Emerging Investment Opportunities in Cybersecurity Stocks

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 08 2026

0mins

Source: Fool

- Palo Alto Growth: Palo Alto Networks (PANW) has strengthened its identity and access management security features through a $25 billion acquisition of CyberArk, with Q2 sales rising 15% year-over-year to $2.6 billion, indicating strong demand for its security products, and total sales are projected to reach $11.3 billion by 2026, a nearly 23% increase.

- AI-Driven Security Platform: The Prisma AIR artificial intelligence security platform from Palo Alto has tripled its customer base in just one quarter, with CEO Arora noting that as customers adopt AI security, the company's market position will continue to strengthen, highlighting a long-term trend in cybersecurity.

- Microsoft's Silent Leadership: Microsoft (MSFT) is projected to achieve security revenues of $37 billion by 2025 and potentially $50 billion by 2030, with 1.6 million global security customers, showcasing its strong competitive edge in an increasingly complex AI threat landscape.

- Cloud and Security Integration: Microsoft's Azure cloud computing business holds a 21% market share and is closely tied to its security business, expected to attract more customers, especially as the AI cloud market is projected to approach $2 trillion by 2030, further solidifying its market position.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PANW?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PANW

Wall Street analysts forecast PANW stock price to fall

34 Analyst Rating

28 Buy

5 Hold

1 Sell

Strong Buy

Current: 260.580

Low

157.00

Averages

232.49

High

265.00

Current: 260.580

Low

157.00

Averages

232.49

High

265.00

About PANW

Palo Alto Networks, Inc. is a global artificial intelligence (AI) cybersecurity company, with a comprehensive portfolio of cybersecurity solutions and platforms across network, cloud, security operations, AI and Identity. Its network security platform includes Secure Access Service Edge (SASE), Next-Generation Firewalls, Cloud Delivered Security Services (CDSS), Prisma AIRS, and Strata Cloud Manager (SCM). It delivers security operations capabilities that unifies standalone Security Information and Event Management (SIEM) tools, endpoint security, security automation, cloud detection and response (CDR), as well as attack surface management (ASM) capabilities on its Cortex platform. It delivers comprehensive security across the cloud application development lifecycle through Cortex Cloud. Its Unit 42 brings together expertise across threat research, incident response, and security consulting to deliver intelligence-driven, response-ready outcomes that help customers reduce cyber risk.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Integrated Cyber Solutions Releases White Paper on Data Compression

- Data Compression Breakthrough: Integrated Cyber Solutions' white paper reveals that its VEIL™ technology can achieve data compression rates of 95% to 99.96%, allowing enterprises to eliminate data exposure risks without sacrificing model performance, thereby enhancing data security and compliance.

- Significant Industry Impact: As the White House warns of state-sponsored cyberattacks from China, the exposure of enterprise data has become a national security issue, and the introduction of VEIL™ provides a new solution for companies to protect critical data while maintaining competitiveness in the face of increasing cybersecurity threats.

- Performance Validation and Comparison: The white paper indicates that VEIL™ performs excellently across multiple supervised learning tasks, matching or exceeding the predictive performance of raw data models, and outperforms differential privacy and homomorphic encryption in attack simulations, showcasing its potential for real-world applications.

- Academic Endorsement and Market Prospects: The white paper is supported by an assistant professor from Simon Fraser University, enhancing its credibility, and if VEIL™ performs as expected in commercial deployments, it could significantly improve enterprise AI infrastructure efficiency, potentially reducing storage and computational costs.

See More

Integrated Cyber Solutions Releases White Paper Showing Over 95% Data Compression Rate

- Data Compression Innovation: Integrated Cyber Solutions' white paper reveals that its VEIL™ product can achieve data compression rates of up to 99.96%, significantly reducing data exposure risks while maintaining model performance, thereby enhancing enterprise competitiveness in AI security.

- Privacy Protection Capability: The white paper indicates that VEIL™ excels across multiple supervised learning tasks, compressing sensitive input data while matching or exceeding the predictive performance of raw data models, addressing the performance trade-offs of traditional privacy-preserving methods.

- Significant Market Potential: As enterprises increasingly prioritize AI security, the introduction of VEIL™ could transform the foundational infrastructure for data processing, potentially leading to substantial reductions in storage and computational costs, attracting more corporate attention and investment.

- Independent Validation Support: The white paper is endorsed by an assistant professor at Simon Fraser University, further enhancing VEIL™'s credibility and indicating its potential for broad application in real-world deployments.

