VTI ETF Update, October 3, 2025

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Oct 03 2025

0mins

Source: TipRanks

VTI Stock Performance: The Vanguard Total Stock Market ETF (VTI) has increased by 0.34% over the past week and 14.7% year-to-date, with a Moderate Buy consensus from analysts and a price target suggesting an 11.43% upside.

Holdings Analysis: VTI's top five holdings with the highest upside potential include BioAtla and Cibus, while those with the greatest downside risk include Wolfspeed and GoPro; the ETF's Smart Score indicates it may underperform the market.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GPRO?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GPRO

Wall Street analysts forecast GPRO stock price to rise

1 Analyst Rating

0 Buy

0 Hold

1 Sell

Moderate Sell

Current: 0.801

Low

1.30

Averages

1.30

High

1.30

Current: 0.801

Low

1.30

Averages

1.30

High

1.30

About GPRO

GoPro, Inc. produces cameras, and mountable and wearable accessories. The Company offers a family of flagship cameras, including HERO13 Black, HERO13 Black Creator Edition, HERO, HERO12 Black, HERO12 Black Creator Edition, HERO11 Black, HERO11 Black Creator Edition, and MAX. HERO13 Black is its flagship camera, featuring a GP2 processor and HyperSmooth 6.0 image stabilization. MAX is a 360-degree waterproof camera featuring MAX HyperSmooth image stabilization, 360-degree MAX TimeWarp Video, MAX SuperView, PowerPano, voice control and a front facing touch display. Its subscription service offers full access to the video and photo editing features in the new Quik desktop app and Quik mobile app. It offers mobile, desktop and Web applications that provide a media workflow for archiving, editing, multi-clip story creation, and sharing content on the fly. It also offers a lifestyle gear lineup that melds its signature design and versatility across a line of bags, backpacks and cases.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Apple to Raise Prices Due to Memory Shortage

- Memory Shortage Impact: Apple CEO Tim Cook stated that price increases are 'unavoidable' due to global memory shortages, indicating that even market leaders cannot escape cost pressures, which may affect consumer purchasing decisions.

- Price Increase Expectations: Analysts predict that Apple may raise the prices of the iPhone Pro and Pro Max by $100 each, while lower-end devices might remain unchanged, potentially altering the competitive landscape in the high-end market.

- Market Share Opportunity: As Android manufacturers cut specs or raise prices due to rising memory costs, Apple could capitalize on this by attracting budget-conscious consumers, thereby expanding its market share, especially with smartphone prices expected to rise by 20% this year.

- Supply Chain Response Strategy: Cook mentioned that Apple might leverage its cash reserves to increase memory supply, demonstrating the company's adaptability in facing supply chain challenges, aiming to ensure the ongoing competitiveness of its products.

See More

GoPro Faces Survival Battle Amid Strategic Overhaul

- Financial Distress: GoPro disclosed in recent US securities filings that it has incurred operating losses and negative cash flows, with auditing firm PwC warning of substantial doubt regarding its ability to continue as a going concern, highlighting the severe financial challenges the company faces.

- Strategic Overhaul: The company is in active discussions with lenders, including Farallon Capital Management and Wells Fargo, and has engaged a financial advisory firm to evaluate a range of strategic alternatives, including a potential sale or merger, indicating its urgent need for survival strategies.

- Intensifying Competition: Despite going public in 2014 and thriving with the rise of social media, GoPro now faces fierce competition from smartphones, with revenues in 2025 reported at $651.5 million, down approximately 44% from four years earlier, reflecting weak market demand.

- Layoffs and Product Launch: In April, GoPro announced a 23% workforce reduction, with first-quarter revenues of $99.1 million, a 26% decline year-over-year, while launching its new Mission 1 product line, touted as the “world's smallest, lightest, and most rugged 8K and 4K Open Gate cinema cameras,” though market reception remains uncertain.

See More

Yamaha Champions Riding School Partners with GoPro as Official Camera

- Strategic Partnership: Yamaha Champions Riding School has entered a multi-year partnership with GoPro, designating GoPro as the official camera, marking a significant collaboration between two industry leaders that enhances rider learning efficiency and safety.

- Technology Integration: GoPro cameras will be extensively utilized in ChampSchool's curriculum, filming each student multiple times to provide frame-by-frame analysis, which helps riders master techniques faster and significantly improves riding safety.

- Media Exposure: ChampSchool's media ecosystem is projected to deliver approximately 29 million social media impressions and over 2 million YouTube views annually for GoPro, ensuring high-frequency brand visibility in an educational environment focused on skill enhancement.

