AppLovin Shows Strong Financials Amid Regulatory Scrutiny

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 42 minutes ago

0mins

Should l Buy APP?

Source: NASDAQ.COM

- Significant Financial Growth: AppLovin reported nearly $2 billion in revenue for Q1, reflecting a 59% year-over-year increase, demonstrating strong performance in the advertising market despite pressures from short-seller reports.

- Rising Profit Margins: The company achieved a net profit margin of 65.4% in Q1, consistently exceeding 60% over the past year, indicating enhanced profitability that could lay the groundwork for future stock price increases.

- Rapid Market Share Expansion: AppLovin is gaining ad market share faster than both Alphabet and Meta Platforms, and while its total revenue remains significantly lower than these giants, its rapid growth trend may attract more investor interest.

- Regulatory Investigation Risks: Despite strong fundamentals, AppLovin faces an ongoing SEC probe, and if the investigation reveals illegal practices in its business model, it could have a substantial negative impact on its stock price.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy APP?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on APP

Wall Street analysts forecast APP stock price to rise

15 Analyst Rating

15 Buy

0 Hold

0 Sell

Strong Buy

Current: 492.380

Low

465.00

Averages

745.50

High

860.00

Current: 492.380

Low

465.00

Averages

745.50

High

860.00

About APP

AppLovin Corporation is a marketing platform. The Company provides end-to-end software and artificial intelligence (AI) solutions for businesses to reach, monetize and grow their global audiences. Its advertising solutions include a comprehensive suite of tools including AppDiscovery, MAX, Adjust, Wurl and Axon Ads Manager. AppDiscovery is powered by AXON, its AI-powered advertising engine, and matches advertiser demand with publisher supply through auctions at vast scale and at microsecond-level speeds. MAX is its monetization solution, utilizing an advanced in-app bidding technology that optimizes the value of a publisher’s advertising inventory by running a real-time competitive auction, driving more competition, and higher returns for publishers. Adjust is its measurement and analytics marketing platform which provides marketers with the visibility, insights, and data needed to scale their apps marketing and drive more informed results. Wurl is its connected TV (CTV) platform.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

AppLovin Shows Strong Financials Amid Regulatory Scrutiny

- Significant Financial Growth: AppLovin reported nearly $2 billion in revenue for Q1, reflecting a 59% year-over-year increase, demonstrating strong performance in the advertising market despite pressures from short-seller reports.

- Rising Profit Margins: The company achieved a net profit margin of 65.4% in Q1, consistently exceeding 60% over the past year, indicating enhanced profitability that could lay the groundwork for future stock price increases.

- Rapid Market Share Expansion: AppLovin is gaining ad market share faster than both Alphabet and Meta Platforms, and while its total revenue remains significantly lower than these giants, its rapid growth trend may attract more investor interest.

- Regulatory Investigation Risks: Despite strong fundamentals, AppLovin faces an ongoing SEC probe, and if the investigation reveals illegal practices in its business model, it could have a substantial negative impact on its stock price.

See More

AppLovin's Stock Volatility and Growth Potential

- Short-Term Volatility: AppLovin's stock has dropped approximately 27% year-to-date, yet it has achieved a remarkable 687% gain over the past five years, highlighting the contrast between short-term fluctuations and long-term growth, which may affect investor confidence.

- Short-Selling Pressure: Recent reports from multiple short-sellers have raised concerns about AppLovin's operations, alleging money laundering, although the company has denied these claims and demanded retractions, indicating market apprehension regarding its compliance.

- Strong Financial Performance: In Q1, AppLovin achieved a net profit margin of 65.4% with revenues nearing $2 billion, and while it still lags behind Meta and Alphabet, its faster growth rate suggests improving profitability.

- Future Growth Potential: As AppLovin continues to scale, its Q1 costs increased only 26.2% year-over-year, and if revenue growth remains high, profit margins are likely to expand further, enhancing its competitive position in the market.

See More

Microsoft and AppLovin: Growth Stocks Poised for Spring Surge

- Strong Cloud Performance: Microsoft's Azure cloud business achieved a 40% revenue growth last quarter, marking its eleventh consecutive quarter of over 30% growth, indicating a solid foundation for future expansion in the cloud computing sector.

