EMCOR Group Projects Strong 2026 Financial Outlook

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 26 2026

0mins

Should l Buy EME?

Source: NASDAQ.COM

- 2026 Revenue Forecast: EMCOR Group anticipates revenues between $17.75 billion and $18.50 billion for 2026, reflecting the company's optimistic outlook on its project mix and providing a stable growth signal for investors.

- Operating Margin Outlook: The company expects an operating margin between 9.0% and 9.4% for 2026, demonstrating ongoing efforts in cost control and efficiency improvements, which further enhance its competitive position in the market.

- Fourth Quarter Performance: EMCOR reported a fourth-quarter net income of $434.61 million, or $9.68 per share, significantly up from $292.16 million and $6.32 per share last year, indicating strong performance and improved profitability in the market.

- Year-over-Year Revenue Growth: The fourth-quarter revenue increased by 19.7%, rising from $3.77 billion to $4.513 billion, reflecting the company's positive performance amid industry recovery and strengthening its future market position.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy EME?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on EME

Wall Street analysts forecast EME stock price to fall

1 Analyst Rating

1 Buy

0 Hold

0 Sell

Moderate Buy

Current: 930.030

Low

754.00

Averages

754.00

High

754.00

Current: 930.030

Low

754.00

Averages

754.00

High

754.00

About EME

EMCOR Group, Inc. is a specialty contractor in the United States and a provider of electrical and mechanical construction and facilities services, building services, and industrial services. The Company’s services are provided to a range of commercial, technology, manufacturing, industrial, healthcare, utility, and institutional customers through approximately 100 operating subsidiaries. Such operating subsidiaries are organized into the various reportable segments, including the United States electrical construction and facilities services, United States mechanical construction and facilities services, United States building services, and United States industrial services. Its electrical and mechanical construction services primarily involve the design, integration, installation, start-up, operation and maintenance, and provision of services relating to roadway and transit lighting and signaling and fiber optic lines, and fire protection and suppression systems.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Market Highs Analysis and Investment Recommendations

- Electronic Arts Outlook: Despite being renowned for its FIFA and Madden NFL franchises, Electronic Arts (EA) has shown a muted annual revenue growth of only 3% over the past three years, indicating a lag in demand compared to peers, with expectations of continued soft demand over the next 12 months potentially leading to investor losses.

- American Express Global Business Travel Challenges: American Express Global Business Travel (GBTG) has achieved a 12.5% annual revenue growth over the last two years, which is acceptable in absolute terms but tepid for a tech company benefiting from industry tailwinds, and its gross margin of 59% is significantly below competitors, limiting investment in marketing and R&D.

- EMCOR's Strong Performance: EMCOR (EME) has reported an impressive annual revenue growth of 16.3% over the past two years, indicating an increase in market share during this cycle, and its share buybacks have accelerated earnings per share growth, while returns on capital are rising as management makes more lucrative investments.

- Market Sentiment and Investment Risks: While some stocks are nearing their 52-week highs and market sentiment appears positive, short-term trends may lead to investor losses, necessitating a cautious evaluation of investment opportunities, particularly in companies like Electronic Arts and American Express Global Business Travel.

See More

Electrical Infrastructure Firms Thrive Amid Data Center Boom

- Emcor's Strong Performance: Emcor reported record revenue of $4.63 billion in Q1, a 19.7% year-over-year increase, with EPS of $6.84, up 30%, and a backlog of $15.6 billion, up 32.9%, indicating robust demand for high-margin data center projects.

- Schneider's Regional Growth: Schneider Electric's overall revenue rose 4.7% year-over-year to €9.77 billion in Q1, led by a 14.4% increase in North America and a 14.2% rise in China and East Asia, showcasing the effectiveness of its diversified market strategy against regional economic fluctuations.

- Quanta Services' Market Position: Quanta Services reported a record backlog of $39.2 billion in Q1, with revenue of $7.9 billion, up 26%, and EPS of $1.45, up 51%, highlighting its competitive edge in large-scale multi-state transmission projects.

