PennyMac's $390.2 Million Mortgage Trust Receives Preliminary Ratings from KBRA

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 07 2026

0mins

Source: Businesswire

- Credit Rating Assignment: KBRA has assigned preliminary ratings to 57 classes of mortgage-backed securities from PennyMac Corp.'s PMT Loan Trust 2026-INV1, involving a total of $390.2 million in fixed-rate mortgages, indicating market confidence in the transaction.

- Loan Pool Characteristics: The trust comprises 1,032 mortgages, with 72.6% being investment properties and 27.4% second homes, reflecting a diversified asset base that helps mitigate risk.

- Borrower Credit Quality: The pool's weighted average original loan-to-value (LTV) ratio stands at 74.6%, while the weighted average credit score is 779, both within the prime mortgage range, demonstrating strong borrower repayment capacity.

- Rating Methodology: KBRA utilized its Residential Asset Loss Model (REALM) for loan-level analysis of the mortgage pool, supplemented by third-party due diligence results and cash flow modeling analysis, ensuring the accuracy and reliability of the ratings.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PMT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PMT

Wall Street analysts forecast PMT stock price to rise

7 Analyst Rating

1 Buy

6 Hold

0 Sell

Hold

Current: 10.370

Low

13.00

Averages

13.85

High

14.50

Current: 10.370

Low

13.00

Averages

13.85

High

14.50

About PMT

PennyMac Mortgage Investment Trust is a mortgage real estate investment trust (REIT) that invests primarily in residential mortgage loans and mortgage-related assets. The Company's segments include credit sensitive strategies, interest rate sensitive strategies and correspondent production. The credit sensitive strategies segment represents its investments in CRT arrangements referencing loans from its own correspondent production and subordinate MBS. The interest rate sensitive strategies segment represents its investments in MSRs, Agency and senior non-Agency MBS and the related interest rate hedging activities. The correspondent production segment represents its operations aimed at serving as an intermediary between lenders and the capital markets by purchasing, pooling and reselling newly originated prime credit quality loans either directly or in the form of MBS, using the services of PCM and PLS. The Company is externally managed by PNMAC Capital Management, LLC.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Banking Sector Faces Challenges Amid Rising Rates

- Industry Growth Challenges: While the banking sector has seen a 10.6% gain over the past six months, Fulton Financial's annual revenue growth of only 8.9% indicates a lag in market demand compared to peers, potentially impacting its long-term profitability.

- Declining Profitability: PennyMac Mortgage Investment Trust has experienced a 23.1% decline in annual sales over the past five years, with earnings per share decreasing more than revenue, suggesting its products struggle to compete in the market, which may weaken investor confidence.

- Soft Capital Generation: Wells Fargo's net interest income growth of 5.1% has fallen short of other banks, and its net interest margin has shrunk by 38.7 basis points over the last two years, indicating a decline in loan profitability and potential challenges in future capital generation.

- Valuation Risks: Fulton Financial and PennyMac Mortgage Investment Trust have forward P/B ratios of 1.1x and 0.7x respectively, reflecting market caution regarding their future growth prospects, which could influence investor decision-making.

See More

Analysis of Risks and Opportunities in Small-Cap Investments

- Clarus Performance Stagnation: Clarus (CLAR) has seen flat sales over the past five years, indicating its failure to effectively expand operations, and declining earnings raise concerns about its long-term growth sustainability; with a current stock price of $2.92, its price-to-sales ratio stands at a mere 0.4x, reflecting market pessimism about its future prospects.

- Custom Truck Integration Challenges: Custom Truck One Source (CTOS) has only achieved an annual growth rate of 4.3% over the past two years, significantly below industry standards, and its earnings per share have plummeted by 45.4% annually, leading to investor doubts about its ability to sustainably generate shareholder value; trading at $10.25 per share, it carries a high price-to-earnings ratio of 59x, raising concerns about its profitability.

- PennyMac Performance Decline: PennyMac Mortgage Investment Trust (PMT) has experienced a 23.1% annual decline in sales over the past five years, with earnings per share decreasing more than revenue, indicating worsening profitability; currently priced at $10.55 per share, it trades at 0.7x price-to-book ratio, highlighting increasing market challenges.

- Risks of Small-Cap Investments: Small-cap stocks often suffer from mispricing due to a lack of analyst coverage, and while potential returns can be significant, the financial performances of companies like Clarus, CTOS, and PMT illustrate the difficulties in expanding competitive advantages, prompting investors to carefully assess risks versus rewards.

