Synopsys & Vector Team Up To Supercharge Software-Defined Vehicles

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 10 2025

0mins

Source: Benzinga

Partnership Announcement: Synopsys, Inc. has formed a strategic partnership with Vector Informatik to enhance the development of software-defined vehicles (SDVs), focusing on cost reduction, improved software quality, and accelerating deployment through integrated tools and open-source enhancements.

Financial Update: Despite reporting first-quarter earnings per share that exceeded estimates, Synopsys' revenue of $1.455 billion fell short of expectations, leading to a slight decline in stock price prior to market opening.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SNPS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SNPS

Wall Street analysts forecast SNPS stock price to rise

12 Analyst Rating

10 Buy

2 Hold

0 Sell

Strong Buy

Current: 442.270

Low

500.00

Averages

565.64

High

602.00

Current: 442.270

Low

500.00

Averages

565.64

High

602.00

About SNPS

Synopsys, Inc. is engaged in providing engineering solutions from silicon to systems, enabling customers to innovate artificial intelligence (AI)-powered products. It delivers silicon design, intellectual property (IP), simulation and analysis solutions, and design services. It supplies mission-critical electronic design automation (EDA) software that engineers use to design and test integrated circuits (ICs). Its Design Automation segment includes its silicon design, verification products and services, Ansys products, system integration products and services, digital, custom and field programmable gate array integrated circuit design software, verification software and hardware products, manufacturing software products and others. Its Design IP segment's portfolio includes logic libraries, embedded memories, interface IP, security IP, and subsystems that serve companies in the semiconductor and electronics industries.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

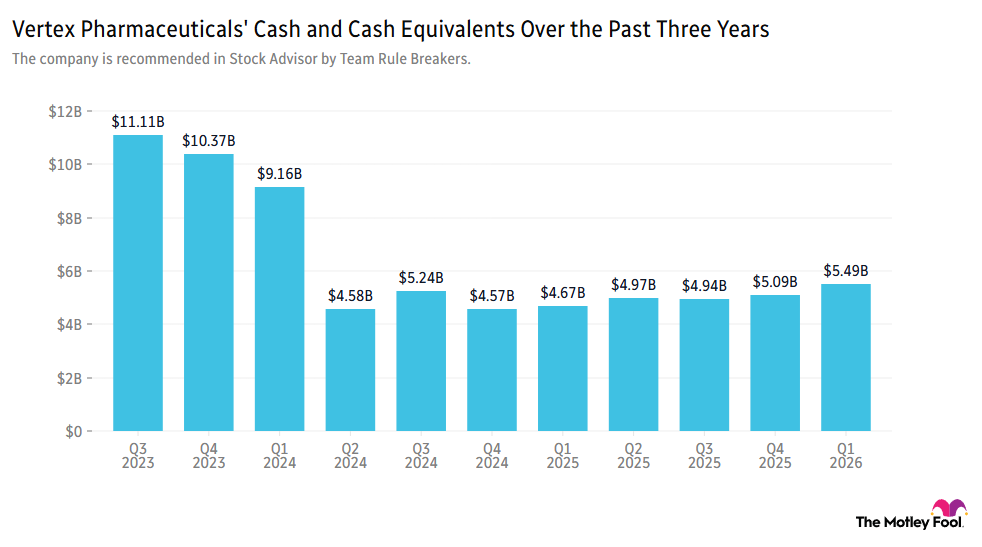

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Synopsys Discontinues Manufacturing Software to Focus on AI Design

- Software Discontinuation Notice: Synopsys has informed over 10 chipmakers, including Samsung and SK Hynix, about the decision to cease updates and support for a suite of manufacturing process control software, which is expected to impact production efficiency.

- Resource Reallocation: The company is reallocating resources to higher-margin AI design products, although this move may lead to insufficient maintenance and updates for production tools, potentially affecting production yields.

- Layoff Impact: The layoffs associated with the software discontinuation have involved several dozen employees, highlighting the company's focus on cost control during its transition while also reflecting a reduction in its traditional product lines.

- Customer Reactions: While some customers like Samsung have developed alternative tools and stated there will be no negative impact on production, concerns remain regarding the potential production risks associated with the discontinuation of the software.

