EXELIXIS Q4 ADJUSTED EPS REACHES USD 0.94, BEATING IBES ESTIMATE OF USD 0.79

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 10 2026

0mins

Source: moomoo

Earnings Report: EXELIXIS reported a Q4 adjusted EPS of $0.94, indicating strong financial performance.

Comparison with Estimates: The reported EPS surpassed the IBES estimate of $0.79, reflecting better-than-expected results.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy EXEL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on EXEL

Wall Street analysts forecast EXEL stock price to fall

16 Analyst Rating

7 Buy

8 Hold

1 Sell

Moderate Buy

Current: 52.700

Low

30.00

Averages

44.09

High

52.00

Current: 52.700

Low

30.00

Averages

44.09

High

52.00

About EXEL

Exelixis, Inc. is an oncology company. The Company has produced four marketed pharmaceutical products, two of which are formulations of its flagship molecule, cabozantinib. It is also advancing and evolving its product pipeline portfolio, including its lead investigational asset, zanzalintinib. Cabozantinib is an inhibitor of multiple tyrosine kinases, including MET, AXL, VEGF receptors and RET and has been also approved as CABOMETYX tablets for advanced renal cell carcinoma, for previously treated hepatocellular carcinoma and for previously treated, radioactive iodine-refractory differentiated thyroid cancer, and as COMETRIQ capsules for progressive, metastatic medullary thyroid cancer. The Company's other two products are COTELLIC, an inhibitor of MEK approved as part of multiple combination regimens to treat specific forms of advanced melanoma and MINNEBRO an oral, non-steroidal, selective blocker of the mineralocorticoid receptor approved the treatment of hypertension in Japan.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

CABOMETYX Shows Significant Efficacy in Advanced NET Treatment

- Risk Reduction: CABOMETYX significantly reduced the risk of disease progression or death by 74% in non-functional and 60% in functional advanced neuroendocrine tumor (NET) patients, reinforcing its position as a critical treatment option.

- Progression-Free Survival Improvement: In the CABINET trial, the median progression-free survival (PFS) for CABOMETYX was 9.4 months in non-functional NET patients compared to just 3.1 months for placebo, highlighting its effectiveness in disease control.

- Clinical Results Presentation: The results will be presented at the 2026 American Society of Clinical Oncology Annual Meeting, emphasizing CABOMETYX's efficacy across different functional statuses of NET, which may influence future treatment decisions.

- Safety Profile Consistency: The safety profile of CABOMETYX remained consistent with known characteristics, with no new safety signals identified; in functional NET patients, the most common grade 3/4 adverse events were hypertension (21%), indicating its acceptable safety profile.

See More

U.S.-Iran Interim Deal Boosts Stock Market to New Highs

- Market Highs: The stock market surged to new highs on Thursday following reports of an interim U.S.-Iran deal, reflecting investor optimism over reduced geopolitical risks, which positively impacted overall market performance.

- Dell's Strong Earnings: Dell Technologies saw its stock soar after reporting robust earnings, demonstrating the company's strong market performance and profitability, which further bolstered investor confidence in tech stocks.

- Improved Investor Sentiment: The positive market reaction to the U.S.-Iran agreement not only lifted stock indices but may also attract more capital into the market, fostering economic recovery and corporate investment.

- Geopolitical Impact: The interim deal between the U.S. and Iran could alleviate tensions in the Middle East, potentially bringing greater stability to global markets and enhancing investors' risk appetite.

See More

Exelixis to Present New Therapies at ASCO Meeting

- New Drug Presentation: Exelixis will showcase its flagship product CABOMETYX® and investigational oral kinase inhibitor zanzalintinib at the 2026 ASCO Annual Meeting, highlighting ongoing progress in tumor treatment, which is expected to attract investor interest and boost market confidence.

- Clinical Trial Results: CABOMETYX has demonstrated significant efficacy in multiple clinical trials, including studies targeting renal cell carcinoma and neuroendocrine tumors, further solidifying its foundational role in patient care and potentially driving sales growth.

- Strategic Development: Dana T. Aftab, Exelixis' EVP of Research and Development, stated that the presented datasets affirm the company's commitment to improving cancer care standards, which may lay the groundwork for future product line expansions.

- FDA Application Progress: The FDA has accepted the New Drug Application for zanzalintinib, with a target action date of December 3, 2026; if approved, this could open new market opportunities for the company and enhance its competitiveness in cancer treatment.

