UBS Downgrades Corteva to Neutral Amid Separation Risks

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 09 2026

0mins

Should l Buy CTVA?

Source: seekingalpha

- Downgrade Rationale: UBS downgraded Corteva (CTVA) from Buy to Neutral, citing the stock's proximity to its price target and the upcoming separation of its seed and crop protection businesses, which introduces execution risks and potential negative surprises.

- Seed Business Outlook: UBS views Corteva's seed segment as its strongest asset, with seed EBITDA growing at approximately 17% annually over the past five years, and projects an 8% growth rate over the next three years, while the Bayer settlement is expected to generate around $1 billion in licensing income.

- Increased Crop Protection Risks: The crop protection segment faces heightened uncertainty as it transitions to a standalone model, with risks related to unbundling sales potentially pressuring volumes and margins, compounded by competitive pricing pressures from generics in China and India.

- Conservative Guidance and Valuation Reset: Despite the downgrade, UBS believes Corteva's earnings guidance is conservative, modeling seed pricing growth of about 2% annually, while lowering its price target from $81 to $80 to reflect separation risks and near-term earnings uncertainties.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CTVA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CTVA

Wall Street analysts forecast CTVA stock price to rise

13 Analyst Rating

9 Buy

4 Hold

0 Sell

Moderate Buy

Current: 75.550

Low

77.00

Averages

83.75

High

89.00

Current: 75.550

Low

77.00

Averages

83.75

High

89.00

About CTVA

Corteva, Inc. is a global pure-play agriculture company. It is a global provider of seed and crop protection solutions focused on the agriculture industry and contributing to a healthier, secure and sustainable food supply. The Seed segment is engaged in developing and supplying commercial seed combining advanced germplasm and traits that produce optimum yield for farms around the world. It operates in various key seed markets, including North American corn and soybeans, European corn and sunflower, as well as Brazil, India, South Africa and Argentina corn. The Crop Protection segment serves the global agricultural input industry with products that protect against weeds, insects and other pests, and disease, and that support overall crop health both above and below ground via nitrogen management and seed-applied technologies. Its crop protection solutions and digital solutions provide farmers with tools to improve productivity and help keep fields free of weeds, insects and diseases.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Trump Signs Executive Order to Boost Phosphorus and Glyphosate Production

- National Security Focus: Trump signed an executive order invoking the Defense Production Act to promote domestic production of phosphorus and glyphosate, emphasizing their critical importance for U.S. economic and national security, thereby ensuring stability in agricultural and defense supply chains.

- Chemical Controversy: Glyphosate has been controversial due to its alleged links to cancer, and Trump's support aligns with the withdrawal of Health Secretary Kennedy from the election, highlighting the administration's focus on agricultural policy.

- Regulatory Implementation Requirement: The order mandates Agriculture Secretary Brooke Rollins to issue regulations to increase the supply of phosphorus and glyphosate, ensuring U.S. self-sufficiency in these critical chemicals and reducing reliance on foreign sources.

- Industry Response: Monsanto stated it will comply with the order, underscoring the urgent need for U.S. farmers to access domestically produced crop protection tools like glyphosate, reflecting the policy's direct impact on the agricultural sector.

See More

Corteva CEO to Speak at Bank of America Agriculture Conference

- Executive Speaking Engagement: Corteva's CEO Chuck Magro and CFO David Johnson are scheduled to speak at the Bank of America Global Agriculture & Materials conference on February 25, 2026, highlighting the company's leadership in the agriculture sector.

- Live Webcast Availability: The presentation will be webcast live via Corteva's Investor Relations website, ensuring that global investors can access the latest company updates in real-time, thereby enhancing transparency and investor confidence.

- Replay Arrangement: A replay of the presentation will be available 24 hours after it concludes and accessible until February 26, 2027, providing convenience for investors who cannot attend live, further improving information accessibility.

- Company Background Overview: Corteva is a leading global agriculture company committed to addressing the world's agricultural challenges through innovation and effective customer engagement, showcasing its market advantages in seeds, crop protection, and digital products and services.

See More

BP Freezes Stock Buybacks to Prioritize Debt Reduction

- Financial Performance Overview: BP reported adjusted earnings of 60 cents per share, slightly exceeding the consensus estimate of 59 cents, yet total revenue of $47.38 billion fell short of analyst projections of $49.36 billion, indicating challenges in revenue growth.

- Debt Management Strategy: The company has decided to suspend stock buybacks to allocate excess cash towards debt reduction, aiming to lower net debt to between $14 billion and $18 billion by the end of 2027, reflecting a strong emphasis on financial stability.

- Segment Performance: The Oil Production & Operations segment recorded a replacement cost profit of $1.7 billion, with underlying profit adjusted down to $2.0 billion due to impacts from production mix and lower income share, highlighting pressures in the market environment.

