Rambus Q1 2026 Earnings Call Highlights

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 28 2026

0mins

Should l Buy RMBS?

Source: seekingalpha

- Strong Financial Performance: Rambus reported non-GAAP revenue of $180.2 million in Q1 2026, with product revenue at $88 million, reflecting a 15% year-over-year increase, demonstrating the company's robust market positioning amid accelerating AI demands.

- Optimistic Outlook: The company expects Q2 revenue to range between $192 million and $198 million, with product revenue projected between $95 million and $101 million, indicating management's confidence in sustained growth.

- New Product Launch: Rambus introduced the JEDEC-standard LPDDR5X SOCAMM2 module, enabling power-efficient operation at up to 9.6 Gbps, marking a strategic move into LPDDR-based server module solutions.

- Cash Flow and Inventory Management: The company generated free cash flow of $66.3 million in Q1, ending with $786 million in cash and equivalents, while planning to strategically increase inventory to support product revenue growth and manage potential supply chain constraints.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy RMBS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on RMBS

Wall Street analysts forecast RMBS stock price to fall

6 Analyst Rating

4 Buy

1 Hold

1 Sell

Moderate Buy

Current: 127.050

Low

83.00

Averages

107.40

High

130.00

Current: 127.050

Low

83.00

Averages

107.40

High

130.00

About RMBS

Rambus Inc. is a global semiconductor company dedicated to enabling data centers and artificial intelligence by delivering memory and security solutions that address the evolving needs of the industry. It offers a balanced and diverse portfolio of products encompassing chips and silicon intellectual property (IP). Its solutions maximize performance and security in computationally intensive systems. Its DDR memory interface chips for server memory modules enable increased bandwidth and expanded capacity in enterprise and cloud servers. Its portfolio includes DDR5 and DDR4 memory interface chipsets. Its DDR5 chipset solutions include the Registering Clock Driver, Multiplexed Registering Clock Driver, Multiplexed Data Buffer, Power Management Integrated Circuits, Serial Presence Detect Hubs, Temperature Sensors, and Client Clock Driver. Its Silicon IP includes interface and security IP solutions that move and protect data in advanced data center, government and automotive applications.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

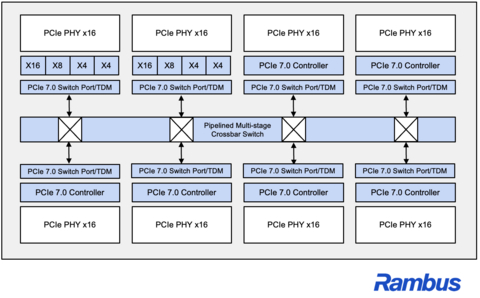

Rambus Launches PCIe 7.0 Switch IP with TDM for AI Infrastructure

- Technological Innovation: Rambus's newly launched PCIe 7.0 Switch IP with Time Division Multiplexing (TDM) is designed to meet the escalating demands for bandwidth, latency, and scalability in AI, cloud, and high-performance computing (HPC) systems, thereby enhancing data transfer efficiency and overall system performance.

- Architectural Flexibility: This switch IP optimizes PCIe link utilization through intelligent traffic multiplexing, simplifying system design and supporting disaggregated and pooled compute architectures, which facilitates efficient handling of diverse workloads such as large-scale AI training and latency-sensitive inference.

- Market Leadership: The PCIe 7.0 Switch IP expands Rambus's industry-leading PCIe IP portfolio, which includes controllers, retimers, and debug solutions, helping customers accelerate time-to-market while meeting the stringent performance and reliability requirements of modern AI infrastructure.

- Strategic Significance: As AI infrastructure rapidly evolves, Rambus's technological innovations not only enhance system bandwidth and efficiency but also provide customers with critical capabilities for efficient data movement within complex architectures, further solidifying its leadership position in high-speed interface IP.

See More

Rambus Launches PCIe 7.0 Switch IP with TDM for AI Infrastructure

- Technological Innovation: Rambus's newly launched PCIe 7.0 Switch IP with Time Division Multiplexing (TDM) addresses the escalating demands for bandwidth and latency in AI, cloud, and high-performance computing systems, thereby enhancing data transfer efficiency and managing system complexity.

- Architectural Flexibility: This switch IP supports intelligent traffic multiplexing, enabling efficient scheduling of traffic across shared links, maximizing network utilization, and accommodating diverse workloads from large-scale AI training to latency-sensitive inference, significantly boosting system performance.

- Market Leadership: The Rambus PCIe 7.0 Switch IP expands its industry-leading PCIe IP portfolio, which includes controllers, retimers, and debug solutions, helping customers accelerate time-to-market while meeting the high performance and reliability requirements of modern AI infrastructure.

- Strategic Implications: As AI infrastructure rapidly evolves, Rambus strengthens its leadership in high-speed interface IP by providing advanced PCIe switching technologies, empowering customers to tackle challenges in AI, cloud, and HPC sectors.

