2026 Optimism Relies on Productivity — These Future-of-Work ETFs Offer the Best Investment Opportunity

Wall Street's Optimism for 2026: Major firms like JPMorgan, HSBC, and Deutsche Bank predict that the next market surge will be driven by productivity gains from AI and automation, essential for justifying high S&P 500 targets of 7,500–8,000.

Future-of-Work ETFs: A new category of ETFs is emerging, focusing on real-world applications of AI and automation, which are expected to deliver significant earnings growth. These include funds like iShares Exponential Technologies ETF and ROBO Global Robotics and Automation Index ETF.

Key ETFs for Productivity Gains: The article highlights specific ETFs that capture the productivity boom, such as KOMP and SIMS, which invest in companies driving digital transformation and smart infrastructure, respectively.

The Bottom Line: If Wall Street's bullish forecasts materialize, it will be due to tangible efficiency improvements from AI and automation, rather than mere belief in the technology, making future-of-work ETFs a viable investment strategy amidst market volatility.

Trade with 70% Backtested Accuracy

Analyst Views on META

About META

About the author

Meta Plans to Rent Out AI Computing Capacity

- AI Infrastructure Expansion: Meta Platforms has aggressively built AI infrastructure over the past few years, particularly for training its Llama models, with capital expenditures expected to exceed $145 billion in 2026, indicating the company's ongoing investment and growth potential in the AI sector.

- New Revenue Stream: Meta may create a new revenue stream by renting out its excess computing capacity, a strategy similar to SpaceX's successful model, which could generate over $2 billion in monthly revenue, highlighting the profitability potential of this market.

- User Growth Challenges: Despite attracting over 3.5 billion users daily across its social media apps, Meta is addressing stagnant advertising growth by enhancing user engagement through AI, which helps increase ad revenue and mitigates growth stagnation in its advertising business.

- Attractive Market Valuation: With a current P/E ratio of 21.2, which is 25% lower than its 10-year average, Meta's stock appears undervalued, suggesting that investors may consider long-term investment despite uncertainties surrounding its potential cloud business.

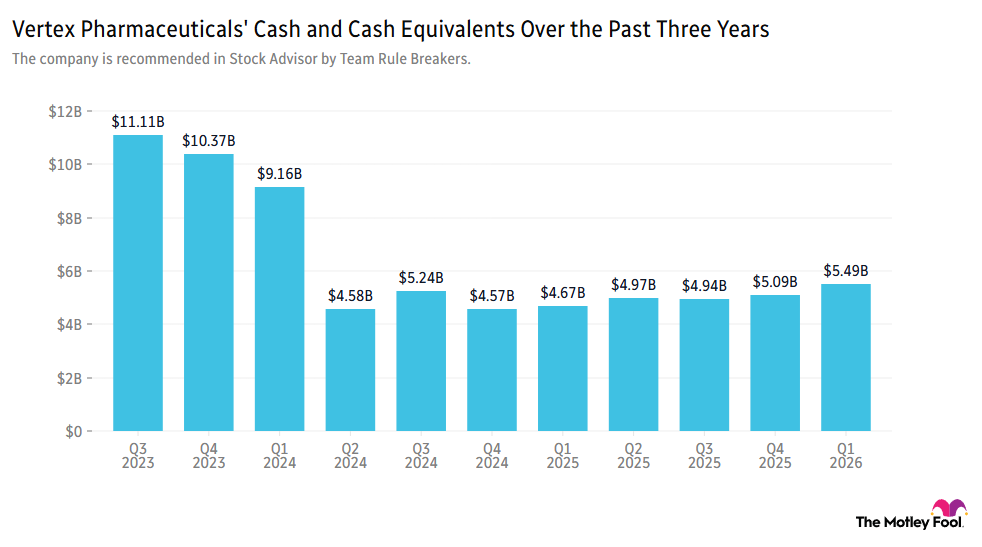

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

SpaceX IPO Sets Record but Faces Challenges Ahead

- Record IPO Financing: SpaceX raised $85.7 billion in its IPO, nearly tripling Saudi Aramco's previous record of $29.4 billion, demonstrating strong market confidence in its AI and space infrastructure ventures.