See More

Anthropic's Mythos LLM Raises Cybersecurity Concerns

- Cybersecurity Threat: Anthropic's newly announced Mythos LLM is deemed a significant cybersecurity threat due to its ability to uncover dormant vulnerabilities in codebases, which, if released, could be exploited by malicious actors, posing serious security risks.

- Project Glasswing: In response to the risks posed by Mythos, Anthropic has launched Project Glasswing, partnering with select businesses to provide access to Mythos, thereby enhancing their cybersecurity defenses and demonstrating strategic foresight in the security domain.

- Market Opportunity: As large enterprises increasingly consolidate their security software vendors, Palo Alto Networks is capitalizing on this trend with its platformization strategy, which has led to a 35% year-over-year increase in platformized customers, indicating robust market demand for comprehensive security solutions.

- Investment Value Analysis: Despite Palo Alto's stock surging 60% in a month and a half, trading at 70 times forward earnings and 18.5 times sales expectations, the company is well-positioned to leverage AI-driven security needs for significant growth, making it a potential investment consideration for those looking at future opportunities.

See More

Anthropic Unveils Mythos but Withholds Public Release Due to Cybersecurity Risks

- Mythos Release and Security Risks: On April 7, Anthropic announced its large language model Mythos but withheld its public release due to significant cybersecurity threats, highlighting the company's commitment to user protection against potential exploits.

- Project Glasswing Collaboration: Anthropic launched Project Glasswing, partnering with select businesses to provide access to Mythos for enhanced cybersecurity, demonstrating a proactive strategy in addressing emerging threats in the digital landscape.

- Palo Alto Stock Surge: Following the announcement of Project Glasswing, Palo Alto Networks' stock surged 60% over a month and a half, reflecting strong market confidence in its platformization strategy and future growth potential.

- AI-Driven Security Software Consolidation: As enterprises increasingly consolidate security software vendors, Palo Alto is well-positioned to capitalize on this trend with its comprehensive security solutions and robust customer base, which may drive revenue growth despite its high current P/E ratio of 70, indicating strong market recognition of its long-term value.

