Biohaven Reports New Clinical Data on Opakalim for Epilepsy Treatment

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 48 minutes ago

0mins

Source: Newsfilter

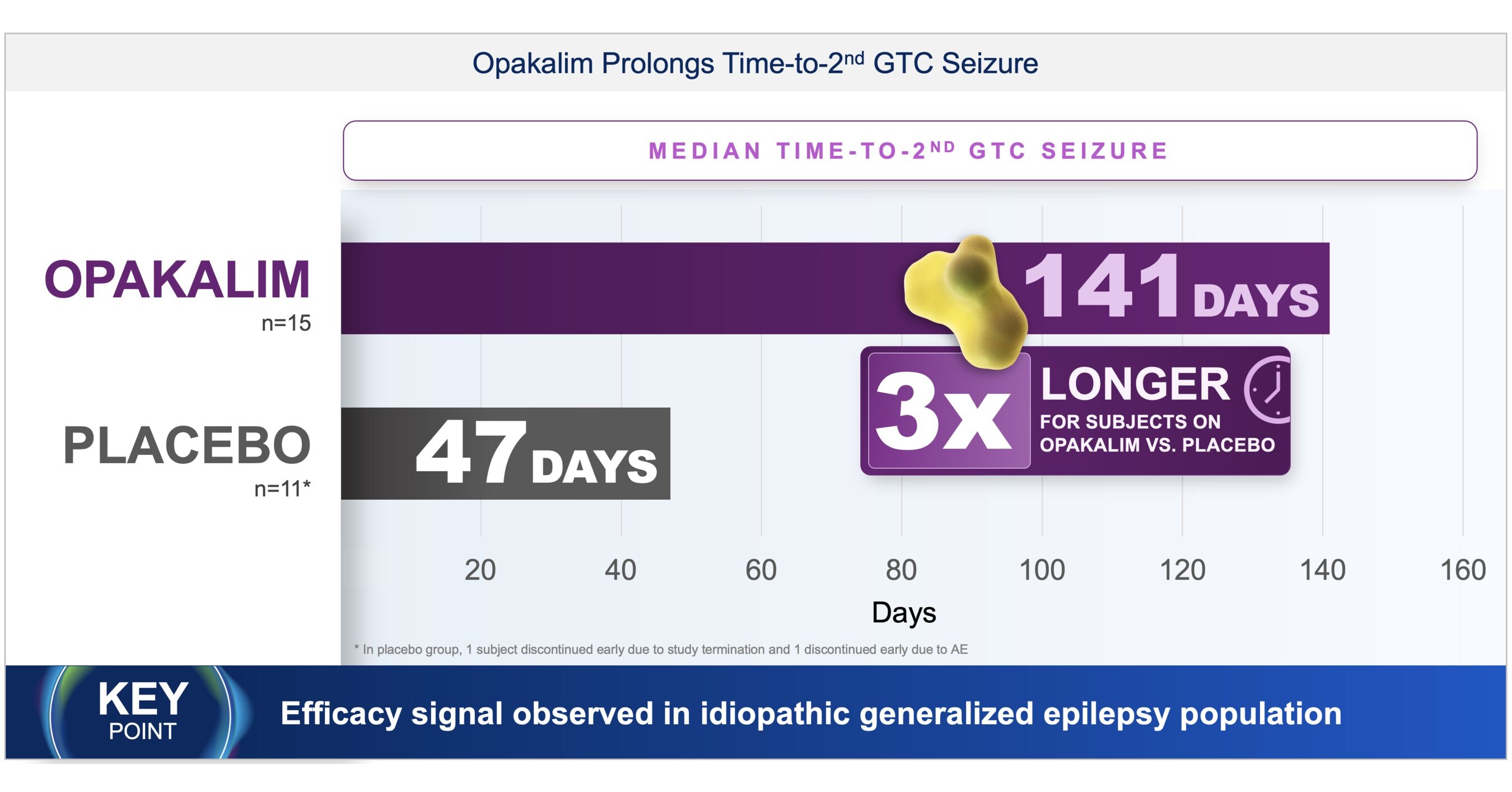

- Breakthrough in Epilepsy Treatment: In a randomized controlled trial, the median time to the second generalized tonic-clonic seizure was 141 days for the Opakalim 75 mg once-daily group compared to 47 days for the placebo group, indicating a threefold prolongation and highlighting its potential in treating refractory epilepsy.