- AI Revenue Surge: The company's artificial intelligence annual recurring revenue (ARR) skyrocketed by 123%, while the usage of its GitHub solutions is rapidly increasing, with expectations that the new usage-based pricing model will further drive revenue growth and enhance market competitiveness.

- AppLovin's Growth Momentum: AppLovin reported a 59% revenue surge to $1.84 billion in the latest quarter, with adjusted EBITDA soaring 66% to $1.56 billion, showcasing its strong performance and efficient operations in the adtech space, which is likely to continue attracting investor interest.

- New Opportunities from Platform Opening: AppLovin plans to launch a self-service platform in June, allowing smaller advertisers to utilize its ad technology, a strategic shift that is expected to expand market share and drive growth beyond its core gaming vertical.

See More

Applovin Emerges as Most Profitable Company

- Profitability Highlight: Applovin's stock price surged by 7.05% on May 12, 2026, indicating its strong profitability in the industry and further solidifying its market leadership.

- Increased Market Attention: With Applovin recognized as the most profitable company, investor interest in its future growth potential has significantly risen, potentially attracting more capital inflows.

- Enhanced Industry Influence: Applovin's impressive earnings not only boost its own market valuation but may also pressure competitors in the industry to improve operational efficiency to remain competitive.

- Strategic Growth Outlook: As the most profitable company, Applovin is likely to leverage its financial strength for more strategic investments and expansions, thereby further enhancing its market share and industry influence.