- Product Development Collaboration: The partnership extends beyond camera usage, as GoPro will also engage in product development, on-site testing, and co-creating authentic content with ChampSchool instructors and students, further solidifying its core position in motorcycle training.

See More

FTSE Russell Announces Changes to Russell Microcap Index

- New Additions: Five consumer discretionary companies, including GoPro, Chegg, SES AI, Dave & Buster’s, and Oddity Tech, are set to join the Russell Microcap Index on June 26, which is expected to enhance their market visibility and liquidity, attracting more investor interest.

- Companies Removed: Five firms, namely Faraday Future, Newegg, Cardlytics, Nerdy, and Destination XL, will be removed from the index, potentially putting pressure on their stock prices and affecting investor confidence, reflecting a cautious market outlook on these companies.

- Market Reaction: This adjustment may prompt investors to reassess the related companies, particularly as the new additions are likely to benefit from increased exposure through the index, which could positively influence their stock performance and impact the overall dynamics of the consumer discretionary sector.

- Index Reconstitution Impact: The reconstitution of the FTSE Russell Microcap Index will take place after US equity markets close, and this adjustment not only affects the market performance of individual companies but may also have far-reaching implications for the liquidity and investment strategies within the entire microcap market.

See More

FTSE Russell Announces Changes to 3000 Index

- New Additions: FTSE Russell has announced the preliminary list of companies joining the 3000 Index, effective June 26, including GoPro (GPRO), SES AI Corporation (SES), Unusual Machines (UMAC), Oddity Tech Ltd. (ODD), and Fossil Group (FOSL), which will enhance their market visibility and potential investment appeal.

- Companies Removed: Conversely, companies such as Faraday Future Intelligent Electric (FFAI), Travelzoo (TZOO), Gambling.com Group (GAMB), Sleep Number Corporation (SNBR), and BARK, Inc. (BARK) are set to be removed, which may lead to decreased liquidity and impact their stock performance.

- Market Reaction Anticipation: This adjustment reflects FTSE Russell's assessment of the consumer discretionary sector dynamics, and investors may closely monitor the performance of newly added companies to gauge their competitiveness and growth potential in the market.

- Annual Reconstitution Impact: The annual reconstitution not only affects the market positions of individual companies but may also have far-reaching implications for investment strategies across the consumer discretionary sector, prompting investors to keep a close eye on the subsequent performance of the related stocks.