See More

PennyMac (PMT) Q1 2026 Earnings Transcript

See More

PennyMac Mortgage Investment Trust Q1 2026 Earnings Insights

- Net Income Performance: PennyMac reported a net income of $14 million for Q1 2026, translating to $0.16 per diluted share, with a 4% annualized return on common equity, indicating that profitability was impacted by seasonal factors and a larger-than-expected runoff of mortgage servicing rights (MSRs).

- Dividend Maintenance: The company plans to maintain its quarterly dividend at $0.40 per share, supported by taxable income, although management acknowledged that earnings have fallen below the dividend level in recent quarters, reflecting pressure from market-driven value changes.

- Securitization Progress: In Q1, PennyMac completed eight private-label securitizations totaling $2.8 billion in UPB, with expectations to complete approximately 30 securitizations in 2026, aimed at building a solid investment foundation to support future earnings.

- Asset Allocation Strategy: Management is strategically evaluating the MSR portfolio to shift capital away from lower-returning assets, with potential plans for a non-QM securitization within the next year to mitigate market volatility and enhance returns.

See More

PennyMac to Announce Q1 Earnings on May 5

- Earnings Announcement Schedule: PennyMac Mortgage Investment Trust is set to release its Q1 2023 earnings report on May 5 after market close, with consensus estimates predicting an EPS of $0.39 and revenue of $92.92 million, indicating significant market interest in its financial performance.

- Earnings Estimate Changes: Over the past three months, EPS estimates have seen one upward revision and four downward adjustments, while revenue estimates have not experienced any upward revisions and have faced three downward changes, suggesting a decline in analyst confidence regarding the company's future performance.

- Risk Assessment: Despite the downward revisions in earnings expectations, analysts believe that the risks associated with PennyMac are not as high as they may appear, likely due to the company's stability in the mortgage market and its historical performance.

- Historical Financial Data: The historical earnings data and dividend scorecard for PennyMac Mortgage Investment Trust demonstrate its ongoing performance in the market, allowing investors to assess its future investment value based on these metrics.

See More

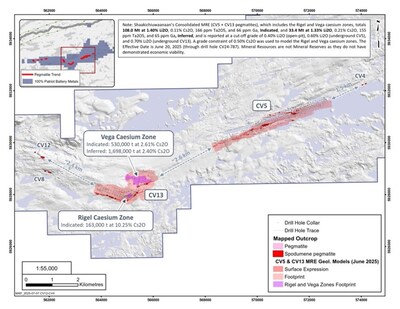

PMET Partners with Koch Technology Solutions to Develop Caesium Chemicals

- Strategic Partnership Initiated: PMET has launched a strategic testwork program with Koch Technology Solutions to convert Shaakichiuwaanaan caesium concentrates into high-value caesium chemical products, which is expected to support supply chains for critical industries such as defense, aerospace, and energy in the U.S.

- Significant Resource Potential: The Shaakichiuwaanaan project hosts the world's largest caesium resource, with 0.69 Mt at 4.40% Cs2O and 1.70 Mt at 2.40% Cs2O, establishing a strong foundation for PMET's leadership in the caesium market.

- Innovative Technology Application: Koch Technology Solutions will leverage its proprietary caesium chemical production techniques to drive efficient extraction, with pathways for producing various value-added caesium chemicals expected to be developed over the next four months, enhancing PMET's market competitiveness.

- Broad Market Prospects: Through collaboration with Koch, PMET aims to not only enhance the commercial value of its caesium resources but also explore applications of caesium chemicals in the emerging solar panel industry, further expanding market opportunities.

See More

Banking Sector Faces Challenges Amid Rising Rates

- Industry Growth Challenges: While the banking sector has seen a 10.6% gain over the past six months, Fulton Financial's annual revenue growth of only 8.9% indicates a lag in market demand compared to peers, potentially impacting its long-term profitability.

- Declining Profitability: PennyMac Mortgage Investment Trust has experienced a 23.1% decline in annual sales over the past five years, with earnings per share decreasing more than revenue, suggesting its products struggle to compete in the market, which may weaken investor confidence.

- Soft Capital Generation: Wells Fargo's net interest income growth of 5.1% has fallen short of other banks, and its net interest margin has shrunk by 38.7 basis points over the last two years, indicating a decline in loan profitability and potential challenges in future capital generation.

- Valuation Risks: Fulton Financial and PennyMac Mortgage Investment Trust have forward P/B ratios of 1.1x and 0.7x respectively, reflecting market caution regarding their future growth prospects, which could influence investor decision-making.