- Future Outlook: BP anticipates capital expenditures in the range of $13 billion to $13.5 billion for 2026, with upstream production expected to slightly decline, demonstrating a cautious approach in response to industry challenges while also projecting approximately $1.6 billion in Gulf of America settlement payments.

See More

UBS Downgrades Corteva to Neutral Amid Separation Risks

- Downgrade Rationale: UBS downgraded Corteva (CTVA) from Buy to Neutral, citing the stock's proximity to its price target and the upcoming separation of its seed and crop protection businesses, which introduces execution risks and potential negative surprises.

- Seed Business Outlook: UBS views Corteva's seed segment as its strongest asset, with seed EBITDA growing at approximately 17% annually over the past five years, and projects an 8% growth rate over the next three years, while the Bayer settlement is expected to generate around $1 billion in licensing income.

- Increased Crop Protection Risks: The crop protection segment faces heightened uncertainty as it transitions to a standalone model, with risks related to unbundling sales potentially pressuring volumes and margins, compounded by competitive pricing pressures from generics in China and India.

- Conservative Guidance and Valuation Reset: Despite the downgrade, UBS believes Corteva's earnings guidance is conservative, modeling seed pricing growth of about 2% annually, while lowering its price target from $81 to $80 to reflect separation risks and near-term earnings uncertainties.

See More

Comparison Analysis of Consumer Staples ETFs

- Cost and Yield Comparison: Vanguard Consumer Staples ETF (VDC) charges an annual fee of just 0.09%, significantly lower than Invesco Food & Beverage ETF (PBJ) at 0.61%, while VDC also offers a higher dividend yield of 2.1% compared to PBJ's 1.7%, making VDC more appealing for income-focused investors.

- Portfolio Composition Differences: VDC encompasses over 100 consumer stocks, with 98% in consumer defensive, whereas PBJ focuses on 31 food and beverage companies, including Sysco and Corteva, which may increase specific company risk due to its concentrated investments.

- Market Performance and Risk: Over the past year, VDC achieved a return of 4.6%, while PBJ only managed 1.2%, and VDC's maximum drawdown of 16.55% is lower than PBJ's 15.84%, indicating VDC's relative stability amid market volatility.

- Investment Strategy Choices: As a pure index fund, VDC provides comprehensive defensive exposure to consumer staples, while PBJ employs quantitative analysis for a concentrated portfolio, charging nearly seven times the fees of VDC, yet recent performance suggests this may not justify the cost, prompting investors to choose wisely.

See More

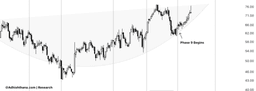

Analysis of Corteva Stock's Cakra Formation

- Cakra Structure Overview: Corteva's stock entered Phase 4 in 2022 and formed a visible Cakra structure by the end of Phase 8 in November 2025, establishing a foundation for a breakout in Phase 9; however, the current trading position near the lower end of the Cakra indicates a lack of ideal breakout conditions.

- Increased Breakout Risk: Although Corteva initially bounced at the start of Phase 9, it has failed to decisively break above the upper boundary of the Cakra, facing repeated selling pressure, which suggests that if a breakout does not materialize, the risk of a significant downside increase is likely.

- Monthly Chart Warning: On the monthly charts, Corteva is currently in Phase 2 and has transitioned into the Buddhi segment, but the absence of prior consolidation during the Sankhya period further weakens the bullish case and adds to the structural caution already evident on the weekly charts.

- Investor Outlook: Investors should avoid chasing Corteva stock, and existing holders must closely monitor the Cakra structure, being prepared to act if a breakdown occurs, as a Cakra breakdown often indicates underlying fundamental risks that may not yet be fully reflected in the stock price.

See More

Trump Signs Executive Order to Boost Phosphorus and Glyphosate Production

- National Security Focus: Trump signed an executive order invoking the Defense Production Act to promote domestic production of phosphorus and glyphosate, emphasizing their critical importance for U.S. economic and national security, thereby ensuring stability in agricultural and defense supply chains.

- Chemical Controversy: Glyphosate has been controversial due to its alleged links to cancer, and Trump's support aligns with the withdrawal of Health Secretary Kennedy from the election, highlighting the administration's focus on agricultural policy.

- Regulatory Implementation Requirement: The order mandates Agriculture Secretary Brooke Rollins to issue regulations to increase the supply of phosphorus and glyphosate, ensuring U.S. self-sufficiency in these critical chemicals and reducing reliance on foreign sources.

- Industry Response: Monsanto stated it will comply with the order, underscoring the urgent need for U.S. farmers to access domestically produced crop protection tools like glyphosate, reflecting the policy's direct impact on the agricultural sector.

See More

Corteva CEO to Speak at Bank of America Agriculture Conference

- Executive Speaking Engagement: Corteva's CEO Chuck Magro and CFO David Johnson are scheduled to speak at the Bank of America Global Agriculture & Materials conference on February 25, 2026, highlighting the company's leadership in the agriculture sector.

