Atlas Energy Solutions Signs $840 Million Agreement with Caterpillar

Atlas Energy Solutions Inc. shares rose by 6.21% as the company reached a 20-day high following the announcement of a significant Global Framework Agreement with Caterpillar. This agreement covers approximately 1.4 gigawatts of incremental power generation assets, with deliveries scheduled from 2027 to 2029, and includes a commitment of about $840 million in purchase obligations. CEO John Turner emphasized that the growing demand for private grid solutions driven by AI infrastructure and manufacturing reshoring presents multi-year growth opportunities for Atlas. The strategic partnership with Caterpillar is expected to enhance Atlas's competitive edge in the rapidly growing private grid market.

The agreement not only secures timely equipment delivery but also positions Atlas favorably in the market, addressing the increasing demand for electricity. This deal is a confirmed catalyst for the stock's rise, as it solidifies Atlas's operational capacity and market presence. Investors are likely to view this positively, potentially leading to further interest in the stock as it aligns with the company's growth strategy.

Overall, the signing of this agreement marks a significant milestone for Atlas Energy Solutions, enhancing its capabilities and positioning in the energy sector, which could lead to sustained growth in the coming years.

Trade with 70% Backtested Accuracy

Analyst Views on AESI

About AESI

About the author

ATLAS ENERGY SOLUTIONS: BARCLAYS INCREASES TARGET PRICE FROM $12 TO $16

Barclays Raises Price Target: Barclays has increased its price target for Atlas Energy Solutions to $16 from a previous target of $12.

Market Implications: This adjustment reflects Barclays' positive outlook on Atlas Energy Solutions and may influence investor sentiment and market performance.