- Significant Efficacy: In an ongoing open-label extension study, 54% of patients with focal epilepsy achieved a ≥50% reduction in seizure frequency on Opakalim, demonstrating comparable efficacy to other Kv7 activators but with significantly lower side effects.

- Safety Advantage: Opakalim has shown excellent tolerability across studies, with over 1,000 subjects reporting adverse event rates below 5%, marking a significant improvement over other antiseizure medications in terms of central nervous system side effects.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 trials in the second half of 2026, which will support the registration of Opakalim and further solidify its market position in epilepsy treatment.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BHVN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BHVN

Wall Street analysts forecast BHVN stock price to rise

13 Analyst Rating

9 Buy

4 Hold

0 Sell

Moderate Buy

Current: 9.480

Low

11.00

Averages

18.00

High

30.00

Current: 9.480

Low

11.00

Averages

18.00

High

30.00

About BHVN

Biohaven Ltd. is a biopharmaceutical company focused on the discovery, development and commercialization of treatments in key therapeutic areas, including immunology, neuroscience, and oncology. It is advancing its portfolio of therapeutics, leveraging its drug development experience and multiple proprietary drug development platforms. Its clinical and preclinical programs include Kv7 ion channel modulation for epilepsy; Molecular Degrader of Extracellular Proteins (MoDE) and Targeted Removal of Aberrant Protein (TRAP) extracellular protein degradation for immunological diseases; and myostatin-activin pathway targeting agent for neuromuscular and metabolic diseases, including obesity. Its pipeline includes TYK2/JAK1 Inhibitor (brain-penetrant), IgG Degrader, Gd-IgA1 TRAP Degrader, Taldefgrobep Alfa, Kv7 Activator, TRPM3 Antagonist FGFR3 ADC, CD30 ADC, Trop2 ADC +/- PD1, and others. Its advanced product candidate from its glutamate receptor antagonist platform is troriluzole.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Biohaven Reports New Data on Opakalim for Epilepsy Treatment

- Clinical Trial Progress: Biohaven will present new data on Opakalim's Phase 2/3 studies for focal epilepsy at its upcoming R&D Day, indicating its potential to provide more effective treatment options for patients in seizure control.

- Safety Advantages: Opakalim demonstrated zero rates of somnolence, dizziness, and fatigue in a small proof-of-concept study, suggesting that its selective Kv7.2/7.3 activation mechanism may offer better tolerability, enhancing patients' quality of life.

- Patient Case Update: A 9-year-old patient with KCNQ2-DEE showed seizure control after transitioning to Opakalim, highlighting the drug's efficacy in treatment-resistant epilepsy patients and supporting its clinical application potential.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 randomized double-blind studies in the second half of 2026, aiming to support Opakalim's registration and advance its commercialization efforts.

See More

Biohaven Reports New Clinical Data on Opakalim for Epilepsy Treatment

- Breakthrough in Epilepsy Treatment: In a randomized controlled trial, the median time to the second generalized tonic-clonic seizure was 141 days for the Opakalim 75 mg once-daily group compared to 47 days for the placebo group, indicating a threefold prolongation and highlighting its potential in treating refractory epilepsy.

- Significant Efficacy: In an ongoing open-label extension study, 54% of patients with focal epilepsy achieved a ≥50% reduction in seizure frequency on Opakalim, demonstrating comparable efficacy to other Kv7 activators but with significantly lower side effects.

- Safety Advantage: Opakalim has shown excellent tolerability across studies, with over 1,000 subjects reporting adverse event rates below 5%, marking a significant improvement over other antiseizure medications in terms of central nervous system side effects.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 trials in the second half of 2026, which will support the registration of Opakalim and further solidify its market position in epilepsy treatment.

See More

Biohaven Q1 Earnings Miss Expectations

- Earnings Miss: Biohaven reported a Q1 GAAP EPS of -$0.88, missing expectations by $0.04, indicating challenges in profitability that could undermine investor confidence.

- Cash Position: As of March 31, 2026, Biohaven's cash, cash equivalents, marketable securities, and restricted cash totaled approximately $351.8 million, providing some liquidity but necessitating scrutiny on future capital efficiency.

- Rating Downgrade Impact: The stock was downgraded to 'Hold' due to setbacks with Troriluzole and potential implications from obesity data expected in the second half of 2026, prompting a reassessment of the company's growth prospects.