- Significant Valuation Fluctuations: Although SpaceX's valuation approached $3 trillion post-IPO, it has since retraced to $2.13 trillion as of July 2, with a share price still 20% above its IPO listing, reflecting cautious market sentiment regarding its future performance.

- Complex Lockup Period: SpaceX sold only about 5% of its outstanding shares in its IPO, with the float expected to increase rapidly in the coming months as insiders become eligible to sell, potentially exerting downward pressure on the stock price.

- High Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical average of 30, SpaceX's stock faces substantial correction risks, particularly amid fluctuating market emotions and investor sentiment.

Meta's Plans to Compete in Cloud Computing Market Impact Neocloud Providers

- Stock Price Volatility: Following news of Meta's plans to enter the cloud computing market, CoreWeave's stock plummeted nearly 14% in a single day, while Nebius dropped 17%, reflecting market concerns about the future prospects of both companies, especially with Meta as a customer.

- Massive Contract Expansion: CoreWeave expanded its agreement with Meta in April 2023 to provide cloud computing capacity through 2032, valued at $21 billion, while Nebius announced in March it would provide $12 billion in cloud capacity, showcasing the strong collaborative potential in the AI data center sector.

- Sustained Demand Growth: Despite the competitive threat from Meta, demand for AI data centers from CoreWeave and Nebius remains robust, with CoreWeave noting that its 2026 capacity is largely sold out and 30% of its $99.4 billion revenue backlog comes from foundational AI labs, indicating urgent market demand for their services.

- Investment Opportunity Emerges: Although Meta's plans could impact CoreWeave and Nebius, the demand for AI data centers far exceeds supply, making the current stock price pullback a buying opportunity, particularly as CoreWeave's price-to-sales ratio is only 6.6, indicating potential investment value.

SpaceX IPO Raises Record $85.7 Billion

- Record IPO Financing: SpaceX's IPO on June 12 raised an unprecedented $85.7 billion, nearly tripling Saudi Aramco's previous record of $29.4 billion, indicating strong market confidence in its future potential.

- Market Performance Volatility: Although the company's market cap briefly approached $3 trillion post-IPO, it retraced to $2.13 trillion by July 2, with a share price still 20% above the IPO price, reflecting investor caution regarding long-term performance.

- Lockup Period Challenges: SpaceX's staggered lockup schedule allowed only about 5% of shares to be sold initially, with a significant number of insiders expected to sell their shares in the coming months, which could exert downward pressure on the stock price.

- Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical threshold of 30, SpaceX faces substantial challenges in sustaining profitability, leading to market expectations that its stock price may fall below $100 before the end of 2026.

Meta Enters AI Data Center Market, Impact on CoreWeave and Nebius

- Increased Competition: Meta's plan to enter the AI data center market led to a 14% and 17% drop in CoreWeave and Nebius shares respectively, indicating market concerns over new competition that could impact future revenue growth for both companies.

- Shifting Customer Dynamics: CoreWeave's agreement with Meta has been extended to 2032, valued at $21 billion, while Nebius has committed to providing $12 billion in cloud computing capacity, highlighting the importance of their business relationships despite increased competition.

- Strong Demand Continues: CoreWeave's AI cloud platform demand is nearing saturation for 2026, with 30% of its $99.4 billion revenue backlog coming from foundational AI labs, showcasing its robust market position and growth potential.

- Optimistic Industry Outlook: According to Goldman Sachs, U.S. data center power demand is projected to double to 66GW by 2027, indicating that the demand for AI data centers will continue to grow, positioning CoreWeave and Nebius to benefit from this trend.

Meta Plans to Rent Out AI Computing Capacity

- AI Infrastructure Expansion: Meta Platforms has aggressively built AI infrastructure over the past few years, particularly for training its Llama models, with capital expenditures expected to exceed $145 billion in 2026, indicating the company's ongoing investment and growth potential in the AI sector.

- New Revenue Stream: Meta may create a new revenue stream by renting out its excess computing capacity, a strategy similar to SpaceX's successful model, which could generate over $2 billion in monthly revenue, highlighting the profitability potential of this market.

- User Growth Challenges: Despite attracting over 3.5 billion users daily across its social media apps, Meta is addressing stagnant advertising growth by enhancing user engagement through AI, which helps increase ad revenue and mitigates growth stagnation in its advertising business.

