Key Takeaway

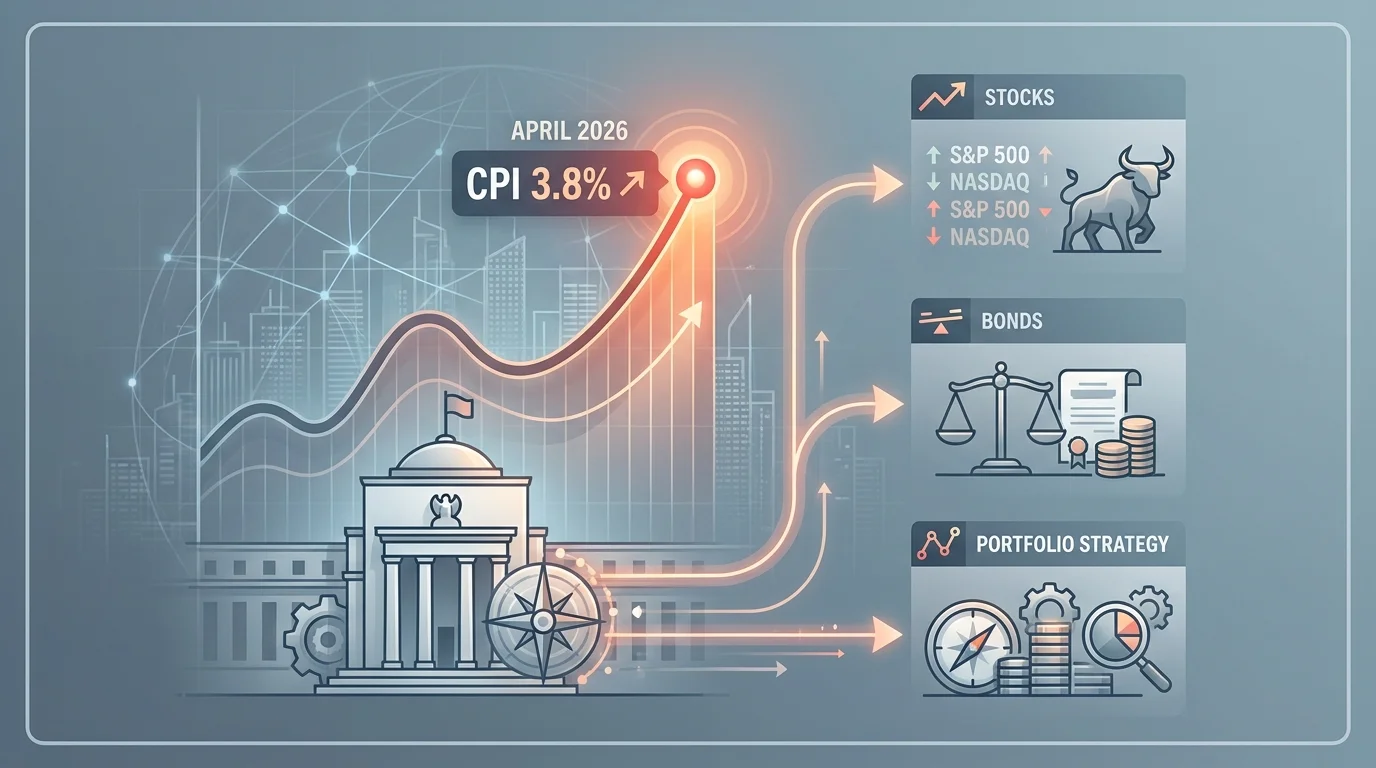

The U.S. Consumer Price Index (CPI) surged to 3.8% year-over-year in April 2026, significantly exceeding market expectations and marking a sharp acceleration from March's 3.3% reading. This hotter-than-expected inflation print, driven primarily by spiking energy costs due to the ongoing conflict in Iran, has fundamentally shifted market expectations for Federal Reserve monetary policy. Investors who had been positioning for potential rate cuts later this year are now recalibrating for a prolonged period of elevated interest rates, with markets pricing in a nearly 98% probability that the Fed will hold rates steady at 3.5%-3.75% through most of 2026.

