Karooooo Reports FY 2026 Non-GAAP EPS and Dividend Increase

Written by Emily J. Thompson, Senior Investment Analyst

Updated: May 13 2026

0mins

Source: seekingalpha

- Earnings Performance: Karooooo reported a FY 2026 Non-GAAP EPS of ZAR 32.55, indicating stable profitability, although the stock's appeal remains unconvincing in the current market.

- Cash Flow Growth: The adjusted free cash flow for FY 2026 surged 90% year-over-year to ZAR 809 million, demonstrating significant improvement in cash generation capabilities, which will support future investments and expansion.

- Dividend Increase: The company declared a USD 1.50 dividend per share, a 20% increase year-over-year, reflecting confidence in future profitability while enhancing shareholder returns.

- Market Rating: Despite strong financial performance, Seeking Alpha's Quant Rating suggests that Karooooo's stock is not yet a compelling buy, which may influence investor decisions moving forward.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy KARO?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on KARO

Wall Street analysts forecast KARO stock price to rise

4 Analyst Rating

4 Buy

0 Hold

0 Sell

Strong Buy

Current: 46.440

Low

55.00

Averages

58.33

High

60.00

Current: 46.440

Low

55.00

Averages

58.33

High

60.00

About KARO

Karooooo Ltd. is a Singapore-based company. The principal activities include the provision of real-time mobility data analytics solutions for smart transportation through its software-as-a-service (SaaS) platform, physical and electronic commerce vehicle buying and selling, and providing a technology platform focused on last-mile delivery. The Company’s segments include Cartrack, Carzuka, and Karooooo Logistics. Cartrack offers an on-the-ground operational Internet of Things (IoT) SaaS cloud that optimizes transportation, operations, and workflow data. Carzuka is a physical and electronic commerce marketplace for vehicle buying and selling, allowing customers to source, buy, and sell vehicles. Karooooo Logistics provides a software application for managing last-mile delivery and general operational logistics. The Company’s subsidiaries include Cartrack Holdings Proprietary Limited, Carzuka.com Pte Ltd, Karooooo Management Company Pte. Ltd., Karooooo Cartrack Limited, and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Karooooo Highlights Record FY 2026 Financial Results

- Strong Financial Performance: Karooooo reported record financial results for FY 2026, with accelerating subscription revenue and annual recurring revenue (ARR) growth, indicating robust market demand and business expansion potential.

- Robust Cash Flow Generation: The company generated strong free cash flow during FY 2026, demonstrating improved operational efficiency and profitability, which provides funding support for future investments and expansion.

- Optimistic FY 2027 Outlook: Management's outlook for FY 2027 indicates accelerating Cartrack subscription revenue growth and healthy earnings per share (EPS) expansion, reflecting the company's competitive advantages and sustainable growth capabilities in the market.

- Global Business Scale: Karooooo serves over 125,000 commercial customers and 2.7 million active subscribers globally, showcasing its extensive influence and market penetration across more than 20 countries.

See More

Karooooo Market Trends Analysis

- Market Trend Insights: In a video published on May 25, 2026, analysts explored market dynamics surrounding Karooooo, offering deep insights into future investment opportunities, although specific data was not disclosed, the overall market trend indicates positive potential.

- Investment Opportunity Assessment: Experts analyzed Karooooo's business model and market positioning, emphasizing its adaptability in a rapidly changing market environment, which could yield long-term returns for investors.

- Stock Performance Review: As of March 25, 2026, Karooooo's stock price increased by 2.37%, reflecting market confidence in its future growth, despite the lack of detailed financial data to support this.

- Video Content Value: The video provides investors with an in-depth analysis of Karooooo, and while specific financial metrics are absent, the discussion on its market prospects offers crucial decision-making insights for potential investors.

See More

Karooooo Investment Insights from Motley Fool

- Market Trend Insights: In the latest Motley Fool video, analysts discuss market trends for Karooooo, noting that while the company did not make the recommended top 10 stocks list, it still provides valuable investment insights to help investors make informed decisions.

- Return Comparison: The Motley Fool Stock Advisor boasts an average return of 986%, significantly outperforming the S&P 500's 208%, indicating the potential profitability of its recommended stocks, even though Karooooo was not included.

- Future Investment Opportunities: Analysts highlight that Karooooo may face intense market competition, particularly in the AI and technology sectors, prompting investors to carefully assess its future growth potential to avoid missing out on higher returns.