- Attractive Market Valuation: With a current P/E ratio of 21.2, which is 25% lower than its 10-year average, Meta's stock appears undervalued, suggesting that investors may consider long-term investment despite uncertainties surrounding its potential cloud business.

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

SpaceX IPO Sets Record but Faces Challenges Ahead

- Record IPO Financing: SpaceX raised $85.7 billion in its IPO, nearly tripling Saudi Aramco's previous record of $29.4 billion, demonstrating strong market confidence in its AI and space infrastructure ventures.

- Significant Valuation Fluctuations: Although SpaceX's valuation approached $3 trillion post-IPO, it has since retraced to $2.13 trillion as of July 2, with a share price still 20% above its IPO listing, reflecting cautious market sentiment regarding its future performance.

- Complex Lockup Period: SpaceX sold only about 5% of its outstanding shares in its IPO, with the float expected to increase rapidly in the coming months as insiders become eligible to sell, potentially exerting downward pressure on the stock price.

- High Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical average of 30, SpaceX's stock faces substantial correction risks, particularly amid fluctuating market emotions and investor sentiment.

Meta's Plans to Compete in Cloud Computing Market Impact Neocloud Providers

- Stock Price Volatility: Following news of Meta's plans to enter the cloud computing market, CoreWeave's stock plummeted nearly 14% in a single day, while Nebius dropped 17%, reflecting market concerns about the future prospects of both companies, especially with Meta as a customer.

- Massive Contract Expansion: CoreWeave expanded its agreement with Meta in April 2023 to provide cloud computing capacity through 2032, valued at $21 billion, while Nebius announced in March it would provide $12 billion in cloud capacity, showcasing the strong collaborative potential in the AI data center sector.

- Sustained Demand Growth: Despite the competitive threat from Meta, demand for AI data centers from CoreWeave and Nebius remains robust, with CoreWeave noting that its 2026 capacity is largely sold out and 30% of its $99.4 billion revenue backlog comes from foundational AI labs, indicating urgent market demand for their services.

- Investment Opportunity Emerges: Although Meta's plans could impact CoreWeave and Nebius, the demand for AI data centers far exceeds supply, making the current stock price pullback a buying opportunity, particularly as CoreWeave's price-to-sales ratio is only 6.6, indicating potential investment value.

SpaceX IPO Raises Record $85.7 Billion

- Record IPO Financing: SpaceX's IPO on June 12 raised an unprecedented $85.7 billion, nearly tripling Saudi Aramco's previous record of $29.4 billion, indicating strong market confidence in its future potential.

- Market Performance Volatility: Although the company's market cap briefly approached $3 trillion post-IPO, it retraced to $2.13 trillion by July 2, with a share price still 20% above the IPO price, reflecting investor caution regarding long-term performance.

- Lockup Period Challenges: SpaceX's staggered lockup schedule allowed only about 5% of shares to be sold initially, with a significant number of insiders expected to sell their shares in the coming months, which could exert downward pressure on the stock price.

- Valuation Risks: With a current price-to-sales ratio of 114, significantly above the historical threshold of 30, SpaceX faces substantial challenges in sustaining profitability, leading to market expectations that its stock price may fall below $100 before the end of 2026.

Meta Enters AI Data Center Market, Impact on CoreWeave and Nebius

- Increased Competition: Meta's plan to enter the AI data center market led to a 14% and 17% drop in CoreWeave and Nebius shares respectively, indicating market concerns over new competition that could impact future revenue growth for both companies.

- Shifting Customer Dynamics: CoreWeave's agreement with Meta has been extended to 2032, valued at $21 billion, while Nebius has committed to providing $12 billion in cloud computing capacity, highlighting the importance of their business relationships despite increased competition.

- Strong Demand Continues: CoreWeave's AI cloud platform demand is nearing saturation for 2026, with 30% of its $99.4 billion revenue backlog coming from foundational AI labs, showcasing its robust market position and growth potential.

- Optimistic Industry Outlook: According to Goldman Sachs, U.S. data center power demand is projected to double to 66GW by 2027, indicating that the demand for AI data centers will continue to grow, positioning CoreWeave and Nebius to benefit from this trend.