- Market Reaction Outlook: Analysts' quant ratings reflect a cautious stance on Biohaven's future performance, urging investors to closely monitor subsequent financial and R&D developments to evaluate long-term investment value.

See More

Biohaven Stock Surges 10.14% Following Analyst Buy Rating

- Analyst Strong Buy: Sumant Kulkami from Canaccord Genuity initiated coverage on Biohaven with a bullish buy rating and a price target of $21 per share, indicating a potential upside of over 100% from current levels, reflecting strong confidence in the company's growth prospects.

- Clinical Trial Progress: Biohaven's drug Opakalim is currently in phase 3 clinical testing for epilepsy, and Kulkami expressed satisfaction with its performance, suggesting significant potential for commercialization in the near future, which could enhance the company's market position.

- Positive Market Reaction: Following the analyst's report, Biohaven's stock surged over 10% in a single trading session, indicating investor optimism about the company's future and heightened expectations surrounding its clinical trial outcomes.

- Favorable Investment Timing: Kulkami believes that now is an opportune time to buy Biohaven shares, especially ahead of the anticipated clinical trial results, which could lead to substantial returns for investors if the outcomes are favorable.

See More

Biohaven Shares Enter Oversold Territory

- Oversold Signal: Biohaven Ltd (Ticker: BHVN) saw its RSI drop to 29.9 during Tuesday's trading, indicating an oversold condition as shares hit a low of $8.28, suggesting that recent heavy selling may be nearing exhaustion, prompting bullish investors to seek buying opportunities.

- Market Comparison: Compared to the current RSI of 38.6 for the S&P 500 ETF (SPY), BHVN's 29.9 RSI indicates relative weakness, potentially attracting investors looking for a rebound, especially amid increasing market volatility.

- Price Fluctuation: BHVN's 52-week low stands at $7.48 per share, with a high of $31.18, while the latest trade price is $8.39, indicating that the stock is hovering at low levels, which may present potential buying opportunities for investors.

- Investor Sentiment: Despite the current low stock price, investors should carefully assess market sentiment and fundamental factors to determine whether to invest under the oversold signal, avoiding potential risks.

See More

Sarissa Capital Management Acquires Stake in Biohaven Ltd.

- New Investment Position: Sarissa Capital Management established a new position in Biohaven Ltd. (BHVN) during Q4 2026 by acquiring 513,184 shares valued at approximately $5.79 million, indicating a strategic move into the biopharmaceutical sector.

- Increased Ownership Percentage: This acquisition brings Biohaven to 2.6% of Sarissa's reportable U.S. equity AUM, reflecting a strategic emphasis on the company despite its stock price plummeting 70% over the past year.

- Financial Condition Overview: Biohaven ended 2025 with around $322 million in cash and raised an additional $178.9 million post-year-end, maintaining a relatively stable financial position despite facing FDA rejections and disappointing trial results.

- Future Growth Potential: Biohaven is focusing on late-stage programs, including a Phase 2 obesity candidate, with data expected in the second half of 2026, which could provide new growth momentum if successful.

See More

Biohaven Reports New Data on Opakalim for Epilepsy Treatment

- Clinical Trial Progress: Biohaven will present new data on Opakalim's Phase 2/3 studies for focal epilepsy at its upcoming R&D Day, indicating its potential to provide more effective treatment options for patients in seizure control.

- Safety Advantages: Opakalim demonstrated zero rates of somnolence, dizziness, and fatigue in a small proof-of-concept study, suggesting that its selective Kv7.2/7.3 activation mechanism may offer better tolerability, enhancing patients' quality of life.

- Patient Case Update: A 9-year-old patient with KCNQ2-DEE showed seizure control after transitioning to Opakalim, highlighting the drug's efficacy in treatment-resistant epilepsy patients and supporting its clinical application potential.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 randomized double-blind studies in the second half of 2026, aiming to support Opakalim's registration and advance its commercialization efforts.

See More

Biohaven Reports New Clinical Data on Opakalim for Epilepsy Treatment

- Breakthrough in Epilepsy Treatment: In a randomized controlled trial, the median time to the second generalized tonic-clonic seizure was 141 days for the Opakalim 75 mg once-daily group compared to 47 days for the placebo group, indicating a threefold prolongation and highlighting its potential in treating refractory epilepsy.