- Investor Attention on Growth Potential: Although these companies are not well-known, their stock prices have surged between 18% and 78% this year, reflecting market recognition of their growth prospects, particularly Emcor's reasonable valuation and Quanta Services' greater long-term growth potential.

See More

Insights into EMCOR's Market Trends and Investment Opportunities

- Market Trend Analysis: In a video published on May 5, 2026, analysts discussed EMCOR's performance in the current market environment, emphasizing attention to future investment opportunities despite the lack of specific data.

- Investment Opportunity Exploration: Experts noted that EMCOR may exhibit growth potential in future markets, providing insights for investors even without concrete financial metrics.

- Video Content Overview: The video offers viewers an in-depth analysis of EMCOR, providing valuable insights for potential investors despite the absence of specific stock price data.

- Expert Opinions Summary: The participating experts shared their views on EMCOR's future development, laying a strategic foundation for investors' considerations despite the lack of quantifiable data.

See More

EMCOR Group Reports Record Q1 2026 Earnings Driven by Data Center Demand

- Record Revenue: EMCOR achieved revenues of $4.63 billion in Q1 2026, marking a quarterly record, with operating income reaching $404 million and an operating margin of 8.7%, reflecting strong demand in data centers and digital transformation.

- Strengthened Performance Obligations: By the end of the quarter, EMCOR's remaining performance obligations (RPO) totaled $15.62 billion, significantly increasing from the previous quarter, indicating sustainability in future revenues and robust market demand.

- Raised Full-Year Guidance: Management raised the full-year 2026 revenue guidance to between $18.5 billion and $19.25 billion, with diluted earnings per share expectations increased to between $28.25 and $29.75, demonstrating confidence in maintaining strong operating margins.

- Shareholder Returns: In Q1, EMCOR returned $105 million to shareholders through stock repurchases and quarterly dividends, showcasing the company's commitment to shareholder value while maintaining stable cash flow.

See More

EMCOR Q1 Earnings Exceed Expectations

- Earnings Beat: EMCOR reported a Q1 non-GAAP EPS of $6.84, surpassing expectations by $0.94, which underscores the company's robust profitability in the current economic climate and boosts investor confidence.

- Significant Revenue Growth: The company achieved Q1 revenue of $4.63 billion, reflecting a 19.6% year-over-year increase and exceeding market expectations by $430 million, indicating strong competitive positioning and business expansion capabilities.

- 2026 Revenue Guidance Raised: EMCOR increased its 2026 revenue guidance range from $17.75 billion - $18.50 billion to $18.50 billion - $19.25 billion, surpassing the consensus estimate of $18.14 billion, demonstrating confidence in future growth prospects.

- EPS Guidance Upgrade: The company raised its 2026 diluted EPS guidance from $27.25 - $29.25 to $28.25 - $29.75, aligning with the market consensus of $28.25, reflecting ongoing improvements in its profitability.

