Trump Media & Technology, Sezzle among financial movers

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 28 2024

0mins

Should l Buy SEZL?

Source: SeekingAlpha

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SEZL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SEZL

Wall Street analysts forecast SEZL stock price to rise

3 Analyst Rating

2 Buy

1 Hold

0 Sell

Moderate Buy

Current: 99.820

Low

83.00

Averages

101.00

High

110.00

Current: 99.820

Low

83.00

Averages

101.00

High

110.00

About SEZL

Sezzle Inc. is a fintech company. The Company’s payment platform increases the purchasing power of consumers by offering access to point-of-sale financing options and digital payment services connecting millions of customers with its global network of merchants. Its payment options allow consumers to take control over their spending. Its digital payments platform provides consumers a flexible alternative to traditional credit. Its Sezzle Platform offers a payments solution for consumers that instantly extends credit at the point-of-sale, allowing consumers to purchase and receive the ordered merchandise at the time of sale while paying in installments over time. The Sezzle Platform flagship product, pay-in-four, allows consumers to pay a fourth of the purchase price up front, and then another fourth of the purchase price every two weeks thereafter over a total of six weeks. Its Sezzle Virtual Card provides rapid-installation and point-of-sale option for brick-and-mortar retailers.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Sezzle Inc. Under Investigation for Securities Law Violations

- Board Member Resignation: Sezzle disclosed on April 9, 2026, that Karen Webster, a member of the Audit and Risk Committee, resigned from the Board due to growing differences with management regarding the company's direction, potentially destabilizing corporate governance.

- Legal Firm Involvement: Lowey Dannenberg P.C. is investigating whether Sezzle provided investors with accurate and complete information, and if issues are found, the company may face legal liabilities that could impact its stock price and investor confidence.

- Investor Loss Alert: Attorney Andrea Farah indicated that investors who suffered losses exceeding $50,000 in Sezzle securities should contact the law firm to participate in the investigation, which may attract more investor attention and potential lawsuits.

- Governance Risk: Webster's resignation may indicate underlying issues within Sezzle's governance structure, and if not addressed promptly, could lead to a larger management crisis and a decline in investor trust.

See More

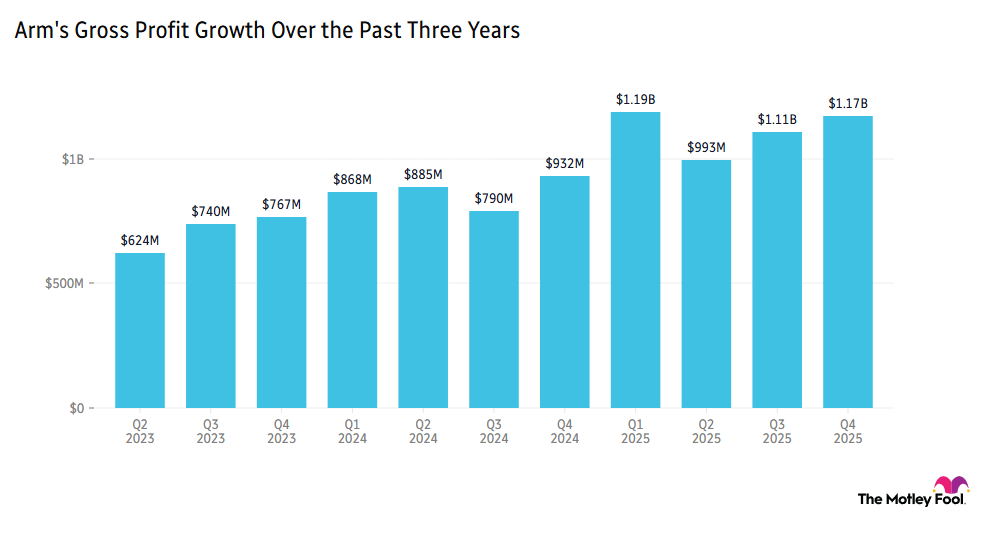

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

SEZZLE INC: NEEDHAM INCREASES TARGET PRICE FROM $94 TO $122

- Company Announcement: Needham raises the price target for SEZLLE Inc. stock.

- New Price Target: The new price target is set at $122, up from the previous $94.

See More

SEZZLE INC: KBW Increases Target Price from $85 to $115

- Company Update: SEZL Inc. has raised its target price significantly.

- New Target Price: The target price has increased from $85 to $115.

See More

Sezzle Reports Significant Earnings Growth in Q1

- Earnings Growth: Sezzle Inc. reported Q1 earnings of $51.30 million, translating to $1.47 per share, a significant increase from last year's $36.16 million and $1.00 per share, indicating enhanced profitability.

- Adjusted Earnings: Excluding items, Sezzle's adjusted earnings stood at $49.99 million or $1.43 per share, reflecting robust performance in core operations and bolstering investor confidence.

- Revenue Increase: The company's revenue surged 29.2% year-over-year to $135.54 million from $104.91 million last year, showcasing strong market demand and successful business expansion.

- Full-Year Guidance: Sezzle's guidance for full-year EPS is set at $5.10, signaling an optimistic outlook for future performance, which may attract more investor interest in its long-term growth potential.