See More

Exelixis Poised for Doubling Growth Over Next Five Years

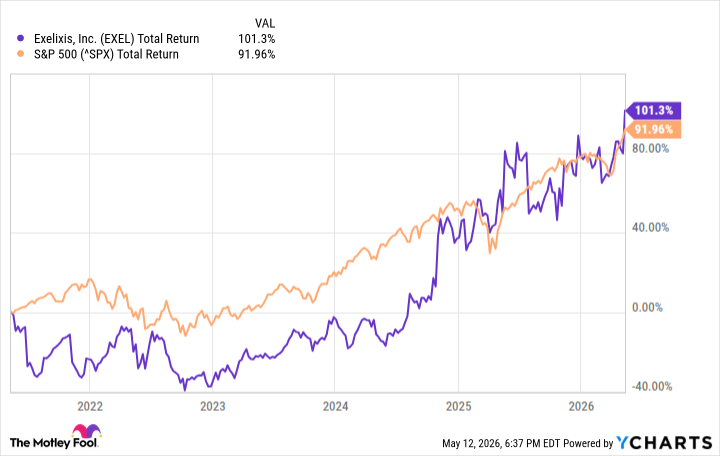

- Strong Stock Performance: Exelixis has seen its stock price rise by 101% over the past five years, outperforming the S&P 500, indicating robust performance in the biotech sector, with potential for another doubling in the next five years attracting investor interest.

- Cabometyx Growth: The company's flagship product, Cabometyx, generated $610.8 million in revenue in Q1 2023, a 10% year-over-year increase, with projected revenue of $2.58 billion for fiscal year 2026, underscoring its strong market position in liver and kidney cancers.

- Next-Gen Drug Potential: Exelixis is developing zanzalintinib, which has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, addressing a significant unmet need with projected peak sales of $5 billion, enhancing the company's growth prospects.

- Diverse Pipeline Strategy: Beyond Cabometyx, Exelixis is testing zanzalintinib for various cancers, including renal cell carcinoma, and successful indications could provide substantial financial support, ensuring continued growth in the competitive oncology market.

See More

Exelixis Shows Significant Future Growth Potential

- Strong Stock Performance: Exelixis shares have risen 101% over the past five years, slightly outperforming the S&P 500, indicating robust performance and investment appeal in the biotech sector.

- Cabometyx Drives Growth: As Exelixis' flagship product, Cabometyx saw a 10% year-over-year revenue increase to $610.8 million in Q1, with projected midpoint revenue of $2.58 billion for FY 2026, reflecting sustained demand and strong sales capabilities in the cancer treatment market.

- New Drug Development Progress: The investigational drug zanzalintinib has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, with potential peak sales of $5 billion, showcasing the company's strategic focus on addressing unmet medical needs.

- Optimistic Future Outlook: Despite the impending patent cliff for Cabometyx, Exelixis has several early-stage pipeline candidates expected to drive financial growth in the coming years, suggesting a bright medium-term outlook with potential for stock doubling by 2031.

See More

Exelixis Q1 2026 Earnings Call Insights

- CABOMETYX Growth Momentum: Exelixis reported the highest number of new patient starts for CABOMETYX in Q1, with TRx market share increasing from 44% to 47%, indicating strong demand in the renal cell carcinoma and neuroendocrine tumor markets, further solidifying its leadership position.

- Capital Repurchase Plan: The company repurchased approximately $430.8 million of stock in Q1 and received board approval for a new $750 million stock repurchase plan, aimed at enhancing shareholder confidence while providing funding for future R&D investments.

- ZANZA R&D Progress: Management emphasized that the CRC NDA application for ZANZA and atezolizumab is the company's top priority, with a PDUFA expected in early December 2026, highlighting the strategic focus on colorectal cancer treatment.

- Strong Financial Performance: Q1 total revenues were approximately $611 million, with GAAP net income around $210.5 million, demonstrating effective control over operating expenses despite pressures from the 340B program and Medicare discounts.

See More

CABOMETYX Shows Significant Efficacy in Advanced NET Treatment

- Risk Reduction: CABOMETYX significantly reduced the risk of disease progression or death by 74% in non-functional and 60% in functional advanced neuroendocrine tumor (NET) patients, reinforcing its position as a critical treatment option.

- Progression-Free Survival Improvement: In the CABINET trial, the median progression-free survival (PFS) for CABOMETYX was 9.4 months in non-functional NET patients compared to just 3.1 months for placebo, highlighting its effectiveness in disease control.

- Clinical Results Presentation: The results will be presented at the 2026 American Society of Clinical Oncology Annual Meeting, emphasizing CABOMETYX's efficacy across different functional statuses of NET, which may influence future treatment decisions.

- Safety Profile Consistency: The safety profile of CABOMETYX remained consistent with known characteristics, with no new safety signals identified; in functional NET patients, the most common grade 3/4 adverse events were hypertension (21%), indicating its acceptable safety profile.