See More

Rambus Appoints New CFO to Drive Growth

- Executive Appointment: Rambus has named Sumeet Gagneja as Senior Vice President and Chief Financial Officer effective April 29, 2026, bringing extensive financial management experience from his previous role as divisional CFO for AMD’s Data Center segment, which is expected to enhance the company's financial strategy.

- Financial Outlook: The company anticipates a non-GAAP EPS of $0.65 to $0.73 for Q2 2026, with projected revenues between $192 million and $198 million, indicating stability and growth potential in its market positioning.

- Market Reaction: Despite the strong financial outlook, Rambus's stock fell following a rating downgrade by Baird, reflecting a cautious market sentiment regarding the company's future performance.

- Strategic Planning: Gagneja's appointment aligns with Rambus's ambitious $2.2 billion roadmap, aiming to drive long-term growth through optimized financial strategies and improved operational efficiency.

See More

U.S. Stocks Close Lower, Weighed Down by Tech Sector

- Tech Sector Decline: Technology stocks fell broadly as concerns about the return on massive AI investments grew, with OpenAI missing its new user and sales targets, putting pressure on shares of partners like Nvidia and Oracle, which negatively impacted market sentiment.

- Positive Economic Data: Despite the market downturn, the U.S. consumer confidence index unexpectedly rose to 92.8, surpassing expectations, indicating economic resilience that could provide support for the market.

- Surging Oil Prices: WTI crude oil prices jumped over 3% to a two-week high amid escalating tensions between the U.S. and Iran in the Strait of Hormuz, potentially exacerbating the global energy crisis and pushing inflation expectations higher.

- Fed Policy Expectations: The market anticipates that the Federal Reserve will keep interest rates unchanged at the upcoming meeting, focusing on oil prices and inflation dynamics, reflecting a cautious outlook on the economic landscape.

See More

OpenAI's Missed Targets Impact Tech Stocks

- OpenAI's Missed Targets: OpenAI was expected to reach 1 billion weekly users by the end of 2025 but failed to meet this target, raising concerns about its future growth potential and possibly affecting investor confidence.

- Compute Capacity Bottleneck: Analysts highlight that compute capacity is a critical bottleneck for AI development, and if OpenAI falls short of its spending commitments nearing $1 trillion, it could negatively impact the market and lead to reduced investments in related companies.

- Tech Stock Volatility: Following this news, Nvidia's stock dropped by 1%, while smaller tech stocks like Rambus plummeted by 20%, indicating the market's sensitivity and volatility regarding high-risk tech stocks.

- Sustained Demand Growth: Despite the challenges, CorWeve noted that as more companies build and deploy AI, the demand for compute continues to grow, with expectations that it will consistently exceed supply, providing long-term support for the market.

See More

Rambus Shares Plunge 21.2% Amid Downgrade

- Significant Stock Drop: Rambus shares plummeted 21.2% on Tuesday, with a current price of $113.58 and a market cap of $15 billion, reflecting investor concerns about the company's future outlook.

- Earnings Report Disappointment: Although Rambus reported an 8.1% year-over-year revenue increase to $180.2 million and a 6.8% rise in adjusted earnings per share to $0.63, these results fell short of market expectations for higher performance, leading to a stock pullback.

- Analyst Downgrade: Analysts at Baird downgraded Rambus from Outperform to Neutral, maintaining a target price of $120, citing potential severe memory shortages that could impact unit sales in the future.

- Market Outlook Analysis: Despite facing supply shortages in the short term, Rambus may benefit from the widespread adoption of AI technologies, making it an attractive option for investors looking to enter the memory market, even though its current valuation stands at approximately 38 times this year's earnings estimates.

See More

Rambus Launches PCIe 7.0 Switch IP with TDM for AI Infrastructure

- Technological Innovation: Rambus's newly launched PCIe 7.0 Switch IP with Time Division Multiplexing (TDM) is designed to meet the escalating demands for bandwidth, latency, and scalability in AI, cloud, and high-performance computing (HPC) systems, thereby enhancing data transfer efficiency and overall system performance.

- Architectural Flexibility: This switch IP optimizes PCIe link utilization through intelligent traffic multiplexing, simplifying system design and supporting disaggregated and pooled compute architectures, which facilitates efficient handling of diverse workloads such as large-scale AI training and latency-sensitive inference.

- Market Leadership: The PCIe 7.0 Switch IP expands Rambus's industry-leading PCIe IP portfolio, which includes controllers, retimers, and debug solutions, helping customers accelerate time-to-market while meeting the stringent performance and reliability requirements of modern AI infrastructure.

- Strategic Significance: As AI infrastructure rapidly evolves, Rambus's technological innovations not only enhance system bandwidth and efficiency but also provide customers with critical capabilities for efficient data movement within complex architectures, further solidifying its leadership position in high-speed interface IP.