See More

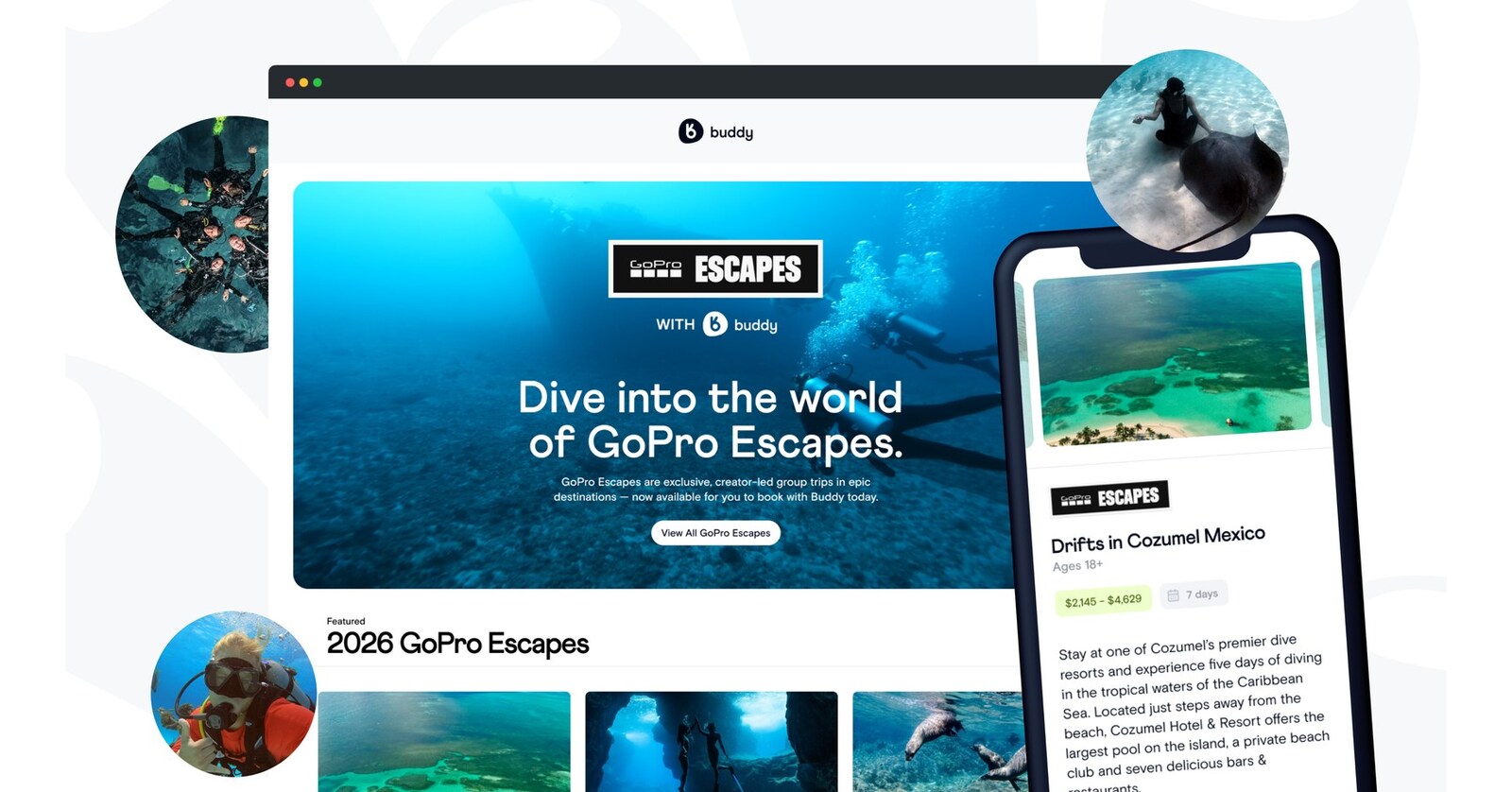

GoPro Launches Exclusive Dive Travel Experiences

- Unique Dive Experiences: GoPro has partnered with Dive with Buddy to launch GoPro Escapes, offering multi-day dive trips led by GoPro athletes and professional dive guides, aimed at enhancing the experience and community for diving enthusiasts.

- Global Destination Coverage: The first wave of GoPro Escapes will launch across the Americas and Asia-Pacific, featuring premier dive locations such as Cozumel, Hawaii, and Fiji, expected to attract a significant number of divers and creators in 2026.

- Convenient Booking Platform: Divers can easily browse and book upcoming GoPro Escapes through BookWithBuddy.com and the Buddy mobile app, significantly improving accessibility and convenience for dive travel.

- Brand Partnership Benefits: This collaboration not only provides dive shops with new business growth opportunities but also strengthens community cohesion through GoPro's brand influence, promoting the culture of diving.

See More

Apple to Raise Prices Due to Memory Shortage

- Memory Shortage Impact: Apple CEO Tim Cook stated that price increases are 'unavoidable' due to global memory shortages, indicating that even market leaders cannot escape cost pressures, which may affect consumer purchasing decisions.

- Price Increase Expectations: Analysts predict that Apple may raise the prices of the iPhone Pro and Pro Max by $100 each, while lower-end devices might remain unchanged, potentially altering the competitive landscape in the high-end market.

- Market Share Opportunity: As Android manufacturers cut specs or raise prices due to rising memory costs, Apple could capitalize on this by attracting budget-conscious consumers, thereby expanding its market share, especially with smartphone prices expected to rise by 20% this year.

- Supply Chain Response Strategy: Cook mentioned that Apple might leverage its cash reserves to increase memory supply, demonstrating the company's adaptability in facing supply chain challenges, aiming to ensure the ongoing competitiveness of its products.

See More

GoPro Faces Survival Battle Amid Strategic Overhaul

- Financial Distress: GoPro disclosed in recent US securities filings that it has incurred operating losses and negative cash flows, with auditing firm PwC warning of substantial doubt regarding its ability to continue as a going concern, highlighting the severe financial challenges the company faces.

- Strategic Overhaul: The company is in active discussions with lenders, including Farallon Capital Management and Wells Fargo, and has engaged a financial advisory firm to evaluate a range of strategic alternatives, including a potential sale or merger, indicating its urgent need for survival strategies.