See More

Analysis of Risks and Opportunities in Small-Cap Investments

- Clarus Performance Stagnation: Clarus (CLAR) has seen flat sales over the past five years, indicating its failure to effectively expand operations, and declining earnings raise concerns about its long-term growth sustainability; with a current stock price of $2.92, its price-to-sales ratio stands at a mere 0.4x, reflecting market pessimism about its future prospects.

- Custom Truck Integration Challenges: Custom Truck One Source (CTOS) has only achieved an annual growth rate of 4.3% over the past two years, significantly below industry standards, and its earnings per share have plummeted by 45.4% annually, leading to investor doubts about its ability to sustainably generate shareholder value; trading at $10.25 per share, it carries a high price-to-earnings ratio of 59x, raising concerns about its profitability.

- PennyMac Performance Decline: PennyMac Mortgage Investment Trust (PMT) has experienced a 23.1% annual decline in sales over the past five years, with earnings per share decreasing more than revenue, indicating worsening profitability; currently priced at $10.55 per share, it trades at 0.7x price-to-book ratio, highlighting increasing market challenges.

- Risks of Small-Cap Investments: Small-cap stocks often suffer from mispricing due to a lack of analyst coverage, and while potential returns can be significant, the financial performances of companies like Clarus, CTOS, and PMT illustrate the difficulties in expanding competitive advantages, prompting investors to carefully assess risks versus rewards.

See More

PennyMac (PMT) Q1 2026 Earnings Transcript

See More

PennyMac Mortgage Investment Trust Q1 2026 Earnings Insights

- Net Income Performance: PennyMac reported a net income of $14 million for Q1 2026, translating to $0.16 per diluted share, with a 4% annualized return on common equity, indicating that profitability was impacted by seasonal factors and a larger-than-expected runoff of mortgage servicing rights (MSRs).

- Dividend Maintenance: The company plans to maintain its quarterly dividend at $0.40 per share, supported by taxable income, although management acknowledged that earnings have fallen below the dividend level in recent quarters, reflecting pressure from market-driven value changes.

- Securitization Progress: In Q1, PennyMac completed eight private-label securitizations totaling $2.8 billion in UPB, with expectations to complete approximately 30 securitizations in 2026, aimed at building a solid investment foundation to support future earnings.

- Asset Allocation Strategy: Management is strategically evaluating the MSR portfolio to shift capital away from lower-returning assets, with potential plans for a non-QM securitization within the next year to mitigate market volatility and enhance returns.

See More

PennyMac to Announce Q1 Earnings on May 5

- Earnings Announcement Schedule: PennyMac Mortgage Investment Trust is set to release its Q1 2023 earnings report on May 5 after market close, with consensus estimates predicting an EPS of $0.39 and revenue of $92.92 million, indicating significant market interest in its financial performance.

- Earnings Estimate Changes: Over the past three months, EPS estimates have seen one upward revision and four downward adjustments, while revenue estimates have not experienced any upward revisions and have faced three downward changes, suggesting a decline in analyst confidence regarding the company's future performance.

- Risk Assessment: Despite the downward revisions in earnings expectations, analysts believe that the risks associated with PennyMac are not as high as they may appear, likely due to the company's stability in the mortgage market and its historical performance.

- Historical Financial Data: The historical earnings data and dividend scorecard for PennyMac Mortgage Investment Trust demonstrate its ongoing performance in the market, allowing investors to assess its future investment value based on these metrics.

See More

PMET Partners with Koch Technology Solutions to Develop Caesium Chemicals

- Strategic Partnership Initiated: PMET has launched a strategic testwork program with Koch Technology Solutions to convert Shaakichiuwaanaan caesium concentrates into high-value caesium chemical products, which is expected to support supply chains for critical industries such as defense, aerospace, and energy in the U.S.

- Significant Resource Potential: The Shaakichiuwaanaan project hosts the world's largest caesium resource, with 0.69 Mt at 4.40% Cs2O and 1.70 Mt at 2.40% Cs2O, establishing a strong foundation for PMET's leadership in the caesium market.

- Innovative Technology Application: Koch Technology Solutions will leverage its proprietary caesium chemical production techniques to drive efficient extraction, with pathways for producing various value-added caesium chemicals expected to be developed over the next four months, enhancing PMET's market competitiveness.

- Broad Market Prospects: Through collaboration with Koch, PMET aims to not only enhance the commercial value of its caesium resources but also explore applications of caesium chemicals in the emerging solar panel industry, further expanding market opportunities.

See More