See More

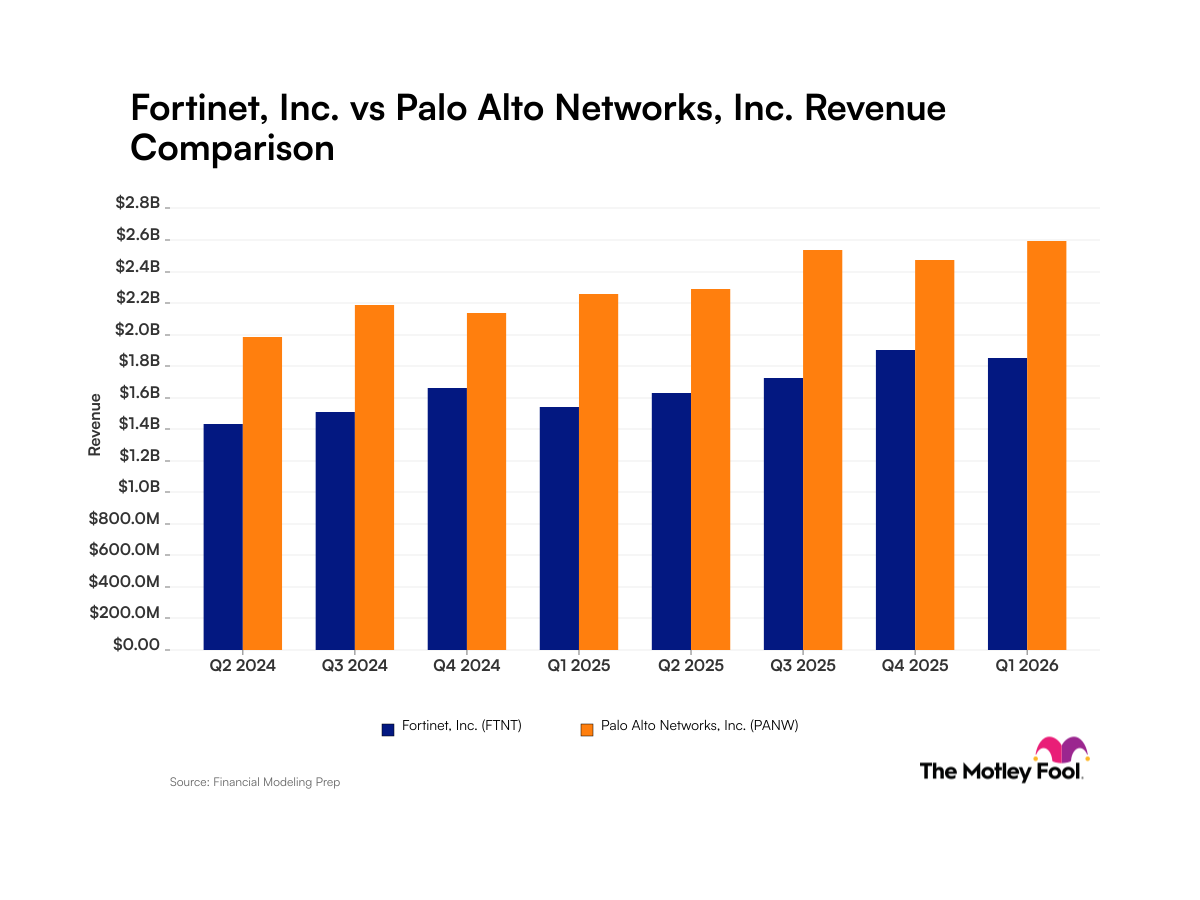

Comparison of Cybersecurity Companies' Earnings Reports

- Revenue Gap Analysis: Palo Alto Networks reported $2.6 billion in revenue while Fortinet generated $1.8 billion in its latest earnings report; despite Palo Alto's higher revenue, Fortinet's 20% year-over-year growth indicates a faster business expansion that may narrow the revenue gap in the future.

- Net Margin Comparison: Fortinet achieved a net income margin of 29% for Q1 2026, compared to Palo Alto Networks' 17%, suggesting that Fortinet is performing better in cost control and profitability, which may attract more investor interest in its stock.

- Stock Price Fluctuations: On May 22, Fortinet's stock hit a 52-week high of $134.19, while Palo Alto Networks reached $261.41, reflecting market optimism about both companies' future growth potential, despite previous sell-offs due to AI concerns.

- Strong Market Demand: Despite fears of competition from AI, the cybersecurity sector continues to show robust customer demand, as evidenced by the year-over-year revenue growth of both Palo Alto Networks and Fortinet, indicating a positive outlook for the industry.

See More

Fortinet and Palo Alto Networks Revenue Growth

- Fortinet Revenue Growth: Fortinet reported $1.8 billion in revenue for Q1 2026, reflecting a 20% year-over-year increase, which underscores its robust growth in the network security hardware and software services sector, further solidifying its market position.

- Palo Alto Networks Performance: Palo Alto Networks generated $2.6 billion in revenue for Q1 2026, marking a 15% year-over-year growth; while its growth rate is lower than Fortinet's, it maintains a strong leadership position in the large enterprise and government markets.

- Stock Price Rebound: On May 22, Fortinet's stock reached a 52-week high of $134.19, while Palo Alto Networks hit $261.41, reflecting a restored investor confidence in cybersecurity demand, particularly in the context of the AI era.

- Strong Market Demand: The sales growth of both companies in their latest quarterly results indicates that despite initial market fears regarding AI, the demand for cybersecurity remains robust, highlighting the urgent need for protective measures among clients.

See More

Integrated Cyber Solutions Releases White Paper on Data Compression

- Data Compression Breakthrough: Integrated Cyber Solutions' white paper reveals that its VEIL™ technology can achieve data compression rates of 95% to 99.96%, allowing enterprises to eliminate data exposure risks without sacrificing model performance, thereby enhancing data security and compliance.

- Significant Industry Impact: As the White House warns of state-sponsored cyberattacks from China, the exposure of enterprise data has become a national security issue, and the introduction of VEIL™ provides a new solution for companies to protect critical data while maintaining competitiveness in the face of increasing cybersecurity threats.

- Performance Validation and Comparison: The white paper indicates that VEIL™ performs excellently across multiple supervised learning tasks, matching or exceeding the predictive performance of raw data models, and outperforms differential privacy and homomorphic encryption in attack simulations, showcasing its potential for real-world applications.

- Academic Endorsement and Market Prospects: The white paper is supported by an assistant professor from Simon Fraser University, enhancing its credibility, and if VEIL™ performs as expected in commercial deployments, it could significantly improve enterprise AI infrastructure efficiency, potentially reducing storage and computational costs.

See More

Integrated Cyber Solutions Releases White Paper Showing Over 95% Data Compression Rate

- Data Compression Innovation: Integrated Cyber Solutions' white paper reveals that its VEIL™ product can achieve data compression rates of up to 99.96%, significantly reducing data exposure risks while maintaining model performance, thereby enhancing enterprise competitiveness in AI security.

- Privacy Protection Capability: The white paper indicates that VEIL™ excels across multiple supervised learning tasks, compressing sensitive input data while matching or exceeding the predictive performance of raw data models, addressing the performance trade-offs of traditional privacy-preserving methods.