See More

Synopsys Upgraded to Overweight by Piper Sandler

- Rating Upgrade: Piper Sandler upgraded Synopsys, Inc. (NASDAQ:SNPS) from Neutral to Overweight, raising the price target from $450 to $550, reflecting optimism about the recovery of its intellectual property business.

- Customer Demand Recovery: Analyst Clarke Jeffries noted that Intel's 18A-P manufacturing node is seen as a practical alternative to constrained TSMC capacity, which is expected to accelerate the recovery of intellectual property demand at Synopsys' largest customer, Intel.

- Board Changes: Synopsys reached a settlement with Elliott Investment Management, appointing managing partner Jesse Cohn to its board and expanding the board to 11 members, indicating proactive adjustments in corporate governance.

- AI Investment Outlook: Cohn stated that Synopsys is moving in a direction to benefit from rising AI investments and growing engineering complexity, although analysts believe certain AI stocks offer greater upside potential and less downside risk.

See More

Major Rating Changes on Wall Street

- IBM Upgrade: JPMorgan upgraded IBM from Neutral to Overweight, citing a deeper analysis of its software business that suggests significant performance acceleration in 2H'26, thereby enhancing market confidence in the company's growth trajectory.

- Qiagen Upgrade: Morgan Stanley upgraded Qiagen from Equal Weight to Overweight, noting that AI-driven growth improvements and the clearing of competitive risks are expected to positively impact the life sciences sector.

- Smurfit Westrock Initiation: Deutsche Bank initiated coverage of Smurfit Westrock with a Buy rating and a $57 price target, emphasizing its high-margin operations and strong market position as catalysts for value creation in the packaging industry.

- Target Upgrade: Wolfe upgraded Target from Peer Perform to Outperform, stating that now is the optimal time to buy, as the company is poised for significant improvements driven by store resets and a new leadership team shaking up the status quo.

See More

Synopsys Launches New Multiphysics Fusion Platform for AI Chip Design

- Platform Launch: Synopsys announced the launch of its new Multiphysics Fusion platform on June 17, combining AI-powered chip design tools with Ansys analysis technology to expedite the development of advanced AI chips, enhancing market competitiveness.

- Performance Boost: The platform delivers up to 3x faster timing signoff and 10x faster design closure, with early users like MediaTek reporting runtimes that are 10 times faster than before, indicating significant efficiency gains.

- Customer Validation: The technology has been validated by companies such as NVIDIA, Samsung Electronics, MediaTek, and Cisco, with NVIDIA's pilot designs achieving up to 5x faster design closure and 86% IR fix rates, demonstrating its effectiveness in real-world applications.

- Market Impact: Although Synopsys stock is currently trading slightly lower at around $458.61, the launch of the new platform could serve as a positive catalyst, especially if customer adoption and AI semiconductor spending remain strong.

See More

Synopsys Launches Multiphysics Fusion Solutions for Advanced Chip Design

- Technological Innovation: Synopsys' newly launched Multiphysics Fusion™ solutions integrate multiphysics analysis directly into design workflows, enabling earlier and more accurate design decisions, thereby enhancing efficiency and reliability in chip design.

- Performance Enhancement: The solutions achieve up to 3x faster runtimes and deliver up to 10x faster design closure, significantly improving engineering change order success rates while optimizing power, performance, and area metrics.

- Market Validation: Leading semiconductor firms like MediaTek and NVIDIA have validated the value of this technology, with MediaTek noting that unified multiphysics analysis allows for earlier insights into cross-domain interactions, reducing late-stage rework and enhancing design predictability.

- Industry Impact: Companies such as Samsung and Cisco are leveraging this technology to optimize their design closure processes, ensuring accurate timing signoff at advanced nodes, which further accelerates the design of high-performance computing platforms.

See More

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Synopsys Discontinues Manufacturing Software to Focus on AI Design

- Software Discontinuation Notice: Synopsys has informed over 10 chipmakers, including Samsung and SK Hynix, about the decision to cease updates and support for a suite of manufacturing process control software, which is expected to impact production efficiency.

- Resource Reallocation: The company is reallocating resources to higher-margin AI design products, although this move may lead to insufficient maintenance and updates for production tools, potentially affecting production yields.