- Community Investment Philosophy: Motley Fool encourages individual investors to join its community to share investment experiences and strategies, and while Karooooo is not on the recommendation list, its analysis still offers valuable references for investors.

See More

Karooooo Executives to Attend Investor Conference

- Executive Participation: Karooooo's Group COO Richard Schubert and VP of Investor Relations Paul Bieber will participate in the 46th Annual William Blair Growth Stock Conference on June 3, showcasing the company's leadership in mobility and operational intelligence solutions.

- Live Webcast Availability: The presentation will be available via live webcast in the Events and Presentations section of Karooooo's Investor Relations website, ensuring that global investors can access the latest updates and strategic direction in real-time.

- Business Transformation Capability: Karooooo simplifies decision-making through its cloud platform, enabling businesses to enhance efficiency in fleet maintenance, fuel management, and asset utilization, thereby reducing costs and improving customer satisfaction, highlighting its competitive edge in the market.

- Global Customer Base: With over 125,000 commercial customers and more than 2,700,000 active subscribers across over 20 countries, Karooooo demonstrates significant influence and market penetration within the industry.

See More

Karooooo Ltd. Q4 Fiscal 2026 Earnings Call Insights

- Significant Revenue Growth: Karooooo Ltd. reported a 20% increase in total revenue for Q4 FY 2026, reaching ZAR 5,479 million, with subscription revenue rising 19% to ZAR 4,844 million, demonstrating strong market performance despite foreign exchange pressures.

- Annual Recurring Revenue Increase: The annual recurring revenue (ARR) grew by 18% to ZAR 5,179 million (approximately USD 325 million), indicating a sustained enhancement in customer base and revenue stability, further solidifying the company's market position.

- Cash Flow and Shareholder Returns: Adjusted free cash flow surged by 90% to ZAR 809 million, alongside a declared dividend of USD 1.50 per share, marking a 20% increase, which reflects the company's commitment to shareholders and improved financial health.

- Cautious Future Outlook: Management's guidance for FY 2027 projects subscription revenue between ZAR 5,700 million and ZAR 6,000 million, indicating a planned acceleration in subscription revenue growth despite challenges related to cost pressures and hiring slowdowns, showcasing confidence in future performance.

See More

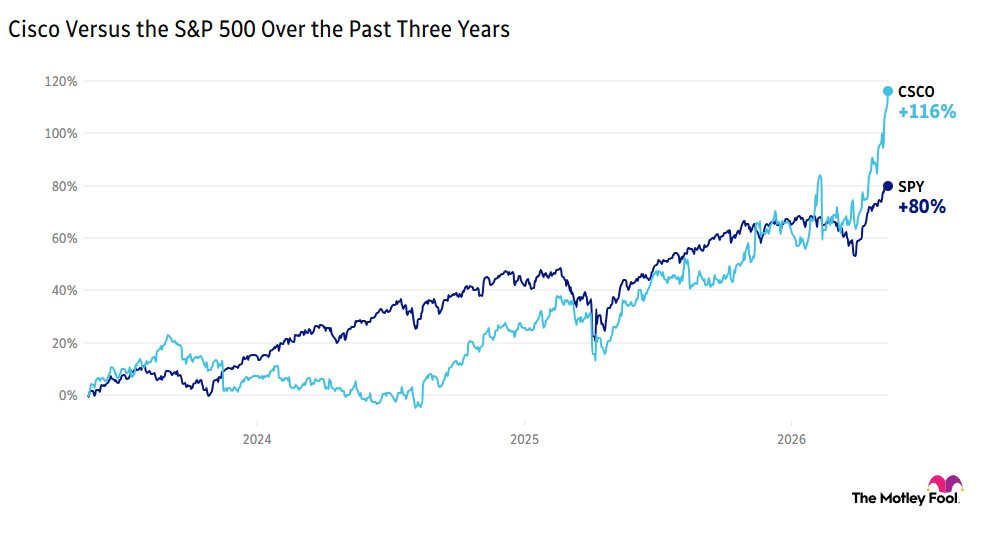

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

Karooooo Highlights Record FY 2026 Financial Results

- Strong Financial Performance: Karooooo reported record financial results for FY 2026, with accelerating subscription revenue and annual recurring revenue (ARR) growth, indicating robust market demand and business expansion potential.

