0.03, indicating a sustained enhancement in profitability that reinforces market confidence in future growth.

- Significant Revenue Growth: The company reported Q1 revenue of $128.3 million, a 19.3% year-over-year increase, exceeding market expectations by $1.27 million, reflecting a robust demand in the digital forensics sector that drives overall performance.

- Robust Subscription Revenue: Subscription revenue reached $117.9 million, up 23% year-over-year, showcasing significant progress in establishing a stable revenue stream, which enhances long-term financial stability.

- Optimistic Future Outlook: The company anticipates Q2 2026 annual recurring revenue to be between $510 million and $513 million, with an annual growth rate of 22% to 23%, demonstrating management's confidence in future performance, potentially attracting more investor interest.

See More

Cellebrite to Announce Q1 Earnings on May 14

- Earnings Announcement: Cellebrite (CLBT) is set to announce its Q1 2023 earnings on May 14 before the market opens, with a consensus EPS estimate of $0.09, reflecting a 10% year-over-year decline, which may impact investor sentiment.

- Revenue Expectations: Analysts forecast revenue of $127.03 million, representing an 18.2% year-over-year increase, indicating the company's growth potential in the market despite the decline in EPS expectations.

- Performance Track Record: Over the past two years, Cellebrite has exceeded EPS estimates 100% of the time and revenue estimates 88% of the time, showcasing the company's financial stability and reliability, which could bolster investor confidence.

- Estimate Revision Trends: In the last three months, EPS estimates have seen no upward revisions and three downward revisions, while revenue estimates experienced two upward and two downward revisions, reflecting a cautious market outlook on the company's future performance.

See More

Wall Street's Latest Rating Changes Overview

- Openlane Upgrade: JPMorgan upgraded Openlane from neutral to overweight and raised its December 2026 price target to $38, indicating that the online used car marketplace is experiencing robust growth and has potential for sustainable expansion over the coming years.

- Dollar General Downgrade: Deutsche Bank downgraded Dollar General from buy to hold, citing challenges in its customer base and the widening gap in the K-shaped economy, which may limit same-store sales upside, reflecting a cautious outlook on the company.

- Ecolab Upgrade: UBS upgraded Ecolab from neutral to buy and raised its price target to $325, demonstrating strong demand and positive performance expectations for the chemicals company amid a favorable market environment.

- FedEx Upgrade: JPMorgan upgraded FedEx from neutral to overweight, expressing optimism ahead of its upcoming earnings report, particularly regarding the separation of its freight business, which is seen as an attractive risk-reward opportunity.

See More

Cellebrite Exceeds Q1 2026 Earnings Expectations

- Annual Recurring Revenue Growth: Cellebrite's annual recurring revenue (ARR) increased by 21% year-over-year to $493 million, exceeding expectations and demonstrating the company's strong market performance and sustained customer demand.

- Significant EBITDA Improvement: The adjusted EBITDA for Q1 reached $30.6 million, a 29% increase from the previous year, reflecting the company's success in cost control and operational efficiency, which further boosts investor confidence.

- Market Potential of AI Solution Genesis: Following the launch of the next-gen AI solution Genesis, Cellebrite registered over 500 users within eight weeks, which is expected to drive future revenue growth and could tap into a $12.5 billion market opportunity over the next four years.

- New Opportunities from Federal Authorization: Cellebrite announced on May 6 that it received FedRAMP high authorization, which is expected to provide a unique advantage for the company's expansion into the U.S. federal market, supporting revenue growth in the coming quarters.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

Cellebrite Reports 21% ARR Growth in Q1 2026

- Strong Financial Performance: Cellebrite reported Q1 2026 revenue of $128.3 million, a 19.2% year-over-year increase, reflecting robust demand for its digital investigative solutions and reinforcing its market leadership.

- Accelerated ARR Growth: The company achieved an annual recurring revenue (ARR) of $510 million to $513 million in Q1, with a year-over-year growth rate of 22% to 23%, indicating a sustained increase in customer demand following the launch of new products.

- Free Cash Flow Performance: The first quarter saw a free cash flow of $16.8 million, with a free cash flow margin of 13.1%, demonstrating the company's ability to generate cash from operations, despite a decline from the previous year, supporting future strategic investments.

- Positive Future Outlook: Cellebrite anticipates Q2 2026 revenue between $130 million and $133 million, with a growth rate of 15% to 17%, suggesting optimism regarding market response to new products and a commitment to driving future growth through continuous innovation.

See More

Cellebrite Q1 Earnings Exceed Expectations

- Strong Earnings Report: Cellebrite's Q1 non-GAAP EPS of $0.12 surpassed expectations by $0.03, indicating a sustained enhancement in profitability that reinforces market confidence in future growth.

- Significant Revenue Growth: The company reported Q1 revenue of $128.3 million, a 19.3% year-over-year increase, exceeding market expectations by $1.27 million, reflecting a robust demand in the digital forensics sector that drives overall performance.

- Robust Subscription Revenue: Subscription revenue reached $117.9 million, up 23% year-over-year, showcasing significant progress in establishing a stable revenue stream, which enhances long-term financial stability.

- Optimistic Future Outlook: The company anticipates Q2 2026 annual recurring revenue to be between $510 million and $513 million, with an annual growth rate of 22% to 23%, demonstrating management's confidence in future performance, potentially attracting more investor interest.

See More

Cellebrite to Announce Q1 Earnings on May 14

- Earnings Announcement: Cellebrite (CLBT) is set to announce its Q1 2023 earnings on May 14 before the market opens, with a consensus EPS estimate of $0.09, reflecting a 10% year-over-year decline, which may impact investor sentiment.

- Revenue Expectations: Analysts forecast revenue of $127.03 million, representing an 18.2% year-over-year increase, indicating the company's growth potential in the market despite the decline in EPS expectations.

- Performance Track Record: Over the past two years, Cellebrite has exceeded EPS estimates 100% of the time and revenue estimates 88% of the time, showcasing the company's financial stability and reliability, which could bolster investor confidence.

- Estimate Revision Trends: In the last three months, EPS estimates have seen no upward revisions and three downward revisions, while revenue estimates experienced two upward and two downward revisions, reflecting a cautious market outlook on the company's future performance.

See More