See More

Rambus Launches PCIe 7.0 Switch IP with TDM for AI Infrastructure

- Technological Innovation: Rambus's newly launched PCIe 7.0 Switch IP with Time Division Multiplexing (TDM) addresses the escalating demands for bandwidth and latency in AI, cloud, and high-performance computing systems, thereby enhancing data transfer efficiency and managing system complexity.

- Architectural Flexibility: This switch IP supports intelligent traffic multiplexing, enabling efficient scheduling of traffic across shared links, maximizing network utilization, and accommodating diverse workloads from large-scale AI training to latency-sensitive inference, significantly boosting system performance.

- Market Leadership: The Rambus PCIe 7.0 Switch IP expands its industry-leading PCIe IP portfolio, which includes controllers, retimers, and debug solutions, helping customers accelerate time-to-market while meeting the high performance and reliability requirements of modern AI infrastructure.

- Strategic Implications: As AI infrastructure rapidly evolves, Rambus strengthens its leadership in high-speed interface IP by providing advanced PCIe switching technologies, empowering customers to tackle challenges in AI, cloud, and HPC sectors.

See More

Rambus Appoints New CFO to Drive Growth

- Executive Appointment: Rambus has named Sumeet Gagneja as Senior Vice President and Chief Financial Officer effective April 29, 2026, bringing extensive financial management experience from his previous role as divisional CFO for AMD’s Data Center segment, which is expected to enhance the company's financial strategy.

- Financial Outlook: The company anticipates a non-GAAP EPS of $0.65 to $0.73 for Q2 2026, with projected revenues between $192 million and $198 million, indicating stability and growth potential in its market positioning.

- Market Reaction: Despite the strong financial outlook, Rambus's stock fell following a rating downgrade by Baird, reflecting a cautious market sentiment regarding the company's future performance.

- Strategic Planning: Gagneja's appointment aligns with Rambus's ambitious $2.2 billion roadmap, aiming to drive long-term growth through optimized financial strategies and improved operational efficiency.

See More

U.S. Stocks Close Lower, Weighed Down by Tech Sector

- Tech Sector Decline: Technology stocks fell broadly as concerns about the return on massive AI investments grew, with OpenAI missing its new user and sales targets, putting pressure on shares of partners like Nvidia and Oracle, which negatively impacted market sentiment.

- Positive Economic Data: Despite the market downturn, the U.S. consumer confidence index unexpectedly rose to 92.8, surpassing expectations, indicating economic resilience that could provide support for the market.

- Surging Oil Prices: WTI crude oil prices jumped over 3% to a two-week high amid escalating tensions between the U.S. and Iran in the Strait of Hormuz, potentially exacerbating the global energy crisis and pushing inflation expectations higher.

- Fed Policy Expectations: The market anticipates that the Federal Reserve will keep interest rates unchanged at the upcoming meeting, focusing on oil prices and inflation dynamics, reflecting a cautious outlook on the economic landscape.

See More

OpenAI's Missed Targets Impact Tech Stocks

- OpenAI's Missed Targets: OpenAI was expected to reach 1 billion weekly users by the end of 2025 but failed to meet this target, raising concerns about its future growth potential and possibly affecting investor confidence.

- Compute Capacity Bottleneck: Analysts highlight that compute capacity is a critical bottleneck for AI development, and if OpenAI falls short of its spending commitments nearing $1 trillion, it could negatively impact the market and lead to reduced investments in related companies.

- Tech Stock Volatility: Following this news, Nvidia's stock dropped by 1%, while smaller tech stocks like Rambus plummeted by 20%, indicating the market's sensitivity and volatility regarding high-risk tech stocks.

- Sustained Demand Growth: Despite the challenges, CorWeve noted that as more companies build and deploy AI, the demand for compute continues to grow, with expectations that it will consistently exceed supply, providing long-term support for the market.

See More

Rambus Shares Plunge 21.2% Amid Downgrade

- Significant Stock Drop: Rambus shares plummeted 21.2% on Tuesday, with a current price of $113.58 and a market cap of $15 billion, reflecting investor concerns about the company's future outlook.

- Earnings Report Disappointment: Although Rambus reported an 8.1% year-over-year revenue increase to $180.2 million and a 6.8% rise in adjusted earnings per share to $0.63, these results fell short of market expectations for higher performance, leading to a stock pullback.

- Analyst Downgrade: Analysts at Baird downgraded Rambus from Outperform to Neutral, maintaining a target price of $120, citing potential severe memory shortages that could impact unit sales in the future.

- Market Outlook Analysis: Despite facing supply shortages in the short term, Rambus may benefit from the widespread adoption of AI technologies, making it an attractive option for investors looking to enter the memory market, even though its current valuation stands at approximately 38 times this year's earnings estimates.

See More