DocuSign Q1 Performance Analysis

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Source: stocktwits

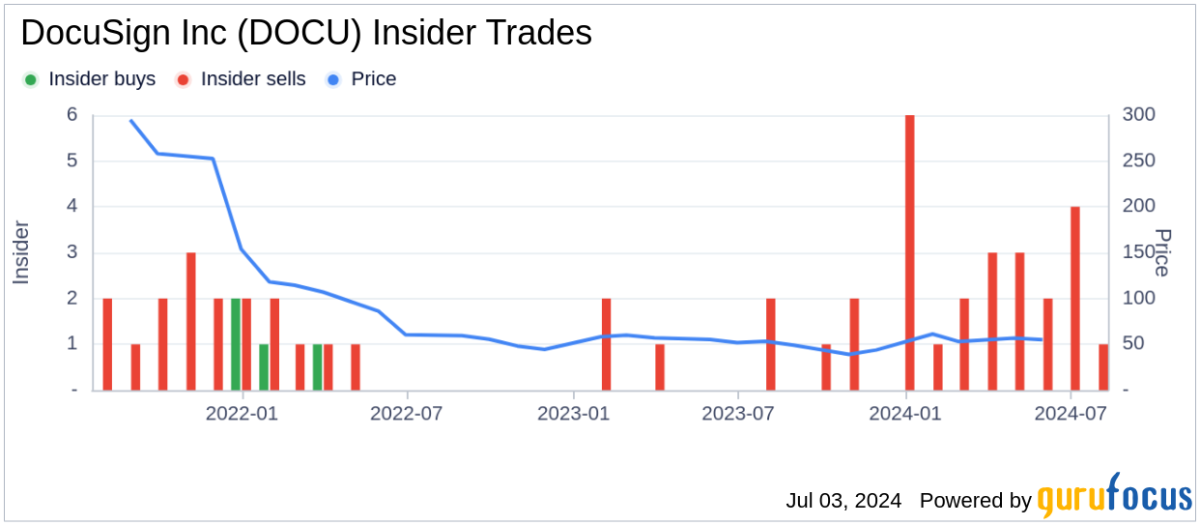

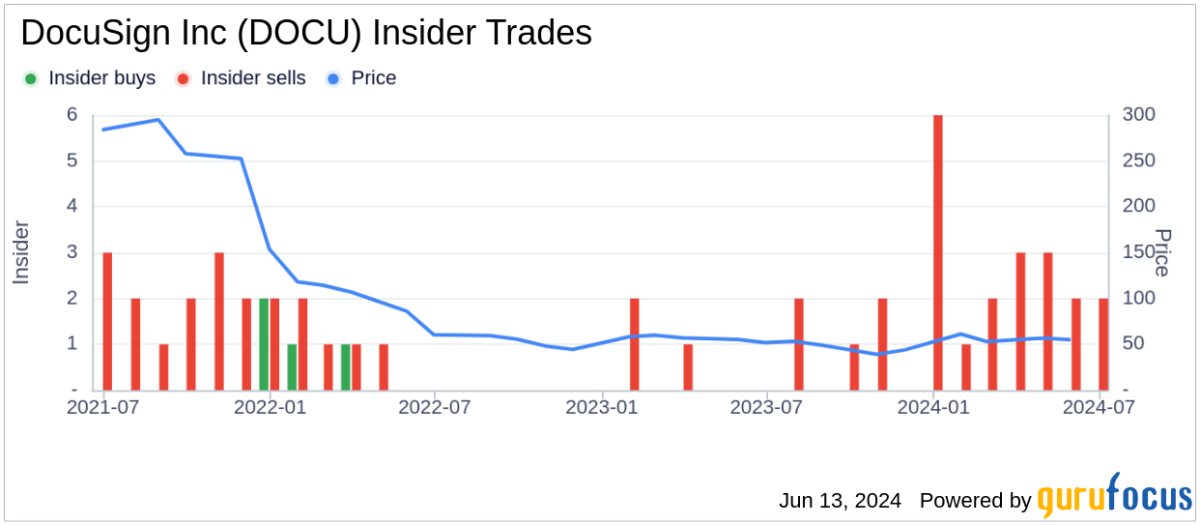

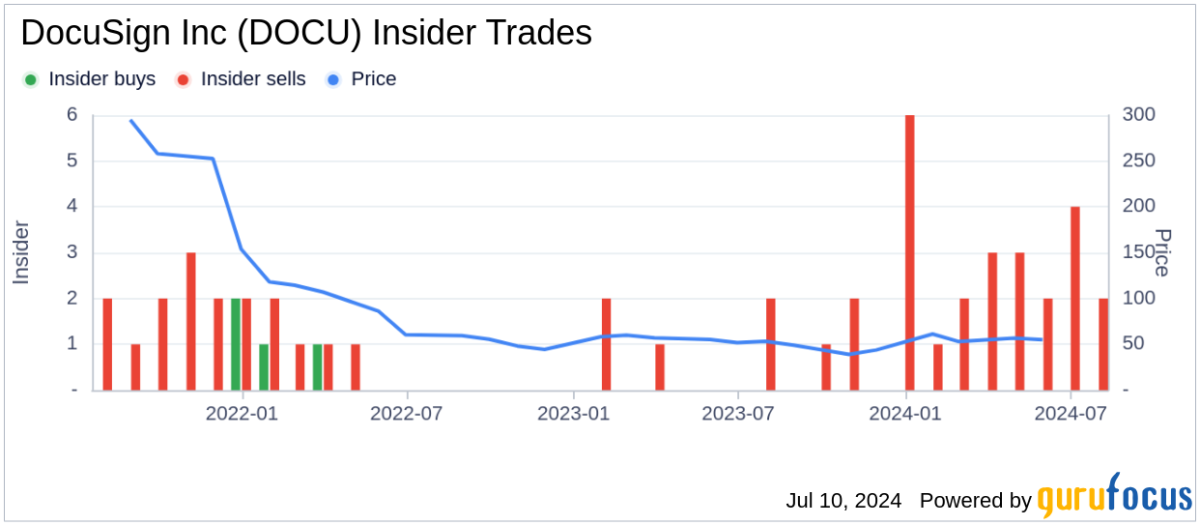

- Performance Overview: DocuSign reported Q1 revenue of $830.2 million, exceeding analyst expectations of $824 million, with adjusted earnings of $1.09 per share surpassing the $0.99 forecast; however, concerns linger over the weak 3% year-over-year billings growth, indicating overall sluggish growth.

- Financial Guidance: The company guided for fiscal year 2027 revenue between $3.49 billion and $3.50 billion, suggesting approximately 9% growth at the midpoint, while annual recurring revenue (ARR) growth is expected to be between 8.25% and 8.75%, highlighting potential for future growth but requiring market validation.

- Market Reaction: Following the earnings report, DocuSign's stock fell 5%, with a cumulative decline of over 11% for the week, reflecting investor caution regarding the sustainability of growth post-IAM (Intelligent Agreement Management) launch.

- Analyst Perspectives: While Jefferies raised its price target to $50 and Citi to $54, Wells Fargo cut its target to $55, indicating a mixed sentiment among analysts who believe the company faces significant growth challenges that could impact its long-term performance.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy DOCU?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on DOCU

Wall Street analysts forecast DOCU stock price to rise

16 Analyst Rating

3 Buy

13 Hold

0 Sell

Hold

Current: 52.400

Low

70.00

Averages

80.23

High

105.00

Current: 52.400

Low

70.00

Averages

80.23

High

105.00

About DOCU