See More

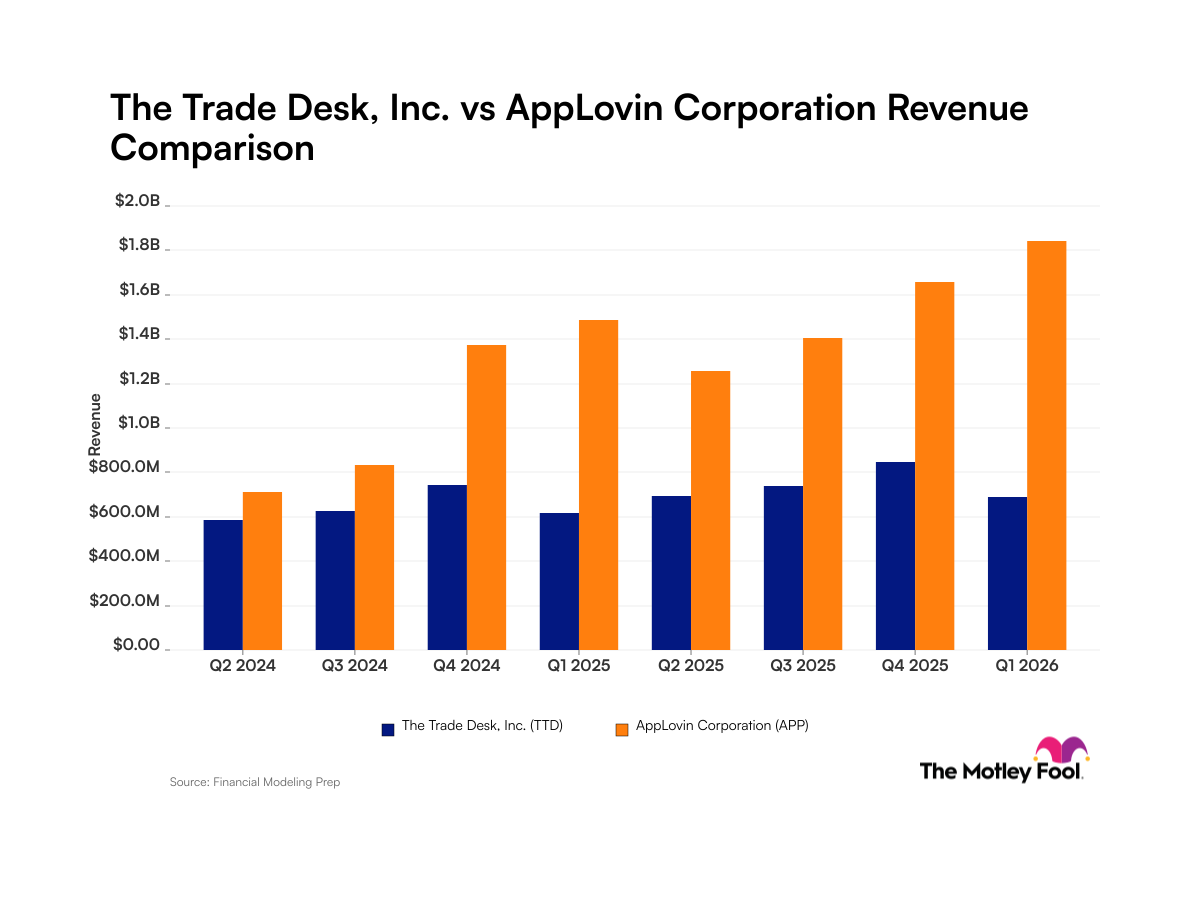

Quarterly Revenue Comparison: The Trade Desk vs. AppLovin

- Trade Desk Revenue Performance: For the quarter ending March 31, 2026, The Trade Desk reported a net income margin of 6%, with Q1 revenue reaching $689 million, reflecting a 12% year-over-year growth despite facing an investigation regarding its previous guidance, indicating stable growth potential.

- AppLovin Revenue Growth: AppLovin achieved $1.8 billion in revenue for Q1 2026, representing a remarkable 59% year-over-year increase, with net income soaring to $1.2 billion, nearly double the prior year's $576.4 million, showcasing its significant market appeal.

- Seasonal Revenue Trends: The Trade Desk typically sees its revenue peak in Q4 due to increased advertiser spending during the holiday season, while AppLovin demonstrated consistent quarter-over-quarter growth in Q1, breaking the typical industry seasonality pattern.

- Investor Considerations: For investors, AppLovin's robust sales growth positions it as a more attractive option in the digital advertising space, while The Trade Desk's stable growth, though positive, may not match AppLovin's expansion pace, potentially influencing investment decisions.

See More

AppLovin Reports Strong Q1 Growth, Stock Potential Looks Promising

- Significant Revenue Growth: AppLovin reported a remarkable 59% year-over-year revenue increase to $1.84 billion in Q1 2023, indicating the successful impact of its Axon 2.0 engine on business expansion and enhancing its competitive position in the market.

- Profitability Improvement: The adjusted EBITDA margin rose by 400 basis points to 85%, with earnings per share soaring 70% from $2.10 last year to $3.56, showcasing the company's strong performance in profitability.

- Cash Flow and Buybacks: The company generated $1.3 billion in free cash flow during the quarter and repurchased 2.2 million shares worth $1 billion, which not only enhances shareholder returns but also reflects confidence in future growth prospects.

- Optimistic Future Outlook: Management projected Q2 revenue to range between $1.915 billion and $1.945 billion, representing a growth rate of 52% to 55%, indicating that the company's strategic initiatives to expand market opportunities and broaden its advertising customer base will continue to drive growth.

See More

AppLovin Shows Strong Financials Amid Regulatory Scrutiny

- Significant Financial Growth: AppLovin reported nearly $2 billion in revenue for Q1, reflecting a 59% year-over-year increase, demonstrating strong performance in the advertising market despite pressures from short-seller reports.

- Rising Profit Margins: The company achieved a net profit margin of 65.4% in Q1, consistently exceeding 60% over the past year, indicating enhanced profitability that could lay the groundwork for future stock price increases.

- Rapid Market Share Expansion: AppLovin is gaining ad market share faster than both Alphabet and Meta Platforms, and while its total revenue remains significantly lower than these giants, its rapid growth trend may attract more investor interest.

- Regulatory Investigation Risks: Despite strong fundamentals, AppLovin faces an ongoing SEC probe, and if the investigation reveals illegal practices in its business model, it could have a substantial negative impact on its stock price.

See More

AppLovin's Stock Volatility and Growth Potential

- Short-Term Volatility: AppLovin's stock has dropped approximately 27% year-to-date, yet it has achieved a remarkable 687% gain over the past five years, highlighting the contrast between short-term fluctuations and long-term growth, which may affect investor confidence.

- Short-Selling Pressure: Recent reports from multiple short-sellers have raised concerns about AppLovin's operations, alleging money laundering, although the company has denied these claims and demanded retractions, indicating market apprehension regarding its compliance.