The implications extend far beyond the bond market. Higher-for-longer rates are already rippling through equities, particularly rate-sensitive growth sectors and small-cap stocks, while simultaneously strengthening the U.S. dollar and pressuring commodity prices outside of energy. For investors, this environment demands a strategic pivot toward quality factors, defensive positioning, and careful attention to duration risk across fixed income portfolios. Understanding how sticky inflation interacts with Fed policy will be critical for portfolio performance in the months ahead.

Breaking Down the April 2026 CPI Report

The Bureau of Labor Statistics released the April 2026 CPI report on May 12, revealing inflation pressures that caught markets off guard. The headline CPI increased 0.8% on a non-seasonally adjusted basis for the month, pushing the annual inflation rate to 3.8%—the highest level seen in nearly three years and well above the Federal Reserve's 2% target. Core CPI, which excludes volatile food and energy components, also came in hotter than anticipated, indicating that inflationary pressures have broadened beyond just energy costs.

Energy prices emerged as the primary driver of the acceleration, with crude oil surging amid escalating tensions in the Middle East. The Iran war has disrupted supply chains and created significant uncertainty in global energy markets, pushing gasoline and heating costs higher for American consumers. However, what concerns policymakers most is the persistence of inflation across services sectors and shelter costs, which tend to be stickier and more resistant to rapid decline. The combination of supply-driven energy inflation and demand-driven services inflation creates a challenging environment for the Federal Reserve.

When analyzing the monthly components, food prices continued their modest upward trajectory, while transportation costs excluding energy showed mixed signals. Housing costs, which comprise a significant weighting in the CPI basket, remain elevated despite some cooling in the housing market. This broad-based inflation suggests that price pressures have become entrenched in the economy, making the Fed's job considerably more difficult than if inflation were concentrated in just one or two categories.

Federal Reserve Policy Response and Market Expectations

The hotter CPI print has triggered a dramatic repricing of Federal Reserve policy expectations across financial markets. According to CME FedWatch data, markets are now pricing in nearly 98% odds that the Federal Open Market Committee will hold the federal funds rate steady at its current 3.5%-3.75% target range through the June meeting and potentially through the remainder of 2026. This represents a sharp pivot from earlier expectations that had been building for rate cuts as early as the third quarter.

Fed Chair Jerome Powell and other FOMC members have consistently emphasized their data-dependent approach to monetary policy, and the April CPI data provides little justification for monetary easing. With inflation running nearly twice the Fed's target rate, any discussion of rate cuts has been pushed to the back burner. Some hawkish commentators have even begun speculating about the possibility of additional rate hikes if inflation fails to show meaningful progress toward 2% in the coming months.

The Treasury yield curve has steepened in response to the inflation data, with longer-dated yields rising more than short-term rates. The 10-year Treasury yield has climbed back above 4.5%, reflecting both inflation expectations and term premium demands from investors. This bear steepening of the curve historically signals concerns about persistent inflation and higher rates over the medium term.

For fixed income investors, this environment presents both challenges and opportunities. While existing bond holdings have experienced mark-to-market losses as yields rise, new investments can capture higher income streams. The key consideration is duration management—shorter-duration bonds and floating-rate instruments offer protection against further rate increases, while longer-duration securities could face additional pressure if the Fed maintains its hawkish stance longer than currently anticipated.

Stock Market Impact: Winners and Losers

Equity markets have responded to the inflation data with increased volatility and notable sector rotation. The Russell 2000 small-cap index, which is more sensitive to interest rate changes due to its higher proportion of financially leveraged companies, experienced sharper declines than large-cap indices. Small-cap firms typically carry more floating-rate debt and have less pricing power to pass along increased costs to customers, making them particularly vulnerable in a higher-rate environment.