DocuSign, Inc. provides intelligent agreement management (IAM) platform an eSignature solution, and contract lifecycle management (CLM) solution - allow organizations to increase productivity, accelerate contract review cycles, and transform agreement data into insights and actions. The Company’s IAM platform automates agreement workflows, uncovers actionable insights, and leverages artificial intelligence (AI) capabilities, enabling organizations to create, commit, and manage agreements virtually. Its products include eSignature, CLM, IAM Apps, and Add-on Products. Its Add-on Products include Payments to collect payments along with signed agreements; Identity and standards-based signature for enhanced signer-identification and signatures with digital certification; Notary for remote online notarization; Monitor for advanced analytics; Gen for Salesforce for automated agreement generation within Salesforce, among others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Docusign Q1 Results Beat Estimates but Shares Drop

- Earnings Beat: Docusign's Q1 results exceeded market expectations, yet shares fell about 4% in premarket trading, indicating investor concerns regarding future growth, particularly around the uncertainty of annual recurring revenue (ARR) guidance.

- IAM Platform Progress: The company's Intelligent Agreement Management (IAM) cloud platform shows strong growth momentum, expected to reach about 18% of ARR by year-end 2027; however, analysts highlight the opaque economics of IAM, lacking clarity on pricing uplift and annual contract value expansion.

- Analyst Rating Divergence: Morgan Stanley maintains an Equal-weight rating with a $69 price target, while BofA lowers its target to $52, reflecting differing views on the company's growth potential, especially given the uncertainty surrounding IAM's revenue-driving capabilities.

- Uncertain Future Outlook: Despite solid Q1 performance, analysts express caution regarding Docusign's growth trajectory, suggesting that IAM may primarily support customer retention rather than drive revenue acceleration, thereby reducing the likelihood of a market re-rating.

