STAAR Surgical Reports 111% Revenue Growth in Q1

STAAR Surgical Co shares surged 27.27% after crossing above the 5-day SMA, reflecting strong investor confidence following the company's announcement of preliminary net sales exceeding $90 million for Q1 2026, which represents a remarkable 111% growth compared to the previous year.

The significant revenue growth was primarily driven by robust sales performance in China, which was highlighted by CFO Deborah Andrews, indicating strong market demand and product acceptance. This positive news led to heightened investor optimism, with shares jumping 19.25% in pre-market trading, showcasing the market's reaction to the company's strong fundamentals and improved inventory management.

The implications of this growth are substantial, as it not only reflects STAAR's successful market penetration but also positions the company favorably for future financial performance, potentially leading to further investor interest and confidence in the stock.

Trade with 70% Backtested Accuracy

Analyst Views on STAA

About STAA

About the author

Broadwood Capital Increases Stake in STAAR Surgical

- Increased Holdings: Broadwood Capital purchased 1,104,351 shares of STAAR Surgical in Q1 2026, amounting to approximately $21.08 million, indicating a bullish outlook as its stake rose to 21.25%.

- Valuation Fluctuation: Despite the increase in holdings, Broadwood's quarter-end position in STAAR decreased by $45.28 million, reflecting the impact of stock price volatility and the newly acquired shares, highlighting market uncertainties.

- Strong Performance: STAAR Surgical achieved record Q1 sales of $93.5 million in 2026, representing a massive 120% year-over-year increase, primarily driven by growth in the Chinese market, enhancing the company's competitive position globally.

- Surging Stock Price: As of May 14, 2026, STAAR's stock reached a 52-week high of $35.87, up 83.6% year-to-date, with a forward P/E ratio of 130, reflecting optimistic market expectations for its future growth.

Broadwood Capital Increases Stake in STAAR Surgical

- Increased Holdings: Broadwood Capital purchased an additional 1,104,351 shares of STAAR Surgical in Q1 2026, raising its total stake to 16,123,842 shares valued at $301.52 million, indicating a strong bullish outlook on the company.

- Capital Movement: The estimated transaction amount was approximately $21.08 million, and despite a $45.28 million decrease in the value of the fund's STAAR position due to stock price fluctuations at quarter-end, it reflects confidence in future growth.

- Strong Performance: STAAR Surgical reported record Q1 revenue of $93.5 million in fiscal 2026, representing a massive 120% year-over-year increase, with significant sales growth in the China market further solidifying its market position.

- Stock Surge: Following its impressive performance, STAAR Surgical's stock soared to a 52-week high of $35.87 on May 14, with a forward price-to-earnings ratio of 130, reflecting optimistic market expectations for its future growth.

Staar Surgical Q1 Results Exceed Expectations, Analysts Turn Bullish

- Strong Earnings Beat: Staar Surgical reported Q1 net sales of $93.5 million, surpassing Wall Street's expectations of $78.72 million, indicating robust performance amid market recovery and likely driving stock price appreciation.

- Analyst Upgrades: Wedbush upgraded Staar Surgical from 'Neutral' to 'Outperform' and raised its price target from $26 to $40, reflecting optimistic expectations for the company's future growth and potentially prompting a re-rating of its valuation.

- Recovery in China: The company noted that net sales in China were primarily driven by a recovery in market demand, positioning it favorably for growth in the upcoming quarters, suggesting that the company is at or near an inflection point for recovery.

- Improved Retail Sentiment: On Stocktwits, retail sentiment around Staar Surgical improved from 'Bullish' to 'Extremely Bullish', with message volume significantly increasing, indicating heightened investor confidence in the company's future performance.

STAAR Surgical Surges 10% After Massive Q1 Earnings Beat

- Earnings Beat: STAAR Surgical reported a Q1 non-GAAP EPS of $0.48, exceeding estimates by $0.40, with revenue soaring 119.5% year-over-year to $93.5 million, surpassing analyst expectations by $14.78 million, indicating robust market demand and recovery in profitability.

- China as Growth Driver: Sales from China reached $47.4 million, driven by strong demand for the newly launched EVO+ lenses, with management noting that distributor inventory is fully normalized, meaning growth is fueled by real customer demand rather than inventory restocking.