- Layoff Impact: The layoffs associated with the software discontinuation have involved several dozen employees, highlighting the company's focus on cost control during its transition while also reflecting a reduction in its traditional product lines.

- Customer Reactions: While some customers like Samsung have developed alternative tools and stated there will be no negative impact on production, concerns remain regarding the potential production risks associated with the discontinuation of the software.

See More

Synopsys Upgraded to Overweight by Piper Sandler

- Rating Upgrade: Piper Sandler upgraded Synopsys, Inc. (NASDAQ:SNPS) from Neutral to Overweight, raising the price target from $450 to $550, reflecting optimism about the recovery of its intellectual property business.

- Customer Demand Recovery: Analyst Clarke Jeffries noted that Intel's 18A-P manufacturing node is seen as a practical alternative to constrained TSMC capacity, which is expected to accelerate the recovery of intellectual property demand at Synopsys' largest customer, Intel.

- Board Changes: Synopsys reached a settlement with Elliott Investment Management, appointing managing partner Jesse Cohn to its board and expanding the board to 11 members, indicating proactive adjustments in corporate governance.

- AI Investment Outlook: Cohn stated that Synopsys is moving in a direction to benefit from rising AI investments and growing engineering complexity, although analysts believe certain AI stocks offer greater upside potential and less downside risk.

See More

Major Rating Changes on Wall Street

- IBM Upgrade: JPMorgan upgraded IBM from Neutral to Overweight, citing a deeper analysis of its software business that suggests significant performance acceleration in 2H'26, thereby enhancing market confidence in the company's growth trajectory.

- Qiagen Upgrade: Morgan Stanley upgraded Qiagen from Equal Weight to Overweight, noting that AI-driven growth improvements and the clearing of competitive risks are expected to positively impact the life sciences sector.

- Smurfit Westrock Initiation: Deutsche Bank initiated coverage of Smurfit Westrock with a Buy rating and a $57 price target, emphasizing its high-margin operations and strong market position as catalysts for value creation in the packaging industry.

- Target Upgrade: Wolfe upgraded Target from Peer Perform to Outperform, stating that now is the optimal time to buy, as the company is poised for significant improvements driven by store resets and a new leadership team shaking up the status quo.

See More

Synopsys Launches New Multiphysics Fusion Platform for AI Chip Design

- Platform Launch: Synopsys announced the launch of its new Multiphysics Fusion platform on June 17, combining AI-powered chip design tools with Ansys analysis technology to expedite the development of advanced AI chips, enhancing market competitiveness.

- Performance Boost: The platform delivers up to 3x faster timing signoff and 10x faster design closure, with early users like MediaTek reporting runtimes that are 10 times faster than before, indicating significant efficiency gains.

- Customer Validation: The technology has been validated by companies such as NVIDIA, Samsung Electronics, MediaTek, and Cisco, with NVIDIA's pilot designs achieving up to 5x faster design closure and 86% IR fix rates, demonstrating its effectiveness in real-world applications.

- Market Impact: Although Synopsys stock is currently trading slightly lower at around $458.61, the launch of the new platform could serve as a positive catalyst, especially if customer adoption and AI semiconductor spending remain strong.

See More

Synopsys Launches Multiphysics Fusion Solutions for Advanced Chip Design

- Technological Innovation: Synopsys' newly launched Multiphysics Fusion™ solutions integrate multiphysics analysis directly into design workflows, enabling earlier and more accurate design decisions, thereby enhancing efficiency and reliability in chip design.

- Performance Enhancement: The solutions achieve up to 3x faster runtimes and deliver up to 10x faster design closure, significantly improving engineering change order success rates while optimizing power, performance, and area metrics.

- Market Validation: Leading semiconductor firms like MediaTek and NVIDIA have validated the value of this technology, with MediaTek noting that unified multiphysics analysis allows for earlier insights into cross-domain interactions, reducing late-stage rework and enhancing design predictability.

- Industry Impact: Companies such as Samsung and Cisco are leveraging this technology to optimize their design closure processes, ensuring accurate timing signoff at advanced nodes, which further accelerates the design of high-performance computing platforms.

See More