See More

Sezzle Expected to Exceed Q1 Earnings Estimates

- Earnings Announcement Preview: Sezzle (SEZL) is set to announce its Q1 earnings on May 6th after market close, with consensus EPS estimate at $1.24 and revenue at $129.16 million, reflecting a robust 23.1% year-over-year growth.

- Strong Historical Performance: Over the past year, Sezzle has beaten both EPS and revenue estimates 100% of the time, indicating financial stability and strong market confidence, which could further drive stock price appreciation.

- Expectation Revision Dynamics: In the last three months, EPS estimates have seen two upward revisions and one downward revision, while revenue estimates have also experienced two upward and one downward revision, showcasing analysts' optimistic outlook on the company's future performance.

- Market Reaction Analysis: Despite a recent decline in Sezzle's stock price due to a director's resignation, the company's positive growth momentum and improved valuation ahead of the earnings report may attract renewed investor interest, potentially driving the stock price recovery.

See More

Sezzle Inc. Under Investigation for Securities Law Violations

- Board Member Resignation: Sezzle disclosed on April 9, 2026, that Karen Webster, a member of the Audit and Risk Committee, resigned from the Board due to growing differences with management regarding the company's direction, potentially destabilizing corporate governance.

- Legal Firm Involvement: Lowey Dannenberg P.C. is investigating whether Sezzle provided investors with accurate and complete information, and if issues are found, the company may face legal liabilities that could impact its stock price and investor confidence.

- Investor Loss Alert: Attorney Andrea Farah indicated that investors who suffered losses exceeding $50,000 in Sezzle securities should contact the law firm to participate in the investigation, which may attract more investor attention and potential lawsuits.

- Governance Risk: Webster's resignation may indicate underlying issues within Sezzle's governance structure, and if not addressed promptly, could lead to a larger management crisis and a decline in investor trust.

See More

Arm Faces Challenges Amid Chip Supply Strains

- Smartphone Market Slowdown: Arm Holdings fell over 6% in pre-market trading due to a memory chip shortage, which has slowed growth in the smartphone market, despite an improved outlook for AI data centers, impacting major tech companies reliant on Arm's services.

- Strong Demand for New CPU: Arm's new CPU has over $2 billion in customer demand over the next two financial years, indicating a positive market reception for its homegrown chips, which strengthens its position in the cloud computing sector, particularly among top hyperscalers with a 50% market share.

- Memory Stocks Rally: Micron Technology and Western Digital saw their stocks rise over 4% amid chip shortages and ongoing AI demand, demonstrating strong pricing power in the current market backdrop, although future prospects remain uncertain due to historical volatility.

- Celsius's Impressive Performance: Celsius Holdings reported a staggering 137.7% revenue increase in Q1, reaching $782.6 million, showcasing robust growth in both its core brand and Alani Nu, which boosts market confidence in its future performance.

See More

SEZZLE INC: NEEDHAM INCREASES TARGET PRICE FROM $94 TO $122

- Company Announcement: Needham raises the price target for SEZLLE Inc. stock.

- New Price Target: The new price target is set at $122, up from the previous $94.

See More

SEZZLE INC: KBW Increases Target Price from $85 to $115

- Company Update: SEZL Inc. has raised its target price significantly.

- New Target Price: The target price has increased from $85 to $115.

See More

Sezzle Reports Significant Earnings Growth in Q1

- Earnings Growth: Sezzle Inc. reported Q1 earnings of $51.30 million, translating to $1.47 per share, a significant increase from last year's $36.16 million and $1.00 per share, indicating enhanced profitability.

- Adjusted Earnings: Excluding items, Sezzle's adjusted earnings stood at $49.99 million or $1.43 per share, reflecting robust performance in core operations and bolstering investor confidence.

- Revenue Increase: The company's revenue surged 29.2% year-over-year to $135.54 million from $104.91 million last year, showcasing strong market demand and successful business expansion.

- Full-Year Guidance: Sezzle's guidance for full-year EPS is set at $5.10, signaling an optimistic outlook for future performance, which may attract more investor interest in its long-term growth potential.

See More

Sezzle Expected to Exceed Q1 Earnings Estimates

- Earnings Announcement Preview: Sezzle (SEZL) is set to announce its Q1 earnings on May 6th after market close, with consensus EPS estimate at $1.24 and revenue at $129.16 million, reflecting a robust 23.1% year-over-year growth.

- Strong Historical Performance: Over the past year, Sezzle has beaten both EPS and revenue estimates 100% of the time, indicating financial stability and strong market confidence, which could further drive stock price appreciation.

- Expectation Revision Dynamics: In the last three months, EPS estimates have seen two upward revisions and one downward revision, while revenue estimates have also experienced two upward and one downward revision, showcasing analysts' optimistic outlook on the company's future performance.

- Market Reaction Analysis: Despite a recent decline in Sezzle's stock price due to a director's resignation, the company's positive growth momentum and improved valuation ahead of the earnings report may attract renewed investor interest, potentially driving the stock price recovery.

See More