- Significant Profit Recovery: The company swung to a net income of $5.2 million from a loss of $54.2 million last year, with adjusted EBITDA at $24.4 million, showcasing strong margin recovery and operating leverage, which further boosts investor confidence.

- Optimistic Market Outlook: Although management did not provide full-year revenue guidance, they expect a strong Q2 and continue to target around 75% gross margin for FY26, with analysts raising STAAR's 12-month price targets from $26 to $40, reflecting optimistic market sentiment regarding future growth.

STAAR Surgical Surpasses Q1 2026 Expectations, Upgraded by Wedbush

- Significant Revenue Growth: STAAR Surgical reported $93.5 million in revenue for Q1 2026, achieving over 100% year-over-year growth and exceeding consensus estimates by $14.8 million, indicating a strong recovery in its Chinese operations and continued double-digit growth in the U.S.

- Analyst Rating Upgrade: Wedbush Securities upgraded STAAR's rating from Neutral to Outperform, reflecting confidence in the company's future performance, particularly in light of the recovery in the Chinese market, which is expected to drive continued growth in the upcoming quarters.

- Positive Management Outlook: Although the company declined to issue guidance again, management's positive remarks during the conference call suggest that STAAR is positioned to outperform initial analyst expectations, especially as it approaches the historically strong seasonal demand during China's summer peak in Q2/Q3.

- Price Target Increase: Analyst Michael Piccolo raised his price target on STAAR from $26 to $40, based on increased revenue estimates for FY26 and a reassessment of valuation multiples, reflecting an optimistic outlook on the company's growth potential moving forward.

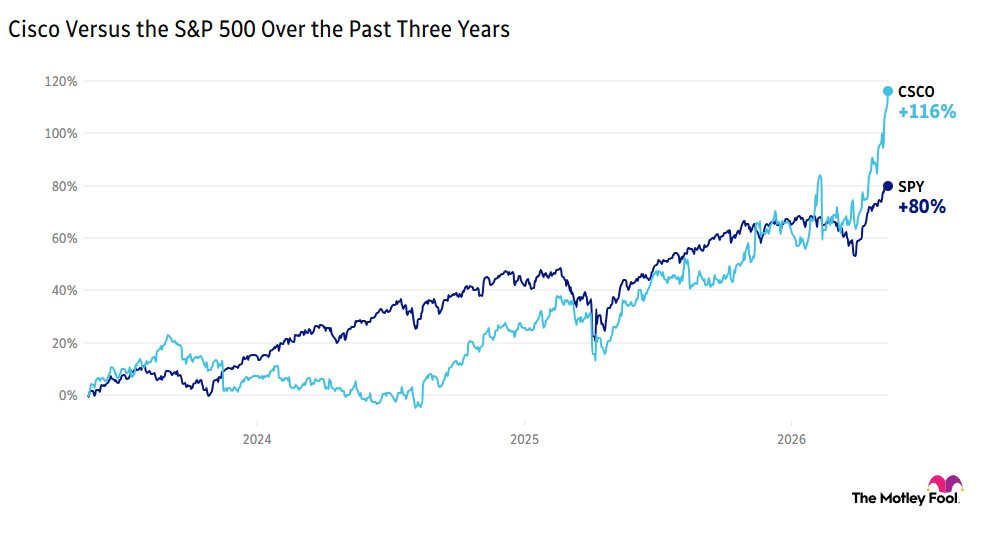

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

Broadwood Capital Increases Stake in STAAR Surgical

- Increased Holdings: Broadwood Capital purchased 1,104,351 shares of STAAR Surgical in Q1 2026, amounting to approximately $21.08 million, indicating a bullish outlook as its stake rose to 21.25%.

- Valuation Fluctuation: Despite the increase in holdings, Broadwood's quarter-end position in STAAR decreased by $45.28 million, reflecting the impact of stock price volatility and the newly acquired shares, highlighting market uncertainties.

- Strong Performance: STAAR Surgical achieved record Q1 sales of $93.5 million in 2026, representing a massive 120% year-over-year increase, primarily driven by growth in the Chinese market, enhancing the company's competitive position globally.