Growth stocks, especially in the technology sector, have also faced pressure as higher discount rates reduce the present value of future earnings. Companies trading at elevated valuation multiples based on projected profits five to ten years out see those valuations compress when rates rise. This dynamic particularly affects unprofitable tech companies and those in emerging sectors like electric vehicles and renewable energy, where profitability remains further out on the horizon.

Conversely, financial stocks have generally benefited from higher rates, as the spread between what banks pay on deposits and what they charge on loans widens. Insurance companies also tend to perform better in rising rate environments because they can reinvest premiums at higher yields. Value stocks with strong cash flows and pricing power have demonstrated resilience, as have defensive sectors like consumer staples and utilities that provide essential services regardless of economic conditions.

Energy Markets and Inflation Transmission

The Iran conflict has become a central factor in the inflation narrative, with crude oil prices surging and creating second-order effects throughout the economy. Energy costs feed into virtually every sector through transportation, manufacturing, and heating expenses, making oil price spikes particularly pernicious for inflation control. The strategic petroleum reserve releases that had been used to manage prices in previous years have depleted reserves, limiting the government's ability to respond to supply shocks.

Gasoline prices at the pump have become a visible symbol of inflation for consumers, affecting both household budgets and consumer sentiment. When drivers see higher prices every time they fill up, inflation expectations become unanchored, creating a feedback loop where workers demand higher wages and businesses raise prices preemptively. This wage-price spiral is precisely what the Federal Reserve fears most, as it can sustain inflation long after the initial supply shock subsides.

Beyond the immediate energy impact, the conflict has created uncertainty in shipping lanes and global trade routes, particularly through the Strait of Hormuz. Any disruption to this critical chokepoint could send oil prices significantly higher, adding further fuel to inflationary pressures. Investors need to monitor geopolitical developments closely, as the trajectory of energy markets will heavily influence both inflation outcomes and Fed policy responses in the coming quarters.

Sector Analysis: Positioning for Higher-for-Longer Rates

Different sectors of the economy respond distinctly to sustained higher interest rates, and understanding these dynamics is essential for portfolio positioning. The real estate sector faces obvious headwinds, as mortgage rates above 7% have dramatically reduced affordability for homebuyers and pressured commercial real estate valuations. Real Estate Investment Trusts (REITs) with significant leverage or shorter debt maturities are particularly at risk.

The consumer discretionary sector is experiencing a bifurcation between high-end and budget-oriented retailers. Luxury brands serving wealthy consumers have maintained resilience, as this demographic is less affected by interest rate changes. However, mid-market retailers serving middle-class households with mortgages and credit card debt are seeing demand soften as disposable income gets squeezed by higher borrowing costs.

Healthcare and pharmaceuticals offer defensive characteristics that become more attractive in uncertain economic environments. These sectors tend to have recession-resistant demand, strong pricing power, and many companies carry less debt relative to their cash flows. Additionally, the aging demographics in developed markets provide structural tailwinds regardless of the interest rate environment.

Industrial companies with pricing power and exposure to infrastructure spending have demonstrated resilience, though those with significant international operations face headwinds from the stronger U.S. dollar. The Inflation Reduction Act and Infrastructure Investment and Jobs Act continue to drive federal spending in these areas, providing some offset to higher financing costs.

International Implications and Currency Markets

The divergence between U.S. inflation and monetary policy compared to other major economies has significant implications for currency markets and international investments. The U.S. dollar has strengthened against most major currencies as interest rate differentials widen in America's favor. This dollar strength creates headwinds for U.S. multinationals by making American exports more expensive and reducing the value of overseas earnings when converted back to dollars.

Emerging markets face particular challenges from a stronger dollar and higher U.S. rates. Many developing economies carry dollar-denominated debt, which becomes more expensive to service when the greenback appreciates. Additionally, higher U.S. yields attract capital flows away from emerging markets, putting pressure on their currencies and forcing their central banks to raise rates to defend exchange rates, even when their domestic economies may not warrant tighter policy.