See More

U.S.-Iran Interim Deal Boosts Stock Market to New Highs

- Market Highs: The stock market surged to new highs on Thursday following reports of an interim U.S.-Iran deal, reflecting investor optimism over reduced geopolitical risks, which positively impacted overall market performance.

- Dell's Strong Earnings: Dell Technologies saw its stock soar after reporting robust earnings, demonstrating the company's strong market performance and profitability, which further bolstered investor confidence in tech stocks.

- Improved Investor Sentiment: The positive market reaction to the U.S.-Iran agreement not only lifted stock indices but may also attract more capital into the market, fostering economic recovery and corporate investment.

- Geopolitical Impact: The interim deal between the U.S. and Iran could alleviate tensions in the Middle East, potentially bringing greater stability to global markets and enhancing investors' risk appetite.

See More

Exelixis to Present New Therapies at ASCO Meeting

- New Drug Presentation: Exelixis will showcase its flagship product CABOMETYX® and investigational oral kinase inhibitor zanzalintinib at the 2026 ASCO Annual Meeting, highlighting ongoing progress in tumor treatment, which is expected to attract investor interest and boost market confidence.

- Clinical Trial Results: CABOMETYX has demonstrated significant efficacy in multiple clinical trials, including studies targeting renal cell carcinoma and neuroendocrine tumors, further solidifying its foundational role in patient care and potentially driving sales growth.

- Strategic Development: Dana T. Aftab, Exelixis' EVP of Research and Development, stated that the presented datasets affirm the company's commitment to improving cancer care standards, which may lay the groundwork for future product line expansions.

- FDA Application Progress: The FDA has accepted the New Drug Application for zanzalintinib, with a target action date of December 3, 2026; if approved, this could open new market opportunities for the company and enhance its competitiveness in cancer treatment.

See More

Exelixis Poised for Doubling Growth Over Next Five Years

- Strong Stock Performance: Exelixis has seen its stock price rise by 101% over the past five years, outperforming the S&P 500, indicating robust performance in the biotech sector, with potential for another doubling in the next five years attracting investor interest.

- Cabometyx Growth: The company's flagship product, Cabometyx, generated $610.8 million in revenue in Q1 2023, a 10% year-over-year increase, with projected revenue of $2.58 billion for fiscal year 2026, underscoring its strong market position in liver and kidney cancers.

- Next-Gen Drug Potential: Exelixis is developing zanzalintinib, which has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, addressing a significant unmet need with projected peak sales of $5 billion, enhancing the company's growth prospects.

- Diverse Pipeline Strategy: Beyond Cabometyx, Exelixis is testing zanzalintinib for various cancers, including renal cell carcinoma, and successful indications could provide substantial financial support, ensuring continued growth in the competitive oncology market.

See More

Exelixis Shows Significant Future Growth Potential

- Strong Stock Performance: Exelixis shares have risen 101% over the past five years, slightly outperforming the S&P 500, indicating robust performance and investment appeal in the biotech sector.

- Cabometyx Drives Growth: As Exelixis' flagship product, Cabometyx saw a 10% year-over-year revenue increase to $610.8 million in Q1, with projected midpoint revenue of $2.58 billion for FY 2026, reflecting sustained demand and strong sales capabilities in the cancer treatment market.

- New Drug Development Progress: The investigational drug zanzalintinib has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, with potential peak sales of $5 billion, showcasing the company's strategic focus on addressing unmet medical needs.

- Optimistic Future Outlook: Despite the impending patent cliff for Cabometyx, Exelixis has several early-stage pipeline candidates expected to drive financial growth in the coming years, suggesting a bright medium-term outlook with potential for stock doubling by 2031.

See More

Exelixis Q1 2026 Earnings Call Insights

- CABOMETYX Growth Momentum: Exelixis reported the highest number of new patient starts for CABOMETYX in Q1, with TRx market share increasing from 44% to 47%, indicating strong demand in the renal cell carcinoma and neuroendocrine tumor markets, further solidifying its leadership position.

- Capital Repurchase Plan: The company repurchased approximately $430.8 million of stock in Q1 and received board approval for a new $750 million stock repurchase plan, aimed at enhancing shareholder confidence while providing funding for future R&D investments.

- ZANZA R&D Progress: Management emphasized that the CRC NDA application for ZANZA and atezolizumab is the company's top priority, with a PDUFA expected in early December 2026, highlighting the strategic focus on colorectal cancer treatment.

- Strong Financial Performance: Q1 total revenues were approximately $611 million, with GAAP net income around $210.5 million, demonstrating effective control over operating expenses despite pressures from the 340B program and Medicare discounts.

See More