- Significant Efficacy: In an ongoing open-label extension study, 54% of patients with focal epilepsy achieved a ≥50% reduction in seizure frequency on Opakalim, demonstrating comparable efficacy to other Kv7 activators but with significantly lower side effects.

- Safety Advantage: Opakalim has shown excellent tolerability across studies, with over 1,000 subjects reporting adverse event rates below 5%, marking a significant improvement over other antiseizure medications in terms of central nervous system side effects.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 trials in the second half of 2026, which will support the registration of Opakalim and further solidify its market position in epilepsy treatment.

See More

Biohaven Q1 Earnings Miss Expectations

- Earnings Miss: Biohaven reported a Q1 GAAP EPS of -$0.88, missing expectations by $0.04, indicating challenges in profitability that could undermine investor confidence.

- Cash Position: As of March 31, 2026, Biohaven's cash, cash equivalents, marketable securities, and restricted cash totaled approximately $351.8 million, providing some liquidity but necessitating scrutiny on future capital efficiency.

- Rating Downgrade Impact: The stock was downgraded to 'Hold' due to setbacks with Troriluzole and potential implications from obesity data expected in the second half of 2026, prompting a reassessment of the company's growth prospects.

- Market Reaction Outlook: Analysts' quant ratings reflect a cautious stance on Biohaven's future performance, urging investors to closely monitor subsequent financial and R&D developments to evaluate long-term investment value.

See More

Biohaven Stock Surges 10.14% Following Analyst Buy Rating

- Analyst Strong Buy: Sumant Kulkami from Canaccord Genuity initiated coverage on Biohaven with a bullish buy rating and a price target of $21 per share, indicating a potential upside of over 100% from current levels, reflecting strong confidence in the company's growth prospects.

- Clinical Trial Progress: Biohaven's drug Opakalim is currently in phase 3 clinical testing for epilepsy, and Kulkami expressed satisfaction with its performance, suggesting significant potential for commercialization in the near future, which could enhance the company's market position.

- Positive Market Reaction: Following the analyst's report, Biohaven's stock surged over 10% in a single trading session, indicating investor optimism about the company's future and heightened expectations surrounding its clinical trial outcomes.

- Favorable Investment Timing: Kulkami believes that now is an opportune time to buy Biohaven shares, especially ahead of the anticipated clinical trial results, which could lead to substantial returns for investors if the outcomes are favorable.

See More

Biohaven Shares Enter Oversold Territory

- Oversold Signal: Biohaven Ltd (Ticker: BHVN) saw its RSI drop to 29.9 during Tuesday's trading, indicating an oversold condition as shares hit a low of $8.28, suggesting that recent heavy selling may be nearing exhaustion, prompting bullish investors to seek buying opportunities.

- Market Comparison: Compared to the current RSI of 38.6 for the S&P 500 ETF (SPY), BHVN's 29.9 RSI indicates relative weakness, potentially attracting investors looking for a rebound, especially amid increasing market volatility.

- Price Fluctuation: BHVN's 52-week low stands at $7.48 per share, with a high of $31.18, while the latest trade price is $8.39, indicating that the stock is hovering at low levels, which may present potential buying opportunities for investors.

- Investor Sentiment: Despite the current low stock price, investors should carefully assess market sentiment and fundamental factors to determine whether to invest under the oversold signal, avoiding potential risks.

See More

Sarissa Capital Management Acquires Stake in Biohaven Ltd.

- New Investment Position: Sarissa Capital Management established a new position in Biohaven Ltd. (BHVN) during Q4 2026 by acquiring 513,184 shares valued at approximately $5.79 million, indicating a strategic move into the biopharmaceutical sector.

- Increased Ownership Percentage: This acquisition brings Biohaven to 2.6% of Sarissa's reportable U.S. equity AUM, reflecting a strategic emphasis on the company despite its stock price plummeting 70% over the past year.

- Financial Condition Overview: Biohaven ended 2025 with around $322 million in cash and raised an additional $178.9 million post-year-end, maintaining a relatively stable financial position despite facing FDA rejections and disappointing trial results.

- Future Growth Potential: Biohaven is focusing on late-stage programs, including a Phase 2 obesity candidate, with data expected in the second half of 2026, which could provide new growth momentum if successful.

See More