- Significant Market Potential: As enterprises increasingly prioritize AI security, the introduction of VEIL™ could transform the foundational infrastructure for data processing, potentially leading to substantial reductions in storage and computational costs, attracting more corporate attention and investment.

- Independent Validation Support: The white paper is endorsed by an assistant professor at Simon Fraser University, further enhancing VEIL™'s credibility and indicating its potential for broad application in real-world deployments.

See More

Anthropic's Mythos LLM Raises Cybersecurity Concerns

- Cybersecurity Threat: Anthropic's newly announced Mythos LLM is deemed a significant cybersecurity threat due to its ability to uncover dormant vulnerabilities in codebases, which, if released, could be exploited by malicious actors, posing serious security risks.

- Project Glasswing: In response to the risks posed by Mythos, Anthropic has launched Project Glasswing, partnering with select businesses to provide access to Mythos, thereby enhancing their cybersecurity defenses and demonstrating strategic foresight in the security domain.

- Market Opportunity: As large enterprises increasingly consolidate their security software vendors, Palo Alto Networks is capitalizing on this trend with its platformization strategy, which has led to a 35% year-over-year increase in platformized customers, indicating robust market demand for comprehensive security solutions.

- Investment Value Analysis: Despite Palo Alto's stock surging 60% in a month and a half, trading at 70 times forward earnings and 18.5 times sales expectations, the company is well-positioned to leverage AI-driven security needs for significant growth, making it a potential investment consideration for those looking at future opportunities.

See More

Anthropic Unveils Mythos but Withholds Public Release Due to Cybersecurity Risks

- Mythos Release and Security Risks: On April 7, Anthropic announced its large language model Mythos but withheld its public release due to significant cybersecurity threats, highlighting the company's commitment to user protection against potential exploits.

- Project Glasswing Collaboration: Anthropic launched Project Glasswing, partnering with select businesses to provide access to Mythos for enhanced cybersecurity, demonstrating a proactive strategy in addressing emerging threats in the digital landscape.

- Palo Alto Stock Surge: Following the announcement of Project Glasswing, Palo Alto Networks' stock surged 60% over a month and a half, reflecting strong market confidence in its platformization strategy and future growth potential.

- AI-Driven Security Software Consolidation: As enterprises increasingly consolidate security software vendors, Palo Alto is well-positioned to capitalize on this trend with its comprehensive security solutions and robust customer base, which may drive revenue growth despite its high current P/E ratio of 70, indicating strong market recognition of its long-term value.

See More

Comparison of Cybersecurity Companies' Earnings Reports

- Revenue Gap Analysis: Palo Alto Networks reported $2.6 billion in revenue while Fortinet generated $1.8 billion in its latest earnings report; despite Palo Alto's higher revenue, Fortinet's 20% year-over-year growth indicates a faster business expansion that may narrow the revenue gap in the future.

- Net Margin Comparison: Fortinet achieved a net income margin of 29% for Q1 2026, compared to Palo Alto Networks' 17%, suggesting that Fortinet is performing better in cost control and profitability, which may attract more investor interest in its stock.

- Stock Price Fluctuations: On May 22, Fortinet's stock hit a 52-week high of $134.19, while Palo Alto Networks reached $261.41, reflecting market optimism about both companies' future growth potential, despite previous sell-offs due to AI concerns.

- Strong Market Demand: Despite fears of competition from AI, the cybersecurity sector continues to show robust customer demand, as evidenced by the year-over-year revenue growth of both Palo Alto Networks and Fortinet, indicating a positive outlook for the industry.

See More

Fortinet and Palo Alto Networks Revenue Growth

- Fortinet Revenue Growth: Fortinet reported $1.8 billion in revenue for Q1 2026, reflecting a 20% year-over-year increase, which underscores its robust growth in the network security hardware and software services sector, further solidifying its market position.

- Palo Alto Networks Performance: Palo Alto Networks generated $2.6 billion in revenue for Q1 2026, marking a 15% year-over-year growth; while its growth rate is lower than Fortinet's, it maintains a strong leadership position in the large enterprise and government markets.

- Stock Price Rebound: On May 22, Fortinet's stock reached a 52-week high of $134.19, while Palo Alto Networks hit $261.41, reflecting a restored investor confidence in cybersecurity demand, particularly in the context of the AI era.

- Strong Market Demand: The sales growth of both companies in their latest quarterly results indicates that despite initial market fears regarding AI, the demand for cybersecurity remains robust, highlighting the urgent need for protective measures among clients.

See More