See More

DocuSign Q1 Performance Analysis

- Performance Overview: DocuSign reported Q1 revenue of $830.2 million, exceeding analyst expectations of $824 million, with adjusted earnings of $1.09 per share surpassing the $0.99 forecast; however, concerns linger over the weak 3% year-over-year billings growth, indicating overall sluggish growth.

- Financial Guidance: The company guided for fiscal year 2027 revenue between $3.49 billion and $3.50 billion, suggesting approximately 9% growth at the midpoint, while annual recurring revenue (ARR) growth is expected to be between 8.25% and 8.75%, highlighting potential for future growth but requiring market validation.

- Market Reaction: Following the earnings report, DocuSign's stock fell 5%, with a cumulative decline of over 11% for the week, reflecting investor caution regarding the sustainability of growth post-IAM (Intelligent Agreement Management) launch.

- Analyst Perspectives: While Jefferies raised its price target to $50 and Citi to $54, Wells Fargo cut its target to $55, indicating a mixed sentiment among analysts who believe the company faces significant growth challenges that could impact its long-term performance.

See More

Lululemon Lowers Full-Year Earnings Guidance, Shares Drop

- Lululemon Earnings Decline: Lululemon Athletica's shares fell 13% after the company lowered its full-year earnings and revenue guidance, primarily due to market headwinds, which weakened investor confidence and may impact future sales growth.

- Docusign's Lackluster Outlook: Docusign's stock slipped 4% as its second-quarter revenue forecast of $865 million to $869 million, while in line with consensus, failed to impress analysts, reflecting concerns about its growth potential in a competitive market.

- Chip Stocks Under Pressure: Following Broadcom's earnings report, chip stocks faced renewed selling pressure, with Broadcom down 1% again, and AMD and Intel dropping nearly 3% and over 2.5% respectively, indicating a pessimistic sentiment towards the semiconductor sector's outlook.

- Cooper Companies Beats Expectations: Cooper Companies shares rose nearly 5% after reporting second-quarter adjusted earnings of $1.21 per share, exceeding the $1.10 consensus estimate, and revenue of $1.08 billion, highlighting strong demand in the medical devices sector.

See More

DocuSign (DOCU) Q1 2027 Earnings Transcript

See More

Docusign Reports 9% Revenue Growth in Q1 Earnings

- Revenue Growth: Docusign reported Q1 revenue of $830 million, reflecting a 9% year-over-year increase, demonstrating the company's resilience in the market, although the growth rate was below expectations, it still lays a foundation for future growth.

- Margin Improvement: The company achieved an operating margin of 32% and a free cash flow margin of 35%, supporting a record stock buyback of $318 million, indicating effective capital management strategies.

- Innovative Platform: Docusign's AI-native Intelligent Agreement Management (IAM) platform has attracted 40,000 companies, contributing 12.6% to annual recurring revenue, showcasing its innovative capabilities and growth potential in the market.

- Market Recognition: Docusign has been recognized by Fast Company as one of the Most Innovative Companies and by Newsweek as one of the most trusted software companies, further solidifying its market position in the agreement management space.

See More

Docusign Q1 Earnings: Strong Growth in IAM Platform

- Revenue Growth: Docusign reported Q1 revenue of $830 million, reflecting a 9% year-over-year increase, with approximately 1.6 percentage points attributed to foreign exchange rates, indicating strong performance in international markets that is expected to drive ongoing growth.

- IAM Platform Expansion: The IAM platform's contribution to total annual recurring revenue rose from 10.8% last quarter to 12.6%, with expectations to reach 18% by the end of fiscal 2027, showcasing the company's success in driving product innovation and market penetration.

- Share Buyback Activity: The company repurchased $318 million in shares during Q1, demonstrating strong cash flow and capital management capabilities, which further enhances shareholder value while maintaining approximately $1 billion in cash reserves.

- Management Changes: The appointment of Graham Sheldon as the new Chief Product Officer signifies a new direction in product strategy, while acknowledging the contributions of outgoing Chief Product Officer Dmitri Krakovsky reflects the company's commitment to continuous innovation and leadership.

See More

Docusign Q1 Results Beat Estimates but Shares Drop

- Earnings Beat: Docusign's Q1 results exceeded market expectations, yet shares fell about 4% in premarket trading, indicating investor concerns regarding future growth, particularly around the uncertainty of annual recurring revenue (ARR) guidance.

- IAM Platform Progress: The company's Intelligent Agreement Management (IAM) cloud platform shows strong growth momentum, expected to reach about 18% of ARR by year-end 2027; however, analysts highlight the opaque economics of IAM, lacking clarity on pricing uplift and annual contract value expansion.