European and Japanese markets, dealing with their own inflation challenges but responding with different monetary policy approaches, present opportunities for investors willing to navigate currency risk. The European Central Bank and Bank of Japan have been more cautious in their rate hiking cycles, creating potential valuation opportunities in their equity markets relative to the U.S., though currency hedging becomes an important consideration.

Investment Strategies for the Current Environment

Navigating a higher-for-longer rate environment requires adjustments to traditional portfolio construction. Cash and cash equivalents have become genuinely competitive asset classes for the first time in years, with money market funds and short-term Treasury bills offering yields above 5% with minimal duration risk. Investors should consider maintaining higher cash allocations both for yield and for opportunistic deployment during market dislocations.

Within fixed income, a barbell strategy combining very short-duration securities with longer-duration high-quality bonds can provide income while managing interest rate risk. Credit quality matters more when rates are elevated, as refinancing becomes more expensive for lower-rated issuers. Investment-grade corporate bonds and agency mortgage-backed securities offer attractive risk-adjusted yields for investors willing to extend modestly in duration.

Equity investors should emphasize quality factors including strong balance sheets, consistent cash flows, and pricing power. Companies with competitive moats that can pass along cost increases to customers will fare better than those operating on thin margins in competitive markets. Dividend growth stocks, particularly those with long histories of increasing payouts, historically outperform in higher inflation environments.

Alternative investments including private credit, infrastructure, and real assets can provide diversification benefits and inflation protection. These asset classes often have floating-rate characteristics or explicit inflation linkages in their contracts. However, liquidity considerations become more important in uncertain environments, and investors should ensure they maintain adequate liquid reserves.

The Path Forward: Scenarios to Watch

Several scenarios could unfold from the current inflationary environment, and investors should prepare for multiple possibilities rather than betting on a single outcome. The base case assumes the Fed successfully engineers a soft landing, with inflation gradually declining toward target over the next 12-18 months without triggering a recession. In this scenario, quality stocks and intermediate-duration bonds would likely perform well.

A more bearish scenario involves inflation remaining persistently elevated, forcing the Fed to raise rates further and eventually triggering an economic downturn. This stagflationary environment would be challenging for both stocks and bonds, favoring commodities, cash, and potentially defensive equities with pricing power. Gold and other precious metals historically perform well in stagflation scenarios.

The optimistic scenario would see energy prices moderating as geopolitical tensions ease, allowing inflation to cool more rapidly than expected and enabling the Fed to pivot toward rate cuts. Growth stocks and longer-duration bonds would likely outperform in this environment, reversing some of the current market leadership.

Monitoring key indicators including weekly jobless claims, core PCE inflation (the Fed's preferred measure), and consumer sentiment surveys will provide early signals about which scenario is materializing. The University of Michigan inflation expectations data is particularly important, as the Fed closely watches whether households and businesses are becoming unanchored from the 2% target.

Conclusion

The April 2026 CPI report confirming 3.8% inflation represents a significant inflection point for financial markets and Federal Reserve policy. With energy costs surging due to Middle East tensions and core inflation proving stickier than hoped, investors must adjust to a higher-for-longer interest rate environment that could persist through much of 2026 and potentially beyond.

The implications are far-reaching, affecting asset allocation decisions, sector positioning, and risk management across portfolios. Cash has returned as a viable asset class, bonds require careful duration management, and equity selection must prioritize quality, pricing power, and strong balance sheets over speculative growth stories.

For investors seeking to navigate these challenging conditions, leveraging AI-powered analysis tools can provide a significant edge. Intellectia.ai's AI Screener helps identify companies with the financial strength to weather higher rates, while the AI Stock Picker analyzes thousands of securities to find opportunities aligned with the current macro environment. Whether you're adjusting your fixed income duration or seeking inflation-resistant equities, these tools can help you make data-driven decisions in uncertain times.

Start your free trial today at Intellectia.ai and access institutional-grade analysis to position your portfolio for whatever the Fed and inflation throw at markets next.