- Robust Cash Flow Generation: The company generated strong free cash flow during FY 2026, demonstrating improved operational efficiency and profitability, which provides funding support for future investments and expansion.

- Optimistic FY 2027 Outlook: Management's outlook for FY 2027 indicates accelerating Cartrack subscription revenue growth and healthy earnings per share (EPS) expansion, reflecting the company's competitive advantages and sustainable growth capabilities in the market.

- Global Business Scale: Karooooo serves over 125,000 commercial customers and 2.7 million active subscribers globally, showcasing its extensive influence and market penetration across more than 20 countries.

See More

Karooooo Market Trends Analysis

- Market Trend Insights: In a video published on May 25, 2026, analysts explored market dynamics surrounding Karooooo, offering deep insights into future investment opportunities, although specific data was not disclosed, the overall market trend indicates positive potential.

- Investment Opportunity Assessment: Experts analyzed Karooooo's business model and market positioning, emphasizing its adaptability in a rapidly changing market environment, which could yield long-term returns for investors.

- Stock Performance Review: As of March 25, 2026, Karooooo's stock price increased by 2.37%, reflecting market confidence in its future growth, despite the lack of detailed financial data to support this.

- Video Content Value: The video provides investors with an in-depth analysis of Karooooo, and while specific financial metrics are absent, the discussion on its market prospects offers crucial decision-making insights for potential investors.

See More

Karooooo Investment Insights from Motley Fool

- Market Trend Insights: In the latest Motley Fool video, analysts discuss market trends for Karooooo, noting that while the company did not make the recommended top 10 stocks list, it still provides valuable investment insights to help investors make informed decisions.

- Return Comparison: The Motley Fool Stock Advisor boasts an average return of 986%, significantly outperforming the S&P 500's 208%, indicating the potential profitability of its recommended stocks, even though Karooooo was not included.

- Future Investment Opportunities: Analysts highlight that Karooooo may face intense market competition, particularly in the AI and technology sectors, prompting investors to carefully assess its future growth potential to avoid missing out on higher returns.

- Community Investment Philosophy: Motley Fool encourages individual investors to join its community to share investment experiences and strategies, and while Karooooo is not on the recommendation list, its analysis still offers valuable references for investors.

See More

Karooooo Executives to Attend Investor Conference

- Executive Participation: Karooooo's Group COO Richard Schubert and VP of Investor Relations Paul Bieber will participate in the 46th Annual William Blair Growth Stock Conference on June 3, showcasing the company's leadership in mobility and operational intelligence solutions.

- Live Webcast Availability: The presentation will be available via live webcast in the Events and Presentations section of Karooooo's Investor Relations website, ensuring that global investors can access the latest updates and strategic direction in real-time.

- Business Transformation Capability: Karooooo simplifies decision-making through its cloud platform, enabling businesses to enhance efficiency in fleet maintenance, fuel management, and asset utilization, thereby reducing costs and improving customer satisfaction, highlighting its competitive edge in the market.

- Global Customer Base: With over 125,000 commercial customers and more than 2,700,000 active subscribers across over 20 countries, Karooooo demonstrates significant influence and market penetration within the industry.

See More

Karooooo Ltd. Q4 Fiscal 2026 Earnings Call Insights

- Significant Revenue Growth: Karooooo Ltd. reported a 20% increase in total revenue for Q4 FY 2026, reaching ZAR 5,479 million, with subscription revenue rising 19% to ZAR 4,844 million, demonstrating strong market performance despite foreign exchange pressures.

- Annual Recurring Revenue Increase: The annual recurring revenue (ARR) grew by 18% to ZAR 5,179 million (approximately USD 325 million), indicating a sustained enhancement in customer base and revenue stability, further solidifying the company's market position.

- Cash Flow and Shareholder Returns: Adjusted free cash flow surged by 90% to ZAR 809 million, alongside a declared dividend of USD 1.50 per share, marking a 20% increase, which reflects the company's commitment to shareholders and improved financial health.

- Cautious Future Outlook: Management's guidance for FY 2027 projects subscription revenue between ZAR 5,700 million and ZAR 6,000 million, indicating a planned acceleration in subscription revenue growth despite challenges related to cost pressures and hiring slowdowns, showcasing confidence in future performance.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More