- Surging Stock Price: As of May 14, 2026, STAAR's stock reached a 52-week high of $35.87, up 83.6% year-to-date, with a forward P/E ratio of 130, reflecting optimistic market expectations for its future growth.

Broadwood Capital Increases Stake in STAAR Surgical

- Increased Holdings: Broadwood Capital purchased an additional 1,104,351 shares of STAAR Surgical in Q1 2026, raising its total stake to 16,123,842 shares valued at $301.52 million, indicating a strong bullish outlook on the company.

- Capital Movement: The estimated transaction amount was approximately $21.08 million, and despite a $45.28 million decrease in the value of the fund's STAAR position due to stock price fluctuations at quarter-end, it reflects confidence in future growth.

- Strong Performance: STAAR Surgical reported record Q1 revenue of $93.5 million in fiscal 2026, representing a massive 120% year-over-year increase, with significant sales growth in the China market further solidifying its market position.

- Stock Surge: Following its impressive performance, STAAR Surgical's stock soared to a 52-week high of $35.87 on May 14, with a forward price-to-earnings ratio of 130, reflecting optimistic market expectations for its future growth.

Staar Surgical Q1 Results Exceed Expectations, Analysts Turn Bullish

- Strong Earnings Beat: Staar Surgical reported Q1 net sales of $93.5 million, surpassing Wall Street's expectations of $78.72 million, indicating robust performance amid market recovery and likely driving stock price appreciation.

- Analyst Upgrades: Wedbush upgraded Staar Surgical from 'Neutral' to 'Outperform' and raised its price target from $26 to $40, reflecting optimistic expectations for the company's future growth and potentially prompting a re-rating of its valuation.

- Recovery in China: The company noted that net sales in China were primarily driven by a recovery in market demand, positioning it favorably for growth in the upcoming quarters, suggesting that the company is at or near an inflection point for recovery.

- Improved Retail Sentiment: On Stocktwits, retail sentiment around Staar Surgical improved from 'Bullish' to 'Extremely Bullish', with message volume significantly increasing, indicating heightened investor confidence in the company's future performance.

STAAR Surgical Surges 10% After Massive Q1 Earnings Beat

- Earnings Beat: STAAR Surgical reported a Q1 non-GAAP EPS of $0.48, exceeding estimates by $0.40, with revenue soaring 119.5% year-over-year to $93.5 million, surpassing analyst expectations by $14.78 million, indicating robust market demand and recovery in profitability.

- China as Growth Driver: Sales from China reached $47.4 million, driven by strong demand for the newly launched EVO+ lenses, with management noting that distributor inventory is fully normalized, meaning growth is fueled by real customer demand rather than inventory restocking.

- Significant Profit Recovery: The company swung to a net income of $5.2 million from a loss of $54.2 million last year, with adjusted EBITDA at $24.4 million, showcasing strong margin recovery and operating leverage, which further boosts investor confidence.

- Optimistic Market Outlook: Although management did not provide full-year revenue guidance, they expect a strong Q2 and continue to target around 75% gross margin for FY26, with analysts raising STAAR's 12-month price targets from $26 to $40, reflecting optimistic market sentiment regarding future growth.

STAAR Surgical Surpasses Q1 2026 Expectations, Upgraded by Wedbush

- Significant Revenue Growth: STAAR Surgical reported $93.5 million in revenue for Q1 2026, achieving over 100% year-over-year growth and exceeding consensus estimates by $14.8 million, indicating a strong recovery in its Chinese operations and continued double-digit growth in the U.S.

- Analyst Rating Upgrade: Wedbush Securities upgraded STAAR's rating from Neutral to Outperform, reflecting confidence in the company's future performance, particularly in light of the recovery in the Chinese market, which is expected to drive continued growth in the upcoming quarters.

- Positive Management Outlook: Although the company declined to issue guidance again, management's positive remarks during the conference call suggest that STAAR is positioned to outperform initial analyst expectations, especially as it approaches the historically strong seasonal demand during China's summer peak in Q2/Q3.

- Price Target Increase: Analyst Michael Piccolo raised his price target on STAAR from $26 to $40, based on increased revenue estimates for FY26 and a reassessment of valuation multiples, reflecting an optimistic outlook on the company's growth potential moving forward.

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.