See More

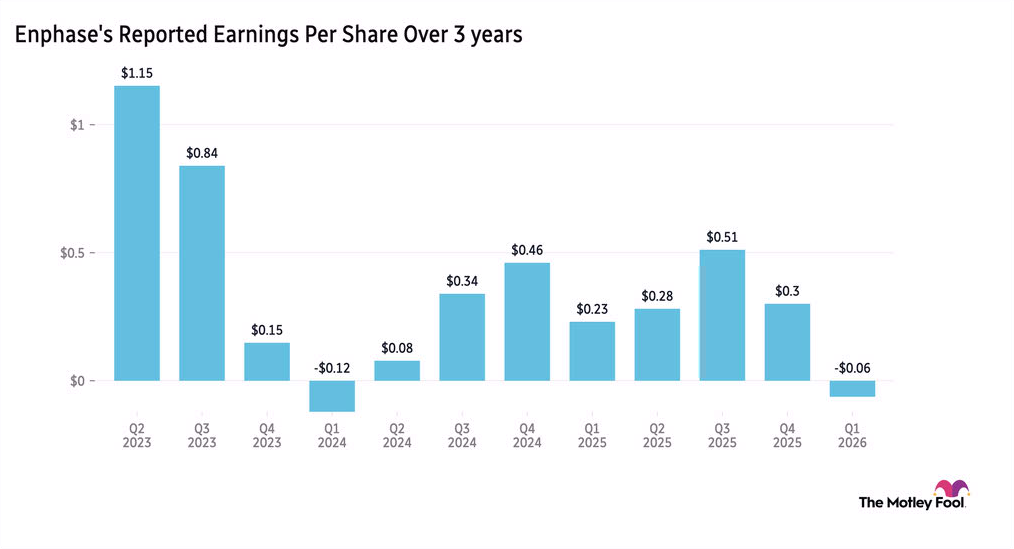

Enphase Energy Drops as Solar Demand Weakens

- Earnings Decline: Enphase Energy reported a 31% year-over-year drop in non-GAAP earnings per share for Q1, leading to a more than 10% decline in pre-market trading, highlighting significant challenges in the U.S. market amid tariff costs and oil-centric energy policies.

- International Market Expansion: Despite domestic struggles, CEO Kothandaraman noted healthy double-digit growth in battery demand across Europe, which is expected to drive revenue growth; however, to combat competition, the company plans to reduce distributor prices for batteries by approximately 10% in May.

- Revenue Outlook: Management anticipates Q2 revenue between $280 million and $310 million, following Q1 revenue of $282.9 million, while maintaining non-GAAP gross margins between 44% and 47%, indicating confidence in the commercialization of next-generation products.

- Intensifying Market Competition: With a prior 20% price reduction on microinverters implemented last December, the upcoming price adjustments may impact short-term margins but could pave the way for long-term market share gains, reflecting the company's adaptability in the rapidly evolving solar market.

See More

Market Highs Analysis and Investment Recommendations

- Electronic Arts Outlook: Despite being renowned for its FIFA and Madden NFL franchises, Electronic Arts (EA) has shown a muted annual revenue growth of only 3% over the past three years, indicating a lag in demand compared to peers, with expectations of continued soft demand over the next 12 months potentially leading to investor losses.

- American Express Global Business Travel Challenges: American Express Global Business Travel (GBTG) has achieved a 12.5% annual revenue growth over the last two years, which is acceptable in absolute terms but tepid for a tech company benefiting from industry tailwinds, and its gross margin of 59% is significantly below competitors, limiting investment in marketing and R&D.

- EMCOR's Strong Performance: EMCOR (EME) has reported an impressive annual revenue growth of 16.3% over the past two years, indicating an increase in market share during this cycle, and its share buybacks have accelerated earnings per share growth, while returns on capital are rising as management makes more lucrative investments.

- Market Sentiment and Investment Risks: While some stocks are nearing their 52-week highs and market sentiment appears positive, short-term trends may lead to investor losses, necessitating a cautious evaluation of investment opportunities, particularly in companies like Electronic Arts and American Express Global Business Travel.

See More

Electrical Infrastructure Firms Thrive Amid Data Center Boom

- Emcor's Strong Performance: Emcor reported record revenue of $4.63 billion in Q1, a 19.7% year-over-year increase, with EPS of $6.84, up 30%, and a backlog of $15.6 billion, up 32.9%, indicating robust demand for high-margin data center projects.

- Schneider's Regional Growth: Schneider Electric's overall revenue rose 4.7% year-over-year to €9.77 billion in Q1, led by a 14.4% increase in North America and a 14.2% rise in China and East Asia, showcasing the effectiveness of its diversified market strategy against regional economic fluctuations.

- Quanta Services' Market Position: Quanta Services reported a record backlog of $39.2 billion in Q1, with revenue of $7.9 billion, up 26%, and EPS of $1.45, up 51%, highlighting its competitive edge in large-scale multi-state transmission projects.