Atlas Energy (AESI) Q1 2026 Earnings Transcript

Atlas Energy Q1 Earnings: Revenue Beats Expectations

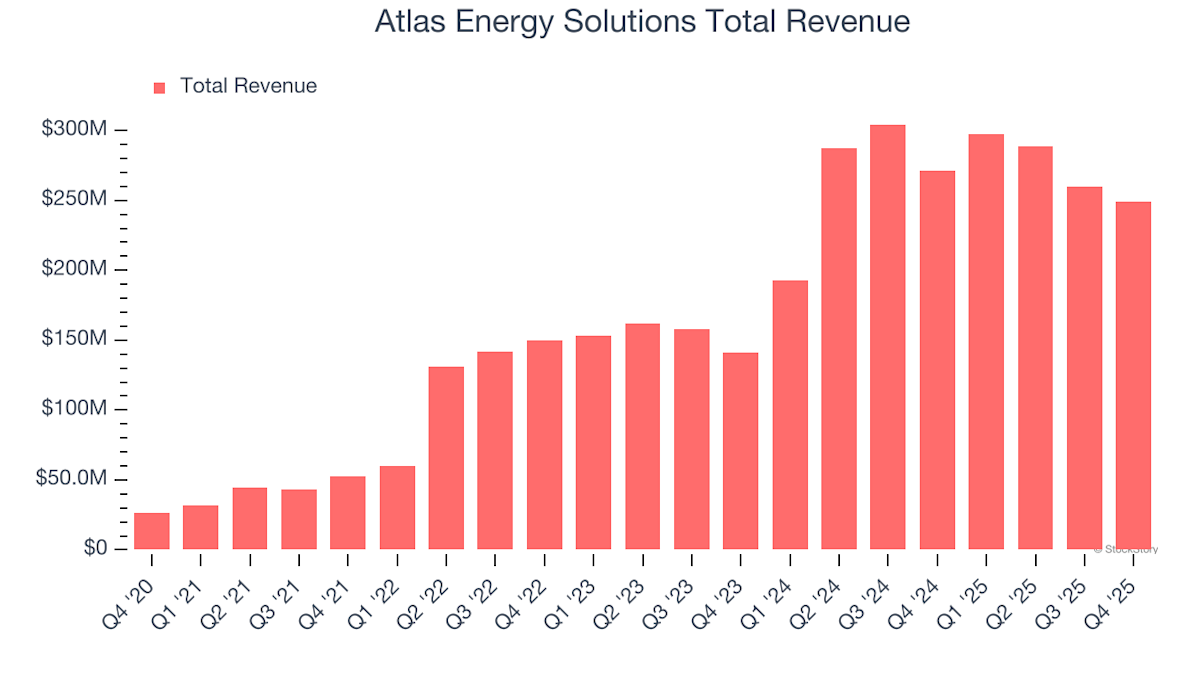

- Earnings Performance: Atlas Energy Solutions reported a Q1 GAAP EPS of -$0.38, missing expectations by $0.12, indicating challenges in profitability, although revenue of $265.5 million, down 10.8% year-over-year, exceeded expectations by $9.39 million, reflecting market demand fluctuations.

- Rising Expenses: Selling, general, and administrative expenses increased by $2 million in Q1 compared to Q4 2025, reaching $35.7 million or 5.9% of total revenue, indicating pressure on the company’s cost control, which may impact future profitability.

- Liquidity Position: As of March 31, 2026, the company’s total liquidity stood at $89.5 million, comprising $39.8 million in cash and cash equivalents and $49.7 million available under the 2023 ABL Credit Facility, demonstrating relative stability in cash management but necessitating attention to future capital expenditures.

- Future Guidance: The company provided financial guidance for Q2 2026, based on current market outlook and plans, but due to various known and unknown uncertainties, actual results may differ materially from the guidance, reflecting the complexities of the market environment.

ATLAS ENERGY SOLUTIONS REPORTS Q1 SALES OF USD 265.583 MILLION, BEATING IBES ESTIMATE OF USD 258.3 MILLION

- Sales Performance: Atlas Energy Solutions reported Q1 sales of USD 265.58 million.

- Comparison with Estimates: This figure exceeds the Ibes estimate of USD 258.3 million.

Atlas Energy Solutions Earnings Preview

- Earnings Expectations: Atlas Energy Solutions is set to report earnings after the bell on Monday, with market expectations indicating a 13.8% year-over-year revenue decline, contrasting sharply with last year's 54.5% growth, highlighting increased industry volatility.

- Last Quarter Performance: The company reported revenues of $249.4 million last quarter, down 8.1% year-over-year, yet it exceeded analysts' EBITDA estimates, indicating resilience in profitability amidst challenges.

- Market Sentiment: Investor sentiment in the oilfield services sector has been positive, with average share prices rising 4.1% over the past month, while Atlas Energy Solutions saw a remarkable 55.4% increase during the same period, reflecting strong market confidence in its future performance.

- Analyst Outlook: Despite missing Wall Street's revenue estimates multiple times over the past two years, most analysts have reaffirmed their expectations in the last 30 days, with an average price target of $15.36 compared to the current share price of $17.34, suggesting optimism about its future.

Atlas Energy Solutions Set to Announce Q1 Earnings on May 4th

- Earnings Announcement: Atlas Energy Solutions (AESI) is set to release its Q1 2023 earnings on May 4th after market close, with consensus EPS estimates at -$0.21, reflecting a staggering 2200% year-over-year decline, indicating significant profitability challenges for the company.

- Revenue Decline: The anticipated revenue for Q1 is $256.11 million, representing a 13.9% year-over-year decrease, which highlights the company's struggles in the current market environment and may impact its future investment appeal.

- Estimate Revisions: Over the past three months, EPS estimates have seen no upward revisions and two downward adjustments, while revenue estimates experienced two upward revisions and seven downward adjustments, reflecting a pessimistic outlook from the market regarding the company's performance.

- Market Rating Changes: Despite financial challenges, Citi has upgraded Atlas Energy Solutions to a “Buy” rating, suggesting that there is optimism in the market regarding the company's potential improvements in the Permian completion market.