- Live Webcast Availability: The presentation will be webcast live via Corteva's Investor Relations website, ensuring that global investors can access the latest company updates in real-time, thereby enhancing transparency and investor confidence.

- Replay Arrangement: A replay of the presentation will be available 24 hours after it concludes and accessible until February 26, 2027, providing convenience for investors who cannot attend live, further improving information accessibility.

- Company Background Overview: Corteva is a leading global agriculture company committed to addressing the world's agricultural challenges through innovation and effective customer engagement, showcasing its market advantages in seeds, crop protection, and digital products and services.

See More

BP Freezes Stock Buybacks to Prioritize Debt Reduction

- Financial Performance Overview: BP reported adjusted earnings of 60 cents per share, slightly exceeding the consensus estimate of 59 cents, yet total revenue of $47.38 billion fell short of analyst projections of $49.36 billion, indicating challenges in revenue growth.

- Debt Management Strategy: The company has decided to suspend stock buybacks to allocate excess cash towards debt reduction, aiming to lower net debt to between $14 billion and $18 billion by the end of 2027, reflecting a strong emphasis on financial stability.

- Segment Performance: The Oil Production & Operations segment recorded a replacement cost profit of $1.7 billion, with underlying profit adjusted down to $2.0 billion due to impacts from production mix and lower income share, highlighting pressures in the market environment.

- Future Outlook: BP anticipates capital expenditures in the range of $13 billion to $13.5 billion for 2026, with upstream production expected to slightly decline, demonstrating a cautious approach in response to industry challenges while also projecting approximately $1.6 billion in Gulf of America settlement payments.

See More

UBS Downgrades Corteva to Neutral Amid Separation Risks

- Downgrade Rationale: UBS downgraded Corteva (CTVA) from Buy to Neutral, citing the stock's proximity to its price target and the upcoming separation of its seed and crop protection businesses, which introduces execution risks and potential negative surprises.

- Seed Business Outlook: UBS views Corteva's seed segment as its strongest asset, with seed EBITDA growing at approximately 17% annually over the past five years, and projects an 8% growth rate over the next three years, while the Bayer settlement is expected to generate around $1 billion in licensing income.

- Increased Crop Protection Risks: The crop protection segment faces heightened uncertainty as it transitions to a standalone model, with risks related to unbundling sales potentially pressuring volumes and margins, compounded by competitive pricing pressures from generics in China and India.

- Conservative Guidance and Valuation Reset: Despite the downgrade, UBS believes Corteva's earnings guidance is conservative, modeling seed pricing growth of about 2% annually, while lowering its price target from $81 to $80 to reflect separation risks and near-term earnings uncertainties.

See More

Comparison Analysis of Consumer Staples ETFs

- Cost and Yield Comparison: Vanguard Consumer Staples ETF (VDC) charges an annual fee of just 0.09%, significantly lower than Invesco Food & Beverage ETF (PBJ) at 0.61%, while VDC also offers a higher dividend yield of 2.1% compared to PBJ's 1.7%, making VDC more appealing for income-focused investors.

- Portfolio Composition Differences: VDC encompasses over 100 consumer stocks, with 98% in consumer defensive, whereas PBJ focuses on 31 food and beverage companies, including Sysco and Corteva, which may increase specific company risk due to its concentrated investments.

- Market Performance and Risk: Over the past year, VDC achieved a return of 4.6%, while PBJ only managed 1.2%, and VDC's maximum drawdown of 16.55% is lower than PBJ's 15.84%, indicating VDC's relative stability amid market volatility.

- Investment Strategy Choices: As a pure index fund, VDC provides comprehensive defensive exposure to consumer staples, while PBJ employs quantitative analysis for a concentrated portfolio, charging nearly seven times the fees of VDC, yet recent performance suggests this may not justify the cost, prompting investors to choose wisely.

See More

Analysis of Corteva Stock's Cakra Formation

- Cakra Structure Overview: Corteva's stock entered Phase 4 in 2022 and formed a visible Cakra structure by the end of Phase 8 in November 2025, establishing a foundation for a breakout in Phase 9; however, the current trading position near the lower end of the Cakra indicates a lack of ideal breakout conditions.

- Increased Breakout Risk: Although Corteva initially bounced at the start of Phase 9, it has failed to decisively break above the upper boundary of the Cakra, facing repeated selling pressure, which suggests that if a breakout does not materialize, the risk of a significant downside increase is likely.

- Monthly Chart Warning: On the monthly charts, Corteva is currently in Phase 2 and has transitioned into the Buddhi segment, but the absence of prior consolidation during the Sankhya period further weakens the bullish case and adds to the structural caution already evident on the weekly charts.

- Investor Outlook: Investors should avoid chasing Corteva stock, and existing holders must closely monitor the Cakra structure, being prepared to act if a breakdown occurs, as a Cakra breakdown often indicates underlying fundamental risks that may not yet be fully reflected in the stock price.

See More