- Strong Financial Performance: In Q1, AppLovin achieved a net profit margin of 65.4% with revenues nearing $2 billion, and while it still lags behind Meta and Alphabet, its faster growth rate suggests improving profitability.

- Future Growth Potential: As AppLovin continues to scale, its Q1 costs increased only 26.2% year-over-year, and if revenue growth remains high, profit margins are likely to expand further, enhancing its competitive position in the market.

See More

Microsoft and AppLovin: Growth Stocks Poised for Spring Surge

- Strong Cloud Performance: Microsoft's Azure cloud business achieved a 40% revenue growth last quarter, marking its eleventh consecutive quarter of over 30% growth, indicating a solid foundation for future expansion in the cloud computing sector.

- AI Revenue Surge: The company's artificial intelligence annual recurring revenue (ARR) skyrocketed by 123%, while the usage of its GitHub solutions is rapidly increasing, with expectations that the new usage-based pricing model will further drive revenue growth and enhance market competitiveness.

- AppLovin's Growth Momentum: AppLovin reported a 59% revenue surge to $1.84 billion in the latest quarter, with adjusted EBITDA soaring 66% to $1.56 billion, showcasing its strong performance and efficient operations in the adtech space, which is likely to continue attracting investor interest.

- New Opportunities from Platform Opening: AppLovin plans to launch a self-service platform in June, allowing smaller advertisers to utilize its ad technology, a strategic shift that is expected to expand market share and drive growth beyond its core gaming vertical.

See More

Applovin Emerges as Most Profitable Company

- Profitability Highlight: Applovin's stock price surged by 7.05% on May 12, 2026, indicating its strong profitability in the industry and further solidifying its market leadership.

- Increased Market Attention: With Applovin recognized as the most profitable company, investor interest in its future growth potential has significantly risen, potentially attracting more capital inflows.

- Enhanced Industry Influence: Applovin's impressive earnings not only boost its own market valuation but may also pressure competitors in the industry to improve operational efficiency to remain competitive.

- Strategic Growth Outlook: As the most profitable company, Applovin is likely to leverage its financial strength for more strategic investments and expansions, thereby further enhancing its market share and industry influence.

See More

Quarterly Revenue Comparison: The Trade Desk vs. AppLovin

- Trade Desk Revenue Performance: For the quarter ending March 31, 2026, The Trade Desk reported a net income margin of 6%, with Q1 revenue reaching $689 million, reflecting a 12% year-over-year growth despite facing an investigation regarding its previous guidance, indicating stable growth potential.

- AppLovin Revenue Growth: AppLovin achieved $1.8 billion in revenue for Q1 2026, representing a remarkable 59% year-over-year increase, with net income soaring to $1.2 billion, nearly double the prior year's $576.4 million, showcasing its significant market appeal.

- Seasonal Revenue Trends: The Trade Desk typically sees its revenue peak in Q4 due to increased advertiser spending during the holiday season, while AppLovin demonstrated consistent quarter-over-quarter growth in Q1, breaking the typical industry seasonality pattern.

- Investor Considerations: For investors, AppLovin's robust sales growth positions it as a more attractive option in the digital advertising space, while The Trade Desk's stable growth, though positive, may not match AppLovin's expansion pace, potentially influencing investment decisions.

See More

AppLovin Reports Strong Q1 Growth, Stock Potential Looks Promising

- Significant Revenue Growth: AppLovin reported a remarkable 59% year-over-year revenue increase to $1.84 billion in Q1 2023, indicating the successful impact of its Axon 2.0 engine on business expansion and enhancing its competitive position in the market.

- Profitability Improvement: The adjusted EBITDA margin rose by 400 basis points to 85%, with earnings per share soaring 70% from $2.10 last year to $3.56, showcasing the company's strong performance in profitability.

- Cash Flow and Buybacks: The company generated $1.3 billion in free cash flow during the quarter and repurchased 2.2 million shares worth $1 billion, which not only enhances shareholder returns but also reflects confidence in future growth prospects.

- Optimistic Future Outlook: Management projected Q2 revenue to range between $1.915 billion and $1.945 billion, representing a growth rate of 52% to 55%, indicating that the company's strategic initiatives to expand market opportunities and broaden its advertising customer base will continue to drive growth.

See More