ATLAS ENERGY SOLUTIONS: BARCLAYS INCREASES TARGET PRICE FROM $12 TO $16

Barclays Raises Price Target: Barclays has increased its price target for Atlas Energy Solutions to $16 from a previous target of $12.

Market Implications: This adjustment reflects Barclays' positive outlook on Atlas Energy Solutions and may influence investor sentiment and market performance.

Atlas Energy (AESI) Q1 2026 Earnings Transcript

Atlas Energy Q1 Earnings: Revenue Beats Expectations

- Earnings Performance: Atlas Energy Solutions reported a Q1 GAAP EPS of -$0.38, missing expectations by $0.12, indicating challenges in profitability, although revenue of $265.5 million, down 10.8% year-over-year, exceeded expectations by $9.39 million, reflecting market demand fluctuations.

- Rising Expenses: Selling, general, and administrative expenses increased by $2 million in Q1 compared to Q4 2025, reaching $35.7 million or 5.9% of total revenue, indicating pressure on the company’s cost control, which may impact future profitability.

- Liquidity Position: As of March 31, 2026, the company’s total liquidity stood at $89.5 million, comprising $39.8 million in cash and cash equivalents and $49.7 million available under the 2023 ABL Credit Facility, demonstrating relative stability in cash management but necessitating attention to future capital expenditures.

- Future Guidance: The company provided financial guidance for Q2 2026, based on current market outlook and plans, but due to various known and unknown uncertainties, actual results may differ materially from the guidance, reflecting the complexities of the market environment.

ATLAS ENERGY SOLUTIONS REPORTS Q1 SALES OF USD 265.583 MILLION, BEATING IBES ESTIMATE OF USD 258.3 MILLION

- Sales Performance: Atlas Energy Solutions reported Q1 sales of USD 265.58 million.

- Comparison with Estimates: This figure exceeds the Ibes estimate of USD 258.3 million.

Atlas Energy Solutions Earnings Preview

- Earnings Expectations: Atlas Energy Solutions is set to report earnings after the bell on Monday, with market expectations indicating a 13.8% year-over-year revenue decline, contrasting sharply with last year's 54.5% growth, highlighting increased industry volatility.

- Last Quarter Performance: The company reported revenues of $249.4 million last quarter, down 8.1% year-over-year, yet it exceeded analysts' EBITDA estimates, indicating resilience in profitability amidst challenges.

- Market Sentiment: Investor sentiment in the oilfield services sector has been positive, with average share prices rising 4.1% over the past month, while Atlas Energy Solutions saw a remarkable 55.4% increase during the same period, reflecting strong market confidence in its future performance.

- Analyst Outlook: Despite missing Wall Street's revenue estimates multiple times over the past two years, most analysts have reaffirmed their expectations in the last 30 days, with an average price target of $15.36 compared to the current share price of $17.34, suggesting optimism about its future.

Atlas Energy Solutions Set to Announce Q1 Earnings on May 4th

- Earnings Announcement: Atlas Energy Solutions (AESI) is set to release its Q1 2023 earnings on May 4th after market close, with consensus EPS estimates at -$0.21, reflecting a staggering 2200% year-over-year decline, indicating significant profitability challenges for the company.

- Revenue Decline: The anticipated revenue for Q1 is $256.11 million, representing a 13.9% year-over-year decrease, which highlights the company's struggles in the current market environment and may impact its future investment appeal.

- Estimate Revisions: Over the past three months, EPS estimates have seen no upward revisions and two downward adjustments, while revenue estimates experienced two upward revisions and seven downward adjustments, reflecting a pessimistic outlook from the market regarding the company's performance.

- Market Rating Changes: Despite financial challenges, Citi has upgraded Atlas Energy Solutions to a “Buy” rating, suggesting that there is optimism in the market regarding the company's potential improvements in the Permian completion market.