- Investor Attention on Growth Potential: Although these companies are not well-known, their stock prices have surged between 18% and 78% this year, reflecting market recognition of their growth prospects, particularly Emcor's reasonable valuation and Quanta Services' greater long-term growth potential.

See More

Insights into EMCOR's Market Trends and Investment Opportunities

- Market Trend Analysis: In a video published on May 5, 2026, analysts discussed EMCOR's performance in the current market environment, emphasizing attention to future investment opportunities despite the lack of specific data.

- Investment Opportunity Exploration: Experts noted that EMCOR may exhibit growth potential in future markets, providing insights for investors even without concrete financial metrics.

- Video Content Overview: The video offers viewers an in-depth analysis of EMCOR, providing valuable insights for potential investors despite the absence of specific stock price data.

- Expert Opinions Summary: The participating experts shared their views on EMCOR's future development, laying a strategic foundation for investors' considerations despite the lack of quantifiable data.

See More

EMCOR Group Reports Record Q1 2026 Earnings Driven by Data Center Demand

- Record Revenue: EMCOR achieved revenues of $4.63 billion in Q1 2026, marking a quarterly record, with operating income reaching $404 million and an operating margin of 8.7%, reflecting strong demand in data centers and digital transformation.

- Strengthened Performance Obligations: By the end of the quarter, EMCOR's remaining performance obligations (RPO) totaled $15.62 billion, significantly increasing from the previous quarter, indicating sustainability in future revenues and robust market demand.

- Raised Full-Year Guidance: Management raised the full-year 2026 revenue guidance to between $18.5 billion and $19.25 billion, with diluted earnings per share expectations increased to between $28.25 and $29.75, demonstrating confidence in maintaining strong operating margins.

- Shareholder Returns: In Q1, EMCOR returned $105 million to shareholders through stock repurchases and quarterly dividends, showcasing the company's commitment to shareholder value while maintaining stable cash flow.

See More

EMCOR Q1 Earnings Exceed Expectations

- Earnings Beat: EMCOR reported a Q1 non-GAAP EPS of $6.84, surpassing expectations by $0.94, which underscores the company's robust profitability in the current economic climate and boosts investor confidence.

- Significant Revenue Growth: The company achieved Q1 revenue of $4.63 billion, reflecting a 19.6% year-over-year increase and exceeding market expectations by $430 million, indicating strong competitive positioning and business expansion capabilities.

- 2026 Revenue Guidance Raised: EMCOR increased its 2026 revenue guidance range from $17.75 billion - $18.50 billion to $18.50 billion - $19.25 billion, surpassing the consensus estimate of $18.14 billion, demonstrating confidence in future growth prospects.

- EPS Guidance Upgrade: The company raised its 2026 diluted EPS guidance from $27.25 - $29.25 to $28.25 - $29.75, aligning with the market consensus of $28.25, reflecting ongoing improvements in its profitability.

See More

Enphase Energy Drops as Solar Demand Weakens

- Earnings Decline: Enphase Energy reported a 31% year-over-year drop in non-GAAP earnings per share for Q1, leading to a more than 10% decline in pre-market trading, highlighting significant challenges in the U.S. market amid tariff costs and oil-centric energy policies.

- International Market Expansion: Despite domestic struggles, CEO Kothandaraman noted healthy double-digit growth in battery demand across Europe, which is expected to drive revenue growth; however, to combat competition, the company plans to reduce distributor prices for batteries by approximately 10% in May.

- Revenue Outlook: Management anticipates Q2 revenue between $280 million and $310 million, following Q1 revenue of $282.9 million, while maintaining non-GAAP gross margins between 44% and 47%, indicating confidence in the commercialization of next-generation products.

- Intensifying Market Competition: With a prior 20% price reduction on microinverters implemented last December, the upcoming price adjustments may impact short-term margins but could pave the way for long-term market share gains, reflecting the company's adaptability in the rapidly evolving solar market.

See More