- Analyst Rating Divergence: Morgan Stanley maintains an Equal-weight rating with a $69 price target, while BofA lowers its target to $52, reflecting differing views on the company's growth potential, especially given the uncertainty surrounding IAM's revenue-driving capabilities.

- Uncertain Future Outlook: Despite solid Q1 performance, analysts express caution regarding Docusign's growth trajectory, suggesting that IAM may primarily support customer retention rather than drive revenue acceleration, thereby reducing the likelihood of a market re-rating.

See More

DocuSign Q1 Performance Analysis

- Performance Overview: DocuSign reported Q1 revenue of $830.2 million, exceeding analyst expectations of $824 million, with adjusted earnings of $1.09 per share surpassing the $0.99 forecast; however, concerns linger over the weak 3% year-over-year billings growth, indicating overall sluggish growth.

- Financial Guidance: The company guided for fiscal year 2027 revenue between $3.49 billion and $3.50 billion, suggesting approximately 9% growth at the midpoint, while annual recurring revenue (ARR) growth is expected to be between 8.25% and 8.75%, highlighting potential for future growth but requiring market validation.

- Market Reaction: Following the earnings report, DocuSign's stock fell 5%, with a cumulative decline of over 11% for the week, reflecting investor caution regarding the sustainability of growth post-IAM (Intelligent Agreement Management) launch.

- Analyst Perspectives: While Jefferies raised its price target to $50 and Citi to $54, Wells Fargo cut its target to $55, indicating a mixed sentiment among analysts who believe the company faces significant growth challenges that could impact its long-term performance.

See More

Lululemon Lowers Full-Year Earnings Guidance, Shares Drop

- Lululemon Earnings Decline: Lululemon Athletica's shares fell 13% after the company lowered its full-year earnings and revenue guidance, primarily due to market headwinds, which weakened investor confidence and may impact future sales growth.

- Docusign's Lackluster Outlook: Docusign's stock slipped 4% as its second-quarter revenue forecast of $865 million to $869 million, while in line with consensus, failed to impress analysts, reflecting concerns about its growth potential in a competitive market.

- Chip Stocks Under Pressure: Following Broadcom's earnings report, chip stocks faced renewed selling pressure, with Broadcom down 1% again, and AMD and Intel dropping nearly 3% and over 2.5% respectively, indicating a pessimistic sentiment towards the semiconductor sector's outlook.

- Cooper Companies Beats Expectations: Cooper Companies shares rose nearly 5% after reporting second-quarter adjusted earnings of $1.21 per share, exceeding the $1.10 consensus estimate, and revenue of $1.08 billion, highlighting strong demand in the medical devices sector.

See More

DocuSign (DOCU) Q1 2027 Earnings Transcript

See More

Docusign Reports 9% Revenue Growth in Q1 Earnings

- Revenue Growth: Docusign reported Q1 revenue of $830 million, reflecting a 9% year-over-year increase, demonstrating the company's resilience in the market, although the growth rate was below expectations, it still lays a foundation for future growth.

- Margin Improvement: The company achieved an operating margin of 32% and a free cash flow margin of 35%, supporting a record stock buyback of $318 million, indicating effective capital management strategies.

- Innovative Platform: Docusign's AI-native Intelligent Agreement Management (IAM) platform has attracted 40,000 companies, contributing 12.6% to annual recurring revenue, showcasing its innovative capabilities and growth potential in the market.

- Market Recognition: Docusign has been recognized by Fast Company as one of the Most Innovative Companies and by Newsweek as one of the most trusted software companies, further solidifying its market position in the agreement management space.

See More

Docusign Q1 Earnings: Strong Growth in IAM Platform

- Revenue Growth: Docusign reported Q1 revenue of $830 million, reflecting a 9% year-over-year increase, with approximately 1.6 percentage points attributed to foreign exchange rates, indicating strong performance in international markets that is expected to drive ongoing growth.

- IAM Platform Expansion: The IAM platform's contribution to total annual recurring revenue rose from 10.8% last quarter to 12.6%, with expectations to reach 18% by the end of fiscal 2027, showcasing the company's success in driving product innovation and market penetration.

- Share Buyback Activity: The company repurchased $318 million in shares during Q1, demonstrating strong cash flow and capital management capabilities, which further enhances shareholder value while maintaining approximately $1 billion in cash reserves.

- Management Changes: The appointment of Graham Sheldon as the new Chief Product Officer signifies a new direction in product strategy, while acknowledging the contributions of outgoing Chief Product Officer Dmitri Krakovsky reflects the company's commitment to continuous innovation and leadership.

See More