- Intensifying Competition: Despite going public in 2014 and thriving with the rise of social media, GoPro now faces fierce competition from smartphones, with revenues in 2025 reported at $651.5 million, down approximately 44% from four years earlier, reflecting weak market demand.

- Layoffs and Product Launch: In April, GoPro announced a 23% workforce reduction, with first-quarter revenues of $99.1 million, a 26% decline year-over-year, while launching its new Mission 1 product line, touted as the “world's smallest, lightest, and most rugged 8K and 4K Open Gate cinema cameras,” though market reception remains uncertain.

See More

Yamaha Champions Riding School Partners with GoPro as Official Camera

- Strategic Partnership: Yamaha Champions Riding School has entered a multi-year partnership with GoPro, designating GoPro as the official camera, marking a significant collaboration between two industry leaders that enhances rider learning efficiency and safety.

- Technology Integration: GoPro cameras will be extensively utilized in ChampSchool's curriculum, filming each student multiple times to provide frame-by-frame analysis, which helps riders master techniques faster and significantly improves riding safety.

- Media Exposure: ChampSchool's media ecosystem is projected to deliver approximately 29 million social media impressions and over 2 million YouTube views annually for GoPro, ensuring high-frequency brand visibility in an educational environment focused on skill enhancement.

- Product Development Collaboration: The partnership extends beyond camera usage, as GoPro will also engage in product development, on-site testing, and co-creating authentic content with ChampSchool instructors and students, further solidifying its core position in motorcycle training.

See More

FTSE Russell Announces Changes to Russell Microcap Index

- New Additions: Five consumer discretionary companies, including GoPro, Chegg, SES AI, Dave & Buster’s, and Oddity Tech, are set to join the Russell Microcap Index on June 26, which is expected to enhance their market visibility and liquidity, attracting more investor interest.

- Companies Removed: Five firms, namely Faraday Future, Newegg, Cardlytics, Nerdy, and Destination XL, will be removed from the index, potentially putting pressure on their stock prices and affecting investor confidence, reflecting a cautious market outlook on these companies.

- Market Reaction: This adjustment may prompt investors to reassess the related companies, particularly as the new additions are likely to benefit from increased exposure through the index, which could positively influence their stock performance and impact the overall dynamics of the consumer discretionary sector.

- Index Reconstitution Impact: The reconstitution of the FTSE Russell Microcap Index will take place after US equity markets close, and this adjustment not only affects the market performance of individual companies but may also have far-reaching implications for the liquidity and investment strategies within the entire microcap market.

See More

FTSE Russell Announces Changes to 3000 Index

- New Additions: FTSE Russell has announced the preliminary list of companies joining the 3000 Index, effective June 26, including GoPro (GPRO), SES AI Corporation (SES), Unusual Machines (UMAC), Oddity Tech Ltd. (ODD), and Fossil Group (FOSL), which will enhance their market visibility and potential investment appeal.

- Companies Removed: Conversely, companies such as Faraday Future Intelligent Electric (FFAI), Travelzoo (TZOO), Gambling.com Group (GAMB), Sleep Number Corporation (SNBR), and BARK, Inc. (BARK) are set to be removed, which may lead to decreased liquidity and impact their stock performance.

- Market Reaction Anticipation: This adjustment reflects FTSE Russell's assessment of the consumer discretionary sector dynamics, and investors may closely monitor the performance of newly added companies to gauge their competitiveness and growth potential in the market.

- Annual Reconstitution Impact: The annual reconstitution not only affects the market positions of individual companies but may also have far-reaching implications for investment strategies across the consumer discretionary sector, prompting investors to keep a close eye on the subsequent performance of the related stocks.

See More

GoPro Launches Exclusive Dive Travel Experiences

- Unique Dive Experiences: GoPro has partnered with Dive with Buddy to launch GoPro Escapes, offering multi-day dive trips led by GoPro athletes and professional dive guides, aimed at enhancing the experience and community for diving enthusiasts.

- Global Destination Coverage: The first wave of GoPro Escapes will launch across the Americas and Asia-Pacific, featuring premier dive locations such as Cozumel, Hawaii, and Fiji, expected to attract a significant number of divers and creators in 2026.

- Convenient Booking Platform: Divers can easily browse and book upcoming GoPro Escapes through BookWithBuddy.com and the Buddy mobile app, significantly improving accessibility and convenience for dive travel.

- Brand Partnership Benefits: This collaboration not only provides dive shops with new business growth opportunities but also strengthens community cohesion through GoPro's brand influence, promoting the culture of diving.

See More